Social Security faces a significant — though manageable — long-term funding shortfall, which policymakers should address primarily by increasing Social Security’s tax revenues. If policymakers elect to reduce Social Security benefits, those cuts will need to be limited and carefully targeted to avoid causing significant hardship. Moreover, the cuts will almost certainly be phased in slowly, which means they could not produce significant savings for many years. Increasing Social Security’s revenues will be necessary.

Social Security’s tax base has eroded since the last time policymakers addressed solvency.Boosting Social Security’s payroll tax revenue also is justified by recent trends: Social Security’s tax base has eroded since the last time policymakers addressed solvency in 1983, largely due to increased inequality and the rising cost of non-taxed fringe benefits, such as health insurance. And it enjoys broad support: the majority of Americans oppose cuts to Social Security and support strengthening the program by contributing more in taxes.

This paper presents three approaches to increasing payroll taxes that would improve the program’s solvency:

- Increasing or eliminating Social Security’s cap on taxable wages, now $118,500 a year. Raising the cap would help mitigate the erosion of Social Security’s payroll tax base caused by rising wage inequality. Most workers’ taxes would not change, while the degree of increase in high earners’ taxes would depend on whether the cap were raised or eliminated. Raising the tax cap could increase higher earners’ benefits as well, depending on how policymakers treated newly taxed earnings. Changes to the tax cap could close roughly a quarter to nearly nine-tenths of Social Security’s solvency gap, depending on how they were structured.

- Expanding compensation subject to Social Security payroll taxes to include fringe benefits such as employer-sponsored health insurance and flexible spending accounts. Fringe benefits are a growing slice of compensation, and including them in Social Security’s tax base would eliminate the discrepancy between those who receive fringe benefits and those who don’t. Affected workers — who would disproportionately be lower- and middle-income — would pay more in taxes but also receive more in Social Security benefits. Including employer-sponsored health insurance premiums could close over one-third of Social Security’s solvency gap; including other fringe benefits could close one-tenth.

- Increasing Social Security payroll tax rates. Changes to the tax rate would affect all covered workers and would not change benefits. Increasing rates alone could close the entire solvency gap; even a modest change, such as a gradual increase of 0.3 percentage points each for employees and employers (or less than $3 per week for an average earner), could close about one-fifth of the gap.

Social Security’s Long-Term Financing Challenge

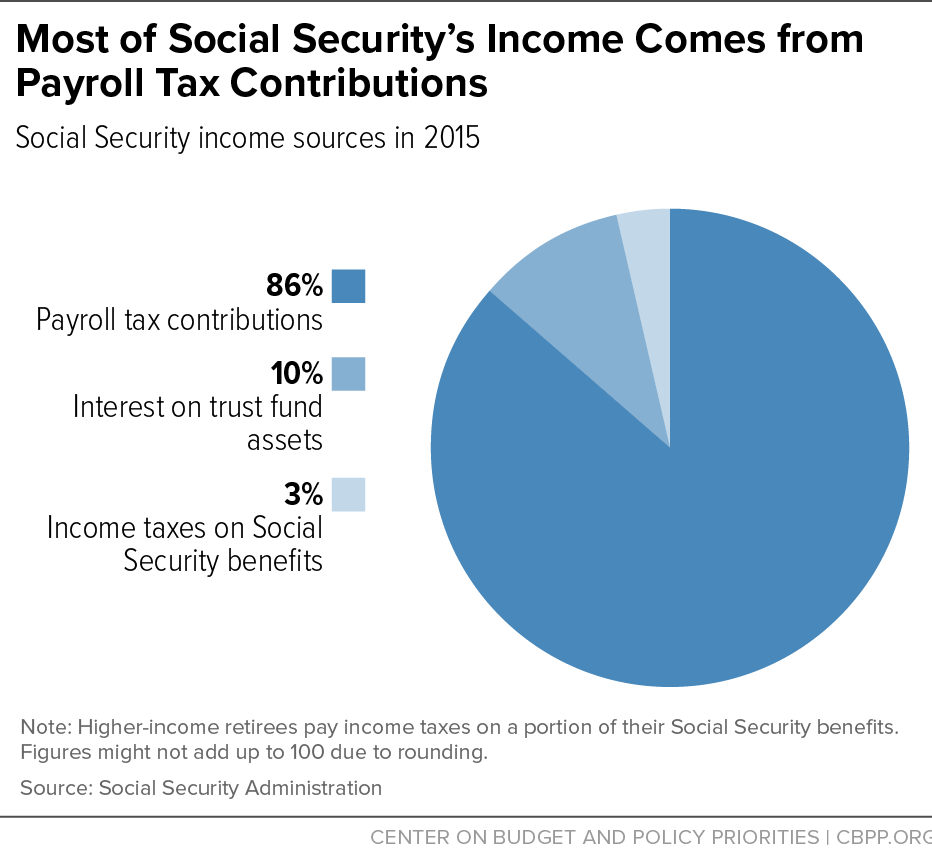

Social Security provides a foundation of income for workers and their families when they retire, become disabled, or when a breadwinner dies. Workers and their employers pay for these benefits primarily through payroll tax contributions, as Figure 1 shows.[2] Higher-income retirees also pay income taxes on part of their Social Security benefits. Social Security’s trustees invest these revenues in trust funds made up of Treasury securities, the interest from which makes up the final source of income.

