Republican Tax Plans Would Largely Exclude Small Businesses — and Could Even Hurt Them

President Trump and congressional Republicans claim that small businesses would benefit from the tax framework they announced in September.[1] Yet, no matter how much the President and congressional Republicans invoke small businesses and typical workers in selling their tax plans, their actual tax and budget policies would do little to help such businesses and workers — and could even hurt them.

“Pass-Through” Tax Break Would Help Few Small Businesses

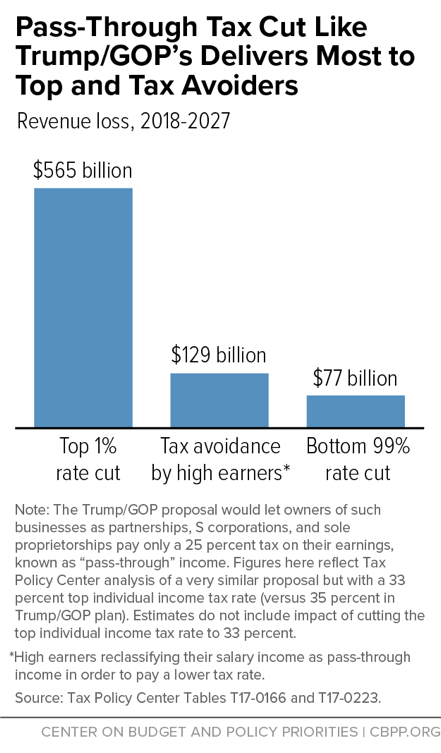

Proponents of the GOP tax plans claim they will help small businesses by enacting a special tax rate for “pass-through” business income — income from businesses such as partnerships, S corporations, and sole proprietorships that is claimed on individual tax returns and is currently taxed at the same rates as wages and salaries. (Unlike business income that faces the 35 percent top corporate tax rate, pass-through income does not face the tax on dividends.) The Trump/GOP framework would sharply cut the top rate on this income, from 39.6 percent to 25 percent — well below its proposed top individual income tax rates of 35 percent. Reducing the top tax rate on pass-through income to 25 percent would cost $770 billion over ten years, with increased avoidance accounting for about $130 billion of that total. Pass-through tax cuts wouldn’t help most small businesses because:

- Most small businesses are in fact “small” and despite what prominent congressional Republicans have said, very few small business owners pay the top rate of 39.6 percent. Some 86 percent of them already pay tax rates at or below Trump and the GOP’s proposed 25 percent pass-through rate. They would receive no benefit from this low pass-through rate. Indeed, only about 2 percent of households with incomes below $100,000 would receive a tax cut from this proposal.

- In reality, as the chart shows, a pass-through tax cut would provide a massive windfall to the very wealthy. (It’s been referred to as the “Trump loophole” because President Trump exemplifies the type of business owner whom it would most benefit, as he owns about 500 pass-through businesses, according to his attorneys.) About 80 percent of the tax cut on existing pass-through income would flow to the top 1 percent, including real estate investors, hedge fund managers, lobbyists, and the like. Additionally, high earners would likely engage in tax avoidance by reclassifying their salaries as pass-through income to take advantage of the lower rate.

Few Small Farms and Businesses Would Benefit From Estate Tax Repeal

Repealing the estate tax would be a boon to the heirs of the wealthiest estates in the country, not small business owners and farms. The estate tax affects very few small farms and businesses and is not a heavy burden for them.

- Only 50 small farm or business estates nationwide will face the tax in 2017, and those that do will pay less than 6 percent of their value in tax, on average. That’s mainly because the estate tax exempts $11 million in assets per couple — which is why repealing it would be a windfall for the heirs of the nation’s wealthiest 0.2 percent of estates.

- Most farm and small business estates that pay the tax will have sufficient liquid assets to pay the tax without having to touch the farm or business. As the New York Times reported in 2001, when the estate tax applied to far more estates than it does today: “Even one of the leading advocates for repeal of estate taxes, the American Farm Bureau Federation, said it could not cite a single example of a farm lost because of estate taxes.”

“Territorial Tax” Doesn’t Help Small and Domestic Business — and Could Hurt

President Trump and congressional Republicans propose moving to a territorial tax system in which U.S.-based multinational corporations wouldn’t pay U.S. corporate taxes on their foreign profits, while domestic businesses would face a 20 or 25 percent rate, depending on whether they are a C-corporation or a pass-through. That could make U.S. domestic and small businesses less competitive relative to large U.S. multinationals.

Under a territorial system, large U.S. multinationals could pay tax lawyers millions of dollars in fees to find ways to report U.S. profits as being earned offshore in order to pay zero U.S. tax on “foreign” profits. That would give them a huge tax advantage over purely domestic businesses — including most small businesses — that don’t have foreign operations and can’t orchestrate complex tax avoidance maneuvers. The tax avoidance savings would flow to profitable U.S. multinationals, especially those in industries that can easily move profits overseas, such as drug and software companies.

Cuts to Critical Government Investments Could Hurt Small Businesses

The Trump and congressional Republican tax plan proposes large, costly tax cuts that would overwhelmingly flow to the wealthy and large profitable corporations — but not credible ways to fully offset the cost by scaling back tax breaks or raising revenue from other sources. Instead, President Trump and congressional Republican budget proposals pair tax cuts with deep cuts to domestic investments that could weaken the economy and harm small businesses. For example:

- President Trump’s, the House, and the Senate Budget Committee’s budgets all propose to cut non-defense discretionary (NDD) programs below the already inadequate sequestration levels. NDD programs include key investments such as education, job training, scientific and medical research, infrastructure, and other programs that promote economic growth and support domestic businesses.

- The President’s budget specifically proposes cuts in education and job training and hence would make it more challenging to develop the skilled workforce that small businesses need. In 2018, the proposal would cut student aid, end a provision adjusting Pell Grants for inflation (making college less affordable for many low-income students), cut the Education Department’s elementary and secondary programs by $4 billion, and slash state Workforce Innovation and Opportunity Act job training grants for adults, dislocated workers, and youth by 40 percent.

The President’s budget would also weaken federal support for infrastructure by reducing Highway Trust Fund spending, cutting discretionary infrastructure investments, and shifting costs to states and localities. It proposes limiting Highway Trust Fund spending to the dedicated revenues it receives, starting in 2021. That would lead to cuts in Highway Trust Fund spending that would grow over time, reaching $20 billion a year by the end of ten years and extending indefinitely.

A House Budget Proposal Would Increase Tax Filing Burdens

The GOP tax framework promises “simplification,” but the House budget’s accompanying documents call for a measure that would increase tax filing burdens on millions of working Americans — problems that would be magnified for 7 million small-business owners and other self-employed individuals.[2] The proposal would delay tax refunds for low- and moderate-income workers who claim the Earned Income Tax Credit (EITC) each year until the IRS verifies their incomes. Supplying the needed documentation could be especially challenging for the nearly 7 million small-business owners and other self-employed individuals who claim the EITC, including large and growing numbers of filers in the “gig” economy. They likely would have to include many more documents with their tax returns — documents that higher-income people with self-employment or business income (a group with a quite high rate of tax non-compliance) do not have to supply.

End Notes

[1] See, for example, The White House, “Widespread Praise for President Trump's Unified Framework for Tax Reform,” September 27, 2017, http://bit.ly/2fS8FDu.

[2] Robert Greenstein and John Wancheck, "House Budget Committee Proposal to Verify Incomes of All EITC Filers Would Delay Refunds, Raise Administrative Costs, and Divert IRS Resources," CBPP, September 11, 2017, http://bit.ly/2wn2RHo.