Unpaid-for Tax Cuts: the Gulf Between Promises and Reality

Chye-Ching Huang, Deputy Director, Federal Tax Policy, Center on Budget and Policy Priorities

Thank you for the opportunity to testify today. President Trump and congressional Republicans’ tax plans propose costly corporate tax rate cuts — and cutting the rate on foreign profits of U.S. multinationals to zero. Prioritizing tax cuts for corporations that are posting record profits starkly contrasts with the President’s promise to focus on raising working and middle-income families’ incomes. Faced with this gulf between their promises and their policies, the Administration and congressional Republicans have made misleading claims about who corporate tax cuts help.

In fact, corporate rate cuts mostly benefit CEOs and shareholders, not typical workers. While the Administration and congressional Republicans claim that corporate rate cuts trickle down to workers through more investment and higher wages, mainstream non-partisan estimates are that the bulk of corporate rate cuts go to shareholders and CEOs, not typical workers. Indeed, the corporate and other tax proposals offered by President Trump and Republican leaders in Congress could hurt workers and most Americans. As my testimony explains:

- A zero percent U.S. tax rate on U.S. multinationals’ foreign profits would increase their incentive to shift profits and possibly investment offshore. Reversing his campaign position, President Trump now supports a “territorial” tax system. U.S.-based multinationals would pay U.S. corporate taxes on their domestic profits, but no U.S. taxes on their foreign profits. That would supercharge their incentive to avoid U.S. taxes by booking profits offshore, bleeding revenues. And, if the even greater advantage for foreign profits encouraged multinationals to move any real investment offshore, that could hurt U.S. workers’ productivity and wages.

- Corporate tax cuts and other tax cuts that skew to the wealthy could harm education, infrastructure, and other federal investments. Senate Republicans are reportedly considering allowing a tax reconciliation bill that loses up to $1.5 trillion in revenues over ten years, and the “Better Way” and Trump tax plans cost even more. Many Republican lawmakers in Congress and President Trump have repeatedly cited the existing projected growth in debt to justify their budget proposals for deep spending cuts in programs like Medicaid and SNAP that help families afford basic needs, and to domestic investments like education. Revenue-losing tax cuts for the wealthy would put these priorities under an increased threat of future cuts. These priorities are vital to the broad population and to the economy; cutting them would leave workers and low- and middle-income Americans worse off — picking up the check for tax cuts for high-income households.

Finally, my testimony notes that some Republicans may use budget gimmicks or other misleading arguments to obscure or explain away their tax plans’ revenue and distributional effects. These fall into two main categories: (1) attempts to use budget gimmicks to make the official estimates look better; and (2) using misleading arguments to try to explain away the sound, non-partisan estimates prepared by the official congressional estimators and undermine their credibility. Accounting gimmicks and misrepresenting official estimates will not alter the reality of a tax plan that would ultimately hurt, rather than help, workers. Instead, lawmakers should measure the revenue and distributional impacts of tax legislation without gimmicks and rosy assumptions. Congress should use conventional estimates prepared by its official, non-partisan scorekeepers, especially when enforcing budget rules.

I’ll now address each of these points in more detail.

Corporate Rate Cuts Go Mostly to CEOs and Shareholders, not Typical Workers

The “Better Way” tax plan would cut the corporate tax rate to 20 percent, and President Trump’s plan would cut it to 15 percent. Administration officials claim that the bulk of the benefits would flow to workers and raise their wages, because companies would invest more and increase workers’ productivity. But the evidence indicates that the bulk of corporate rate cuts go to high-income households, and only a small share flows to low- and moderate-income working families. The Tax Policy Center (TPC) estimates about 70 percent of the benefit of a corporate rate cut will flow to the top fifth of households, with one-third flowing to the top 1 percent alone.[1] (See Figure 1.)

There are two main reasons why:

- Only a modest share of corporate rate cuts flows to workers at any income level, including executives. TPC’s estimates make a reasonable mainstream assumption that about 20 percent of the value of corporate rate cuts flows to workers. The Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) — as well as Treasury’s Office of Tax Analysis — also assess the empirical research as showing that only about a quarter or less of corporate taxes fall on workers, so they would receive a quarter or less of the benefit of corporate tax cuts.[2] A major reason why is that recent research indicates that the overwhelming majority of the corporate tax base consists of “supernormal profits returns,” from sources such as monopoly pricing power. That type of income goes solely to investors, so cutting taxes on it does not help labor. [3]

- Even the modest part of a corporate rate cut that would flow to workers is skewed to high earners such as highly compensated executives and professionals. Whatever share of corporate rate cuts goes to workers likely does so in proportion to their share of total wage and salary income. That income is concentrated among high earners such as highly paid executives, lawyers, and other professionals. Thus, only a small benefit would ultimately flow to struggling workers who have been hurt most by slow wage growth in recent decades.[4]

Further, even assuming workers get any benefit of corporate tax cuts is generous:

- Any small benefit to workers will disappear if the corporate tax cuts swell deficits. The finding that some small share of a corporate rate cut flows to workers assumes that the rate cuts will be paid for. If corporate rate cuts are not offset by spending cuts or increases in other taxes, any assumed increase in domestic investment — and therefore benefit for workers in the form of higher productivity and wages — won’t be sustained.[5] The higher deficits would reduce national saving, meaning less capital would be available for investment in the economy and interest rates could rise. Higher interest rates, in turn, would reduce and ultimately reverse the increase in investment necessary for workers to gain from a corporate rate cut.

