Examining Donald Trump’s Statements Today on Taxes

Today’s speech by Republican presidential nominee Donald Trump included several statements on tax issues that could create mistaken impressions regarding current tax policies and the impact of several of Mr. Trump’s proposals. This brief report, based on prior CBPP analysis, provides some context on four of those issues.

Top Income Tax Rate

Mr. Trump said today that he would set the top individual income-tax rate at 33 percent; his prior plan had a top rate of 25 percent. However, his plan would create a much lower rate than 33 percent for a substantial number of very-high-income households by allowing people to pay a new low rate of 15 percent on “pass-through” income (business income claimed on individual tax returns). More than two-thirds of all pass-through business income flows to the top 1 percent of tax filers.

This new tax break would encourage many wealthy filers to reclassify a greater share of their income as pass-through income in order to take advantage of this much lower rate. As our recent analysis of this issue explains:[1]

History suggests that slashing the top rate on pass-through income to far below the top income and payroll tax rate, which applies to salary and wages, also would spur large-scale tax avoidance by expanding the incentive for high-income professionals to classify their income as business income instead of salary and wages. When, for instance, Kansas exempted all pass-through income from taxes, the state watched the number of pass-through entities grow by many thousands.

This large tax cut for pass-through income would also undercut another tax change Mr. Trump mentioned today: eliminating the tax break for “carried interest.” Under current law, investment fund managers can pay taxes on a large part of their income — their “carried interest,” or the right to a share of their fund’s profits — at the 23.8 percent top capital gains tax rate[2] rather than at normal income tax rates of up to 39.6 percent. The Trump plan ostensibly would tax carried interest at ordinary income tax rates. In fact, however, these investment fund managers generally would be able to arrange to receive their income as pass-through income. As a result, rather than these fund managers paying a higher rate of tax on these often lucrative earnings, their carried interest would, as the Urban-Brookings Tax Policy Center (TPC) has noted, “be taxed at a top rate of 15 percent, a reduction of more than one-third.”[3] In short, the Trump plan would replace one tax break for hedge fund managers (on carried interest) with an even larger one (on pass-through income).

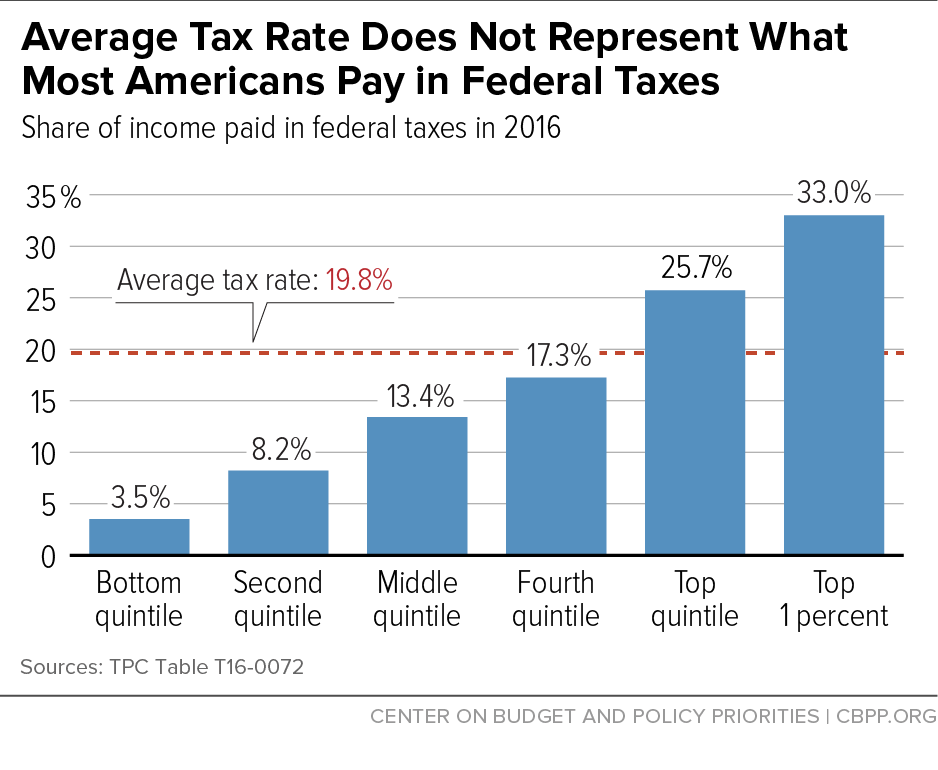

Average Tax Rate

Mr. Trump stated that “[t]he average worker today pays 31.5 percent of their wages to income and payroll taxes.” This figure, however, creates a distorted impression about the federal taxes that most Americans pay. Indeed, TPC estimates that this figure is closer to the average rate paid by the top 1 percent — not the typical filer (see Figure 1).

