Proposed Cap Would Require Deep Cuts In Entitlement Programs

The Republican Study Committee, a group of conservative members of the House of Representatives, has proposed to establish an “entitlement cap” that limits total expenditures for entitlement programs other than Social Security and requires projected expenditures for such programs to be cut $1.8 trillion over the next ten years. This proposal is part of its “Contract with America Renewed,” issued March 8, 2006.[1] The proposed entitlement cap could become part of budget-process legislation being discussed by the House Budget Committee majority and the House majority leadership, or it could be offered as an amendment to that legislation.

Under the RSC entitlement cap proposal, a cap would be set each year on allowable expenditures for entitlement programs other than Social Security. The cap would be set at a level well below what entitlement programs would cost under current law, necessitating deep cuts to reduce costs to the level of the caps. In any year in which Congress and the President did not cut entitlements enough to fit within the cap, automatic cuts in entitlement programs would be triggered.

The Congressional Budget Office issues entitlement-cost projections and related data that enable analysts to compute where the entitlement caps would be set under the RSC proposal. The CBO projections and data indicate that over the next ten years, the entitlement caps would be a total of $1.8 trillion below what the entitlement programs will cost under current law. As a result, the proposed entitlement cap would mandate $1.8 trillion in entitlement cuts over the coming decade.[2]

Broad-based Opposition to Entitlement Cap Proposal

When a nearly identical version of this proposal was debated in 2004, a broad array of organizations expressed strong opposition to entitlement cap proposals. For example, in a letter to Speaker Dennis Hastert on June 22, 2004, the American Legion stated, “The American Legion opposes any and all entitlement cap proposals. Although we fully support deficit reduction, we consider an entitlement cap in any form to be the wrong approach, and a potential breach of national trust.”

Similarly, the Paralyzed Veterans of America wrote in a letter to Members of Congress on June 22, 2004, “PVA would also like to urge you to oppose any proposed amendment that would enact caps on entitlement spending.” In a strong letter sent on June 21, 2004, the AARP stated, “AARP urges you to reject any entitlement caps because they would jeopardize the health and economic security of millions of vulnerable Americans.”

The required entitlement cuts would not be especially deep in the first year, but their severity would grow rapidly thereafter. By 2011, entitlements other than Social Security would have to be cut almost 14 percent on average and the cuts would cumulate to $408 billion over the five-year period 2007-2011. The depth of the cuts would continue to grow forever. By 2016, the entitlement cuts would average more than 24 percent — reaching $416 billion in that year alone — and would total $1.8 trillion over the ten-year period.

The RSC entitlement cap requires cuts of this magnitude primarily because of its treatment of Medicare and Medicaid. Under the proposal, the entitlement cap for each year would be set at a level equal to the sum of the costs in the prior fiscal year of all entitlement programs except Social Security, with two adjustments. One adjustment would be made for projected increases or decreases in the number of people eligible for each entitlement program. The second adjustment would incorporate cost-of-living adjustments required by statute. If a program has no statutory COLA or only a partial inflation adjustment, an adjustment would be made equal to the projected increase in the Consumer Price Index.

The costs of Medicare and Medicaid rise with increases in the cost of health care. As is well known, health care costs are rising rapidly in the private and public sectors alike. The RSC entitlement cap, however, assumes that Medicare and Medicaid costs per beneficiary will rise an average of only 2.2 percent per year over the coming decade, the projected rate of increase in the Consumer Price Index.

Hardly any employer in America can hold increases in health insurance premium costs to 2.2 percent per beneficiary per year; basic health care costs are climbing much faster than that. Mostly for this reason, the RSC entitlement cap would be set $1.8 trillion below projected entitlement costs. As a consequence, not only Medicare and Medicaid but all entitlements other than Social Security would be at risk of deep cuts.

The RSC proposal also includes interest payments on the debt as an entitlement program. This means that whenever interest payments rise faster than inflation, the entitlement cap would be breached by a larger amount, necessitating still deeper program cuts. This is significant because interest payments are indeed projected to rise over the coming decade, both because interest rates will rise from their current low levels as the economy recovers more fully and because the amount of debt on which interest will be paid will continue to increase as the government racks up continued large deficits. Of particular note, every additional tax cut increases projected deficits and debt — and hence interest payments on the debt — and thus would require even deeper cuts in entitlement programs.