Since the mid-1980s, Social Security has collected more in revenue each year than it pays out in benefits and has amassed combined trust fund balances of $2.8 trillion. But Social Security’s costs will grow in coming years as baby boomers continue to age into their retirement years. If policymakers take no action, Social Security’s combined trust funds will be exhausted in 2034, at which point Social Security would no longer be able to pay full benefits; after then, it could pay about three-fourths of scheduled benefits, using its tax income. The program’s shortfall amounts to 1 percent of gross domestic product over the next 75 years, or 2.66 percent of the wages on which workers pay Social Security taxes.[3]

Policymakers must act so the program can fully meet its promises.[4] Congress and the President last addressed Social Security’s solvency in 1983, with a balanced package of reforms — including both tax increases and benefit reductions — that ensured the program’s solvency for about 50 years. The benefit cuts in the 1983 deal were phased in over 40 years; they will not be fully implemented until 2022. Most of today’s policymakers have ruled out benefit cuts for current retirees and near-retirees, and they, too, are unlikely to reduce benefits without phasing them in over time. Any benefit cuts will need to be limited and carefully targeted to avoid causing significant hardship. Thus, significant savings from benefit cuts are unlikely to materialize for many years.[5] Increasing Social Security’s revenues will be necessary. Moreover, polling data indicate that most Americans of both political parties oppose cuts to Social Security benefits and support strengthening the program by contributing more in taxes.[6]

Social Security’s Taxable Payroll Lags Behind Compensation

Social Security’s income comes primarily from payroll taxes. Workers and their employers pay a combined 12.4 percent of earnings (6.2 percent each) up to a cap, which in 2016 is $118,500 of a worker’s wages.[7] Social Security benefits, as well, are based on earnings up to that cap. The benefit formula is progressive, which means that it replaces the first dollar of earnings more generously than the last dollar of earnings.[8]

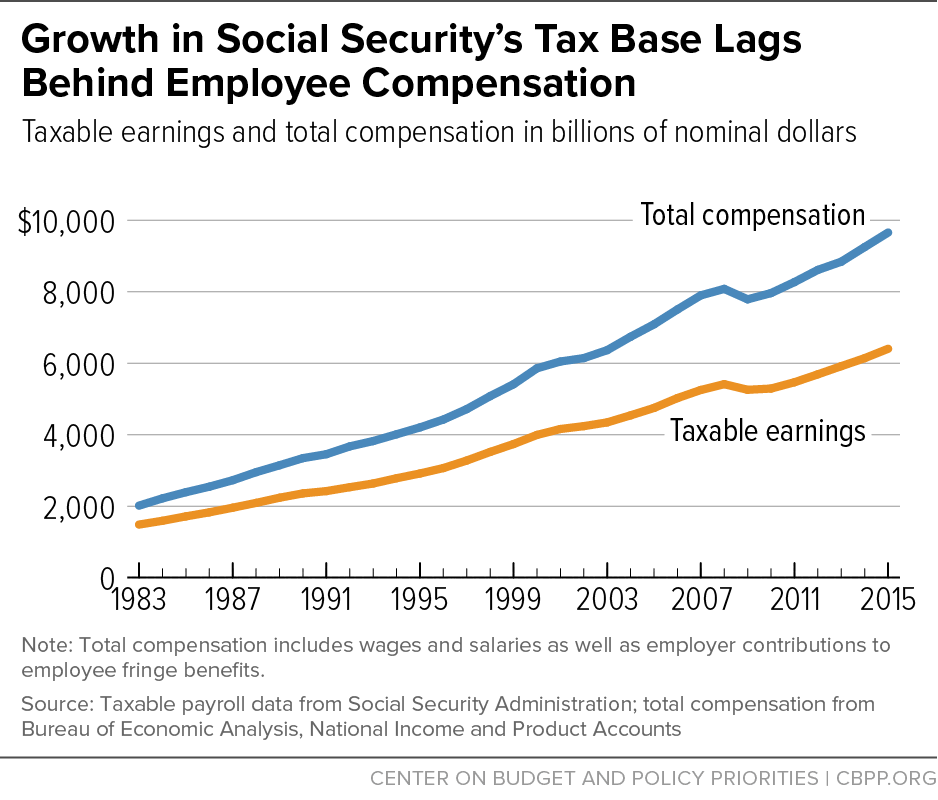

The proportion of employees’ compensation subject to Social Security payroll taxes has shrunk significantly since policymakers last addressed Social Security’s solvency, as Figure 2 shows. In 1983, nearly three-quarters of employees’ compensation was subject to Social Security payroll taxes; in 2015, less than two-thirds was. Two of the major reasons for the lagging tax base are increased wage inequality and the rising share of employee compensation that goes to health care coverage.

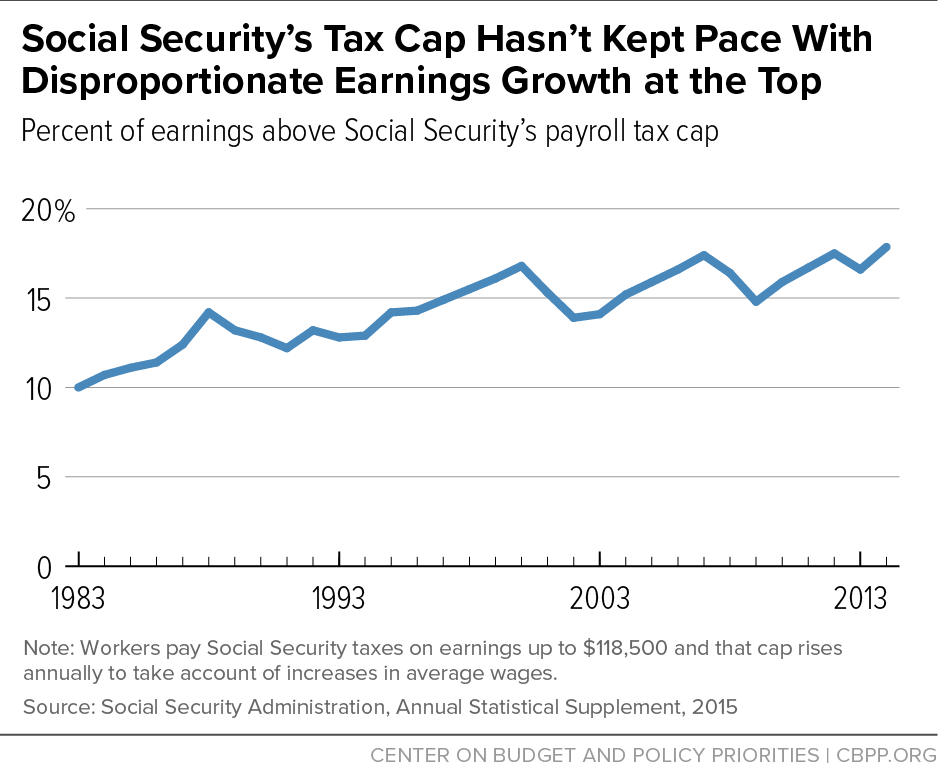

In the past several decades, wage growth among lower- and middle-income Americans has slowed, while wages at the top have continued to grow. In particular, earnings of the top 1 percent — and especially the top 0.1 percent — have grown rapidly, resulting in an increasing share of earnings above Social Security’s tax cap, as shown in Figure 3.[9] When Congress last adjusted the cap in 1977, policymakers set the cap to cover 90 percent of all wages and indexed it to increase annually with average wage growth.[10] But because wages above the cap have grown much faster than average, earnings under the cap now make up only about 82 percent of aggregate wages.[11]