TPC not only estimates a lower average tax rate than Mr. Trump cites, but its figures also show that about 80 percent of households will pay a smaller share of their income in federal taxes this year than the average tax rate. That’s because the United States has a progressive income tax under which higher-income people pay at higher rates, and that — coupled with a high concentration of income at the top of the income scale — raises the “average” percentage of income that is paid in federal taxes to a level substantially above the percentage of income that most people actually pay.

The following example shows how the “average” tax rate can substantially overstate the tax burdens of the typical family. Suppose four families with incomes of $50,000 each pay $2,500 in taxes (5 percent of their income) while one wealthier family with income of $300,000 pays $90,000 in taxes (30 percent of its income). Total income among these five families is $500,000, and the total amount paid in taxes is $100,000. Thus, 20 percent of the total income of the five families goes to pay taxes. But it would be highly misleading to conclude that 20 percent is the typical tax burden for families in this group.

The specific figure that Mr. Trump cited comes from an Organisation for Economic Cooperation and Development (OECD) study that created hypothetical family types to produce comparative statistics across the 34 OECD member countries.[4] The study did not attempt to estimate actual tax rates for typical families.

Corporate Tax Rate

Mr. Trump stated that the United States “has the highest business tax rate among the major industrialized nations of the world, at 35 percent.” As CBPP analyses have explained, however, while the U.S. statutory corporate tax rate is high, the amount that U.S. corporations actually pay in taxes — the effective tax rate — is much lower.[5] This is largely because the U.S. corporate code is riddled with tax preferences that significantly reduce many corporations’ taxes (and also create wide disparities in effective tax rates across the economy).

For example, finance firms paid about 23 percent of their profits in corporate taxes over 2007 to 2010, a Treasury analysis found, far below the statutory rate of 35 percent.[6]

Estate Tax

Finally, calling for repeal of the estate tax, Mr. Trump stated today, “American workers have paid taxes their whole lives, and they should not be taxed again at death.” In reality, as CBPP analyses[7] have explained, only the estates of the wealthiest 0.2 percent of Americans — roughly 2 out of every 1,000 people who die — owe any estate tax at all, because the first $5.45 million of a person’s estate (and the first $10.9 million for a married couple) is entirely exempt from the tax. Much of the wealth that heirs inherit from massive estates would never face taxation if not for the estate tax. Some 55 percent of the value of the very largest estates consist of “unrealized” capital gains that have never been taxed, the Federal Reserve estimates.

Repeal would bestow tax windfalls averaging over $3 million apiece — more than a typical college graduate earns in a lifetime — on the roughly 5,400 wealthy estates that will owe any estate tax in 2016. Such large tax breaks aimed solely at the top would exacerbate wealth inequality, which has grown significantly in recent decades. (In 2012, the wealthiest 1 percent of American families held about 42 percent of total wealth.)[8] Large inheritances play a significant role in the concentration of wealth; inheritances account for about 40 percent of all household wealth and are heavily concentrated at the top.

Repeal would also add $320 billion to deficits over 2016 to 2025, including the additional interest that would have to be paid on the national debt.

End Notes

[1] Chuck Marr and Chye-Ching Huang, “Trump Tax Plan Includes Major Tax Break For Wealthiest Taxpayers,” Center on Budget and Policy Priorities, August 8, 2016, https://www.cbpp.org/research/federal-tax/trump-tax-plan-includes-major-tax-break-for-wealthiest-taxpayers.

[2] The top capital gains tax rate plus the net investment income surtax.

[3] James R. Nunns et al., “Analysis of Donald Trump's Tax Plan,” Tax Policy Center, December 22, 2015, http://www.taxpolicycenter.org/publications/analysis-donald-trumps-tax-plan/full.

[4] OECD, Taxing Wages 2015, page 535, http://www.oecd-ilibrary.org/taxation/taxing-wages-2015_tax_wages-2015-en.

[5] Chuck Marr and Brian Highsmith, “Six Tests for Corporate Tax Reform,” Center on Budget and Policy Priorities, February 24, 2012, https://www.cbpp.org/research/six-tests-for-corporate-tax-reform.

[6] “The President’s Framework for Business Tax Reform: An Update,” joint report by the White House and the Department of the Treasury, April 2016, https://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-An-Update-04-04-2016.pdf.

[7] Chuck Marr, Brandon Debot, and Chye-Ching Huang, “Eliminating Estate Tax on Inherited Wealth Would Increase Deficits and Inequality,” Center on Budget and Policy Priorities, updated April 13, 2015, https://www.cbpp.org/research/federal-tax/eliminating-estate-tax-on-inherited-wealth-would-increase-deficits-and#.

[8] Emmanuel Saez and Gabriel Zucman, “Wealth Inequality in the United States since 1913: Evidence from Capitalized Income Tax Data,” NBER Working Paper 20625, October 2014, http://eml.berkeley.edu/~saez/saez-zucmanNBER14wealth.pdf.

More from the Authors

Areas of Expertise

Areas of Expertise