- The vast majority of workers and Americans would be worse off if corporate tax cuts are paid for with types of spending cut policies in the Administration and House Budget Committee budgets. If the rate cuts are ultimately paid for by cuts in programs that help families meet basic needs and to investments that help strengthen the economy, the vast majority of workers and Americans would be made worse off by the corporate rate cuts. I will elaborate on this point later in my testimony.

A Zero Percent U.S. Tax Rate on Corporations’ Foreign Profits Would Increase Incentives to Shift Profits and Possibly Investment Offshore

President Trump and Republican congressional leaders are now unified in proposing a “territorial tax” under which multinationals would pay no or very low U.S. taxes on their foreign profits. The policy would likely bleed tax revenue, and could hurt U.S. workers. For President Trump, this is a major reversal from his campaign promise that U.S. multinationals would face the U.S. corporate rate on their foreign profits as they are earned.

The current tax system taxes U.S.-based multinationals on a so-called “worldwide” basis, meaning that they owe U.S. tax on the income they make both at home and in other countries. The statutory corporate rate on both U.S. and foreign profits is 35 percent, but tax breaks reduce companies’ actual tax rates far below that. U.S.-based multinationals get a credit for the foreign taxes they pay on their foreign income so they aren’t taxed twice on the same income. But, unlike a pure worldwide tax system, the U.S. tax code doesn’t tax foreign profits in the year they are earned: foreign profits do not face U.S. taxes until companies “repatriate” them, so multinationals can keep foreign profits overseas to defer U.S. tax indefinitely. The incentive is particularly strong to report profits in zero-tax or low-tax “tax haven” countries, where they face little or no foreign tax, either.

A territorial tax would permanently exempt U.S. multinationals from U.S. tax on their foreign profits. (They would still face U.S. corporate taxes on their domestic profits.) A territorial tax of the sort that multinationals are lobbying for would have three main effects:

- Increased incentive to shift profits offshore. Permanently exempting U.S. multinationals’ foreign profits from U.S. tax would increase the incentive for U.S.-based multinationals to artificially report having earned their profits offshore, to get the permanent zero U.S. tax rate. The tax avoidance savings would favor profitable multinationals, especially those in industries that can easily move profits overseas, such as pharmaceuticals and software. A territorial system without strong rules to mitigate these losses could be very costly, Treasury estimates indicate,[6] and tax law experts are skeptical that it is possible to craft effective anti-avoidance rules.[7] The revenue loss would put pressure on public investments like infrastructure and education that help make U.S. workers and businesses productive.

- A zero tax rate on foreign profits would make U.S. domestic and small businesses less competitive relative to large U.S. multinationals. Large U.S. multinationals can pay tax lawyers millions in fees to find ways to report U.S. profits as being offshore in order to get the zero tax rate on “foreign” profits under a territorial system. That would give them a huge tax advantage over U.S. businesses — including small businesses — that don’t have foreign operations and can’t orchestrate complex tax avoidance maneuvers.

- Risks shifting investment offshore and lowering U.S. wages. If a lower U.S. tax rate on foreign profits were to induce U.S. corporations to move real investments offshore, it could hurt U.S. workers’ wages and productivity. As Congressional Research Service economist Jane Gravelle testified, in theory, “[a territorial system] would make foreign investment more attractive. That would cause investment to flow abroad, and that would reduce the capital which workers in the United States have, so it should reduce wages.”[8]

Proponents say a territorial tax would help U.S. firms’ “competitiveness.” The claim has little to do with overall U.S. job creation or wages for typical workers, and is not supported by the evidence:

- Evidence that U.S. multinationals are at a competitive disadvantage is thin. Territorial tax proponents claim that U.S.-based companies are at a disadvantage overseas because they, unlike companies based in territorial-tax countries, face corporate taxes on profits earned outside the country. But many of the multinationals that have lobbied for a territorial tax — such as Google, Apple, and Pfizer — are posting record profits and valuations. Nor are U.S. multinationals more highly taxed on their worldwide income than companies headquartered in other developed countries. U.S. multinationals’ average tax rates worldwide are similar to the average tax rates that corporations headquartered in other “Group of Seven” countries face.[9]

