Making Budget Enforcement More Effective

Testimony of Richard Kogan[1] before the Committee on the Budget, U.S. House of Representatives, June 22, 2016

Mr. Chairman, Mr. Van Hollen, members of the Committee, I am always happy to come home to the House Budget Committee. My prepared testimony is brief. With your permission, I would like that testimony and three accompanying charts to be placed in the record.

Congress is free to use the enforcement tools it already has, and when it chooses not to, the budget process is not to blame.Today’s hearing asks how to make budget enforcement more effective. My answer is that Congress already has the enforcement tools it needs: congressional points of order and the reconciliation process. Congress is free to use them; and when it chooses not to, the budget process is not to blame.

Let me discuss enforcement from two perspectives: what this Committee and Congress can do to enforce budget plans, and what it should not do. From one perspective, there is no mystery to enforcing congressional budget plans: points of order bar legislation that this Committee determines costs too much, and the “reconciliation” process can compel reluctant committees to submit legislation raising taxes or cutting the costs of mandatory programs, rather than sitting on their hands.

A different perspective asserts that so-called mandatory programs are “out of control.” The frequent repetition of this myth leads some people to the notion that the only way, or the best way, to control their long-run costs is to impose rigid dollar or percent-of-GDP caps on the total of all mandatory programs, backed up by automatic across-the-board cuts to those programs. But that notion is dangerous in concept and in practice.

Enforcement Under the Congressional Budget Act

Points of order preclude the House from considering legislation that would breach the agreed-upon level of funding for discretionary appropriations, or from considering tax cuts in excess of those envisioned in the congressional budget plan, or from considering entitlement increases in excess of those envisioned in the congressional budget plan. Points of order are a tool that is clearly adequate to the job.

Points of order, even if never waived, can only limit the cost of legislation that committees bring to the floor of the House: annual appropriations bills, tax cuts, and entitlement increases. Points of order do not compel recalcitrant committees to cut existing mandatory programs or raise taxes if they do not wish to — even if Congress has agreed to a budget plan whose numbers are based on those policy changes and even if Congress fully understands the policies that underlie them. If the committees of jurisdiction prefer existing law to the assumed entitlement cuts and tax increases, they could sit on their hands. That’s why the reconciliation process exists.[2]

As it has evolved, the reconciliation process essentially compels committees to write the intended legislation; if not, this Committee is allowed to pinch hit. Packaging the work of multiple committees into a single reconciliation bill and leaving its management to this Committee and the House Leadership enhances the likelihood that the bill will be approved. The fact that the Senate cannot filibuster a congressional budget plan or the resulting reconciliation bill means that the budget process is more effective than any other aspect of the legislative process; it is wrong to assert that the budget process is broken. History shows that Congress has used the reconciliation process frequently. In fact, some of the most important deficit reduction measures have been enacted through reconciliation. Historically, most reconciliation bills that reach the President’s desk are signed. Specifically —

- Since the reconciliation process was first used in 1980, 21 sets of reconciliation directives contained in congressional budget plans have led to enactment of 17 reconciliation bills, and the veto of four others.

- Two of those reconciliation bills, in 1993 and 2005, were approved by the Senate on a vote of 51 to 50, with the vice president breaking the tie.

- Of the 17 enacted reconciliation bills, 15 reduced projected deficits.

- All four of the vetoed reconciliation bills contained substantial tax cuts, not tax increases. In two of the cases, the tax cuts were not offset at all by spending cuts.

- In five cases, a reconciliation bill was enacted even though different parties controlled the two houses of Congress, and in another six cases, Congress and the President were of different parties.

- At least 13 of the enacted reconciliation bills included provisions that generated savings in Medicare, suggesting that the contention that Congress has no ability to address permanent, open-ended entitlements is wrong.

But the reconciliation process is an optional tool. Congress could approve a budget plan that envisions entitlement cuts and tax increases, but the plan might not contain a matching reconciliation directive. The reconciliation tool is adequate to the job; it is merely a choice whether to leave the tool on the workbench.