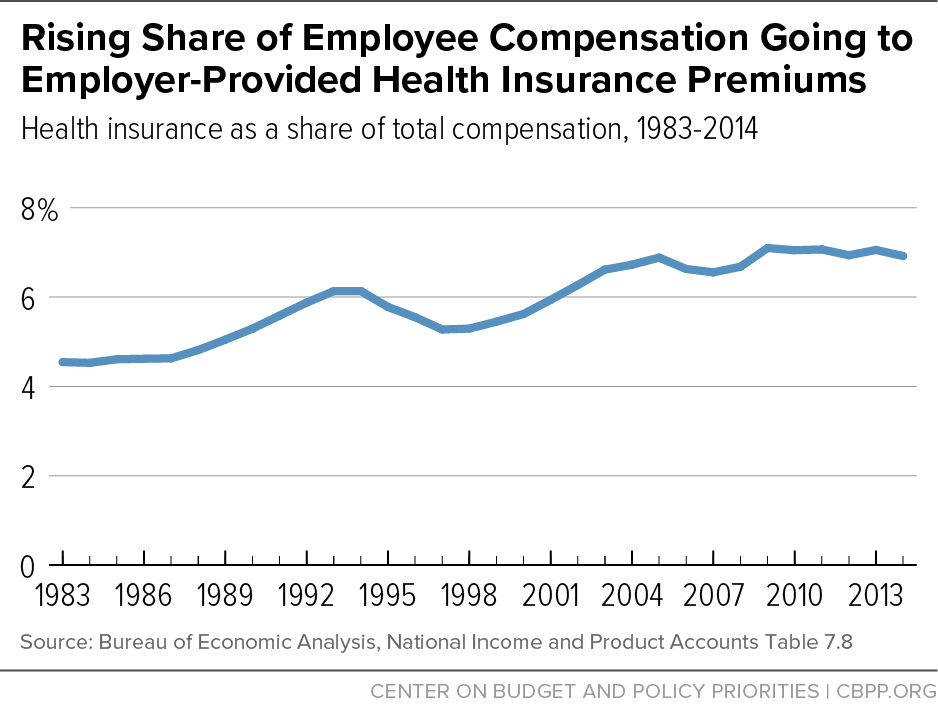

Rising health care costs have also hurt Social Security’s finances. Premiums for employer-sponsored health insurance are exempt from Social Security taxes.[12] As health care costs have risen, wages have fallen as a share of employees’ compensation, while health premiums have risen, nearly doubling as a share of total compensation over the past 30 years.[13] (See Figure 4.) This shift comes at a cost to Social Security. Excluding employer-sponsored health insurance premiums from Social Security payroll taxes cost about $100 billion in forgone payroll taxes in 2015, and will cost about $1.25 trillion over ten years (2016-25).[14]

Driven largely by these two factors, Social Security’s tax base has shrunk significantly as a proportion of employees’ compensation since policymakers last addressed Social Security in 1983. Today’s policymakers should consider how to broaden Social Security’s tax base when they revisit the program’s solvency.[15] This paper focuses on the two most common proposals: raising or eliminating the cap on taxable earnings, and including contributions to fringe benefits as wages subject to the payroll tax. [16] We also consider raising the payroll tax rate.[17]

Raising or Eliminating the Tax Cap

Raising or even eliminating the cap on taxable wages would mitigate the erosion of the Social Security tax base. Rising inequality, driven by rapid wage growth among the highest earners, means a greater proportion of wages are above Social Security’s tax cap.

There is precedent for either approach. Policymakers have raised the Social Security payroll tax cap many times, and they eliminated the Medicare payroll tax cap in 1994. Two prominent deficit-reduction committees have proposed raising the tax cap so that it covers 90 percent of all earnings and then pegging it to that level in the future.[18] Others have proposed eliminating the tax cap altogether.