- Keeping corporate headquarters in the United States for tax purposes doesn’t mean many ordinary workers would benefit. Claims that cutting U.S. companies’ worldwide tax rate would encourage more firms to locate or keep their tax residence in the United States and thereby increase the number of high-quality jobs at U.S. corporate headquarters are dubious. Currently, whether or not companies can claim U.S. tax residence doesn’t depend on where they locate their management operations or any operations – it just depends on where the company is incorporated on paper. Even if territorial tax rules were crafted so multinationals had to locate their management operations here to claim U.S. tax residence and qualify for the U.S. territorial tax, that likely wouldn’t have a large impact on U.S. jobs. That’s because, for many firms, the quality of the U.S. infrastructure, workforce, and legal system may be a more important factor than taxes in corporate decisions on where to place company headquarters.

Meanwhile, even if a zero U.S. tax rate on multinationals’ foreign profits did increase jobs at U.S. corporate headquarters, it could come at the cost of jobs for other workers if multinationals moved investment offshore to get the zero U.S. tax rate on foreign profits. Not every worker can be a CEO or manager or provide services to corporate headquarters.

Workers Could End Up Picking Up the Tab for Corporations

Corporate rate cuts and other tax cuts that skew to wealthy households would leave workers and the majority of Americans worse off if the tax cuts are not fully offset by closing loopholes or other sources of progressive revenues, leaving low- and middle-income Americans to pick up the check for the cost of the tax cuts. President Trump’s and Republican congressional tax plans do not include sufficient proposals to scale back tax breaks or raise other tax revenue to pay for their tax cuts that are skewed overwhelmingly to the wealthy. It is also implausible that these tax cuts will supercharge the economy and so pay for a large portion of their cost. Instead, a revenue-losing tax bill would worsen the nation’s long-term fiscal outlook and would likely put at risk, either now or in the future, key programs that help American families like Medicaid and investments in areas like education, public safety, and infrastructure.

Cutting the top corporate tax rate from 35 to 20 percent, as the “Better Way” plan proposes, would lose $1.8 trillion in revenues over ten years, and cutting it to 15 percent, as President Trump proposes, would lose $2.3 trillion, TPC estimates.[10] Both these tax plans include a raft of additional tax cuts that flow to high-income households, such as: regressive individual income tax rate cuts; a special lower top tax rate for hedge funds, real estate investors, law firms, and other “pass-through” businesses; repealing the AMT; and repealing the estate tax.

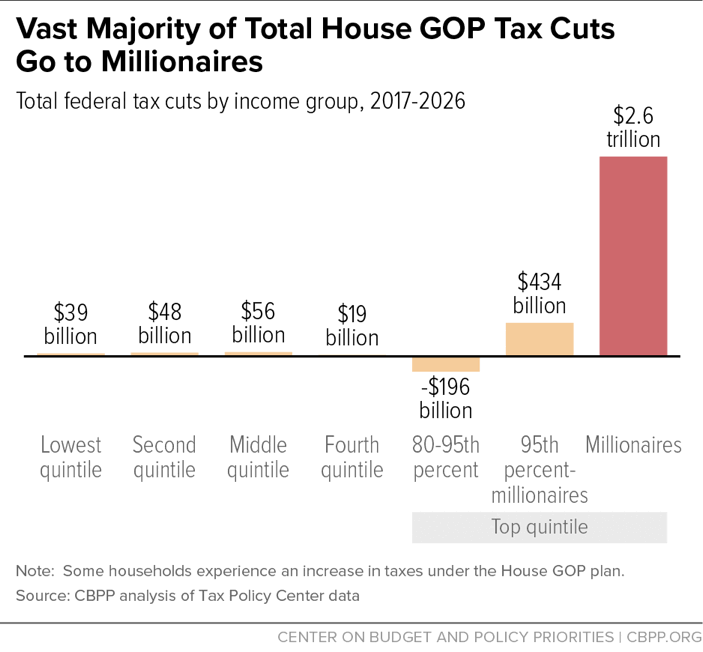

The plans do not propose sufficient revenue-raising provisions to fully offset the cost of their tax cuts. The “Better Way” plan would reduce revenues by $3.1 trillion over ten years, even counting its revenue-raising provisions, TPC estimates. Millionaires would reap 96 percent of plan’s total tax cuts in 2025, and roughly $2.6 trillion in tax cuts over the first decade (see Figure 2).[11] President Trump’s tax plan would cost between $3.5 and $7.8 trillion over ten years and would also be heavily skewed to the top, delivering net tax cuts of more than $250,000 a year to millionaires.

President Trump’s and congressional Republicans’ tax and budget plans avoid explicitly showing how they would pay for these tax cuts for the wealthy. They claim they will close loopholes and scale back other tax breaks to offset the cost of tax cuts. The specifics, however, have yet to materialize, and TPC’s estimates of the costs of these tax plans include the revenue-raisers proposed or mentioned to date (including many that have not been consistently embraced) and show revenue loss.