Entitlement Caps: A Truly Bad Idea

Second, let us consider the notion of going outside the Congressional Budget Act to impose exogenous dollar caps, or percent-of-GDP caps, on mandatory programs. This is a truly dangerous idea, for multiple reasons.

To begin with, many of these programs are designed to provide more assistance as need rises and less as it falls, responding to economic forces that Congress cannot control. The obvious example is unemployment insurance, which provides some modest and temporary income support and whose costs therefore rise when the economy weakens and fall when the economy strengthens. The same is true to a lesser extent of SNAP (formerly food stamps) and Medicaid. Having the costs of these programs run counter to the business cycle is an essential feature of these programs and a great virtue. Caps would destroy the countercyclical aspects of these programs, immiserating millions of people when times are bad, harming their prospects into the future, making recessions deeper and more frequent, and slowing overall economic growth over time.

The virtue of countercyclical benefit programs is mirrored by the virtue of countercyclical tax law. It is good, not bad, that revenues fall even faster than the economy does during bad times, and rise even faster than the economy during good times. Together, the countercyclical aspects of taxes and mandatory benefits serve to moderate booms and busts, make recessions less frequent and shallower, and contribute to higher long-term economic growth. Imposing an exogenous cap on mandatory programs would be as wrongheaded as imposing an exogenous floor on revenues, forcing automatic tax increases when times are bad.[3]

The fact that many of these key mandatory programs grow and shrink, countering the business cycle, says nothing about whether, as a whole, mandatory programs are affordable over time. It is the average cost over time that makes the difference for long-run budget sustainability, not the variations above and below the average. And there is no plausible way to design mandatory caps that fully allow their cyclical ups and downs while imposing constraint on their average costs. That can’t be done. Therefore, if this Committee and Congress think the average costs over time of mandatory programs are too high, the right tool to use is the tool that is already available; the reconciliation process can be used to enact benefit and eligibility changes that decrease average costs over time.

