Alexander-Murray Legislation Can’t Undo the Severe Harm Resulting From Individual Mandate Repeal

Senate Republican leaders have released a new version of their tax bill that adds a provision repealing the Affordable Care Act’s individual mandate, the requirement that most people enroll in health insurance coverage or pay a penalty. Nothing in the Alexander-Murray bill can undo the damage that would result from repealing the individual mandate.Some Senate Republicans have suggested that the harmful effects of eliminating the mandate — increased premiums, greater instability in the individual market, and millions more uninsured — could be mitigated if Congress also adopted the bipartisan individual market reform package introduced by Senators Lamar Alexander and Patty Murray.[1] By itself, the Alexander-Murray legislation could help strengthen the individual market and reduce premiums.[2] But nothing in the bill could undo the damage that would result from repealing the individual mandate.

Repealing the individual mandate would:

- Increase individual market premiums by about 10 percent, according to recent Congressional Budget Office (CBO) estimates.[3]

- Create further instability for the individual market, especially in the near term.

- Increase the number of Americans without health insurance by millions beginning in 2019, when the mandate would be repealed, reaching 13 million by 2025, according to CBO.

Senators Alexander and Murray negotiated their bill in good faith, as a compromise effort to reduce individual market premiums and increase market stability. But Senate Republicans are now seeking to use the bill as cover for changes that would do the exact opposite. As Senator Murray observed, attempting to repair the damage from repealing the individual mandate by passing the Alexander-Murray bill “is like trying to put out a fire with penicillin.”[4]

Moreover, once the savings from individual mandate repeal are dedicated to corporate tax cuts — as Senate Republicans are proposing — it will be nearly impossible to undo the damage in any subsequent legislative vehicle.[5] Nor would congressional Republicans likely seek to do so. Instead, some congressional Republicans have argued that the individual market instability and reductions in coverage resulting from mandate repeal would make it easier for them to repeal the rest of the Affordable Care Act next year, causing millions more people to lose coverage.[6]

Impact of Repealing the Mandate and Passing the Alexander-Murray Bill

The Alexander-Murray bill would undo almost none of the harmful effects of repealing the individual mandate on individual market premiums, market stability, or health insurance coverage.

Individual Market Premiums

The net effect of repealing the individual mandate and passing the Alexander-Murray bill would be a small reduction in silver plan premiums in 2019, higher premiums for all other plans beginning in 2019, and higher premiums for all plans beginning in 2020.[7]

The Alexander-Murray legislation would restore cost-sharing reduction (CSR) payments to insurers, but only through 2019. CSR payments reimburse insurers for the cost-sharing assistance (lower deductibles, co-insurance, and co-payments) they are required to provide to lower-income enrollees. Because this assistance is available only to consumers who enroll in silver plans, insurers in most states raised premiums for silver plans — but not bronze, gold, or platinum plans — to account for the Trump Administration’s decision to stop CSR payments.[8] That is why silver plan premiums increased about 14 percentage points more than bronze or gold plan premiums for 2018.[9] Among unsubsidized consumers purchasing coverage through HealthCare.gov, 57 percent enrolled in non-silver plans for 2017, and a larger fraction are likely to do so this year, given the higher premium increases for silver compared to bronze or gold plans.[10]

The Alexander-Murray bill would reverse only the premium increases resulting from the Administration’s decision not to pay CSRs, and only for 2019.[11] In contrast, repealing the individual mandate would increase premiums in 2019 and beyond, and for all individual market plans, not just silver plans. Without the individual mandate, fewer healthy people would sign up for individual market coverage, increasing average costs. CBO estimates this would raise premiums by about 10 percent, while some major insurers have said they would have to raise premiums across the board by about 15 percent if the individual mandate were repealed or no longer enforced.[12] The premium increase would wipe out much of the 2019 silver plan premium reduction from passing the Alexander-Murray bill, while the Alexander-Murray bill would address none of the premium increases for other plans or in other years. (See Table 1.)

| TABLE 1 | |||||||

|---|---|---|---|---|---|---|---|

| Percent Change in Individual Market Premiums Compared to Annual Projections Under Current Law, Supposing Both Individual Mandate Repeal and Enactment of Alexander-Murray | |||||||

| 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Bronze plans | +10% | +10% | +10% | +10% | +10% | +10% | +10% |

| Silver plans | -4% to -8% | +10% | +10% | +10% | +10% | +10% | +10% |

| Gold plans | +10% | +10% | +10% | +10% | +10% | +10% | +10% |

Individual Market Stability

The combined effect of repealing the individual mandate and passing the Alexander-Murray bill would be to substantially increase insurer uncertainty and confusion and the risk that insurers exit the individual market.

