“Territorial Tax” Is a Zero Rate on U.S. Multinationals’ Foreign Profits, Threatens U.S. Revenues and Wages

Under a “territorial” tax system, U.S.-based multinational corporations wouldn’t pay U.S. corporate taxes on their foreign profits. That is, they would face a zero U.S. corporate tax rate, and such a massive, permanent tax advantage for foreign profits over domestic profits would not help the U.S. economy. It would create a powerful incentive for companies to shift profits and investments overseas, could harm many U.S. businesses and workers, and would likely increase deficits. Corporate tax reform should focus on tax policy changes that would help create jobs, reduce deficits, and raise incomes, especially for workers whose incomes have been close to stagnant while corporate profits have soared — rather than on the largely unsupported claims of U.S.-based multinationals that they are “uncompetitive” with foreign-based corporations and need a large tax cut on their foreign profits. Responsible international tax reform would reduce corporate tax avoidance and the current tax advantage that foreign profits already enjoy, and there are a number of sound ways to do that. A territorial tax moves in the opposite direction.[1]

“Territorial” Means “Zero”

The current tax system taxes U.S.-based multinationals on a so-called “worldwide” basis, meaning that they owe U.S. tax on the income they generate both at home and in other countries. The statutory corporate rate on both U.S. and foreign profits is 35 percent, but extensive tax breaks reduce companies’ actual tax rates far below that. Also, U.S.-based multinationals get a credit for the foreign taxes they pay on their foreign income so they aren’t taxed twice on the same income.

Unlike a pure worldwide tax system, the U.S. tax code doesn’t tax foreign profits in the year they are earned. Instead, foreign profits do not face U.S. taxes until companies “repatriate” them — that is, declare those profits as having been brought back to the United States. This means that multinationals can keep foreign profits overseas to defer U.S. tax indefinitely.

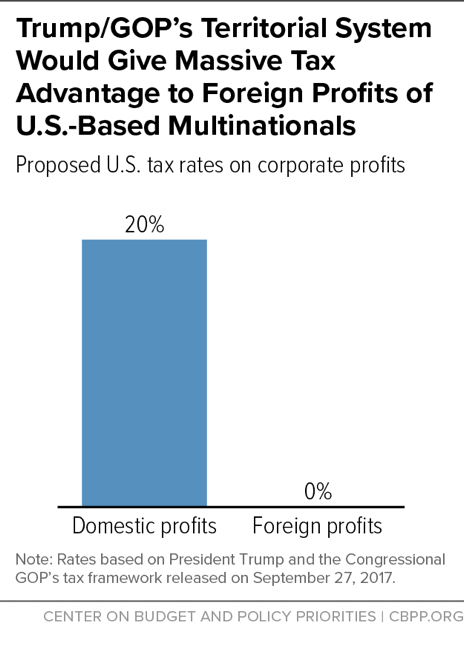

A territorial tax would exempt U.S. multinationals from tax on their foreign profits. (They would still face U.S. corporate taxes on their domestic profits.) President Trump and Republican congressional leaders have proposed a territorial tax, with a domestic corporate tax rate of 20 percent (see chart).

Powerful Incentive to Shift Profits Offshore

U.S.-based multinationals already have a strong incentive to artificially report having earned their profits offshore in order to defer paying U.S. taxes. The incentive is especially strong for multinationals to declare their profits as having been earned in zero-tax or low-tax “tax haven” countries, where the corporation would pay little or no tax to the foreign government, either. Permanently exempting U.S. multinationals’ foreign profits from tax would increase that incentive. The tax avoidance savings that corporations would reap would favor profitable U.S. multinationals, especially those in industries that can easily move profits overseas, such as pharmaceuticals and software.

Risks Shifting Investment Offshore and Lowering U.S. Wages

If a lower U.S. tax rate on foreign profits encourages U.S. corporations to move investments offshore, it could hurt U.S. workers’ wages and productivity. As Congressional Research Service tax economist Jane Gravelle testified before Congress, “[Moving to a territorial system] would make foreign investment more attractive. That would cause investment to flow abroad, and that would reduce the capital which workers in the United States have, so it should reduce wages.”