Under the proposed RSC entitlement cap, the exact size of the cutbacks in each program would depend on decisions that Congress and the President would make. In theory, Congress and the President could initially decline to enact any legislation cutting entitlement programs and let automatic entitlement cuts do all the “dirty work.” Under the rules for automatic cuts contained in the RSC proposal, a few programs (such as Medicare Hospital Insurance) would be exempt from the automatic cuts, and some other programs (such as veterans’ programs, Medicare physicians’ coverage, the Medicare drug benefit, and Medicaid) could be cut no more than two percent per year through an automatic cut. (It should be noted that these programs would be cut an additional two percent each time an automatic cut occurred, so the automatic cuts in these programs could mount to substantial levels over time. If automatic cuts occurred each year, these programs could be cut 18 percent by 2016.)

Deep Cuts in RSC Budget Would be Insufficient to Comply with the Cap

The budget plan released by the Republican Study Committee on March 8 contains cuts in a number of entitlement programs. These include Medicare cuts of $218 billion over five years, which the RSC says could be achieved through some combination of such options as doubling the Medicare Part B premium, raising Medicare deductibles and co-payments, and setting payments to hospitals, home health agencies, and skilled nursing facilities at levels that fall farther behind health care inflation with each passing year.

The RSC budget also would replace Medicaid with a block grant that does not keep pace with health care costs and that would lower projected federal Medicaid payments to states by $92 billion over five years. Some of the other entitlement reduction proposals in the RSC budget would eliminate student loans for graduate students, eliminate the trade adjustment assistance programs, and cut farm programs substantially.

The RSC budget includes painful and highly controversial proposals that would cut projected entitlement expenditures by a total of $359 billion over five years. Yet if every one of these controversial proposals were enacted, these cuts would still fall $50 billion short of the entitlement reductions that would be required over the next five years under the RSC’s entitlement cap proposal.

It is unthinkable, however, that the bulk of the cuts would occur through automatic cuts; the automatic cuts are designed to be so unpalatable that Congress and the President would be compelled to enact legislation cutting entitlements in order to avert or minimize the automatic cuts. Indeed, if all of the reductions needed to comply with the RSC entitlement cap were made through the automatic cuts, then the programs that would be fully subject to the automatic cuts — including farm-price supports, crop insurance, extended unemployment benefits, trade adjustment assistance, the Earned Income Tax Credit, vocational rehabilitation, child care payments to states, and the Social Services Block Grant (Title XX) — as well as the salaries of Member of Congress and Senators — would be entirely eliminated by 2013.

It is inconceivable that Congress would sit idly by and allow these programs — and Members’ own salaries — to be eliminated. Congress clearly would seek to spread the pain more broadly, by enacting legislation that cut more heavily into entitlement programs that have some protection from the automatic cuts, such as Medicare and Medicaid.

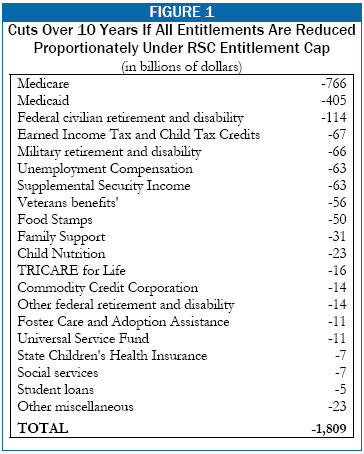

The bottom line is that all entitlement programs except Social Security would be at serious risk of being subject to large cutbacks, since $1.8 trillion in program reductions over ten years would be mandated by law. The table on page one shows the ten-year cuts that would be made in each entitlement program if all entitlements other than Social Security were cut by the same percent.

End Notes

[1] See http://www.house.gov/pence/rsc/doc/RSC_2007_BUDGET.pdf.

[2] The proposal treats interest payments on the federal debt as an entitlement, and therefore subject to the proposed entitlement caps. CBO data show that the combined cost of entitlements and interest would be $2.1 trillion over the caps in the ten-year period through 2016. By cutting entitlements $1.8 trillion, the deficits and debt would be lower than projected, and $0.3 trillion in interest payments would be saved, producing the required total savings of $2.1 trillion. This explains why entitlements themselves would have to be cut $1.8 trillion to adhere to the caps. Our analysis is based on the legislative text of HR 2290, which Rep. Hensarling (the chairman of the RSC task force on budget and spending) introduced in 2005. The RSC has not introduced legislative text to accompany the new “Contract” but their document refers to HR 2290.

More from the Authors