The plans also claim tax cuts would help pay for themselves by boosting growth. But it is implausible that large tax cuts for high-income households will supercharge growth to the extent needed to offset their high costs. In fact, using mainstream economic models and assumptions, TPC estimates that because of the adverse effect of increased deficits, by the end of ten years the “Better Way” plan would reduce economic growth.[12]

Congress may be tempted to allow revenue-losing tax proposals to be financed by cuts in entitlement programs. Since entitlements mainly benefit middle- and lower-income families while the GOP tax-cut proposals unveiled to date heavily favor high-income households and large corporations, legislation that finances large tax cuts with big entitlement cuts would represent a Robin Hood-in-reverse measure.[13]

Senate Republicans appear headed towards a budget resolution that allows a tax reconciliation bill to simply lose $1.5 trillion in revenues, increasing budget deficits. That, however, would likely only kick the budget cuts down the road, as policymakers must pay for tax cuts sooner or later. Here, too, low- and middle-income families would likely end up worse off once lawmakers cut mandatory programs that help families afford basic needs. Deficit-financed tax reform could make Medicare and Medicaid particularly vulnerable to future budget cuts, given their substantial cost and share of non-defense spending. In addition, if a revenue-losing tax cut significantly worsened the outlook for deficits and debt, those who favor substantial cuts in Social Security would likely cite that as a justification.

While President Trump and Republican leaders in Congress may try to avoid explicitly showing the tradeoff between tax cuts for the wealthy and other critical national priorities, they have made their fiscal priorities clear. Using existing predicted deficits — even before another revenue-losing tax cut — as a rationale, President Trump’s and the House Budget Committee budgets propose deep cuts to programs like Medicaid that help families afford basic needs, and to critical domestic investments that strengthen communities and the economy. For example:[14]

- The House Budget Committee budget would cut $4.4 trillion over ten years from mandatory programs that help families meet basic needs, including cuts to Medicaid and Medicare, income assistance for working-poor and other struggling families, basic food assistance, and assistance for students to go to college. These cuts would make it harder for millions of Americans to afford food, health care, and a college education.

- The Administration’s budget and the House Budget Committee budget would cut non-defense discretionary (NDD) programs below the already inadequate sequestration levels. NDD funds key investments including education, job training, scientific and medical research, infrastructure, and other programs that promote economic growth and support domestic businesses, as well as an array of vital public services.[15] The House Budget Committee budget would cut more than $1 trillion over the next decade from NDD. By 2027, total NDD funding would be 44 percent below its 2010 level, after adjusting for inflation, and — measured as a share of the economy — spending on this area of the budget would fall to its lowest level since before the Great Depression. The Trump budget cuts NDD more deeply.

- The President’s budget would weaken federal support for infrastructure in the long run by reducing Highway Trust Fund spending, cutting discretionary infrastructure investments, and shifting costs to states and localities. The Trump budget proposes a bait-and-switch on infrastructure, by offering a temporary boost in funding but then limiting Highway Trust Fund spending to the dedicated revenues it receives, starting in 2021. That means significant cuts in Highway Trust Fund spending that would grow over time, reaching $20 billion a year by the end of ten years and extending indefinitely.[16]

