Puerto Rico Economic Growth Package Should Include Work-Promoting Earned Income Tax Credit

As a congressional task force studies proposals to boost economic growth in Puerto Rico, tax relief for low-income working families — delivered through an Earned Income Tax Credit (EITC) — should be a key component of such a package.

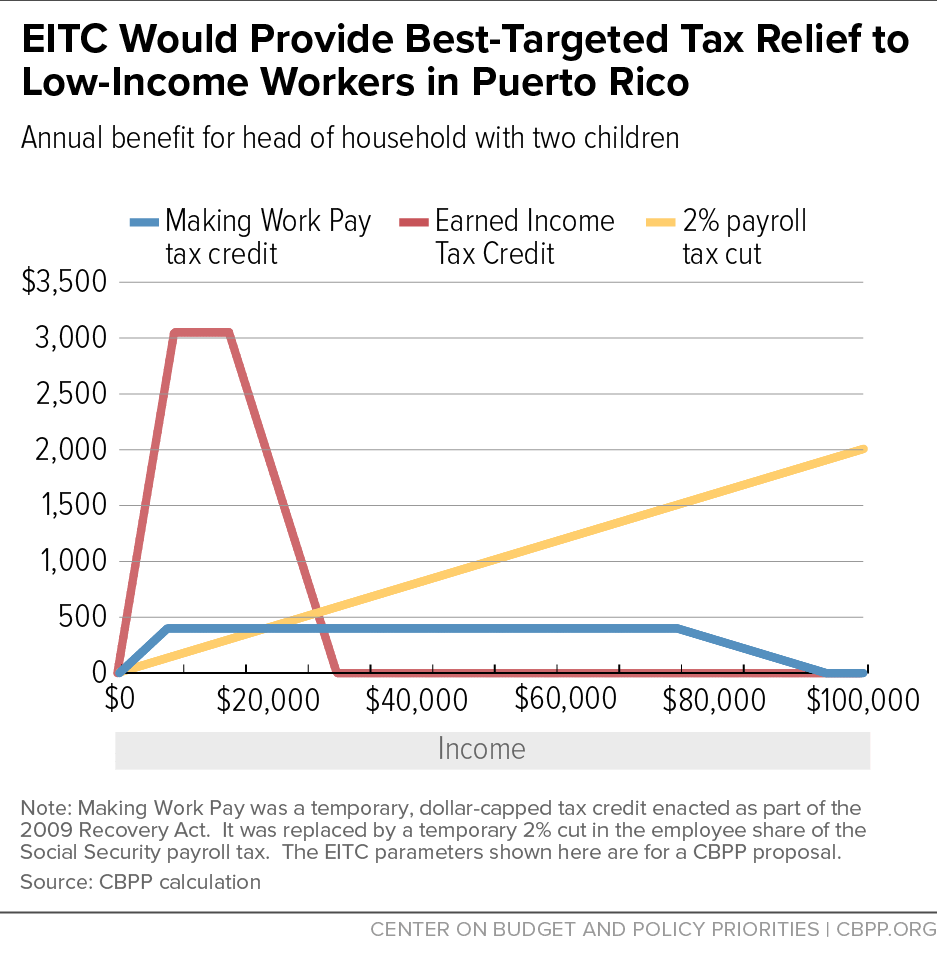

The EITC is now available to low- and moderate-income working families in the 50 states and the District of Columbia. Creating a separate EITC for workers in Puerto Rico would be an effective way to boost labor force participation and reward work. Creating a separate EITC for workers in Puerto Rico would be a more effective way to boost labor force participation and reward the work of low-income families than alternative forms of tax relief that have been proposed. (These alternatives include a tax credit similar to the 2009 Recovery Act’s Making Work Pay credit, which equaled 6.2 percent of wages up to $400 for singles and $800 for couples, and a temporary cut in the employee share of the Social Security payroll tax from 6.2 percent of earnings to 4.2 percent.) An EITC also would boost consumer demand in Puerto Rico more effectively than those alternatives.

