BEYOND THE NUMBERS

Policymakers Should Ensure Pass-Throughs Pay More of Taxes They Owe

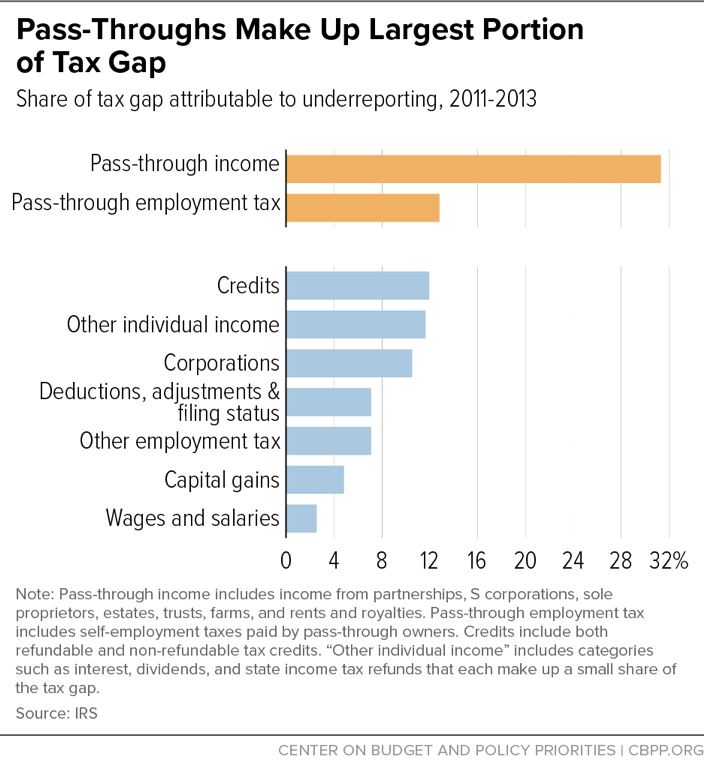

High-income taxpayers drive much of the “tax gap” — the gap between what taxpayers owe and what they voluntarily pay on time — finds a new paper from Professor Natasha Sarin and former Treasury Secretary Lawrence Summers, citing new IRS data for 2011 to 2013. That’s unsurprising, because the tax gap’s single largest source is the underreporting of pass-through income (income from sources such as S corporations, partnerships, and sole proprietorships), which overwhelmingly flows to wealthy households. IRS auditors looking to curb tax evasion as well as policymakers looking to close tax loopholes should make pass-throughs a prime target.

Overall, Americans didn’t pay more than 16 percent — or $441 billion a year — of their federal taxes from 2011 to 2013 voluntarily and on time. The IRS refers to that amount as the “gross tax gap,” of which it later collected about 13 percent through enforcement efforts and other late payments. But, as we discuss below, the IRS’ current enforcement budget shortage threatens its future ability to recover even that modest share of the tax gap.

Taxpayers who didn’t file a return and those underpaying the IRS accounted for 20 percent of the gross tax gap, and income underreporting the other 80 percent, the latest IRS data show. Pass-throughs accounted for nearly half (44 percent) of the underreporting gap, counting both underreported income and self-employment taxes.

Pass-through owners are generally responsible for reporting their income to the IRS, with little independent verification by the government. This “opaqueness,” as Sarin and Summers describe it, makes tax avoidance easier. For example, many S corporation shareholders receive both wages from the company and a share of the company’s profits, but they only pay payroll tax on their wages. Accordingly, many high-income people underreport their wages and overstate their pass-through profits to reduce their payroll tax. Some 13 percent of S corporations underpaid wage compensation from 2003 to 2004, totaling $23.6 billion in underpaid wages and potentially $3 billion in lost revenues, the Government Accountability Office has found.

Pass-through noncompliance accounts for the largest share of the tax gap, as the latest IRS data confirm. But the 2017 tax law may have made it even harder for the IRS to police pass-through tax evasion. The law’s 20 percent deduction for pass-through income has added new incentives for taxpayers to shift their income away from wages since pass-through profits now face a tax rate as low as 29.6 percent, compared to a 37 percent top rate for wages and salaries. As we’ve noted, the deduction also introduced arbitrary distinctions between income that qualifies for the deduction and income that doesn’t, which pass-through owners could easily game to minimize their taxes.

The IRS’ ability to improve pass-through tax compliance requires a well-funded and fully staffed audit capacity, but policymakers in recent years have targeted its enforcement budget for deep budget cuts. The combination of an underfunded IRS and a tax system rife with avoidance opportunities invites wealthy individuals and profitable businesses to engage in schemes that may constitute illegal tax evasion. As policymakers set next year’s IRS funding, they should at least match — and preferably exceed — the House-approved $567 million boost in IRS enforcement and operations support. Looking to the future, policymakers also should close loopholes for pass-through owners — including by repealing the pass-through deduction at their first opportunity.