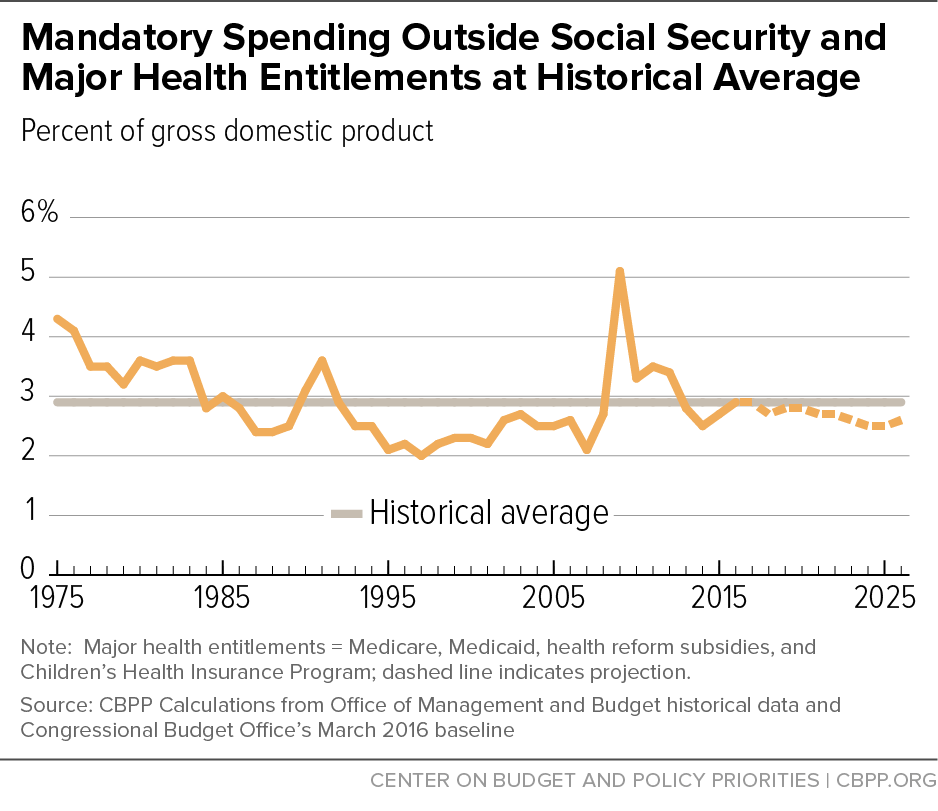

It is a gross oversimplification to believe that mandatory programs are irretrievably “out of control” and therefore that caps are a necessary evil. Putting aside for the moment Social Security and the major health care entitlements, the entire remaining set of mandatory programs currently cost about the same amount, as a percent of the economy, as they have for the past 40 years — since enactment of the Congressional Budget Act — and according to CBO are projected to cost slightly less as the decade progresses. By definition, that means these programs put no upward pressure on long-term budget sustainability. (See Figure 1.)

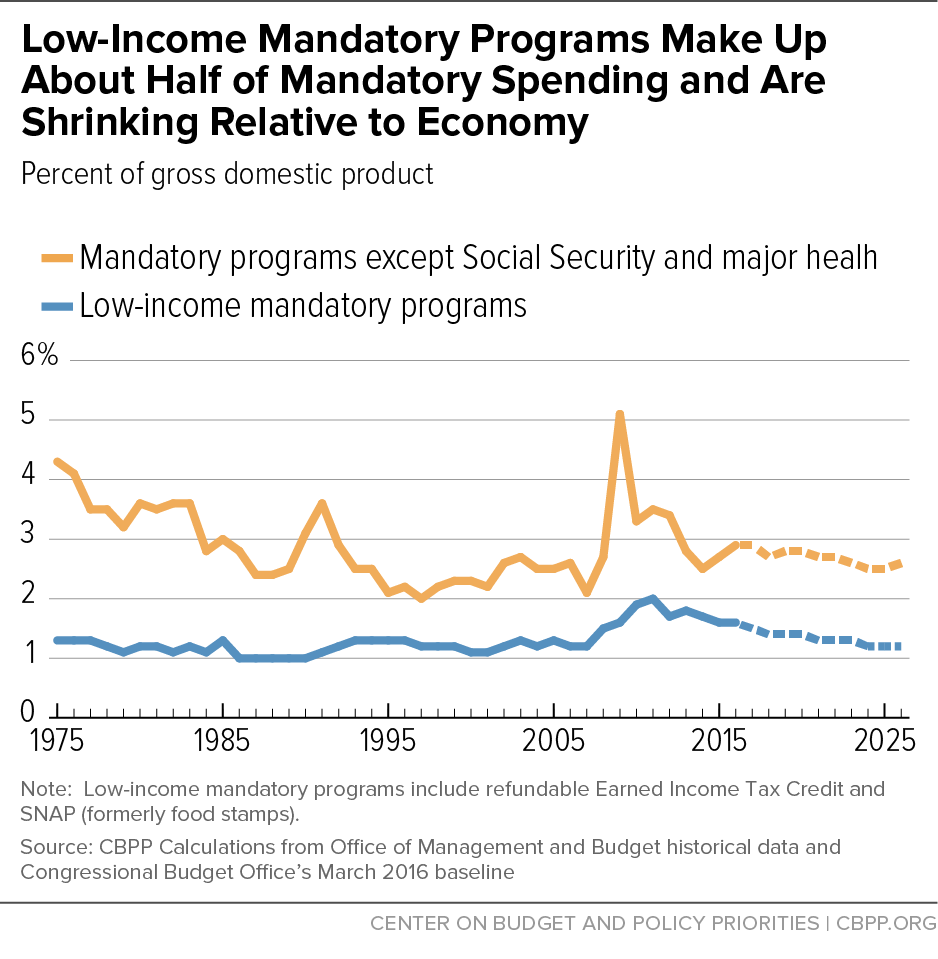

Note also that only a minority of these mandatory programs are directed towards low- and moderate-income households, and that this subset of programs is likewise not growing faster than the economy, either now or in CBO’s projections. (See Figure 2.)[4]

