The President’s Proposal to Make Tax Cuts Permanent

$2.2 Trillion Cost Poses Danger to Economy in the Long Run

In his State of the Union address, the President announced his intention to propose to make permanent a range of tax cuts that are scheduled to expire by the end of 2010. Last year’s budget featured a similar proposal. Since then a new round of tax cuts has become law — including the reduction in the tax rates on dividends and capital gains — which increases the cost of making the tax cuts permanent. The cost has risen to a very high level — approximately $2.2 trillion over the next 10 years, including the costs of the higher interest payments that would have to be paid on the national debt.[1]

This large cost will add substantially to the budget deficits the nation faces. A number of analyses by respected institutions and leading economists — including studies by the Congressional Budget Office, the Joint Committee on Taxation, and economists at Brookings — find that the increased deficits the tax cuts will create will reduce national saving and may weaken the economy over the long run as a result. These studies do not support Administration claims that the tax cuts will significantly increase long-term economic and job growth.

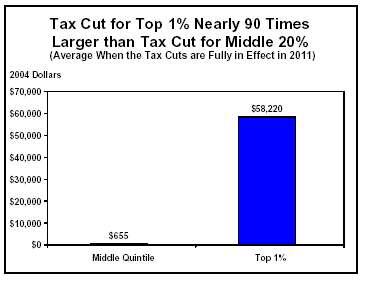

Making the tax cuts permanent would be of greatest benefit to one group — very-high-income households. Estimates based on data from the Urban Institute-Brookings Institution Tax Policy Center show that if the tax cuts are made permanent — including estate tax repeal — the top one percent of households will gain an average of $58,200 a year (in 2004 dollars) when the tax cuts are fully in effect, reflecting a 7.3 percent change in their after-tax income. By contrast, people in the middle of the income spectrum would secure a 2.5 percent change in their after-tax income, with average tax cuts of $655 — a little more than one-ninetieth of what those in the top one percent would receive. The cost to middle- and low-income households from making the tax cuts permanent — from the higher costs they may pay for various services if increasingly large budget cuts are instituted to help pay for the tax cuts, as well as from the higher interest rates and other possible adverse economic effects of the enlarged deficits — is likely to outweigh the modest tax cuts that many of these households would receive.

It also should be noted that the cost of making permanent the key middle-income tax cuts of the past three years — the increase in the child tax credit, the tax cuts for married filers, and the creation of the new 10 percent tax bracket — would be just over one-fifth the cost of making all of the tax cuts permanent.

This analysis looks at three issues related to making the tax cuts permanent: the cost of the policy, its likely impact on the economy, and who would benefit from it.

The High Cost Involved

Since the Administration took office, three tax-cut packages have been enacted. All of the tax-cut measures in these packages are scheduled to expire at some point between 2004 and 2010; these artificial sunsets were one of the devices that masked the tax cuts’ long-term cost. The Administration is now proposing to make nearly all of these tax cuts permanent; the Administration also has called for extending various temporary tax breaks that were initially enacted before the Administration took office, such as the research and experimentation credit, which is scheduled to expire in June 2004.

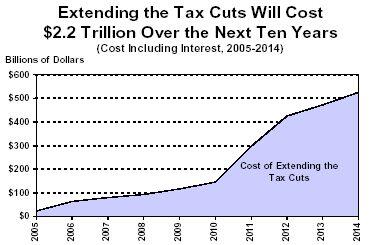

- The revenue loss associated with making permanent all of the tax cuts the Administration has indicated it wishes to extend totals $1.9 trillion over the ten years from 2005 through 2014, based on estimates from the Joint Committee on Taxation and the Congressional Budget Office. The higher interest payments that would have to be paid on the national debt would add another $313 billion to the cost, bringing the total effect on the deficit over the next ten years to $2.2 trillion.[2]

- The $2.2 trillion figure reflects the cost of making permanent all of the tax cuts enacted in the last three years except the bonus depreciation tax break for business, a deduction for higher education expenses, and the “savers credit;” the Administration has not yet indicated whether it will propose to make these three measures permanent. The $2.2 trillion figure includes the cost of extending relief from the Alternative Minimum Tax, which expires at the end of 2004. The Administration has repeatedly said it plans to propose ongoing AMT relief, although not until next year’s budget. Finally, the $2.2 trillion figure includes the cost of extending a series of tax credits and other popular tax breaks that come up for renewal every few years and always are extended on a bipartisan basis. The Administration has proposed extending these tax breaks whenever they have come up for renewal. (See box below.)

