BEYOND THE NUMBERS

What You Need to Know About International Tax Reform Options

The Senate Finance Committee will release the fifth of its tax reform option papers later today, this one on international taxation, Tax Notes reports. Here’s why that’s important.

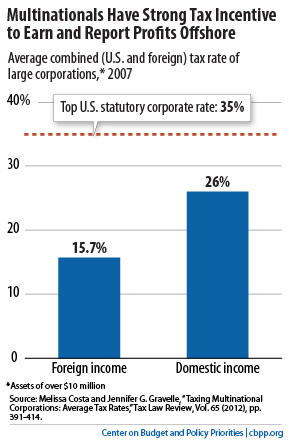

Among its options the committee will likely list is a move toward a “territorial” tax system that exempts or largely exempts the foreign profits of U.S.-based multinational corporations from U.S. tax. As we’ve explained, that would create greater incentives for those companies to invest and book profits overseas rather than at home — and that, in turn, risks reducing wages at home by encouraging investment to flow overseas, increasing budget deficits by draining revenues from the corporate income tax, and raising taxes on smaller companies and domestic businesses.

- The need to lessen the current foreign tilt of the tax code and growing tax avoidance by multinationals (see chart);

- The Organisation for Economic Co-operation and Development’s warning about growing tax avoidance by multinationals that undermines competition; and

- The fact that even a less than “pure” territorial tax system — that is, one that has safeguards against inappropriate profit-shifting to overseas tax havens — carries serious risks.

As our paper describes, a better first step on international tax reform would be President Obama’s fiscal year 2014 budget proposals to reform international taxation, which would reduce incentives for corporations to shift profits and investments overseas and raise $157 billion over ten years. A key provision would prevent companies from deducting their interest expenses associated with loans that support overseas investments as long as they are deferring U.S. tax on the income that those investments generate.