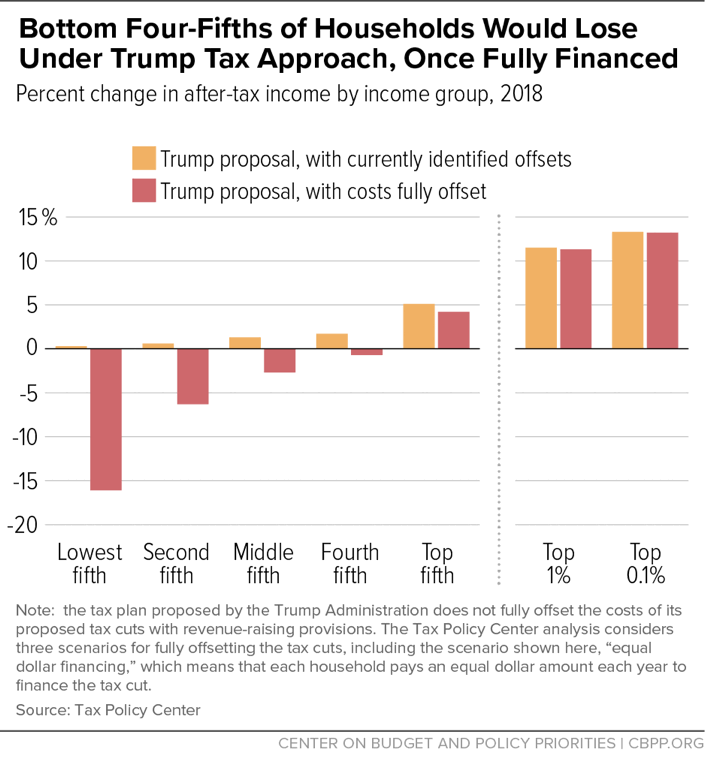

If Republican tax cut plans were ultimately paid for with the types of spending cuts in their budgets, the vast majority of workers and other low- and middle-income Americans would be net losers, even though they might get some small share of the initial tax cuts. A new TPC analysis illustrates this using President Trump’s tax plan. If its cost is paid for through the types of spending cuts the President proposed in his 2018 budget, the vast majority of Americans would be net losers, the TPC analysis indicates:[17]

- Essentially every household in the bottom two-fifths of the income spectrum (those with after-tax incomes currently averaging $22,510) would be “net losers,” losing more from the offsets than they would gain from the tax cuts. On average, they would lose more than $2,000 in after-tax income. (See Figure 3.)

- Households in the middle fifth of the income spectrum (with after-tax incomes currently averaging $57,720) would lose an average of $1,500 once the full financing costs are considered. Nearly all — 94 percent — of these households would be net losers.

- Even once the tax cuts are fully offset, the highest-income households would reap enormous gains. The top 0.1 percent would gain $935,000 on average. Their after-tax incomes would rise by 13.2 percent. Virtually every household in the top 0.1 percent would gain.

- Altogether, 84 percent of households would be net losers. That greatly exceeds the 19 percent of households that are shown to lose when the costs of the tax cuts are only partly offset.

To protect workers and other low- and middle-income Americans from paying for tax cuts for corporations and the wealthy, either now or in the future, any budget resolution should require any tax bill that proceeds through the partisan reconciliation process not lose revenues, at an absolute minimum. Workers and other low- and moderate-income Americans should not have to pick up the check for corporations and high-income Americans.

Gimmicks and Excuses to Obscure Revenue Losses and Tax Cuts for the Wealthy

Rather than admit that revenue-losing tax cuts add to deficits and threaten critical programs in the future, some Republican lawmakers appear to be prepared to try to obscure those outcomes by gaming or dismissing credible official estimates, in two main ways:

- Budget gimmicks to try to make the official estimates look better. Some lawmakers might try to use accounting tricks to try to make the official revenue and distributional estimates that the non-partisan JCT and CBO produce appear more favorable to their eventual tax cut bill. Examples include:[18]

A “current-policy” baseline that could pave the way for more than $400 billion in unfinanced tax cuts over ten years in the next tax bill. That’s the cost of making permanent dozens of corporate and individual tax provisions that Congress has scheduled to expire or that have already expired under current law. The standard “current-law” baseline assumes that time-limited tax breaks will expire on schedule, but the “current-policy” baseline envisioned by some lawmakers assumes Congress will extend them permanently. So, under a current-policy baseline, extending these tax breaks is portrayed as having no cost.[19]

That logic is flawed and has serious repercussions. When policymakers first enacted these tax cuts on a temporary basis, cost estimates assumed they would remain temporary. Switching to a current-policy baseline now would mean never counting the cost of making them permanent. This approach would allow lawmakers to routinely enact temporary tax cuts in the future, merely count the temporary costs, and later make the tax cuts permanent as if that had no additional cost: adding to deficits without ever having to show the full cost. It also ignores Congress’ intent in negotiating a tax package at the end of 2015 tax to make many so-called “tax extenders” permanent while letting others expire or phase out, or be offset with other revenues if later extended.

- Dynamic scoring. House Republicans have changed House rules to require JCT to use “dynamic scoring,” and thereby incorporate into official estimates highly uncertain estimates of the impact of tax policy changes on economic growth. Given the country’s fiscal pressures and the high degree of uncertainty surrounding dynamic scoring, lawmakers should not use it to try to make the cost of a tax-cut bill appear smaller.[20]

- Timing and other gimmicks. Lawmakers also shouldn’t use other gimmicks to hide the cost or distributional impact of tax cuts, such as by making them temporary even though policymakers fully intend to make them permanent later, or by using timing shifts (in, for instance, the tax treatment of retirement accounts) in order to accelerate revenue from future decades into the coming decade and thereby make a tax cut appear less costly and more progressive than it will be over the long run.[21]

Misleading arguments to undermine the credibility of — or explain away — estimates produced by non-partisan official scorekeepers. Instead of trying to game the official score that JCT will produce, lawmakers could use standard JCT estimates to set and enforce budget targets for a tax bill — but try to explain away estimates showing large deficit increases and tax cuts skewed toward the rich by telling the public that they are not credible and should be discounted or ignored.