- More than 80 percent of this $2.2 trillion cost would be incurred during the second half of the decade, from 2010 through 2014. This reflects the proposed elimination of the 2010 sunsets that were written into the 2001 tax-cut legislation. By 2014, the cost (with interest) of making these tax cuts permanent would approach more than $500 billion a year. This indicates that the cost in the following decade would be more than twice the cost in the current decade.

The Impact on the Economy

The Administration contends that making the tax cuts permanent is necessary to spur long-term economic growth and create jobs. These claims are highly dubious; because of the effect of the tax cuts in enlarging the deficits, the tax cuts are more likely to reduce long-term economic growth than to increase it.

The nation faces a serious deficit problem, which permanent extension of the tax cuts would make markedly worse. A recent analysis by the Center on Budget and Policy Priorities finds that budget deficits are likely to total $5.2 trillion over the ten years from 2005 to 2014. Other analysts have reached similar conclusions. For example, Brookings economists estimate the deficits at $5.5 trillion over the same period. [3] Deficits then would rise to still higher levels in decades after that.

Of particular note, a growing number of analyses of the tax cuts prepared by respected institutions and leading economists have found that because of the impact of the tax cuts on the deficit, the tax cuts are more likely to have a long-term negative effect on the economy than a positive effect. These studies explain that the net effect of tax cuts on the long-term growth will reflect the combination of any positive effects on economic incentives and negative effects from larger deficits. These analysts have concluded that the positive effects on economic growth from reduced marginal tax rates will be cancelled out — and may well be outweighed — by the negative effects from the greatly enlarged deficits.

For example, the Congressional Budget Office concluded that the tax cuts “will probably have a net negative effect on saving, investment, and capital accumulation over the next 10 years.”[4] The Joint Committee on Taxation, when analyzing the 2003 tax cuts, found that the effects of the increasing deficits eventually are likely to outweigh the positive effects of the tax cuts.[5] Analyses by economists at institutions such as Brookings and the Federal Reserve have produced similar conclusions. [6]

These analyses explain that higher deficits reduce national saving and thus result in less domestic investment (and more borrowing from overseas). Expectations of persistently high future deficits also can raise long-term interest rates. Such outcomes lower the nation’s future income and standard of living.

The large long-term deficits the United States faces are stirring mounting concern. A report the International Monetary Fund released earlier this month scolded U.S. policymakers in terms usually reserved for third-word countries that have unstable fiscal policies. [7] As the New York Times reported, “. . . the [IMF] report sounded a loud alarm about the shaky fiscal foundations of the United States, questioning the wisdom of the Bush administration’s tax cuts and warning that large budget deficits pose ‘significant risks’ not just for the United States but for the rest of the world.” [8]

Similarly, a new analysis by former Treasury Secretary Robert Rubin, Brookings Institution economist Peter Orszag, and Wall Street economist Allen Sinai warns that “the scale of the nation’s projected budgetary imbalances is now so large that the risk of severe adverse consequences must be taken very seriously, although it is impossible to predict when such consequences may occur.” Rubin and his colleagues warn that the budget deficits we face if we remain on our current policy course — by making the tax cuts permanent and continuing other tax and spending policies — could lead to “financial and fiscal disarray” and cause a “fundamental shift in market expectations and a related loss of confidence at home and abroad.” While it is impossible to know at what point this change in market expectations might take place, Rubin and his colleagues observe that once it occurs, it would “magnify the costs associated with any given underlying budget deficit and depress economic activity much more than the conventional analysis would suggest.” [9]

Other Administration Arguments for Making the Tax Cuts Permanent

In his State of the Union speech, the President nevertheless declared: “For the sake of job growth, the tax cuts you [the Congress] passed should be made permanent.” The President also said the tax cuts have been essential to recent economic growth. In addition, he and other members of the Administration have argued in recent days that making the tax cuts permanent will create “certainty” about the tax code, thereby sustaining the economic recovery.

These arguments do not stand up well under scrutiny. The tax cuts appear to have played only a modest role in the recent economic growth; an analysis by Economy.com found that about 12 percent of the growth in the third quarter of 2003 was due to the tax cuts. [10] ]Factors other than the tax cuts appear to be more important in driving the economic recovery. In addition, making the tax cuts permanent would have little impact on jobs in the coming year (i.e., in 2004) while the job market is still weak, since nearly all of the tax cuts already are scheduled to remain in effect throughout this year.

Brookings Economists Respond to Claims that Extending the Tax Cuts is Necessary to Maintain Economic Growth

In a new analysis,[11] Brookings economists William Gale, Matthew Hall, and Peter Orszag offer the following observations on claims that making the tax cuts permanent is essential for the economy:

“Is extension of the expiring provisions necessary to ensure economic prosperity? In the short run, the answer is clearly no. Reducing taxes in 2014 can actually hurt the economy today because financial markets are forward-looking; larger projected deficits in 2014 can therefore raise interest rates today. In the long run, the answer is also clearly no. The tax cuts themselves may have a modest positive effect on the economy, but they also increase the budget deficit, which has a negative effect on the economy. The net effect, according to a variety of estimates noted above, is likely to be negative, not positive, in the long run.

