BEYOND THE NUMBERS

House Republican “2.0” Tax Plan Skewed to Top, Loses Needed Revenue

The House will vote today on the Ways and Means Committee’s “2.0” tax plan, which would double down on the fundamental flaws of the 2017 tax law. As we’ve explained, the bill would make permanent the law’s individual provisions and thereby favor the wealthy, worsen the nation’s long-term fiscal challenges, and encourage rampant gaming of the tax code. Rather than enacting this fundamentally flawed legislation, policymakers should set a new course by restructuring the 2017 tax law.

- The 2.0 tax plan ignores working-class wage stagnation and shifts more income upward. While working-class wages have stagnated in recent decades, incomes at the top have risen dramatically. From 1979 to 2014, the share of income flowing to the top 1 percent rose by 5.7 percentage points, while the share flowing to the bottom 60 percent fell by 4.4 percentage points.

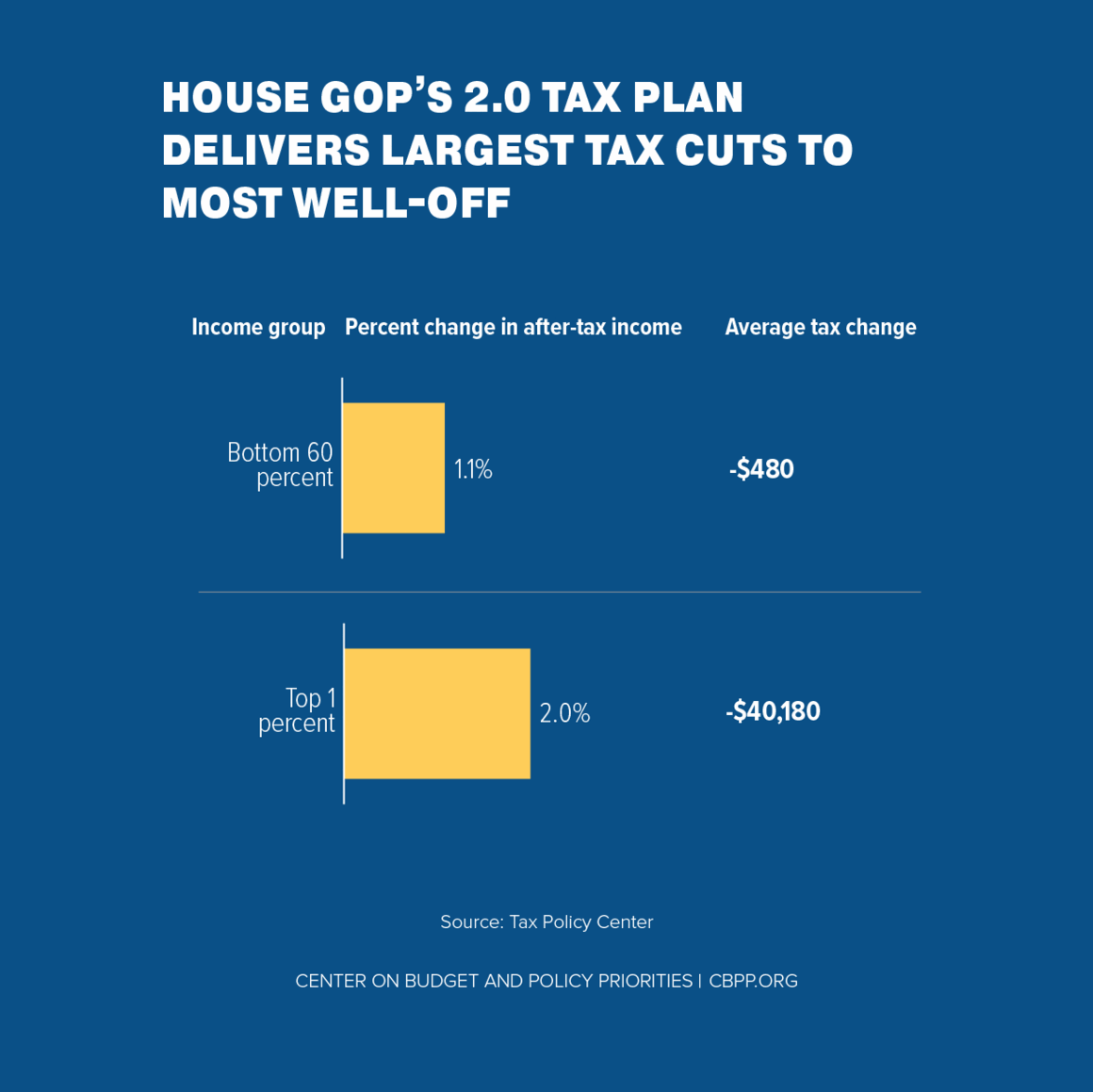

This bill would exacerbate the trend of skewed benefits to the wealthiest. Households in the top 1 percent would see their after-tax incomes rise 2.0 percent (or an average of $40,180) while those in the bottom 60 percent would receive only a 1.1 percent ($480) boost (see first chart).