For example, it has been reported that a group of senators have agreed that the budget resolution should allow a tax bill that loses up to $1.5 trillion in revenues to proceed through reconciliation. It currently appears to be their intention that in the Senate, for the purposes of determining whether a bill met that target, JCT would provide an estimate using a current-law baseline and conventional scoring methods. But some Senate Republicans appear prepared to argue that for the purposes of assessing whether the bill is sound policy, the JCT estimate should be ignored.

The reasoning appears to be that the eventual JCT estimate would count the cost of making expiring tax breaks permanent, and would not likely match some Republicans’ expectations that a tax bill — yet to be written — would produce a huge and implausible $1 trillion in revenues from growth. These “current-policy” and “dynamic scoring” arguments are just as flimsy when used purely for PR purposes — when trying to explain away an unfavorable JCT estimate — as they would be if lawmakers attempted to use them as accounting tricks baked into the official JCT cost estimate.

Some lawmakers may also try to take to explain away or undermine a JCT estimate by:

Questioning the credibility of non-partisan official estimators and pointing to other estimates that use assumptions far outside the mainstream. To undermine CBO’s cost and coverage estimates of their Affordable Care Act repeal bills, Administration officials and Republicans in Congress criticized them baselessly, with Senator John Cornyn, for example, calling the CBO estimates “fake news.”[22] Some lawmakers may try similar tactics with JCT’s estimates of the cost and distribution of a tax bill. For example, last week, Senator Bob Corker suggested that JCT estimates were insufficient,[23] and Senator Orrin Hatch, in discussing a tax bill, said of CBO, “They’re wrong about everything.”[24]

The Trump Administration may provide alternative estimates for the cost and distribution of tax legislation that some Republican lawmakers may use to sell their eventual tax bill, even if CBO and JCT estimates are used to enforce budget rules. Senator Ted Cruz has noted approvingly that the Administration is preparing to do its own estimates of the impacts of tax reform, and suggested that by contrast, CBO and JCT estimates were “funny numbers.”[25] Treasury Secretary Steven Mnuchin has also said that the Administration will provide its own estimates of any tax plan.

Administration estimates could rely on assumptions that lie far outside the mainstream. For example, Secretary Mnuchin has repeatedly claimed that a much higher share of the corporate tax flows to workers than mainstream economists believe to be the case — including the career staff at Treasury. If Administration estimates incorporated such assumptions, they would show that corporate tax cuts are less regressive than JCT estimates.[26] The Trump Administration’s 2018 budget also used very rosy and unrealistic assumptions about economic growth — and the gap between the Administration’s estimate and CBO’s was unprecedented.[27]

Lawmakers may also point to estimates produced by other organizations, which could also be based on unrealistic assumptions that fall far outside the economic mainstream.[28] By contrast, CBO and JCT are institutions that exist for the very purpose of delivering credible, objective non-partisan estimates, drawing on the expertise of independent, non-partisan professional staff. As a letter by former CBO directors appointed under both Republican and Democratic congressional majorities recently explained:[29]

To meet the standard of nonpartisan objectivity, CBO makes no recommendations about policy, regularly consults with researchers and practitioners with a wide range of views (as can be seen in the agency’s panels of advisers and reviewers for major studies), and enhances its transparency by releasing extensive descriptions of its analytic techniques and forecast record. To produce estimates of high quality, CBO uses its detailed understanding of federal programs and economic conditions, ongoing interactions with government officials and private-sector experts, the best academic research, and the latest available data consistent with the timing of the Congressional budget process.

Ignoring huge corporate tax cuts and other tax cuts that flow to the wealthy. As noted above, cutting the corporate tax rate would deliver large tax cuts overwhelmingly high-income households. So would repeal of the estate tax, and the special rate cut for “pass-through businesses” (including private equity funds and law firms) that are part of the “Better Way” and Trump tax plans.

Secretary Mnuchin has sometimes tried to ignore the large net tax cuts for the wealthy that such tax cuts would deliver, by focusing on only the effects of lowering the top individual income tax rate (and reducing tax breaks the individual income tax) in claiming that Republican tax plans won’t offer tax cuts for high-income Americans.[30] However, the highly regressive effects of these business tax cuts must be counted in evaluating the winners and losers of tax plans, as well as other tax cuts that disproportionately benefit the very top such as repeal of the estate tax. JCT distribution tables would show the impact of such tax cuts, and lawmakers should not attempt to point to calculations or other analyses that do not.

- Not getting full analyses in time. As we have seen in their attempts to repeal the Affordable Care Act, many Republican lawmakers have been willing to vote on legislation without a full analysis of its impacts from the CBO. No tax legislation should be voted on without securing and analyzing a JCT analysis of not only a bill’s revenue impacts, but also a JCT distribution analysis that shows how the bill would affect filers at different parts of the income distribution, and JCT’s estimates of the growth impacts of the plan. Policymakers should have this full range of information at their disposal before making decisions about the tax plan.