“The Administration has also claimed that the tax cuts need to be made permanent to reduce the uncertainty that taxpayers face. This argument is misleading. Making the tax cuts permanent would not help resolve the fundamental uncertainty about future tax rates or future policy. The reason is that the true underlying source of uncertainty in fiscal policy is how the fiscal gap is going to be closed — what combination of revenue increases and spending cuts will be used. Enacting another fiscally unsustainable policy (making the tax cuts permanent) on top of the already unsustainable fiscal situation does not make the situation more stable, only less so.”

Moreover, while the tax cuts have made some contribution to recent economic growth, this contribution has come at a high cost. The same level of fiscal stimulus could have been achieved more efficiently. Economic research shows that high-income households are less likely to spend the tax cuts they receive than low- and middle-income households. As analyses issued by Economy.com and the Congressional Budget Office suggest, tax cuts targeted heavily on high-income households — as the Bush tax cuts have been — provide less immediate stimulus to the economy than tax cuts targeted on other households or increases in certain programs such as unemployment insurance.

Finally, making the tax cuts permanent could create more uncertainty in financial markets, because of the large and unsustainable increases in deficits such a policy would engender. Policies rooted in fiscal discipline, rather than unaffordable tax cuts that enlarge high deficits, are more likely to be sustainable over the long run and thus to lead to the type of certainty about the fiscal environment that encourages desired levels of investment and economic growth. Both the recent paper by Rubin and his colleagues and the IMF report emphasize the uncertainty in financial markets that continuing current fiscal policies — of which the tax cuts are a large part — risks exacerbating.

Estimates of the Cost of Making the Tax Cuts Permanent

In his State of the Union speech, the President did not specifically identify all of the tax cuts his administration is proposing to make permanent. For purposes of this analysis, the following assumptions were made.

- With three exceptions, all of the tax cuts enacted in 2001, 2002, and 2003 that are scheduled to expire between now and 2010 would be extended. The three exceptions are: the 50-percent bonus depreciation provision, which allows businesses to write off half of new investments in equipment and which expires at the end of 2004; the “above-the-line” deduction for higher education expenses, scheduled to expire at the end of 2005; and the low-income savers credit, which expires at the end of 2006. The Administration has not yet indicated whether it favors making any of these three tax cuts permanent.

- Relief from the Alternative Minimum Tax, set to expire at the end of 2004, would be extended. The Administration has consistently said it favors extending AMT relief and will propose ongoing AMT relief in 2005. To estimate the cost of continuing AMT relief, this analysis uses the CBO estimate of the cost of a form of AMT relief that is consistent with extending the current type of relief, and that is likely to be the least costly version of AMT relief the Administration considers. This particular form of AMT relief (the form CBO featured in its most recent report on the budget outlook, issued in January 2004) entails indexing the AMT parameters currently in place and continuing the current AMT treatment of non-refundable personal credits.

- A number of temporary tax cuts initially enacted before the Bush Administration took office would be extended. The Administration has explicitly endorsed making permanent some of these “extenders,” such as the research and experimentation credit. The Administration has supported a short-term extension of the other tax breaks in this category each time that they have been scheduled to expire, a position that prior Administrations and most Members of Congress of both parties traditionally have taken as well. The Administration has given no indication it intends to depart from this tradition and to call for allowing some of these tax-cut measures to expire.

The estimates of the cost of extending these tax cuts reflect CBO estimates from its January 2004 report on the budget and economic outlook. As noted in the text, the total cost, including the increased interest payments involved, is $2.2 trillion between 2005 and 2014.

The total would be $644 billion higher if the cost of making permanent the bonus depreciation provision, the education deduction, and the savers credit were included. These three provisions have strong supporters in Congress, and there is likely to be significant pressure to extend them, even if their extension has not been officially endorsed by the Administration. If all tax cuts set to expire between now and 2010 were extended, the cost would be $2.9 trillion including interest.

Who Would Receive the Tax Cuts?

The Urban Institute-Brookings Institution Tax Policy Center has analyzed who will benefit from the tax cuts in 2011 if they are made permanent. (All of the tax cuts would be fully in effect in 2011, including repeal of the estate tax.)

- The one percent of households with the highest incomes would receive nearly one-third of the tax cuts.[12] [11]This amounts to an average tax cut of $58,220 for members of this group. (All figures here are expressed in 2004 dollars and reflect the effects of making permanent both the individual income tax cuts and estate tax repeal.)