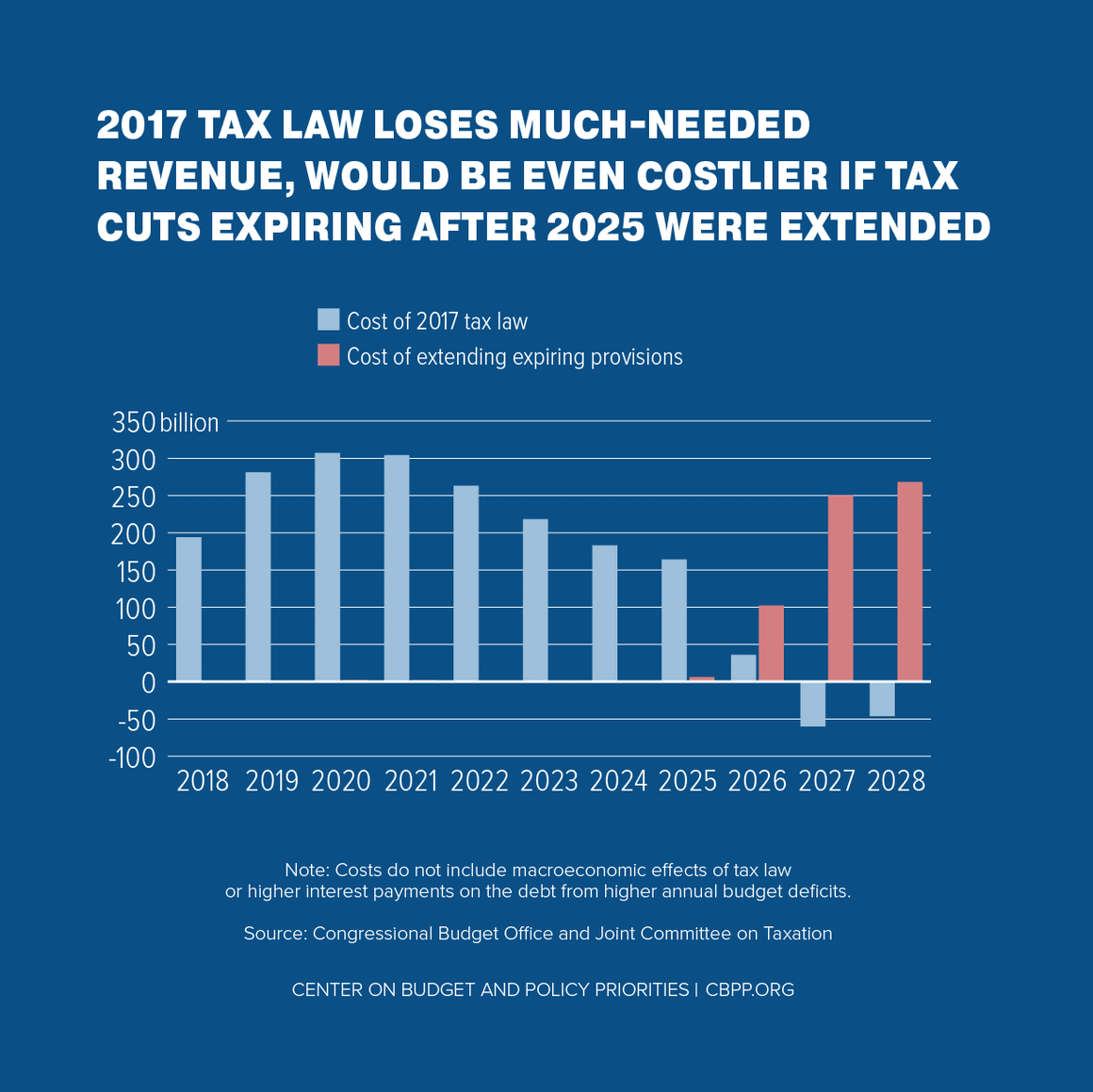

- The bill would weaken revenues when they’re needed the most. Federal spending will necessarily rise as a share of gross domestic product (GDP) over the next few decades due to several factors, most importantly the aging of the population that will increase the costs of Social Security, Medicare, and Medicaid. Making the 2017 tax law’s individual provisions permanent would cost $250 billion in 2027 alone (see second chart), amounting to more than 0.8 percent of GDP. We estimate that the cost of making them permanent in the first ten years that it would be in effect (2026 to 2035) would be roughly $2.8 trillion, and the Tax Policy Center estimates that the cost from 2029 to 2038 would be $3.2 trillion.