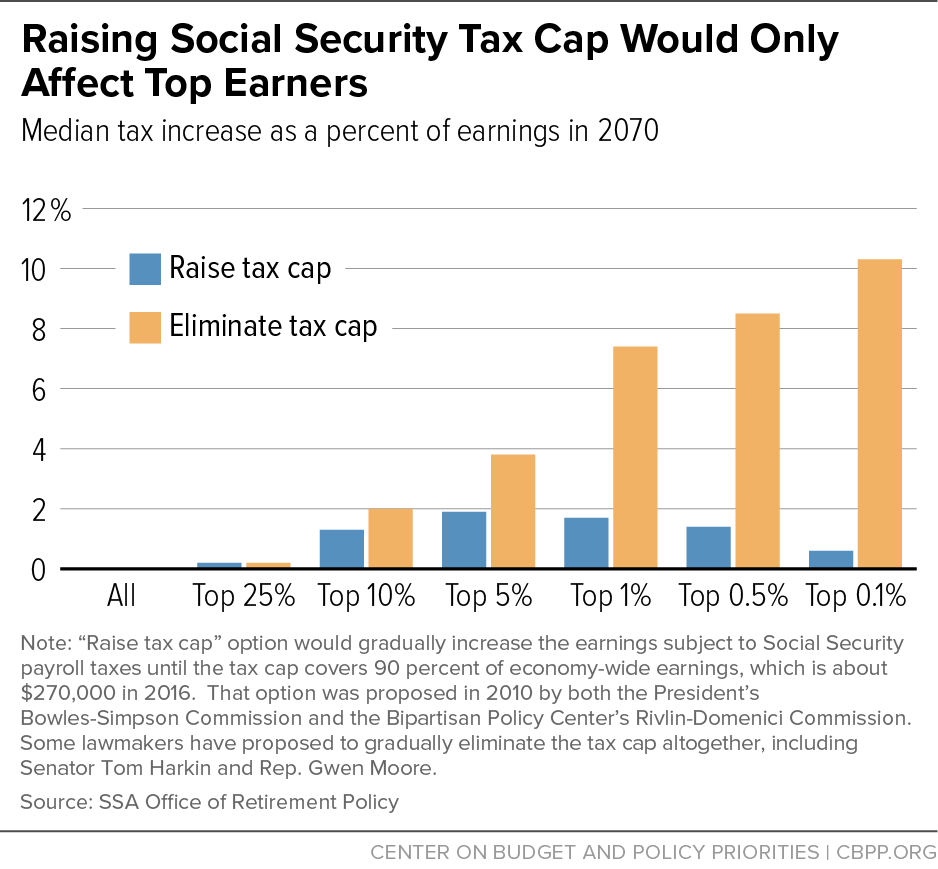

Changes to the tax cap would affect only the highest-earning workers.[19] In any given year, about 6 percent of workers earn more than the current tax cap. Over a lifetime, 20 percent of workers earn more than the tax cap for at least one year. Most of these workers have high lifetime earnings and thus also receive relatively high Social Security benefits. Raising the payroll tax cap to fund Social Security benefits is broadly popular, even among the highest earners — about half of millionaires support raising the cap.[20]

Raising or eliminating the tax cap would make Social Security more progressive. If the cap covered 90 percent of covered earnings in 2016, it would be set at about $270,000, more than double the current-law level.[21] Eliminating the cap would make the Social Security payroll tax proportional so that all workers (and their employers) would contribute 6.2 percent of on every dollar of earnings. In either case, higher earners would pay more.

For most workers, the cap does not affect their taxes, because they earn less than the cap; for high earners, taxes would be quite different depending on whether the cap were raised or eliminated, as Figure 5 shows. If there were no cap, taxes would rise most for the very highest earners, in the top 1 percent and especially the top 0.1 percent. If the cap were increased to cover 90 percent of aggregate earnings, tax increases would be highest (as a percentage of earnings) for the top 5 percent of earners and less for the very highest earners, because their contributions would still be capped.[22]

If policymakers raise or eliminate Social Security’s tax cap, they should also take steps to limit payroll tax avoidance.[23] For example, after policymakers eliminated the Medicare tax cap, some high earners set up special S-corporations in order to take their earnings as corporate profits rather than taxable wages — and thus avoid paying the 2.9 percent Medicare payroll tax.[24] Congress should curtail this “pass-through loophole” and other payroll tax avoidance strategies, as President Obama has proposed.[25]

Raising the tax cap could affect Social Security benefits as well, as policymakers would face a choice about how to account for any newly taxed earnings — specifically, whether and how to include them as part of the average indexed monthly earnings, or AIME, used to calculate benefits. There are three options here:

- Give workers the same benefits they would have received under current law, providing no additional benefits based on newly taxed earnings. For example, Senator Bernie Sanders has proposed applying the full payroll tax to earnings above $250,000. Gradually, as the current-law tax cap rises with wages, more earnings will be subject to the payroll tax, until every dollar of earnings is taxed in around 2034. His proposal would provide no additional benefits based on earnings above the current-law tax cap (now $118,500).[26] This would weaken the link between earnings and benefits — an important principle in a system based on wage replacement — and could also weaken Social Security’s popular support. Doing so would close 89 percent of Social Security’s long-term shortfall.

- Extend the top bracket to encompass newly taxed earnings, replacing them at the 15 percent rate. For example, the Rivlin-Domenici deficit reduction commission proposed gradually raising the tax cap to cover 90 percent of aggregate earnings, and replacing earnings above the current-law cap at a 15 percent rate.[27] Doing so would close about a quarter of Social Security’s long-term shortfall. Extending the top bracket to newly taxed earnings would significantly increase many higher earners’ benefits, especially if the tax cap were eliminated. In that case, benefits for the richest workers could reach extraordinarily high levels: for example, a worker with average earnings of $500,000 would get a Social Security benefit of over $90,000 each year. This politically unpalatable possibility has generally led policymakers to seek a middle ground.

- Provide scaled-back credit for wages above the cap. This approach would mean high earners would receive a less generous replacement rate for their average lifetime earnings above the current tax cap. [28] For example, the Bowles-Simpson deficit reduction commission proposed gradually raising the tax cap to cover 90 percent of aggregate earnings, and replacing earnings above the current-law cap at a 5 percent rate.[29] Doing so would close about a quarter of Social Security’s long-term shortfall. Various congressional Social Security solvency proposals have proposed eliminating the cap and replacing earnings above the current-law tax cap at a 3 percent or 5 percent rate.[30] Doing so would close about three-quarters of Social Security’s long-term shortfall.