The story is somewhat different for Social Security and the major health entitlements: Medicare, Medicaid, and the health reform subsidies. As a whole, this set of programs is growing faster than the economy and so puts upward pressure on budget sustainability. This fact raises questions. To begin with, the growth of Social Security is due to the aging of the population, certainly not because of any design flaw. Indeed, the program’s benefits are not overly generous; a good case can be made for the opposite proposition. In any event, Social Security had cost about 4 percent of GDP before my generation started retiring roughly five years ago, and is projected to cost about 6 percent of GDP when the entire baby boom generation is retired and to stay at that level indefinitely. An increase of 2 percent of GDP over two decades is hardly explosive. The question, of course, is how to fit these costs into a sustainable budget — one whose debt ratio stays stable over the long term, preferably falling during normal times and rising only when the economy is weak or the nation faces a dire emergency.

We all know the options: raise revenues, cut Social Security benefits, or have other programs fall by 2 percent of GDP over the next few decades. It is a policy call about which of these options, or which combination of these options, is preferable. It is not obvious that Social Security must be cut merely because the population is greying; it is reasonable for the shape and contents of the budget to change as the nation’s needs and responsibilities change. Locking in the current shape of the budget, or the shape based on an historical average, would be a policy straightjacket, and an aggregate entitlement cap is just a variation on that straightjacket. But there is no obvious reason why Social Security growth, if the natural aging of the population is to be accommodated, must be offset by cutting other programs that happen to be mandatory, rather than, for example, by raising revenues. An entitlement cap merely evades policy decisions rather than making them.

With respect to the major health entitlements, the story is similar but not identical, for they are projected to grow not just because the population is aging but also because the nation and world keep inventing better medical practices, at greater costs. I should note that the costs of federal health care are lower than the costs of equivalent private-sector health care, accounting for the age of the population and differences in health status. In the case of Medicaid, public costs per beneficiary are far less than equivalent private-sector costs, and per-beneficiary costs have been growing more slowly over the past decade than in either private insurance or Medicare. The problem is not that federal programs are badly designed; it’s that health care in the U.S. is expensive system-wide, and growing more so.

