Tax Credit Changes Under Discussion Won’t Close House Health Bill’s Massive Affordability Gaps

The Affordable Care Act (ACA) repeal bill adopted by House committees would cut financial assistance for low- and moderate-income people buying health insurance in the individual market by $312 billion, according to Congressional Budget Office (CBO) estimates.[1] The bill sharply reduces tax credits that help people pay premiums, especially for people who are older, have lower incomes, or live in states with high health insurance costs.[2] It also eliminates ACA subsidies that reduce deductibles, co-pays, and other out-of-pocket costs for people with incomes below 250 percent of the poverty line, and it allows insurers to charge older people much higher premiums than the ACA permits. Partly as a result, the bill would cause 10 million people to lose private health insurance, the CBO projects — on top of 14 million who would lose Medicaid coverage.[3]

The options under discussion wouldn’t come close to closing the House bill’s massive affordability gaps.Congressional Republicans are considering modest changes to their tax credits to mitigate the large cuts in financial assistance for older and/or lower-income people. House Speaker Paul Ryan has suggested some increases in the credits for older consumers,[4] while Senator John Thune has proposed cutting the credits for higher-income people and reinvesting the savings in larger credits for people with lower incomes.[5] But the options under discussion wouldn’t come close to closing the House bill’s massive affordability gaps.

-

Addressing affordability gaps, especially for lower-income seniors, would require far larger increases in tax credits than appear to be on the table. According to CBO, a 64-year-old with income of $26,500 would see premiums rise by an average of $4,200 and tax credits fall by an average of $8,700 under the House bill in 2026. As a result, her net premium (the amount she pays out of pocket) would rise by $12,900 — or more than seven-fold — and would equal 55 percent of her income.

Protecting this consumer, and older people at similar income levels, would thus require raising the House bill’s tax credits for lower-income, older people by nearly $13,000 in 2026. Even if the provision allowing insurers to charge older consumers higher premiums were dropped from the House bill, protecting these consumers would still require raising tax credits by nearly $9,000. Increases of this magnitude do not appear to be under discussion. Nor could such increases be financed by starting the phase-out of the tax credits at modestly lower income levels than the bill now calls for ($75,000 for singles and $150,000 for couples), as Senator Thune has proposed.