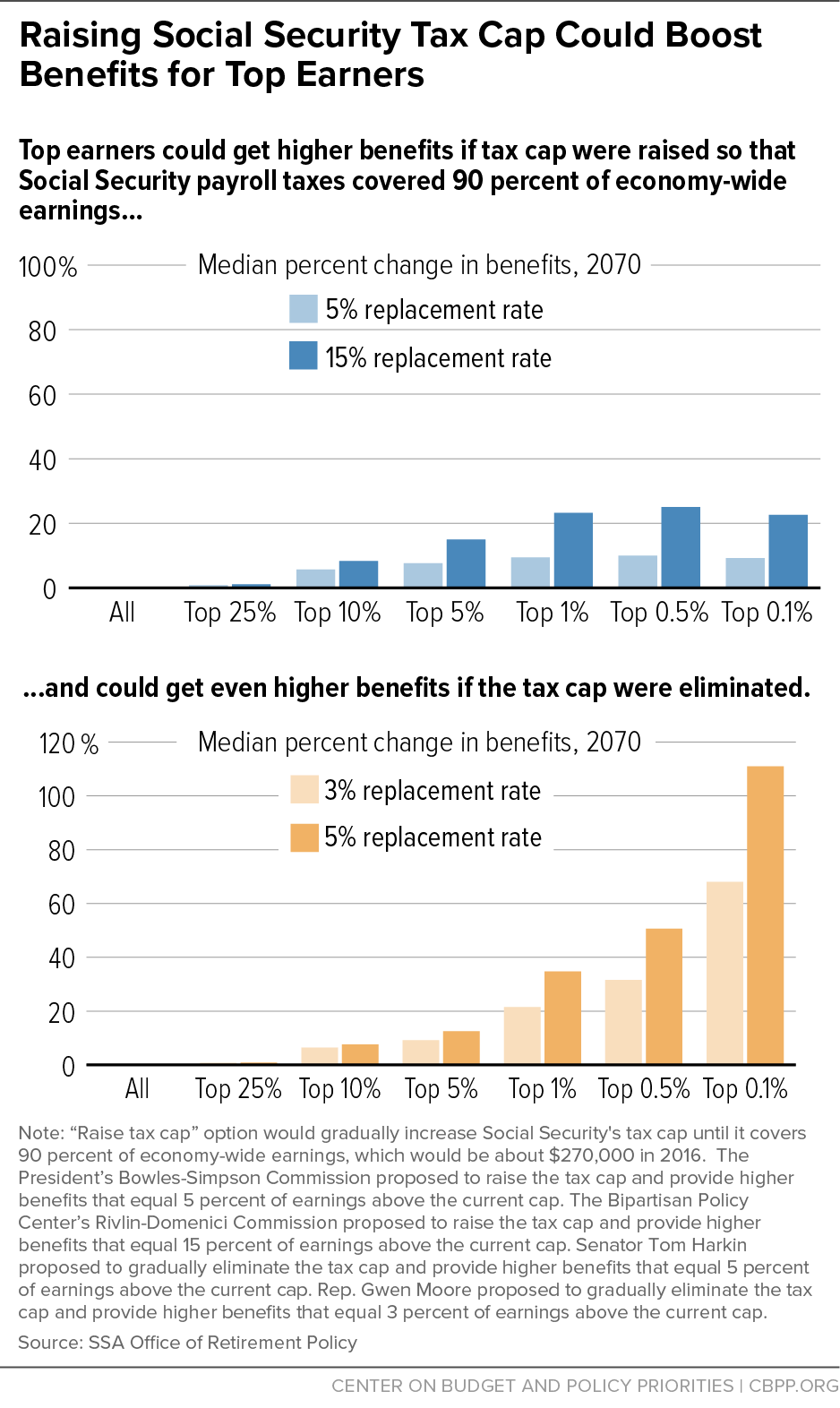

Most beneficiaries would not be affected by increases in the tax cap, because they earn less than the cap. For those who are affected, both the cap level and the replacement rate matter, as Figure 6 shows. For example, if the cap were increased with a 5 percent replacement rate, benefits would rise no more than 10 percent, even for the highest earners; with a 15 percent replacement rate, benefits would rise by about 25 percent for the top 1 percent. Eliminating the cap could mean even larger benefit increases, particularly for the very highest earners. For example, eliminating the cap with a 5 percent replacement rate would more than double benefits for the top 0.1 percent of earners.

Expanding Compensation Subject to the Payroll Tax

As noted above, over time, an increasing proportion of workers’ compensation has been paid not in wages but in fringe benefits that are exempt from Social Security taxes, such as employer-sponsored health insurance premiums and flexible spending accounts. Covering these benefits as taxable compensation for Social Security would broaden the tax base, improve workers’ Social Security benefits, and bolster solvency.

There is precedent for expanding taxable wages for Social Security. In 1983, Social Security began to cover workers’ contributions toward 401(k) plans and other defined-contribution pension plans as earnings for Social Security taxes and benefits.

Taxing Health Insurance Premiums

About half of Americans receive health care coverage through their employers.[31] Both employee and employer premiums are generally excluded from payroll and income taxes. Initially, the tax exclusion for employer-sponsored health insurance applied only to employers’ share of premiums. Since 1978, employees have also been able to shelter their share of premiums from taxes if they are offered as part of a cafeteria plan — as the vast majority are.

Social Security benefits are intended to replace lost wages when workers retire, die, or become disabled, but employer-sponsored health insurance premiums differ from ordinary wages. For example, contributions to other fringe benefits, like 401(k)s and FSAs, would otherwise be paid as cash wages. But employees can decline employer-sponsored health insurance without necessarily getting a higher paycheck — and many do, especially when one spouse pays for coverage for the whole family.

Excluding employer-sponsored health insurance premiums from taxes disproportionately benefits high earners. Higher-income families are more likely to get health coverage at work, and their premiums are significantly higher on average. The value of the tax subsidy has risen over time, especially for high-income families.[32] At the same time, an increasing number of Americans — especially lower-income Americans — buy their health insurance outside the workplace, including through Affordable Care Act health insurance marketplaces.[33] They must pay for their insurance with income that has already been subject to Social Security payroll taxes.

If Social Security’s tax base were expanded to include employer-sponsored health insurance premiums, both employee and employer premiums would count as wages for Social Security payroll tax — and later, benefit — calculations. For example, the Rivlin-Domenici plan would cap and phase out the tax exclusion for employer-sponsored health insurance, closing 33 percent of Social Security’s long-term shortfall.[34] (This paper examines only Social Security payroll taxes, though some proposals — including the Rivlin-Domenici plan — would often end the exclusion of employer-sponsored health insurance premiums from income taxes and Medicare payroll taxes as well.) Alternatively, policymakers could expand Social Security’s tax base to include only employees’ contributions to health insurance premiums, as was the case before 1978.

Counting employer-sponsored health insurance premiums as taxable wages for Social Security purposes would increase both Social Security payroll taxes and benefits for most workers.[35] For the median earner, the change would be equivalent to about a one percentage point increase in the combined payroll tax rate and a 5 percent increase in benefits. The tax and benefit increases would be smallest for the highest earners and largest for lower and middle earners.[36] The option would increase lifetime Social Security payroll taxes more than lifetime Social Security benefits, at all earning levels. Because this option — unlike tax cap changes — would increase benefits for lower earners, it would lower the poverty rate among elderly Social Security beneficiaries, by about 15 percent.

