Have the 2001 and 2003 Tax Cuts Made The Tax Code More Progressive?

With debate beginning on the Senate budget resolution, congressional supporters of the 2001 and 2003 tax cuts have begun recycling old arguments for extending all of these tax cuts. Among these is the claim that the tax cuts have made the tax code more progressive.

The reality is that the tax cuts have made the tax code more regressive. A progressive tax code is one that makes the distribution of after-tax income more equal than the distribution of pre-tax income, and one tax code is “more progressive” than another if it has a larger effect in reducing income inequality. So, in order for the 2001 and 2003 tax cuts to have made the tax code more progressive, after-tax incomes would have to be less unequal today than if the tax cuts had not occurred. In fact, however, the reverse is true: the tax cuts made the distribution of after-tax income more unequal.

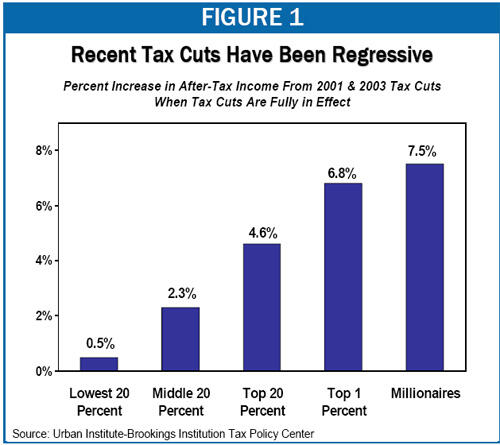

When fully in effect, the 2001 and 2003 tax cuts will increase the incomes of high-income households by a much larger percentage than the incomes of low- or middle-income households, according to estimates by the nonpartisan Urban-Brookings Tax Policy Center. As Figure 1 shows, the tax cuts will increase the after-tax incomes of households with annual incomes above $1 million by an average of 7.5 percent, compared to a 2.3 percent increase for households in the middle of the income spectrum and a 0.5 percent increase for the lowest-income 20 percent of households. This means that high-income households will hold alarger share of the nation’s after-tax income as a result of the tax cuts.

Claims That the Tax Cuts Were Progressive Rely on a Flawed Measure

Supporters of the tax cuts generally do not attempt to refute these facts. Instead, they frequently point to CBO data showing that high-income households paid a larger percentage of federal taxes in 2004 (after the tax cuts) than in 2000 (before the tax cuts). They claim that this shows that the tax cuts made the tax system more progressive, and they imply that it means that high-income households received disproportionately small tax cuts, or even that these households are paying more in taxes now than in earlier years. Such claims and inferences are incorrect.

Other Measures Also Cast Doubt on the Tax Cuts’ Fairness

Comparisons of percentage changes in after-tax earnings, such as those shown in Figure 1 above, measure the tax cuts’ effect on the distribution of income. But in evaluating the tax cuts’ overall fairness, it is also useful to examine the cost of the tax cuts going to different income groups, as well as to compare these costs with expenditures on leading national priorities.

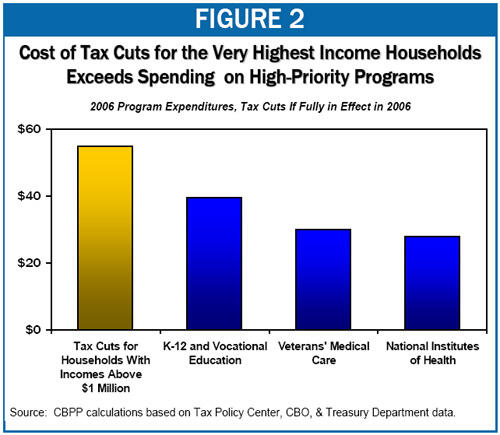

For example, over the next ten years (assuming the tax cuts are extended), more than $700 billion will be spent on tax cuts for the 0.3 percent of households with incomes over $1 million, with these tax cuts averaging over $150,000 per household per year.* In today’s terms, the annual cost of tax cuts for this group will exceed what the federal government currently spends on K-12 and vocation education, veterans’ medical care, or the National Institutes of Health (see Figure 2). At issue is whether providing such large tax benefits to households at the very highest income levels represents the best — or most equitable — use of scarce public resources.

* See Aviva Aron-Dine, “The Skewed Benefits of the Tax Cuts, 2008-2017,” Center on Budget and Policy Priorities, revised February 6, 2007, https://www.cbpp.org/2-5-07tax.htm.

The same CBO data cited by tax-cut supporters also show that high-income households are paying considerably less of their income in taxes now than before the tax cuts. In 2000, households in the top 1 percent of the income scale paid an average of 24.2 percent of their income in federal individual income taxes. By 2004 (the latest year for which data are available), that figure had fallen to 19.6 percent, the lowest level since 1986. That decline works out to a reduction in these households’ tax burden of about $58,000 per household (in 2004 terms).