If it were adopted without other measures undermining the individual market, the Alexander-Murray bill’s potential benefits for individual market stability would go beyond its direct effects. Enactment would show that Congress can come together on a bipartisan basis to protect individual market consumers from the Administration’s efforts to undermine the market. That would reassure insurers, making it more likely that they would re-enter, continue to participate in, or expand their participation in the individual market. But coupling Alexander-Murray with individual mandate repeal would eliminate any of those benefits. Instead of signaling a congressional commitment to a stable individual market, it would show the exact opposite.

Moreover, the uncertainty created by permanent individual mandate repeal would far exceed the uncertainty alleviated by a short-term appropriation for CSRs. As the Kaiser Family Foundation’s Larry Levitt explained, insurers more or less understood how to price for the loss of CSR payments, because they know the cost of providing CSRs to eligible enrollees.[13] They have much less idea how to price for elimination of the individual mandate — for example, how many people they should assume will leave the market, how much healthier this group is than average, and how quickly the full effects of repealing the mandate would be felt.

Facing substantial uncertainty about how to price, some insurers might instead opt to simply exit the individual market altogether, reducing consumer choice or leaving some consumers without any options. Indeed, a number of insurers interviewed about the possibility of mandate repeal for 2018 said that it would lead them to “seriously consider” market withdrawal.[14]

Health Insurance Coverage

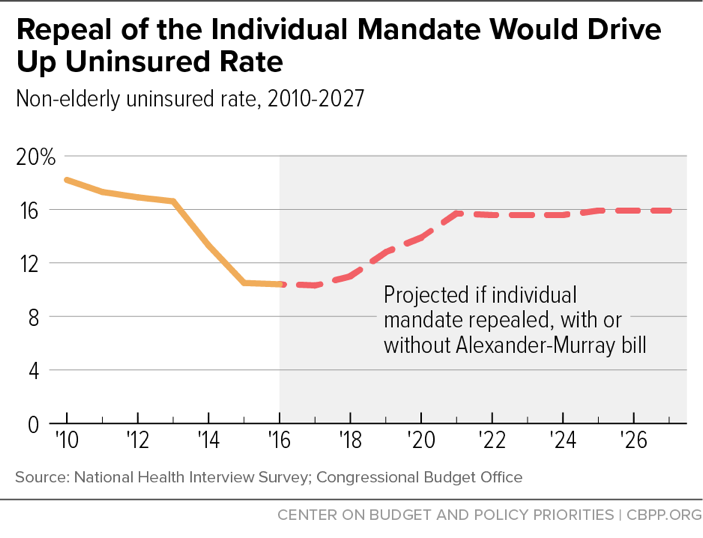

The Alexander-Murray legislation does not include any provisions — such as increased marketplace subsidies — that would undo the coverage reductions from individual mandate repeal. Thus, the net effect of repealing the mandate and passing the Alexander-Murray bill would still be a 13 million increase in the number of uninsured Americans, increasing the share of non-elderly Americans without health insurance from about 11 percent to about 16 percent. (See Figure 1.)

CBO projects that, by itself, the Alexander-Murray legislation “would not substantially change the number of people with health insurance coverage.”[15] Likewise, CBO predicted minimal coverage effects from simply restoring payment of CSRs.[16] That is in part because unsubsidized consumers would mostly switch from silver to bronze or gold plans, rather than dropping coverage, in response to CSR-driven silver plan increases. Meanwhile, enrollment in employer coverage and Medicaid is unaffected by decisions about whether to pay CSRs.

In contrast, repeal of the individual mandate would increase the number of uninsured Americans by 4 million in 2019, when it first took effect; 12 million by 2021; and 13 million by 2025, based on CBO estimates. In addition to large coverage losses in the individual market, repealing the mandate would also lead fewer people to take up employer coverage or Medicaid, partly because — absent the mandate — some low-income people would never learn they are Medicaid eligible.

