Childless Adults Are Lone Group Taxed Into Poverty

EITC Expansion Could Address Problem

Since enactment of the 1986 Tax Reform Act, federal income tax parameters have been designed to ensure that federal income and payroll taxes don’t tax people into, or deeper into, poverty, with one glaring exception — low-income childless adults. Today, more than 5 million workers aged 19-67 are taxed into or deeper into poverty by federal taxes.[1] The main reason is that the Earned Income Tax Credit (EITC) for this group is much too small (and for some, isn’t available at all) to offset the income taxes and employee share of payroll taxes that they must pay.

A number of members of the House and Senate have introduced legislation in this Congress that would make major progress in addressing this problem by substantially expanding the EITC for workers not raising children in their homes. The proposals would reduce poverty among these workers while improving their well-being and strengthening the incentives for jobless individuals who aren’t raising children to enter the labor force.

For example, the Working Families Tax Relief Act, introduced by Senators Sherrod Brown, Michael Bennet, Richard Durbin, and Ron Wyden, as well as by Representatives Dan Kildee and Dwight Evans in the House, would boost the maximum EITC for childless adults from about $530 today to $2,070, raise the income limit at which single individuals no longer qualify for the credit from about $16,000 to about $25,000, and expand the ages at which individuals can be eligible for this credit from 25-64 to 19-67 (except for full-time students aged 19-24, who would remain ineligible because their parents can claim many of them for the larger EITC for families with children).[2] These changes would reduce the number of workers aged 19-67 (other than full-time students) whom the federal tax code taxes into, or deeper into, poverty to by about 91 percent — from 5.51 million today to fewer than 500,000. [3]

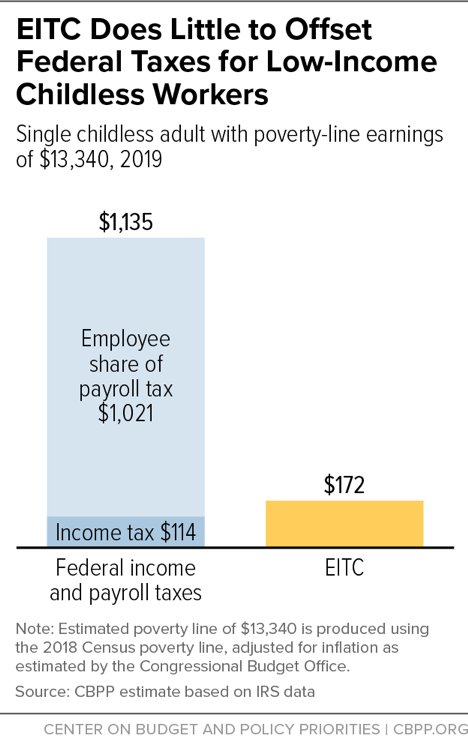

Childless Worker With Income at Poverty Line Owes $1,000 in Federal Taxes

The standard deduction, EITC, and Child Tax Credit (CTC) are set at levels that ensure that families with children don’t have net federal tax liability if they earn poverty-level wages. As a result, no families with children are taxed into poverty. Single childless adults, in contrast, begin owing income tax when their earnings are still below the poverty line, and they receive little or no EITC. They also face significant payroll taxes. As a result, the federal tax code taxes millions of employed individuals aged 19-67 into, or deeper into, poverty.[4]

Consider, for example, a 25-year-old single woman who makes poverty-level wages in 2019 ($13,340) as a retail salesperson, working roughly 35 hours a week throughout the year at the federal minimum wage:

- Some $1,021 (7.65 percent of her earnings) in Social Security and Medicare payroll taxes are deducted from her paychecks.

- When filing her tax return, she will claim a $12,200 standard deduction. Subtracting this amount from her income leaves $1,140 in taxable income. She is in the 10 percent bracket and hence will have a $114 federal income tax liability.

- The sum of her $114 in income tax liability and $1,021 in payroll taxes is $1,135.

- She will be eligible for an EITC of $172.

- Her net federal tax liability thus will be $1,135 minus $172, or $963.

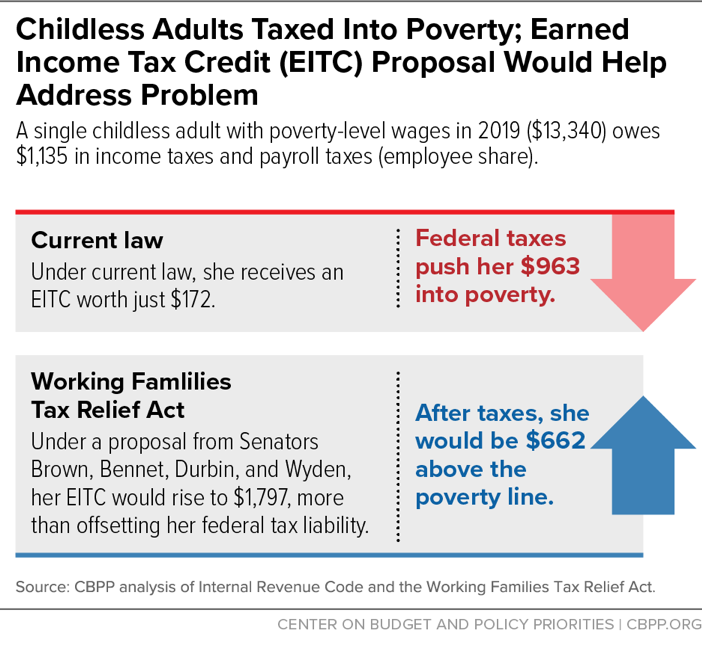

In short, federal taxes will drive this woman making poverty-level wages $963 into poverty. (See Figure 1.)

