Estate Tax "Compromise" With 15 Percent Rate Is Little Different Than Permanent Repeal

The Senate is expected to vote on estate tax repeal in June of this year. Permanent repeal of the estate tax would cost nearly $1 trillion between 2012 and 2021, the first ten year period in which its costs would be fully felt. (This cost includes $776 billion in revenue loss and $213 billion in higher interest payments on the federal debt.[1])

In a recent speech to repeal supporters, Senator Kyl (R-AZ), himself a staunch advocate of repeal, acknowledged that “we do not have the votes” in the Senate to make repeal permanent and emphasized that their “position is eroding.”[2] Senator Kyl has also stressed, however, that “certain types of compromises would be almost as good as full repeal.”[3] This is certainly true in the case of his proposal, which would set the estate tax exemption at $5 million for an individual ($10 million for a couple) and the top estate tax rate at 15 percent, the current rate on capital gains income. Such an approach would generate so little revenue, and provide such large tax cuts to the wealthiest estates, that in practical terms it would differ little from permanent repeal.

Estate-tax opponents such as Senator Kyl are pushing to “lock in” a substantial reduction of the estate tax now due to their fear that Congress will become less willing to forgo estate tax revenue in coming years, as the large fiscal challenges posed by the baby boomers’ retirement grow closer. But these concerns are the exact reason their so-called “compromise” proposals should be resisted. Only reasonable reforms that protect needed revenues deserve support.

Reducing the top rate to 15 percent would lose nearly as much revenue as full repeal.

-

A tax that combined a 15 percent rate and an exemption level of $5 million ($10 million for married couples) would lose 84 percent of the revenue lost by full repeal, according to estimates by the Joint Committee on Taxation. At a higher exemption level, even more revenues would be lost.

-

In contrast, retaining the tax as it will exist in 2009 under current law, with a 45 percent rate and a $3.5 million exemption level ($7 million for married couples) would lose only 40 percent of the revenue lost by full repeal, according to the Joint Tax Committee.

-

Moreover, only 0.3 percent of all the persons who are expected to die in 2011 would face any estate tax if the tax were retained at its 2009 level (based on estimates by the Urban Institute-Brookings Institution Tax Policy Center). In other words, the estates of 997 of any 1,000 people who die would be totally exempt. Only the very largest estates would still be subject to the tax.

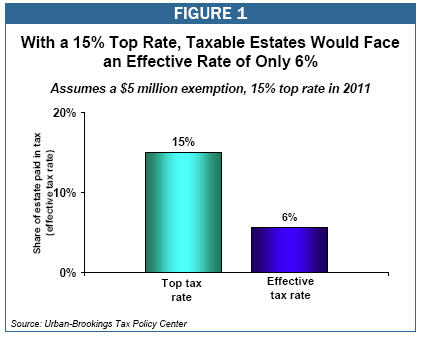

Reducing the top rate to 15 percent would produce an effective rate of just 6 percent.

-

The “effective” tax rate for estates subject to estate taxes — i.e., the share of the estate that would actually be paid in taxes — is well below the top tax rate. A key reason for this is that estate taxes are due only on the portion of an estate’s value that exceeds the exempted amount. Under a $2 million exemption, for example, an estate worth $3 million would owe taxes on a maximum of $1 million. Also, taxpayers can shield a large portion of the estate’s remaining value from taxation by taking allowable deductions for estate taxes paid to states and for charitable bequests, and by using estate planning strategies.

-

In 2004, the most recent year for which data from the Internal Revenue Service are available, taxable estates faced an average effective tax rate of only 20 percent, even though these estates faced a top rate of 49 percent.[4]

-

The Tax Policy Center estimates that if the top rate were reduced to 15 percent (and the exemption were set at $5 million, as called for by Senator Kyl), the average effective tax rate for taxable estates would fall to 6 percent, far lower than the capital gains rate and far less than workers typically pay in income and payroll taxes.

-

In contrast, if the top rate were kept at 45 percent and the exemption were set at $3.5 million — the parameters in 2009 under current law — taxable estates in 2011 would face an average effective rate of 17 percent, or close to the capital gains rate.

Reducing the top rate to 15 percent would provide a tax windfall to extremely large estates.

-

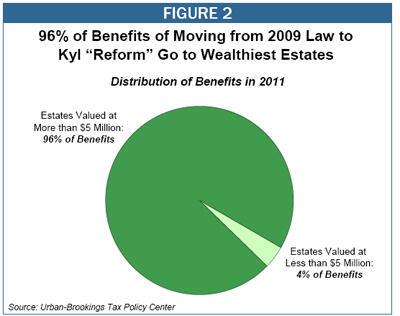

Reducing the top rate to 15 percent — the central element of the Kyl proposal — is the main source of the proposal’s massive revenue losses; it accounts for 90 percent of the cost of moving from making permanent the 2009 law ($3.5 million exemption and 45 percent rate) to the Kyl proposal ($5 million exemption and 15 percent rate).

-

Lowering the tax rate does not exempt more estates from tax, and the benefits from a rate reduction go primarily to those paying the most in estate taxes — that is, the very wealthiest.

-

Only 4 percent of the cost of moving from the 2009 law to the Kyl proposal would be directed towards tax relief for estates valued at less than $5 million. Instead, 96 percent of the benefits would go to estates larger than $5 million, and 76 percent to estates valued at more than $10 million.

Reducing the top rate to 15 percent would largely eliminate an important incentive for charitable giving.

-

The Congressional Budget Office and other researchers have found that the estate tax encourages wealthy individuals to donate more to charity, since these donations reduce estate tax liability. CBO found that if there had been no estate tax in 2000, charitable donations would have been $13 billion to $25 billion lower than they actually were that year. That’s more than the total corporate donations in 2000, which totaled $11 billion, and nearly as much as total foundation contributions. (Foundations contributed $25 billion to charitable causes in 2000.) The CBO analysis also suggests that retaining an estate tax similar in nature to the estate tax that will be in effect in 2008 or 2009 would have a much more modest effect in reducing charitable giving.

-

Lowering the top estate tax rate to 15 percent, however, would sharply reduce donations and have a pronounced negative impact on charities. This is because the incentive to make charitable donations is highly sensitive to the tax rate.

End Notes

[1] The Joint Committee on Taxation estimates that making permanent the repeal of the estate tax would reduce revenues by $369 billion between 2007 and 2016. But that estimate covers only five years of the cost of extending repeal and so understates its true cost.

[2] Susan Cornwell, “Republican Says Compromise Likely on Estate Tax,” Reuters, May 2, 2006.

[3] Martin Vaughan, “Kyl Continuing His Push for Permanent Deal on the Estate Tax,” National Journal’s Congress Daily, January 18, 2006.

[4] The IRS data are for estate taxes paid in 2004, but most of the estates paying tax in 2004 were subject to 2003 estate tax law (with a $1 million exemption and a 49 percent top rate) because estates have nine months to pay their estate tax.

More from the Authors