End Notes

[1] James R. Nunns, “How TPC Distributes the Corporate Tax,” September 13, 2012, http://tpc.io/2wtQLzA; TPC tables T17-0179 and T17-0180, http://tpc.io/2rUNxRC. This section draws from Chye-Ching Huang and Brandon DeBot, “Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims: Eventual Spending Cuts or Tax Increases to Pay for Corporate Rate Cuts Could Leave Most Workers Worse Off,” CBPP, August 16, 2017, http://bit.ly/2ue6Czp.

[2] CBO, “The Distribution of Household Income and Federal Taxes, 2008 and 2009,” July 2012, http://bit.ly/2uKeDzs; CBO, “The Distribution of Household Income and Federal Taxes, 2013,” June 2016, http://bit.ly/2vDk0N9; JCT, “Modeling the Distribution of Taxes on Business Income,” JCX-14-13, October 16, 2013, http://bit.ly/2ubvvxh. U.S. Department of the Treasury, Office of Tax Analysis, “Treasury’s Distribution Methodology and Results,” November, 12, 2015, http://bit.ly/2uDAwiT, and Distribution of the Tax Burden, Current Law, 2018, from http://bit.ly/2uE01Ro.

[3] See Laura Power Nunns and Austin Frerick, “Have Excess Returns to Corporations Been Increasing Over Time?” Treasury Office of Tax Analysis Working Paper 111, November 2016 http://bit.ly/2vxCYoJ; Eric Toder and Kim Rueben, “Should We Eliminate Taxation of Capital Income?” in Henry J. Aaron, Leonard Burman, and C. Eugene Steuerle (eds.), Taxing Capital Income, 2007.

[4] The standard assumption is that workers can freely move between businesses that pay the corporate tax and those that do not, so if corporations invest more and pay higher wages, workers will move from non-corporate jobs into corporate jobs until wages equalize between the two types of businesses.

[5] For example, a 2005 JCT analysis of a hypothetical $500 billion corporate tax cut that is not paid for found that over time “[g]rowth effects eventually become negative without offsetting fiscal policy for each of the proposals, because accumulating Federal government debt crowds out private investment.” Long-run impacts on employment were either close to zero or negative, depending on monetary policy assumptions. JCT, “Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief,” JCX-4-05, March 1, 2005, p.8, http://bit.ly/2wtn8OL.

[6] This section draws from Chye-Ching Huang, Chuck Marr, and Joel Friedman, “The Fiscal and Economic Risks of Territorial Taxation,” CBPP, January 31, 2013, http://bit.ly/2gtMXFj.

[7] See David Van Den Berg, “Territorial Tax Systems Can Be Beaten, Shay Says,” 223 Tax Notes 7, November 16, 2012. Also see Steven Shay, “Unpacking Territorial”, New York University School of Law, 2012, http://bit.ly/2eQviaK.

[8] Jane G. Gravelle, Senior Specialist in Economic Policy, Congressional Research Service, before the House Ways and Means Committee, May 12, 2011, http://bit.ly/2riMIk3.

[9] See, “Actual U.S. Corporate Tax Rates Are in Line with Comparable Countries,” CBPP, April 25, 2017, http://bit.ly/2wB8bsa.

[10] James R. Nunns et al., “An Analysis of the House GOP Tax Plan,” TPC, September 16, 2016 http://tpc.io/2iyFHHj; “The Implications of What we Know and Don’t Know About President Trump’s Tax Plan,” TPC, July 13, 2017, http://tpc.io/2wxs0km.

[11] CBPP analysis based on Page, “Dynamic Analysis of the House GOP Tax Plan: An Update.” See Isaac Shapiro, Chye-Ching Huang, and Richard Kogan, “House GOP Framework Would Give Millionaires $2.6 Trillion in Tax Cuts, While Cutting Programs for Low- and Moderate-Income People by $3.7 Trillion,” CBPP, September 29, 2016, http://bit.ly/2deCtbe.

[12] Nunns et al. TPC’s macroeconomic analysis of the Trump Administration tax plan also found that it would reduce growth by the end of the decade: see “The Implications of What We Know and Don’t Know about President Trump’s Tax Plan.”

[13] Brandon DeBot, “Harsh Trade-off at Core of GOP Health Bill: Keep Medicaid Expansion or Cut Taxes for Wealthy?,” CBPP, June 21, 2017, http://bit.ly/2w9s1NI; Brandon DeBot, “Wealthy, Corporations Still Win Big Under Senate GOP Health Bill Even With Possible Change,” CBPP, June 30, 2017, http://bit.ly/2uYFLXG.

[14] This section draws from Robert Greenstein, “Harsh House GOP Budget Resolution Asks Most from Those Who Have Least”, CBPP, July 18, 2017, http://bit.ly/2uwt35B.