Some Republicans have argued that because the coverage losses that would result from repeal of the mandate would be “voluntary,” they aren’t troubling. But this view is deeply mistaken, for several reasons. First, some of the coverage losses from repealing the mandate would not be “voluntary” in any sense. They would occur not as a direct result of mandate repeal, but rather because repeal would hurt the individual market risk pool and raise premiums, which would then put coverage out of reach for some people. Second, regardless of why people lose coverage, those who become uninsured suffer harm. People without health insurance lack access to preventive care, are less likely to receive needed care, have worse health outcomes, and are exposed to medical bankruptcy if they become seriously ill and seek treatment. Third, many of the those who would become uninsured if the mandate were repealed would ultimately get seriously ill and seek care, but would be unable to pay for it. That would leave their care to be paid for — involuntarily — by other participants in the health care system.[17]

Using Mandate Savings for Tax Cuts Would Make Undoing Coverage Losses Nearly Impossible

Looking beyond the Alexander-Murray proposal, the harms from repealing the individual mandate would be hard to reverse in any subsequent vehicle. For example, some Senate Republicans and conservative experts have suggested repealing the individual mandate and replacing it with alternative measures, such as additional use of automatic enrollment to sign people up for coverage or stronger continuous coverage incentives.[18] Any such measures would likely fall well short as a substitute for the mandate, and some could do harm.[19] But if these alternatives succeeded at all in increasing coverage, they would cost the federal government money, for the same reason that repeal of the individual mandate saves: when more people enroll in health insurance, the federal government spends more on premium tax credits, Medicaid, and the tax exclusion for employer-sponsored coverage.

The Senate bill uses the $318 billion in savings from repealing the individual mandate to help finance its permanent corporate rate cut. Thus, these savings would not be available to pay for any individual mandate replacement. Instead, any replacement would have to be paid for with new tax increases or program cuts, making its enactment even more difficult than it would otherwise be.

End Notes

[1] See Jordain Carney, “Key GOP senator: ObamaCare payments likely to be included in funding bill,” The Hill, November 15, 2017, http://thehill.com/homenews/senate/360495-key-gop-senator-obamacare-payments-likely-to-be-included-in-funding-bill. While Senate Republican leaders have suggested that they might be willing to pass the Alexander-Murray bill after the tax bill, some House Republicans have continued to voice strong opposition. See Holly Rosenkrantz, “‘Terrible’ to Add Obamacare Fix in Spending Deal: Freedom Caucus,” Bloomberg, November 15, 2017.

[2] Robert Greenstein, “Alexander-Murray Agreement an Important Step Toward Bipartisanship on Health Care,” Center on Budget and Policy Priorities, October 18, 2017, https://www.cbpp.org/press/statements/greenstein-alexander-murray-agreement-an-important-step-toward-bipartisanship-on.

[3] Congressional Budget Office, “Repealing the Individual Health Insurance Mandate: An Updated Estimate,” November 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53300-individualmandate.pdf.

[4] “Senator Murray: Tacking Bipartisan Alexander-Murray Health Bill to Partisan Republican Tax Reform ‘Like Trying to Put Out a Fire with Penicillin,’” November 15, 2017, https://www.murray.senate.gov/public/index.cfm/newsreleases?ID=41D56DEB-C7E8-404A-82C7-924A4FF3CC75.

[5] Aviva Aron-Dine, “Senate Tax Bill Would Add 13 Million to Uninsured to Pay for Tax Cuts of Nearly $100,000 Per Year for the Top 0.1 Percent,” Center on Budget and Policy Priorities, November 15, 2017, https://www.cbpp.org/blog/senate-tax-bill-would-add-13-million-to-uninsured-to-pay-for-tax-cuts-of-nearly-100000-per-year.

[6] See, for example, Terrence Dopp, “Obamacare Mandate’s End Will Make Repeal Try Easier: Republicans,” Bloomberg, November 15, 2017.

[7] Silver plans are those with actuarial values of about 70 percent; these plans serve as the “benchmark” plans for setting premium tax credits.

[8] Even the minority of states that instructed insurers to increase premiums for all plans for 2018 to account for non-payment of CSRs may switch to instructing them to raise premiums for silver plans only for 2019. For a survey of state approaches, see Sabrina Corlette, Kevin Lucia, and Maanasa Kona, “States Step Up to Protect Consumers in Wake of Cuts to ACA Cost-Sharing Reduction Payments,” Georgetown Center on Health Insurance Reforms, October 31, 2017, https://ccf.georgetown.edu/2017/10/31/states-step-up-to-protect-consumers-in-wake-of-cuts-to-aca-cost-sharing-reduction-payments/. In many states, insurers only raised premiums for silver plans sold through the ACA marketplaces, meaning that lower-premium silver plans are available off marketplace.