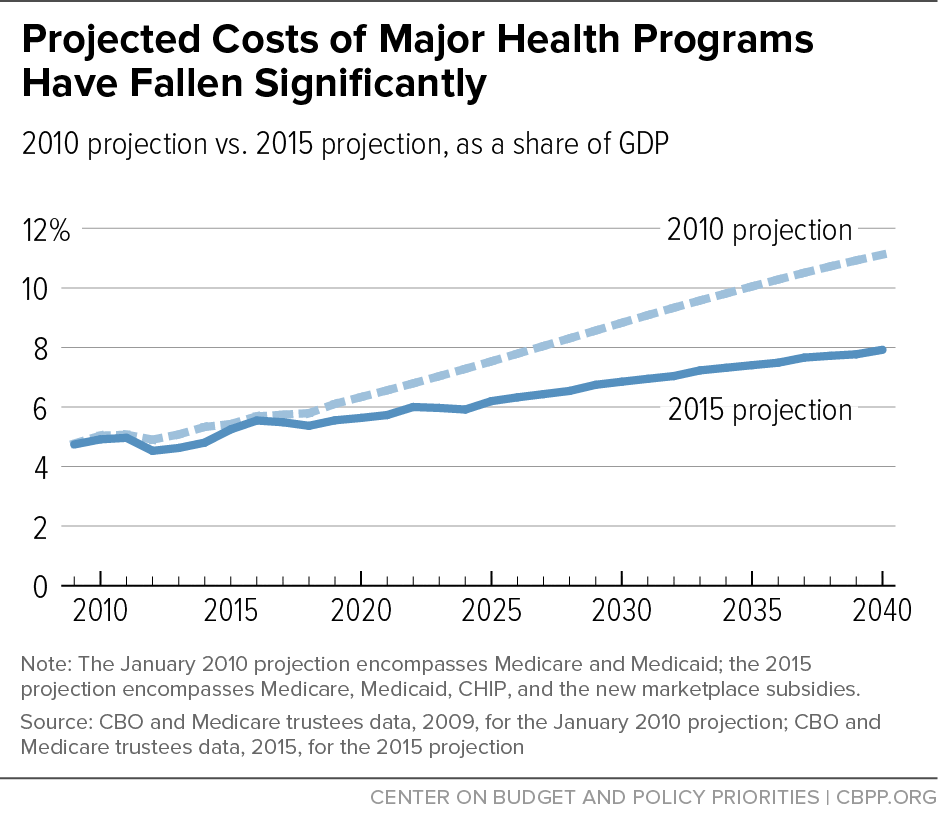

But there is good news: the situation is noticeably less dire than it appeared six years ago. As Figure 3 shows, the costs of the major health entitlements are projected to grow more slowly than was previously thought. In 2010, the combined costs of Medicare and Medicaid were projected to grow from about 5 percent of GDP to 11 percent by 2040. Now, however, the costs of Medicare, an expanded Medicaid, and the new health care subsidies in health reform are projected to total only 8 percent of GDP in 2040.

Still, these health care costs are growing faster than the economy (albeit at a slower rate than previously projected), so the same questions arise as with Social Security: should that growth be further reduced? Should it instead by covered by higher revenues? Should it be covered by reductions in other programs? And if so, which ones? Is the best answer “some combination of the above,” and if so, what combination? Once again, the answer is a policy call. It is not inherently right to say either that health care entitlements as a whole must be capped as a percent of GDP merely because they are growing faster than the economy or that all entitlements as a whole should be capped as a percent of GDP. Either of those simplistic responses evades policy decisions rather than making them.

Conclusion

In the first part of this testimony, I noted that the reconciliation process is an effective tool for cutting the cost of mandatory programs — and for raising revenues — if that is what Congress chooses to do. The tool is at hand, and Congress can use it, as it has many times before. It seems misleading if not disingenuous to call for large, general, or unspecified cuts in mandatory programs in a budget plan but not to reconcile those cuts — and then to wonder if the tools of budget enforcement are inadequate.

In much the same way, it seems inappropriate to engage in public worrying about the rising cost of health care and then wonder if the right solution is to impose some sort of aggregate cap covering all entitlements. If such a cap were enacted and enforced by across-the-board cuts, the result would be equivalent to having Congress enact a wide swath of badly timed and ill-thought-out program cuts without any Member of Congress ever having to vote for the actual cuts. That’s not the way Congress should work.

End Notes

[1] Kogan is a Senior Fellow at the Center on Budget and Policy Priorities, Washington D.C. He previously served for 21 years on the staff of the House Budget Committee, for 5 years in the Congressional Research Service, and for 2½ years in the Office of Management and Budget.

[2] See CBPP, “FAQs on Budget ‘Reconciliation,’” January 22, 2015, https://www.cbpp.org/blog/faqs-on-budget-reconciliation.

[3] For a discussion of the merits of countercyclical fiscal policy, see for example Jared Bernstein and Ben Spielberg, “Preparing for the Next Recession,” Center on Budget and Policy Priorities, March 21, 2016, https://www.cbpp.org/research/economy/preparing-for-the-next-recession-lessons-from-the-american-recovery-and.

[4] CBO estimates that in 2016 the 15 largest of these mandatory programs are, in order: 1) Civil Service retirement, disability, and health; 2) Veterans’ disability compensation; 3) Supplemental Nutrition Assistance Program (SNAP, formerly food stamps); 4) Military retirement, disability, and health; 5) the refundable Earned Income Tax Credit (EITC); 6) Supplemental Security Income (SSI); 7) Unemployment insurance; 8) Child Nutrition; 9) the refundable Child Tax Credit; 10) Temporary Assistance for Needy Families (TANF) and the Contingency Fund; 11) veterans’ readjustment benefits (G.I. bill); 12) Universal Service Fund; 13) Federal Crop Insurance Fund; 14) Commodity Credit Corporation; and 15) Foster Care and Permanency. (CBPP classifies the italicized programs as targeted primarily on low- and moderate-income households.)

More from the Authors