Anti-Abuse Rules Unlikely to Mitigate Revenue Loss

Adopting a territorial system would lose revenue over the long run because firms would shift profits overseas (both by changing where they report the profits on paper and by moving investments offshore) that they would otherwise report in the United States and on which they would pay U.S. tax. A territorial system without strong rules to mitigate these losses could cost roughly $130 billion over ten years, compared to the current system and tax rates, Treasury estimates. Tax experts are quite skeptical that policymakers could craft effective anti-avoidance rules. As noted international tax expert Stephen Shay has warned, “Those of us who have been doing this business for 30 years on the legal side” would find ways to avoid a territorial tax, and “When [lawmakers] don’t fully understand that and the companies come in and say it won't happen, I'm here to tell you it will happen.”

Case for Territorial Taxation Is Weak

Proponents often argue that a territorial system would improve U.S. firms’ “competitiveness.” But these claims have little to do with overall U.S. job creation or wages for ordinary workers, and are not supported by the evidence:

-

Evidence that U.S. multinationals are at a competitive disadvantage is thin. Territorial tax proponents claim that U.S.-based companies are at a disadvantage overseas because they, unlike companies based in territorial-tax countries, face corporate taxes on profits earned outside the country. But many of the large multinationals that have lobbied for a territorial tax — such as Google, Apple, and Pfizer — are posting record profits and valuations.

Nor are U.S. multinationals more highly taxed on their worldwide income than corporations with headquarters in other developed countries. U.S. multinationals’ average tax rates worldwide are similar to the average tax rates that corporations headquartered in other “Group of Seven” countries face.

- A zero tax rate on foreign profits would make U.S. domestic and small businesses less competitive relative to large U.S. multinationals. Large U.S. multinationals can pay tax lawyers millions in fees to find ways to report U.S. profits as being offshore in order to get the zero tax rate on “foreign” profits under a territorial system. That would give them a huge tax advantage over U.S. businesses — including small businesses — that don’t have foreign operations and can’t orchestrate complex tax avoidance maneuvers.

-

Keeping corporate headquarters in the United States for tax purposes doesn’t mean many ordinary workers would benefit. Claims that cutting U.S. companies’ worldwide tax rate would encourage more firms to locate or keep their tax residence in the United States and thereby increase the number of high-quality jobs at U.S. corporate headquarters are dubious. Currently, whether or not companies can claim U.S. tax residence doesn’t depend on where they locate their management operations. Even if territorial tax rules were crafted so multinationals had to locate their management operations here to claim U.S. tax residence and qualify for the U.S. territorial tax (under which profits they booked abroad were exempt from U.S. tax), that likely wouldn’t have a large impact on U.S. jobs. That’s because, for many firms, the quality of the U.S. infrastructure, workforce, and legal system may be a more important factor than taxes in corporate decisions on where to place company headquarters.

Meanwhile, even if a zero U.S. tax rate on multinationals’ foreign profits did increase the number of jobs at U.S. corporate headquarters, it could come at the cost of jobs for other workers if multinationals moved investment offshore to get the zero U.S. tax rate on foreign profits. Not every worker can be a CEO or manager or provide services to corporate headquarters.

- Finally, there’s little evidence that encouraging multinationals to expand overseas would create jobs in the United States. Some proponents argue that a territorial system would expand investment in the United States even if it also encouraged U.S.-based multinationals to invest more offshore, citing a study that finds U.S. multinationals’ investment abroad correlates with their investment in the United States. But that study does not show that firms’ overseas investment causes them to expand their domestic investment: a rise in foreign demand could cause both U.S. and foreign investment to grow at the same time. And the study itself notes that some earlier studies found that increased overseas investment by multinationals is linked to less investment in the United States.

End Notes

[1] Chye-Ching Huang, Chuck Marr, and Joel Friedman, “The Fiscal and Economic Risks of Territorial Taxation,” January 31, 2013, CBPP, http://bit.ly/2qk6nT2; Statement of Jane G. Gravelle, Senior Specialist in Economic Policy, Congressional Research Service, before the House Ways and Means Committee, May 12, 2011, http://bit.ly/2riMIk3; Office of Tax Analysis, “The Case for Responsible Business Tax Reform,” Department of Treasury, January 2017, http://bit.ly/2p1Jkff; CBPP, “Actual U.S. Corporate Tax Rates Are in Line with Comparable Countries,” April 25, 2017, http://bit.ly/2q2h36Y.