-

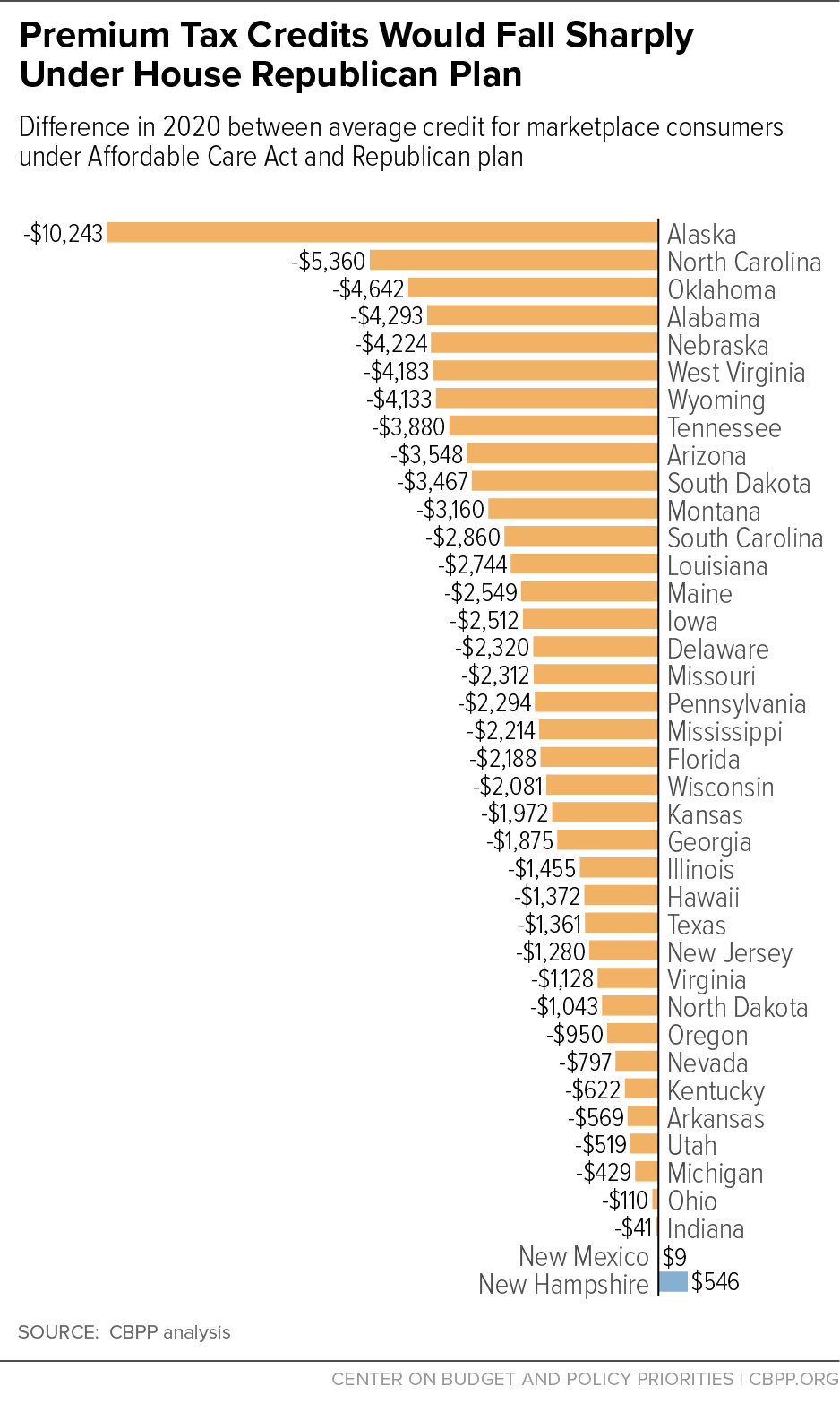

Addressing affordability gaps in high-cost states would require basing tax credits on the actual cost of insurance, as under the ACA. The ACA’s premium tax credits are based on the local cost of insurance, so people in consistently high-cost states like Alaska, Delaware, Louisiana, Maine, Wisconsin, West Virginia, and Wyoming get larger subsidies than people in lower-cost states.[6] Because the House bill eliminates the ACA’s geographic adjustment, it cuts tax credits especially sharply for people in high-cost states. (See Figure 1.)

Without restoring this geographic adjustment, closing the House bill’s affordability gaps for people in these states would be almost impossible. For example, even if tax credits were somehow raised by almost $9,000 to protect the average 64-year-old with income at 175 percent of the federal poverty line (from CBO’s example above), tax credits for such consumers would still be at least $3,000 lower than under current law in ten states: Alaska, North Carolina, Oklahoma, Arizona, Wyoming, Nebraska, West Virginia, Tennessee, Alabama, and Montana.

Similarly, the House bill cuts tax credits for current marketplace consumers by an average of $1,700 nationwide in 2020, the Kaiser Family Foundation estimates.[7] Even in the very unlikely event that congressional Republicans modified their bill to raise tax credits by that amount in every state, people in high-cost states would still see large losses. Tax credits would fall by an average of more than $1,000 for current marketplace consumers in 13 states, and by an average of more than $2,000 in eight states: Alaska, North Carolina, Oklahoma, Alabama, Nebraska, West Virginia, Wyoming, and Tennessee.

- Addressing affordability gaps would also require restoring the ACA’s assistance with out-of-pocket costs and its requirement that insurers offer low-deductible options, both of which the House bill eliminates. In addition to reducing financial assistance that helps people pay premiums, the House bill eliminates the ACA’s cost-sharing reductions that lower deductibles, co-pays, and other out-of-pocket costs for people with incomes below 250 percent of the poverty level (about $60,000 for a family of four). In 2016, these payments lowered out-of-pocket costs by an average of about $1,100 for more than 6 million people, or almost 60 percent of all marketplace consumers.[8]

The House bill would also generally raise deductibles and other out-of-pocket costs for people with incomes above 250 percent of the poverty line, who don’t get cost-sharing reductions under the ACA. The bill effectively eliminates the ACA’s requirement that insurers at least offer consumers the choice of a lower-deductible plan, and CBO projects that many insurers would respond by offering only high-deductible options. As a result, CBO concludes, “individuals’ cost-sharing payments, including deductibles, in the nongroup market would tend to be higher than those anticipated under current law.”[9] Tweaking tax credits won’t do anything to address these increases.

One simple approach would solve the problems with the House health bill’s tax credits: maintaining the current structure and generosity of the ACA’s subsidies. Unfortunately, congressional Republicans do not seem to be considering that approach. The modest changes they are discussing instead would almost certainly leave health insurance and health care out of reach for millions of people.

End Notes

[1] Jacob Leibenluft, “For House GOP Health Bill, Deficit Reduction and Coverage Loss for Millions Go Together,” Center on Budget and Policy Priorities, March 15, 2017, https://www.cbpp.org/blog/for-house-gop-health-bill-deficit-reduction-and-coverage-loss-for-millions-go-together.

[2] Aviva Aron-Dine and Tara Straw, “House Tax Credits Would Make Health Insurance Far Less Affordable in High Cost States,” Center on Budget and Policy Priorities, revised March 16, 2017, https://www.cbpp.org/research/health/house-tax-credits-would-make-health-insurance-far-less-affordable-in-high-cost.

[3] Congressional Budget Office, “Cost Estimate for the American Health Care Act,” March 13, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/americanhealthcareact.pdf.

[4] “Fox News Sunday” transcript, March 19, 2017, http://www.foxnews.com/transcript/2017/03/19/paul-ryan-on-efforts-to-repeal-replace-obamacare-rep-nunes-previews-comey/.

[5] Matthew J. Belvedere, “Sen. Thune proposes amendment to add means test for tax credits in House GOP health bill,” CNBC, March 15, 2017, http://www.cnbc.com/2017/03/15/sen-thune-proposes-an-amendment-to-means-test-for-health-tax-credits-in-house-gop-bill.html.

[6] The states listed are those that had above-average individual-market premiums for three years in a row and also had above-average employer-market premiums in 2016.

[7] Cynthia Cox, Gary Claxton, and Larry Levitt, “How Affordable Care Act Repeal and Replace Plans Might Shift Health Insurance Tax Credits,” Kaiser Family Foundation, March 10, 2017, http://kff.org/health-reform/issue-brief/how-affordable-care-act-repeal-and-replace-plans-might-shift-health-insurance-tax-credits/.

[8] Department of Health and Human Services Assistant Secretary for Planning and Evaluation, “Health Insurance Marketplace Cost Sharing Reduction Subsidies by Zip Code and County for 2016,” https://aspe.hhs.gov/health-insurance-marketplace-cost-sharing-reduction-subsidies-zip-code-and-county-2016 and Center for Medicare & Medicaid Services, “March 31, 2016 Effectuated Enrollment Report,” June 30, 2016, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-06-30.html.

[9] Congressional Budget Office, “Cost Estimate for the American Health Care Act,” March 13, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/americanhealthcareact.pdf.

More from the Authors