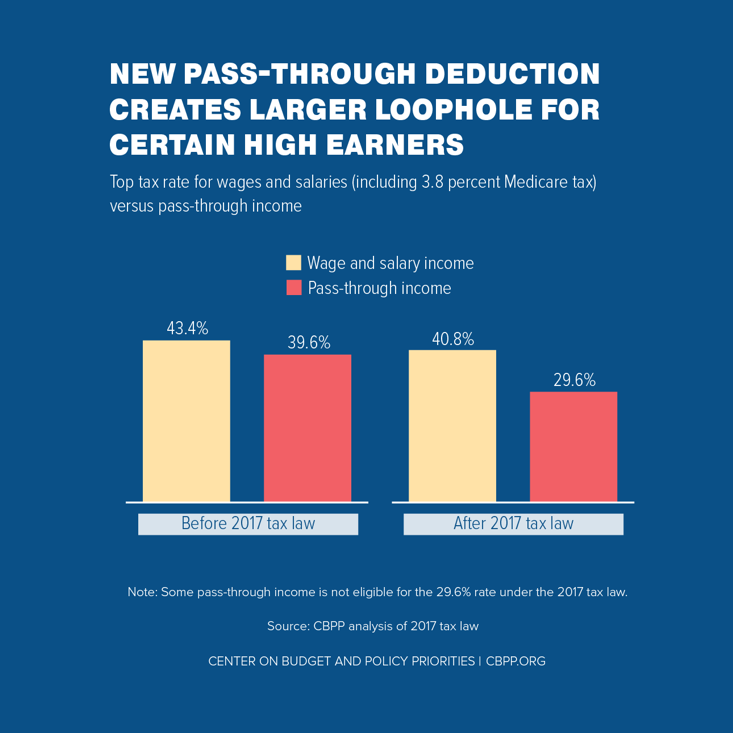

- The bill would encourage more tax gaming and avoidance. The 2017 tax law created a 20 percent deduction for pass-through income — the income that owners of businesses such as partnerships, S corporations, and sole proprietorships report on their individual tax returns. Previously, pass-through income was taxed at the same tax rates as wage and salary income (see third chart). The 2.0 tax plan would make this provision permanent, which would encourage high-income individuals to reclassify as much of their salaries as possible as pass-through income.