Taxing Cafeteria Plans

Like employer-provided health insurance premiums, workers’ contributions to “cafeteria plans” are generally exempt from payroll taxes. Using these plans, workers direct a portion of their pre-tax compensation to pay for fringe benefits such as flexible spending accounts for health and child care expenses, commuting costs, and life insurance.[37]

Cafeteria plans were established in 1978, and were rarely offered when Congress last addressed Social Security solvency in 1983. They have since become common; for example, 40 percent of workers have access to a health care flexible spending account.[38] Their increasing popularity contributes to the growing gap between workers’ taxable wages and their total compensation. Because they are not subject to payroll taxes, the wages workers use to fund such accounts do not count toward their Social Security benefits.

Counting employees’ contributions to cafeteria plans as wages for Social Security would be consistent with the treatment of their contributions to 401(k) and other defined contribution pension plans. The Rivlin-Domenici provision to subject these contributions to Social Security’s payroll tax would close 10 percent of Social Security’s long-term shortfall.[39]

Treating contributions to cafeteria plans as covered earnings for Social Security would increase participating workers’ Social Security taxes, and subsequently their benefits — though to a lesser extent than taxing employer-sponsored health insurance premiums.

Raising Payroll Tax Rates

Finally, policymakers could increase Social Security payroll tax rates. The last major Social Security reform, in 1983, sped up a previously scheduled rate increase, increasing the combined rate over seven years from 10.8 percent to 12.4 percent, where it stands today.

The solvency effect of raising the rate depends on both when and how much policymakers change the rate. If policymakers restored Social Security’s long-term balance solely by raising payroll tax rates now — without making any other changes to taxes or benefits — workers and employers would each pay 1.29 percentage points more of wages toward Social Security, bringing the total combined payroll tax rate to 16.0 percent.[40] If they waited until 2034, they’d need to raise the rate by 2.29 percentage points. Alternatively, they could close a portion of the solvency gap with a smaller, more gradual increase. For example, raising rates 0.1 percentage points per year until the combined payroll tax rate reaches 13.0 percent would close one-fifth of the solvency gap;[41] continuing to raise the rate at that pace until it reached 14.8 percent would close two-thirds of the gap.[42]

Changes to the rate would affect all covered workers and would not change benefits. A payroll tax rate of 13.0 percent would cost an average earner less than $3 in additional contributions each week (on top of his or her employer’s additional contribution of the same amount). A rate of 14.8 percent would cost $11.50 a week in addition to current payroll taxes. Social Security’s payroll tax is regressive, because of its flat rate and its cap, so low- and moderate-income taxpayers pay more of their incomes in payroll tax than do high-income people, on average.[43] However, if one looks at Social Security’s overall impact — its contributions and its benefits — the program is progressive, paying benefits that equal a higher proportion of a lower earners’ previous earnings. Therefore, raising the payroll tax rate to forestall an across-the-board cut in benefits would be progressive.

Conclusion

Social Security will need a larger share of our nation’s resources in the coming decades as the population ages, and polls show a widespread willingness to support it through higher tax contributions. Policymakers should seriously consider increasing payroll taxes to strengthen this vital program. Since policymakers last addressed Social Security solvency in 1983, its payroll tax base has eroded. Benefit cuts won’t be enough to close Social Security’s financing gap, especially in the short run. Increasing revenues will be necessary to restore solvency.

Options to increase Social Security’s revenues, including raising the tax cap, expanding compensation subject to taxes, and raising the payroll tax rate could be combined to improve Social Security’s solvency — and perhaps to strengthen benefits for particularly vulnerable groups. For example, raising both the payroll tax cap and rate would provide an extra solvency boost. Raising the tax cap and counting health insurance premiums as wages would spread the additional contributions more evenly throughout the earnings spectrum. Any of these options would help ensure that Social Security can pay benefits for generations to come.

End Notes

[1] Cecile Murray contributed to this report.

[2] Social Security Administration, “The 2016 Annual Report of the Board of Trustees of the Federal Old-Age and Survivor’s and Federal Disability Insurance Trust Funds,” June 22, 2016, https://www.ssa.gov/oact/tr/2016/tr2016.pdf.

[3] Kathleen Romig, “What the 2016 Trustees’ Report Shows About Social Security,” Center on Budget and Policy Priorities, July 12, 2016, https://www.cbpp.org/research/social-security/what-the-2016-trustees-report-shows-about-social-security. The Congressional Budget Office is somewhat more pessimistic about Social Security’s finances; for more details see Kathy Ruffing, “CBO’s Social Security Projections No Cause for Alarm,” Center on Budget and Policy Priorities, February 16, 2016, https://www.cbpp.org/blog/cbos-social-security-projections-no-cause-for-alarm.

[4] Kathy Ruffing and Paul N. Van de Water, Center on Budget and Policy Priorities, “Social Security Benefits Are Modest: Policymakers Have Limited Room to Reduce Benefits Without Causing Hardship,” August 1, 2016, https://www.cbpp.org/research/social-security/social-security-benefits-are-modest.

[5] It would take at least 20 to 30 years from enactment to net appreciable savings from benefit cuts, so “increasing revenue is almost the only viable short- to medium-tem policy option.” Thomas L. Hungerford, “Broadening the Social Security Tax Base: Issues and Options,” Tax Notes, June 6, 2016, https://assets.documentcloud.org/documents/2853616/Hungerford.pdf.

[6] More than seven in ten registered voters say Social Security benefits should not be reduced in any way, including 68 percent of Republicans and 72 percent of Democrats. (Pew Research Center, “Campaign Exposes Fissures Over Issues, Values and How Life Has Changed in the U.S.,” March 31, 2016, http://www.people-press.org/2016/03/31/3-views-on-economy-government-services-trade/.) More than eight in ten — including 74 percent of Republicans and 88 percent of Democrats — agree that “it is critical to preserve Social Security even if it means increasing Social Security taxes paid by working Americans.” (Jasmine V. Tucker, Virginia P. Reno, and Thomas N. Bethell, “Strengthening Social Security: What Do Americans Want?” National Academy of Social Insurance, January 2013, https://www.nasi.org/sites/default/files/research/What_Do_Americans_Want.pdf.)