A number of recent proposals would address this shortcoming of the tax code. Among the most recent is the Working Families Tax Relief Act, introduced last month by the four senators mentioned above and co-sponsored by 42 others. It would make the following changes:

- Increase the phase-in rate. Under current rules, the EITC for childless workers phases in at a rate of 7.65 percent. In other words, a worker receives an EITC of 7.65 cents for each additional dollar of earnings until the credit is fully phased in at earnings of $6,920 in 2019, at which point the credit equals about $530. The bill would boost the phase-in rate to 20 percent (i.e., 20 cents for each additional dollar earned).

- Boost the maximum credit for childless adults from $530 today to about $2,070. This increase results from raising the phase-in rate (as noted just above) and raising the income level at which the credit stops phasing in. The bill also raises the income level at which the credit starts phasing out. (See Table 1.)

- Expand eligibility to include more low-wage childless adults. The current EITC for single childless adults phases out entirely at an income of $15,570. A cashier or landscaper, for example, working for low wages and making $16,000 a year receives no EITC. The legislation would raise the income level at which the credit entirely phases out to about $25,000.

- Expand the eligibility age range to 19-67. Workers under 25 and over 64 are currently ineligible for the childless workers’ EITC.

| TABLE 1 | ||

|---|---|---|

| Working Families Tax Relief Act’s EITC Proposal for Childless Workers (2019) | ||

| Current law | Proposal | |

| Phase-in rate | 7.65% | 20.00% |

| Phase-out rate | 7.65% | 15.98% |

| Income level at which credit stops phasing in (“first kink point”) | $6,920 | $10,370 |

| Income level at which credit begins to phase down (“second kink point”)* | $8,650 | $11,590 |

| Income level at which credit phases out entirely* | $15,570 | $24,569 |

| Maximum credit | $529 | $2,074 |

| Age range for qualifying tax filers | 25-64 | 19-67 |

The retail salesperson with poverty-line wages in the example cited above would receive an EITC of $1,797 in 2019 under the proposal, a large increase from her $172 EITC under current law. This would more than offset her $1,135 federal tax liability, so the federal tax code would stop taxing her into poverty. Under the proposal, about 600,000 childless working people would no longer be taxed into poverty, and nearly 5 million would no longer be taxed deeper into poverty.

It’s important to note, however, that while expanding the EITC would mark significant progress for low-wage workers, regressive state and local taxes could still push them into poverty. State policymakers should act as well, by raising the income levels at which state income taxes kick in and/or by creating or expanding state EITCs.[5]

The principle that we should not tax people into poverty resonates across the political spectrum. Low-income childless adults are the sole group for whom the federal tax code falls short here. Addressing this shortcoming should be a priority for future tax legislation.

End Notes

[1] “Childless adults” refers to workers, including non-custodial parents who are not raising minor children in their home and not claiming dependents for purposes of the EITC.

[2] For analysis of the proposal, see Chuck Marr et al., “Working Families Tax Relief Act Would Raise Incomes of 46 Million Households, Reduce Child Poverty,” Center on Budget and Policy Priorities, April 10, 2019, https://www.cbpp.org/research/federal-tax/working-families-tax-relief-act-would-raise-incomes-of-46-million-households.

[3] Some 60,000 workers aged 19-67 who aren’t full-time students would still be taxed into, or deeper into, poverty. Many of them are people who would remain ineligible for the EITC because they do not meet the EITC’s net investment test — filers with investment income of more than $3,500 are ineligible for the EITC.

Approximately 200,000 people under age 19 or over age 67 are taxed into, or deeper into, poverty, a number that wouldn’t be affected by the bill. Under the bill, people under 19 would remain ineligible to claim the childless workers’ EITC because children through age 18 can be claimed by their parents for the much larger EITC for families with children. Also, in creating the childless workers’ EITC in 1993, Congress made people age 65 and over (then Social Security’s “normal retirement age,” which now is rising to 67) ineligible for the childless workers’ EITC because such individuals often have Social Security income that isn’t counted as adjusted gross income (AGI), and hence they may be less needy than their AGI may imply. Roughly 550,000 full-time students between the ages of 19 and 24 also would not be affected; as noted, their parents can claim many of them for the larger EITC for families with children.

[4] CBPP analysis of the March 2018 Current Population Survey. The estimate includes all workers aged 19-67 who: 1) do not have a qualifying child for the EITC; 2) are not a tax dependent themselves; 3) are full-time students between the ages of 19 and 24; and 4) owe federal income tax plus the employee share of the payroll tax that push them below the poverty line, or they already are poor (based on their cash income before income and payroll taxes) and are pushed further into poverty by those taxes. It includes workers who are (or whose spouses are) aged 19-67. The calculation starts with the combined cash income of a worker and his or her spouse, which includes pre-tax market income as well as government cash benefits (including, for example, Social Security retirement and disability benefits and Supplemental Security Income), and then considers the effect of subtracting (or not subtracting) federal income taxes and the employee share of payroll taxes. (Note that these estimates do not include housing assistance and SNAP, formerly known as food stamps. Adding a per capita share of housing assistance and SNAP benefits for workers or spouses who receive these benefits does not materially affect the estimate.) Poverty status is determined at the level of the tax filing unit (the tax filer, their spouse, and any dependents, as identified in our tax model), and uses the 2017 Census official poverty threshold appropriate for the tax unit based on number and age of the tax unit members.

[5] Twenty-nine states and the District of Columbia have state EITCs.

More from the Authors