EITC Proven Successful at Raising Labor Force Participation

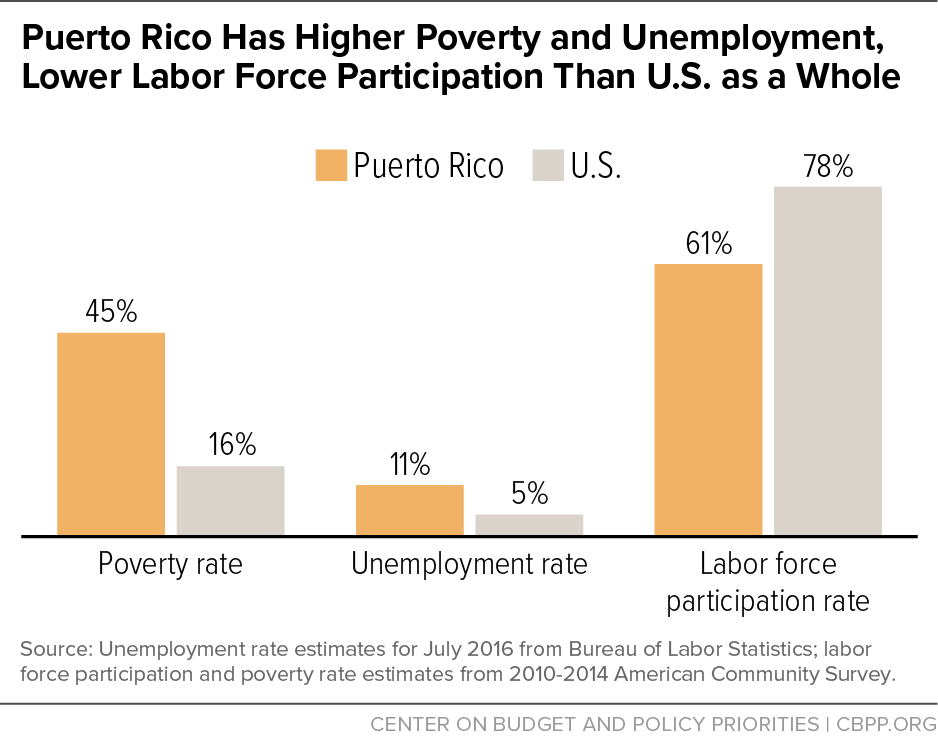

Puerto Rico has high poverty and unemployment and especially low labor force participation — lower than any state’s. Just 61 percent of Puerto Ricans aged 25-64 are working or looking for work in the regular economy, according to Census data for 2010-2014, well below the 78 percent rate for the United States (see Figure 1). A big reason is that many Puerto Ricans work in the informal economy. This also adds to Puerto Rico’s fiscal problems by keeping much of its economic activity outside the tax system. A key goal of a Puerto Rico tax credit should thus be to draw workers into the formal labor force.

An EITC is tailor-made to address this issue. Workers receive the credit starting with their first dollar of earnings, and the credit rises with each added dollar of earnings until reaching its maximum level. Research shows the EITC has powerful effects in inducing people to go to work and drawing them into the regular economy. The EITC expansions in the 1990s were the single largest factor behind the impressive increase in employment among single mothers in that decade — larger, in fact, than the employment gains attributed to the 1996 welfare law — a leading study found.[1]

Consider, for example, a low-income worker in Puerto Rico’s informal economy. Even with a payroll tax cut, he could end up with less after-tax income by joining the formal economy because the tax cut would offset only part of the payroll taxes he would now owe; the employee share of the combined Social Security and Medicare payroll tax equals 7.65 percent of wages. With an EITC, in contrast, the worker likely would end up with more after-tax income by joining the formal economy because his EITC would exceed his payroll taxes.

To ensure that workers end up better off by joining the formal economy, the EITC should phase in at a rate higher than the payroll tax rate. Indeed, the phase-in rate is the most important parameter of the proposal. The higher the phase-in rate, the greater the pro-work effect and the stronger the pull to the formal economy, where workers begin paying taxes. Also, the higher the phase-in rate, the bigger the boost for the Puerto Rican economy per dollar of federal cost, because the lowest-income workers spend rather than save a larger share of their incomes than better-off workers.

Another advantage of an EITC is that it adjusts for family income and number of children, while a payroll tax cut or Making Work Pay tax credit does not. Moreover, for any given cost, an EITC would be much more effectively targeted on families and workers in need. And, because lower-income people tend to spend most of their tax-credit benefits, an EITC would inject more demand into the Puerto Rican economy per dollar of cost.

Figure 2 shows how three alternatives — a Puerto Rican EITC, a Making Work Pay-type tax credit, and a payroll tax rate cut — would affect people in Puerto Rico at different earnings levels. The island’s many low-income workers would get little from a payroll tax rate cut. And, per dollar of cost, a payroll tax cut would do the least to boost labor-force participation and increase consumer spending.

For all these reasons, an EITC should be part of any economic growth package for Puerto Rico.

End Notes

[1] Jeffrey Grogger, “The Effects of Time Limits, the EITC, and Other Policy Changes on Welfare Use, Work, and Income among Female-Head Families,” Review of Economics and Statistics, May 2003; Jeffrey Grogger, “Welfare Transitions in the 1990s: the Economy, Welfare Policy, and the EITC,” NBER Working Paper No. 9472, January 2003, http://www.nber.org/papers/w9472.pdf.

More from the Authors