[7] Most economists agree that employees bear the true cost of employer payroll taxes in the form of lower wages.

[8] Social Security replaces 90 percent of the first $856 of average indexed monthly earnings (AIME), 32 percent of AIME between $856 and $5,157, and 15 percent of AIME above $5,157, for all earnings up to the tax cap.

[9] Kevin Whitman and Dave Shoffner, “The Evolution of Social Security’s Taxable Maximum,” Social Security Administration (SSA), Office of Retirement and Disability Policy, September 2011, https://www.ssa.gov/policy/docs/policybriefs/pb2011-02.html.

[10] The 1977 legislation fully phased in the tax cap changes by 1981, after which the cap was indexed to wage growth. In years in which there is no cost-of-living-adjustment for Social Security, the taxable maximum does not increase. See Kathleen Romig, “No COLA for 2016 Will Affect Medicare Premiums and Social Security Finances,” Center on Budget and Policy Priorities, October 20, 2015, https://www.cbpp.org/blog/no-cola-for-2016-will-affect-medicare-premiums-and-social-security-finances.

[11] Social Security’s actuaries estimate that 81.77 percent of wages are taxed in 2016 and expects the proportion to rise to 82.50 percent in 2025. CBO projects it will fall below 79 percent. See Kathy Ruffing, “CBO’s Social Security Projections No Cause for Alarm,” Center on Budget and Policy Priorities, February 16, 2016, https://www.cbpp.org/blog/cbos-social-security-projections-no-cause-for-alarm.

[12] For more information, see Jonathan Gruber, “The Tax Exclusion for Employer-Sponsored Health Insurance,” National Bureau of Economic Research Working Paper 15766, February 2010, http://www.nber.org/papers/w15766.pdf?new_window=1

[13] Gary Burtless and Sveta Milusheva, “Effects of Employer-Sponsored Health Insurance Costs on Social Security Taxable Wages,” Social Security Bulletin, Vol. 73 No. 1, 2013, http://www.ssa.gov/policy/docs/ssb/v73n1/v73n1p83.html.

[14] Excluding employer sponsored health insurance premiums from both Social Security and Medicare payroll taxes is estimated to cost $127.5 billion in 2015, and $1.6 trillion over 2016-2025. (See Supplementary Table 14-1 at https://www.whitehouse.gov/omb/budget/Analytical_Perspectives.) The Social Security Trustees estimate that the Medicare Hospital Insurance (HI) taxable payroll is about 25 percent larger than the Old-Age, Survivors, and Disability Insurance (OASDI) taxable payroll (TR, p. 200), and the rates are different for each tax: 12.4 percent OASDI and 2.9 percent for HI, with an additional 0.9 percent tax on the highest earners. After factoring in the rate and base for each payroll tax, we estimate that Social Security payroll taxes account for about three-quarters of the total payroll tax expenditure.

[15] Thomas L. Hungerford, “Broadening the Social Security Tax Base: Issues and Options,” Tax Notes, June 6, 2016.

[16] This paper analyzes each of these options using solvency and distributional estimates from SSA’s Office of the Chief Actuary and Office of Retirement Policy. For more on the methodology used to produce these estimates, please see https://www.ssa.gov/policy/about/mint.html.

[17] Policymakers could also raise revenues by taxing a greater proportion of Social Security benefits, by taxing new sources of income like investment returns or by increasing the number of people who pay into the program — for example, by covering state and local workers who do not participate in Social Security or through comprehensive immigration reform. Those options are beyond the scope of this paper.

[18] The bipartisan plans that Alan Simpson and Erskine Bowles (co-chairs of the National Commission on Fiscal Responsibility and Reform) and Alice Rivlin and Pete Domenici (co-chairs of the Bipartisan Policy Center Debt Reduction Task Force) produced in late 2010 each recommended increasing Social Security’s tax cap.

[19] “Population Profiles: Taxable Maximum Earners,” SSA, ORP, March 2015, https://www.ssa.gov/retirementpolicy/fact-sheets/tax-max-earners.html.

[20] Benjamin I. Page, Larry M. Bartels, and Jason Seawright,

“Democracy and the Policy Preferences of Wealthy Americans,” Perspectives on Politics, March 2013, http://faculty.wcas.northwestern.edu/~jnd260/cab/CAB2012%20-%20Page1.pdf.

[21] SSA, OCACT, August 2016, “Social Security Contribution and Benefit Bases for 2016-2025 for Current Law and Levels Needed to Achieve 85%, 86%, 87%, and 90% Ratios of Effective Taxable Payroll to Covered Earnings Under the Intermediate Assumptions of the 2016 Trustees Report.”

[22] Figure 5 shows the difference between the lifetime present value of payroll taxes paid under each option and under current law, divided by the lifetime present value of taxable covered earnings under current law.

[23] The solvency estimates in this paper, from SSA’s Office of the Chief Actuary, account for shifting compensation away from taxable earnings. The distributions estimates, from SSA’s Office of Retirement Policy, do not.

[23]“Payroll Tax Loophole Used by John Edwards and Newt Gingrich Remains Unaddressed by Congress,” Citizens for Tax Justice, September 6, 2013, http://www.ctj.org/taxjusticedigest/archive/2013/09/payroll_tax_loophole_used_by_j.php#.V9rLgPkrJD8.

[25] Chuck Marr, Chye-Ching Huang, and Joel Friedman, “Tax Expenditure Reform: An Essential Ingredient of Needed Deficit Reduction,” Center on Budget and Policy Priorities, February 28, 2013, https://www.cbpp.org/research/tax-expenditure-reform-an-essential-ingredient-of-needed-deficit-reduction, and Joel Friedman, Robert Greenstein, and Sharon Parrott, “Key Elements of the President’s Fiscal Year 2015 Budget,” Center on Budget and Policy Priorities, March 5, 2014, https://www.cbpp.org/research/key-elements-of-the-presidents-fiscal-year-2015-budget.