[15] See CBPP, “Trump Budget’s Radical, Harmful Priorities,” and Joel Friedman, “Black’s Lopsided Budget Is a Dead End for Appropriations,” CBPP, June 26, 2017, http://bit.ly/2u9qKVr.

[16] Jacob Leibenluft, “Trump’s Bait and Switch on Infrastructure,” CBPP, June 7, 2017, http://bit.ly/2tJs5QM.

[17] William G. Gale, Surachai Khitatrakum, and Aaron Krupkin, “Cutting taxes and making future Americans pay for it: How Trump’s tax cuts could hurt many households,” TPC, August 15, 2017, http://brook.gs/2x83DsO. This section draws from Isaac Shapiro and Chye-Ching Huang, “Vast Majority of Americans Would Likely Lose From Trump Tax Cuts, Once They’re Paid For,” CBPP, August 17, 2017, http://bit.ly/2wXMDGr.

[18] For further discussion of the current policy and other gimmicks, see: Chuck Marr, Chye-Ching Huang, and Brendan Duke, “Tax Plans Must Not Lose Revenue and Should Focus on Raising Working-Class Incomes,” CBPP, September 8, 2017 http://bit.ly/2wNEVkR; Seth Hanlon, “Tax Reform Must Be at Least Revenue-Neutral and Avoid Gimmicks,” Center for American Progress, September 22, 2017, http://ampr.gs/2wOUglV.

[19] Chye-Ching Huang and Brandon DeBot, “‘Current Policy’ Baseline Would Hide $439 Billion in Tax Cuts Worth at Least $40,000 a Year for the Top 0.1 Percent,” CBPP, August 16, 2017, http://bit.ly/2fSXoWa.

[20] Paul N. Van de Water, “Budget and Tax Plans Should Not Rely on ‘Dynamic Scoring,’” CBPP, November 17, 2014, http://bit.ly/2vKC4aW.

[21] For examples of timing gimmicks considered in prior tax debates, see: Chye-Ching Huang, Chuck Marr, and Nathaniel Frentz, “Timing Gimmicks Pose Threat to Fiscally Responsible Corporate Tax Reform,” CBPP, January 13, 2014, http://bit.ly/2uPKCP8; Nathaniel Frentz and Chye-Ching Huang, “Four Timing Gimmicks That Could Disguise Fiscally Irresponsible Individual Tax Reform,” CBPP, October 30, 2013, http://bit.ly/2vQylau.

[22] See: Rudolph. G. Penner, “The Attacks on the Congressional Budget Office are Wrong,” June 23, 2017, TaxVox, http://tpc.io/2tcadzN; Aviva Aron-Dine, “CBO Correctly Predicted Historic Coverage Gains Under ACA,” CBPP, May 30, 2017, http://bit.ly/2xA05Cu.

[23] See Alan Rappeport, “In Battle Over Tax Cuts, It’s Republicans vs. Economists,” New York Times, September 22, 2017, http://nyti.ms/2xmSl7C, reporting that “Senator Bob Corker, […] seemed to throw down the gauntlet this week, saying he would push for a pro-growth tax overhaul that pays for itself using “valid models.” He singled out the Joint Committee on Taxation in comments to reporters, suggesting that Republicans would be looking beyond their analysis when assessing the plan’s cost. Mr. Corker […] said that the experience of working with the Congressional Budget Office during Republican efforts to repeal the Affordable Care Act buttressed his view that analyses from economists outside the government should be considered when scoring tax legislation.”

[24] As reported by Alan Rappeport, September 19, 2017, http://bit.ly/2xmvV6r.

[25] Senator Cruz, “Tax Reform Should Focus on Creating More Jobs, Higher Wages, and More Opportunity,” “Talking Tax Reform” hosted by the Tax Foundation, September 13, 2017, http://bit.ly/2f5zqXR.

[26] Huang and DeBot, “Corporate Rate Cuts Skew to Shareholders and CEOs.”

[27] Chad Stone, “Gap Between Trump, CBO Predictions on Economic Growth the Largest on Record, http://bit.ly/2tMwQKL.

[28] Chad Stone and Chye-Ching Huang, “Trump Campaign’s “Dynamic Scoring” of Revised Tax Plan Should Be Taken With More Than a Grain of Salt, Relies on Assumptions Well Outside the Mainstream,” CBPP, September 15, 2016, http://bit.ly/2wJRRZI.

[29] Letter from Former CBO Directors on the Importance of CBO’s Role in the Legislative Process, July 21, 2017, http://bit.ly/2vIvqiQ.

[30] Andrew Soergel, “Mnuchin: ‘Most’ Top Earners Won't Get Tax Cut Under Trump Plan,” U.S. News & World Report, July 31, 2017, http://bit.ly/2wOmk96.

More from the Authors