The CBO data also show that income tax burdens fell by considerably more for high-income households than for other households (see Table 1). While effective federal income tax rates dropped by 4.6 percentage points for those in the top 1 percent of the income scale, they fell by only 2.1 percentage points for those in the middle of the income scale, and by 1.6 percentage points for those at the bottom.[1]

| Table 1: | |

| Income Group | Drop in Effective Federal Individual Income Tax Rate (Percentage Points) |

| Lowest 20 percent | -1.6% |

| Second 20 percent | -2.3% |

| Middle 20 percent | -2.1% |

| Fourth 20 percent | -2.2% |

| Top 20 percent | -3.6% |

| Top 1 Percent | -4.6% |

| Source: Congressional Budget Office | |

As these facts suggest, the change in the “percentage of taxes paid” is not a useful metric for assessing which income groups benefited the most from the tax cuts or whether the tax cuts made the tax code more or less progressive. This measure is fundamentally flawed in three respects.

- It is distorted by growing inequality in pre-tax incomes. When high-income households’ share of the pre-tax incomein the nation increases — as it did in 2003, 2004, and (new data show) 2005 — the share of the total taxes that high-income households pay naturally rises as well, for reasons having nothing to do with legislated changes in tax policy.

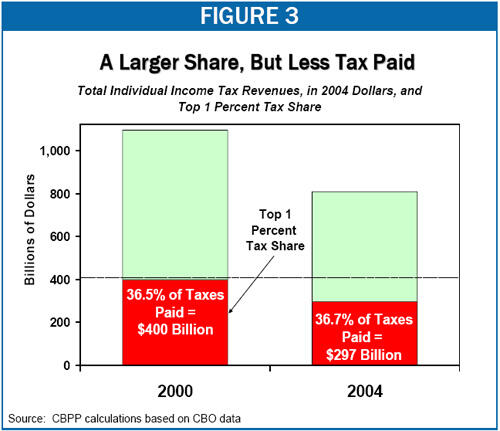

- The “percentage of taxes paid” measure also fails to take into the account the fact that when a tax cut reduces the total amount of revenue collected, high-income households can get a large reduction in their tax bills even if the percentage of taxes they pay is increasing. For example, between 2000 and 2004, the share of individual income taxes paid by the top 1 percent of households edged up marginally, from 36.5 percent to 36.7 percent. But total revenues from the individual income tax fell by more than $250 billion between 2000 and 2004 (in 2004 dollars). The slightly larger percentage of taxes that high-income households paid worked out to a considerably smaller amount of taxes paid — about $100 billion less, adjusted for inflation — as well as a considerably smaller average per-household tax burden (see Figure 3 and Table 1).

- Finally, the “percentage of taxes paid” measure fails to take into account the fact that tax cuts that are financed by government borrowing — as the 2001 and 2003 tax cuts were — must eventually be paid for. As former Federal Reserve Chairman Alan Greenspan warned, “If you’re going to lower taxes, you shouldn’t be borrowing essentially the tax cut. And that over the long run is not a stable fiscal situation.” Simply stated, funds that are borrowed must eventually be paid back.

Tax Policy Center data show that even if the costs of the tax cuts eventually are paid for through measures that reduce income by the same percentage for households at every income level (which is roughly what could occur under a balanced package of program reductions and progressive tax increases), the bottom four-fifths of households will end up worse off, on average, than if the tax cuts had not been enacted(see Table 2).[2] In other words, the large majority of American households are likely to lose more from the measures eventually needed to pay for the tax cuts than they gain from the tax cuts themselves.

| Table 2: | ||

| Income Group | Average Tax Cut, No Financing | Average Tax Increase/Cut, With Financing |

| Lowest 20 percent | -$45 | +$230 |

| Second 20 percent | -470 | +220 |

| Middle 20 percent | -840 | +370 |

| Fourth 20 percent | -1,500 | +660 |

| Top 20 percent | -8,000 | -1,400 |

| Top 1 percent | -67,000 | -27,000 |

| Above $1 million | -162,000 | -73,000 |

| Source: CBPP calculations based on Tax Policy Center data | ||

End Notes

[1] It should be noted that the Tax Policy Center estimates provide a better guide to the effects of the tax changes enacted in 2001 and 2003 than do the Congressional Budget Office data. The CBO data reflect the effects not only of legislative changes but also of changes in the economy. As a result, part of the drop in effective tax rates that the CBO data show for households at the top of the income scale likely reflects the decline in their incomes (which, as of 2004, had not yet recovered to their 2000 level in real terms). On the other hand, the CBO data may understate the regressivity of the tax cuts relative to what it will be when all the tax cuts are fully in effect, since some income tax cuts that are highly skewed to households at the top of the income scale were not yet in effect in 2004.

[2] For further discussion of these issues, see William G. Gale, Peter R. Orszag, and Isaac Shapiro, “The Ultimate Burden of the Tax Cuts: Once the Tax Cuts Are Paid For, Low- and Middle-Income Households Likely to Be Net Losers, On Average,” Center on Budget and Policy Priorities, June 2, 2004, https://www.cbpp.org/6-2-04tax.htm.

More from the Authors