[26] Social Security Expansion Act (S. 731), introduced in 2015, E2.5: https://www.ssa.gov/oact/solvency/BSanders_20150323.pdf

[27] This option would gradually increase the tax cap 2 percent per year beyond current-law indexing, until it covers 90 percent of covered earnings. Any AIME above the current cap would be replaced at a 15 percent rate. SSA, Office of the Chief Actuary, Provisions Affecting Payroll Taxes, https://www.ssa.gov/oact/solvency/provisions/payrolltax.html, E3.5 (beginning in 2017).

[28] Policymakers could also treat any earnings above the tax cap separately, applying a specific replacement rate only to any annual earnings above that year’s tax cap (“AIME+”), instead of the current-law AIME, which measures average earnings over a lifetime. This would limit the benefit increase — and costs — of raising the tax cap.

[29] This option would increase the tax cap 2 percent per year beyond current-law indexing, until it covers 90 percent of covered earnings. Any AIME above the current cap would be replaced at a 5 percent rate. SSA, Office of the Chief Actuary, Provisions Affecting Payroll Taxes, https://www.ssa.gov/oact/solvency/provisions/payrolltax.html, E3.7 (beginning in 2018).

[30] Both the Social Security Enhancement and Protection Act of 2013 (H.R. 1374), introduced by Rep. Gwen Moore, and the Rebuild America Act (S. 2252), introduced by Senator Tom Harkin in 2012, would gradually eliminate the tax cap, by taxing all earnings above the current cap at 1.24 percent in the first year, 2.48 percent in the second, and so on, up to the full 12.4 percent in the tenth year. Any AIME above the current cap would be replaced at a 3 percent rate in the Moore plan and at 5 percent in the Harkin plan. SSA, Office of the Chief Actuary, Provisions Affecting Payroll Taxes, https://www.ssa.gov/oact/solvency/provisions/payrolltax.html, E2.12 and E2.10 (beginning in 2019 and 2018, respectively).

[31] Kaiser Family Foundation, “Health Insurance Coverage of the Total Population, 2014,” http://kff.org/other/state-indicator/total-population/.

[32] Robert Kaestner and Darren Lubotsky, “Health Insurance and Income Inequality,” Journal of Economic Perspectives, Vol. 30, No. 2, Spring 2016, http://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.30.2.53.

[33] The Kaiser Family Foundation found that the number of Americans who purchase insurance on the individual market — including in the marketplaces — grew 46 percent from 2013 to 2014, from 10.6 to 15.6 million. See Larry Levitt, Cynthia Cox, and Gary Claxton, “Data Note: How Has the Individual Insurance Market Grown Under the Affordable Care Act?”, Kaiser Family Foundation, May 12, 2015, http://kff.org/private-insurance/issue-brief/data-note-how-has-the-individual-insurance-market-grown-under-the-affordable-care-act/.

[34] The provision would gradually expand Social Security-covered earnings to include both employer and employee premiums for employer-sponsored health insurance. Starting in 2020, premiums above the 75th percentile would be subject to the payroll tax, with this gradually expanding until all premiums are taxed in 2030. (This proposal would also cap and phase out the exclusion of employer-sponsored health insurance premiums from income taxes.) SSA, OCACT, Provisions Affecting Coverage of Employment or Earnings, https://www.ssa.gov/oact/solvency/provisions/coverage.html, F3, based on the provision from the deficit reduction plan that former Office of Management and Budget and CBO director Alice Rivlin and former Senator Pete Domenici developed for the Bipartisan Policy Center.

[35] For a detailed breakdown of how tax and benefit changes would be distributed in the population, see Kathleen Romig, Dave Shoffner, and Kevin Whitman, “Distributional Effects of Taxing Employer-Sponsored Health Insurance Premiums for Social Security,” SSA, August 2016, https://www.ssa.gov/policy/docs/policybriefs/pb2016-01.html. The change would affect benefits — which are based on covered earnings — gradually. As workers paid Social Security taxes on their health insurance premiums for more years, their resultant benefits would be higher.

[36] Many lower earners get Medicaid; middle earners are the group receiving the greatest share of its compensation as fringe benefits; some higher earners are shielded by the tax cap.

[37] See “FAQ for Government Entities Regarding Cafeteria Plans,” Internal Revenue Service, https://www.irs.gov/Government-Entities/Federal,-State-&-Local-Governments/FAQs-for-government-entities-regarding-Cafeteria-Plans.

[38] See Table 41 in “National Compensation Survey: Employee Benefits in the United States, March 2015,” Bureau of Labor Statistics, September 2015, http://www.bls.gov/ncs/ebs/benefits/2015/ebbl0057.pdf.

[39] This provision would expand Social Security-covered earnings to include contributions to voluntary salary reduction plans (such as Cafeteria 125 plans and Flexible Spending Accounts), starting in starting in 2017. SSA, OCACT, Provisions Affecting Coverage of Employment or Earnings, https://www.ssa.gov/oact/solvency/provisions/coverage.html, F4, based on provision from Rivlin-Domenici commission.

[40] SSA, 2016 Trustees Report, Overview, https://www.ssa.gov/oact/TR/2016/II_A_highlights.html#. In 2034, the 75-year window would include more deficit years than today’s 75-year projection period does.

[41] This provision would increase the payroll tax rate by 0.1 percentage point each year, starting in 2019, until it reaches 13.0 percent in 2024. SSA, OCACT, Provisions Affecting Payroll Taxes, https://www.ssa.gov/oact/solvency/provisions /payrolltax.html, E1.8 (based on based on Social Security Enhancement and Protection Act of 2013, H.R. 1374, introduced by Representative Gwen Moore).

[42] This provision would increase the payroll tax rate by 0.1 percentage point each year, starting in 2020, until it reaches 14.8 percent in 2043, where it would stay for 40 years. Then, from 2082 to 2086, the rate would increase 0.1 percentage point each year until it reached 15.3 percent. SSA, OCACT, Provisions Affecting Payroll Taxes, https://www.ssa.gov/oact/solvency/provisions/payrolltax.html, E1.9 (based on H.R. 1391, The Social Security 2100 Act, introduced in 2015 by Representative John Larson).

[43] “Policy Basics: Federal Payroll Taxes,” Center on Budget and Policy Priorities, March 23, 2016, https://www.cbpp.org/research/federal-tax/policy-basics-federal-payroll-taxes.

More from the Authors