- The top five percent of households would receive 47 percent — or nearly half — of the tax cuts, a larger share than the bottom 90 percent of households would receive.

- Households in the middle fifth of the income spectrum would receive just over 7 percent of the tax cuts; they would get an average tax cut of $655.

- The top one percent would see its after-tax income grow by 7.3 percent as a result of the tax cuts.[13] ] In contrast, the after-tax incomes of those in the middle of the income spectrum would grow by only 2.5 percent.

The Administration often emphasizes the benefits of its tax cuts for middle-class families with children. These families, however, typically benefit from only three of the tax-cut provisions — the increase in the child tax credit to $1,000, the creation of the 10 percent tax bracket, and tax relief for married couples. These three provisions account for just over one-fifth (22 percent) of the cost through 2014 of making all of the tax cuts permanent. This could be extended for a fraction of the cost of making all of the tax cuts permanent.

End Notes

[1] In the previous version of this paper (revised January 23, 2004), the cost of extending the tax cuts was estimated to be $2.5 trillion, including interest. The $2.2 trillion estimate in this paper is lower because it incorporates CBO data from its new January 26, 2004 report, reflecting the impact of its new projection of lower inflation over the decade.

[2] The Administration’s budget will not show the $2.2 trillion amount, largely because the budget is not expected to include the cost of extending relief from the Alternative Minimum Tax beyond 2005. Current AMT relief expires at the end of 2004. Although the Administration has stated its intention to prevent the number of taxpayers subject to the AMT from climbing from about 2.5 million today to 29 million by the end of the decade, as will happen if relief is not extended, the Administration has omitted the ten-year cost of such relief from its budgets, stating it will present a proposal for ongoing AMT relief in the budget it presents a year from now. For a discussion of other costs that the Administration is likely to leave out of its budget, see Richard Kogan, “Will the President’s 2005 Budget Really Cut the Deficit in Half?,” Center on Budget and Policy Priorities, revised January 21, 2004.

[3] Richard Kogan, David Kamin, and Joel Friedman, “Deficit Picture Grimmer Than New CBO Projections Suggest,” Center on Budget and Policy Priorities, January 28, 2004. Robert Rubin, Peter Orszag, and Allen Sinai, “Sustained Budget Deficits: Longer Run U.S. Economic Performance and the Risk of Financial and Fiscal Disarray,” Brookings Institution, January 4, 2004. Alice Rivlin and Isabel Sawhill, eds., Restoring Fiscal Sanity: How To Balance the Budget, Brookings Institution, January, 2004.

[4] Congressional Budget Office, “The Budget and Economic Outlook: An Update,” August 2003.

[5] Joint Committee on Taxation, “Macroeconomic Analysis of H.R. 2, The Jobs Growth and Reconciliation Act of 2003,” Congressional Record, 2003.

[6] See: Joint Committee on Taxation, op.cit,; Congressional Budget Office, op.cit.; Douglas W. Elmendorf and David L. Reifschneider, “Short-Run Effects of Fiscal Policy with Forward-Looking Financial Markets,” prepared for the National Tax Association’s 2002 Spring Symposium; William G. Gale and Samara R. Potter, “An Economic Evaluation of the Economic Growth and Tax Relief and Reconciliation Act of 2001,” National Tax Journal, March 2002; Peter R. Orszag, “Marginal Tax Rate Reductions and the Economy: What Would Be The Long-Term Effects of the Bush Tax Cut? ” Center on Budget and Policy Priorities, March 2001; and Alan Auerbach, “The Bush Tax Cut and National Saving,” prepared for the NTA’s 2002 Spring Symposium.

[7] International Monetary Fund, “U.S. Fiscal Polices and Priorities for Long Run Sustainability,” January 7, 2004.

[8] New York Times , January 7, 2004.

[9] Rubin et. al., op.cit.

[10] Data provided by Economy.com.

[11] William G. Gale, Matthew Hall, and Peter R. Orszag, “Key Points on Making the Bush Tax Cuts Permanent,” Brookings Institution, January 21, 2004, available at http://www.brookings.edu/views/op-ed/gale/20040121taxcuts.htm

[12] See Tax Policy Center, Table T03-0150, June 3, 2003. The TPC estimates have been adjusted to excude the effects of making bonus depreciation permanent, consistent with analysis in this paper, and updated to 2004 dollars.

[13] Tax Policy Center data show that after-tax income among the top one percent of households would rise 5.1 percent as a result of making the individual income tax cuts permanent, without considering the effects of estate tax repeal.

More from the Authors