[9] Ashley Semanskee, Gary Claxton, and Larry Levitt, “How Premiums Are Changing In 2018,” Kaiser Family Foundation, November 14, 2017, https://www.kff.org/health-reform/issue-brief/how-premiums-are-changing-in-2018/. Kaiser previously projected a 19 percent increase in silver plan premiums from non-payment of CSRs. Larry Levitt, Cynthia Cox, and Gary Claxton, “The Effect of Ending the Affordable Care Act’s Cost-Sharing Reduction Payments,” Kaiser Family Foundation, April 25, 2017, https://www.kff.org/health-reform/issue-brief/the-effects-of-ending-the-affordable-care-acts-cost-sharing-reduction-payments/.

[10] Centers for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period Final Open Enrollment Report,” March 15, 2017, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-03-15.html. Increases in sticker price premiums generally affect only unsubsidized individual market consumers, since premium tax credits adjust to shield subsidized consumers from premium increases.

[11] For many subsidized consumers, the increases in silver plan premiums resulting from the Administration’s decision not to pay CSRs will actually make gold and bronze plans more affordable than they otherwise would be. See Aviva Aron-Dine and Tara Straw, “The Outlook for Marketplace Open Enrollment,” Center on Budget and Policy Priorities, October 31, 2017, https://www.cbpp.org/research/health/the-outlook-for-marketplace-open-enrollment.

[12] For example, CareFirst, a major insurer in Maryland, Virginia, and Washington D.C., requested additional rate increases of 15 percent due to concerns about the individual mandate (see https://www.vox.com/2017/5/8/15563448/trump-insurance-premiums-2018), and Pennsylvania’s insurance commissioner reported in June that insurers would request additional rate increases averaging 14.5 percent if concerns about mandate non-enforcement or repeal were not addressed ( see http://www.media.pa.gov/Pages/Insurance-Details.aspx?newsid=248).

[13] Larry Levitt, “Insurers adjusted reasonably well to termination of cost-sharing payments and some people are actually paying lower premiums. Why is the individual mandate different? (thread),” Twitter, November 15, 2017, https://twitter.com/larry_levitt/status/930782635693084672.

[14] Interviews took place in December 2016 and January 2017. Sabrina Corlette et al., “Uncertain Future for Affordable Care Act Leads Insurers to Rethink Participation, Prices,” Urban Institute, January 2017, https://www.urban.org/sites/default/files/publication/87816/2001126-uncertain-future-for-affordable-care-act-leads-insurers-to-rethink-participation-prices_1.pdf.

[15] Congressional Budget Office, “Cost Estimate: Bipartisan Health Care Stabilization Act of 2017,” October 25, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/bipartisanhealthcarestabilizationactof2017_0.pdf

[16] In fact, CBO projected small coverage increases over time if CSRs are not paid. That’s because, as noted above, not paying CSRs makes coverage more affordable for some subsidized consumers. Congressional Budget Office, “The Effects of Terminating Payments for Cost-Sharing Reductions,” August 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53009-costsharingreductions.pdf.

[17] For a more complete discussion of these issues, see Aviva Aron-Dine, “Republicans Considering Increasing Number of Uninsured by Millions, Raising Premiums to Help Pay for Tax Cuts,” Center on Budget and Policy Priorities, updated November 9, 2017, https://www.cbpp.org/research/health/republicans-considering-increasing-number-of-uninsured-by-millions-raising-premiums.

[18] See Sarah Kliff, “The Newest GOP Health Idea? Auto-Enroll the Uninsured,” Vox, April 19, 2017, https://www.vox.com/policy-and-politics/2017/4/19/15363976/auto-enroll-uninsured-health-care-plan, and James C. Capretta, “Republicans are wrong about the individual mandate,” American Enterprise Institute, November 6, 2017, https://www.aei.org/publication/republicans-are-wrong-about-the-individual-mandate/.

[19] See Paul N. Van de Water, “Automatic Enrollment in Health Insurance Would Be Complex and Difficult to Administer,” Center on Budget and Policy Priorities, June 16, 2017, https://www.cbpp.org/research/health/automatic-enrollment-in-health-insurance-would-be-complex-and-difficult-to, and Sarah Lueck, “Commentary: House GOP Proposed Penalty for Non-Coverage Fails on Several Fronts,” Center on Budget and Policy Priorities, March 8, 2017, https://www.cbpp.org/health/commentary-house-gop-proposed-penalty-for-non-coverage-fails-on-several-fronts.

More from the Authors

Areas of Expertise