Deficits Frame Coming Debate on Estate Tax

Later this summer, the Senate is expected to vote on the fate of the estate tax. While this will not be the first time that lawmakers have expressed their views on whether the tax should be repealed, the upcoming vote will occur in a sharply different fiscal context than earlier votes. As Senator Ron Wyden (D-Ore.), who has voted to repeal the estate tax in the past, recently noted, “The deficit picture is different today and the choices are pretty darn hard.”[1]

The deficits that dominate the current fiscal outlook stand in stark contrast to the surpluses that were forecast when past votes on estate tax repeal were taken. In addition, Congress will be facing votes this summer and fall on measures to institute cuts in a range of domestic programs. The trade-offs associated with repealing or dramatically curtailing the estate tax are becoming more evident than they were in the recent past.

- The Senate voted on legislation to repeal the estate tax every year from 1999 through 2002. At the time of each of those votes, the Congressional Budget Office was projecting sizeable surpluses over the coming ten-year budget period. The current fiscal picture is very different. CBO now forecasts large deficits over the next 10 years and beyond.

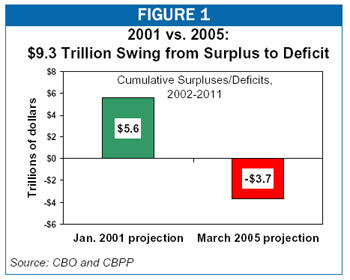

- It is particularly telling to compare the present outlook with the outlook at the time that Congress debated the 2001 tax-cut package, which included the measure that repeals the estate tax in 2010. In 2001, CBO was projecting a surplus of $5.6 trillion over the 2002-2011 period. Today, deficits of $3.7 trillion are projected over that period. [2]

- In addition, this year’s Congressional budget resolution requires reductions in entitlement programs for the first time since 1997. The budget resolution also calls for substantial cuts in non-defense discretionary programs; under the budget resolution, reductions of $158 billion over the next five years are to be made in non-defense discretionary programs. As a result, the votes this summer on proposals to permanently repeal or dramatically shrink the estate tax — which would benefit only the top one to two percent of households — will occur in close proximity to votes on measures to begin cutting various domestic programs, including programs serving the neediest Americans.

- The coming estate tax vote also differs from earlier votes in that it is occurring amidst a debate on how to restore long-term solvency to Social Security. Eliminating or dramatically shrinking the estate tax would take “off the table” a source of revenue that could be used to help close the Social Security shortfall. Some Social Security proposals, such as a plan developed by former Social Security Commissioner Robert Ball, would help restore solvency by maintaining a moderate-size estate tax and dedicating the revenues it collects to Social Security. (The Ball plan combines this measure with changes in Social Security benefits and taxes.) Eliminating most or all of the estate tax would eliminate this option, however, and thereby increase the depth of the Social Security benefit cuts or payroll tax increases that ultimately will be needed to restore solvency.

Estate Tax Repeal Votes and the Fiscal Outlook

The Senate has voted on legislation to repeal the estate tax four times — as a component of comprehensive tax packages in 1999 and 2001, and as a stand-alone bill or amendment in 2000 and 2002. Table 1 shows the ten-year budget outlook projected by CBO at the time of each of those votes. As the table indicates, CBO projected ten-year surpluses each of these times that the Senate voted on the estate tax. [3] This made it easier to argue that the cost of repealing the estate tax was affordable, or at least that cost issues were a secondary concern.

| Table 1: | |

| Year | 10-Year Surplus/Deficit |

| 1999 | $2.9 |

| 2000 | 3.2 |

| 2001 | 5.6 |

| 2002 | 2.3 |

| Source: CBO | |

Now the fiscal outlook is far harsher. In its most recent budget projection, CBO forecast deficits totaling nearly $1 trillion over the next ten years under current policies. Moreover, this projection is universally regarded by budget analysts as a large understatement of the deficit, since it is based on the assumptions that all of the tax cuts enacted in 2001 and 2003 will be allowed to expire after 2010, that the Alternative Minimum Tax will be allowed to explode into the middle class, and that no funding would be provided for operations in Iraq or Afghanistan in 2005 or any subsequent year. If the tax cuts enacted in 2001 and 2003 are extended and relief from the Alternative Minimum Tax is continued, the deficits projected for the period 2006 through 2015 swell to $3.5 trillion.[4] Even this figure is likely to be too optimistic, because it assumes no funding for Iraq and Afghanistan after this year. When estimates of ongoing costs in Iraq and Afghanistan are added in (assuming that these costs phase out over several years), the projected deficit increases to $4.1 trillion over the ten-year period. (As noted earlier, the deficit over the period 2002-2011 is $3.7 trillion when these more realistic assumptions are applied.) It may be noted that Goldman Sachs projects the deficit over the next ten years to be even higher — $4.8 trillion. [5] Given the likelihood of these very large deficits — and even larger deficits in subsequent decades — the fiscal context in which the coming Senate debate on the estate tax will occur is sharply different from the context for previous debates. The looming deficits call into serious question the affordability of estate tax options that would result in massive revenue losses.

2006 Budget Resolution Calls for Cuts in Domestic Programs

The fiscal challenges the nation faces are now beginning to force difficult choices. In February, the Administration released what it called a “lean budget,” and Congress followed suit in April, passing a budget resolution that calls for significant cuts in domestic programs in coming years. Under the budget resolution, cuts in entitlement spending are mandated for the first time since 1997. This will be the first time that entitlement cuts coincide with a vote on estate tax repeal.

In addition, the budget resolution sets 2006 funding levels that require discretionary appropriations for fiscal year 2006, outside of defense and international affairs, to be cut by $13 billion below last year’s levels adjusted for inflation. [6] Indeed, to meet this target, House-passed appropriations bills for 2006 have included some sizeable program cuts. For instance, the bills cut funding for education programs for low-income children by $351 million and the Community Service Block Grant by $327 million. In addition, the bills include substantial funding reductions in the Low Income Home Energy Assistance Program ($232 million), Job Corps and other job training programs ($304 million), state grants that help enforce the Clean Air and Clean Water Acts ($503 million), federal assistance for local law enforcement ($323 million), and the child care block grant ($33 million). [7]

This would only be the beginning of what would become steadily larger cuts over time in domestic discretionary programs. The budget resolution calls for cuts in these programs of $158 billion over five years, with the cuts reaching $48 billion in 2010.

Estate Tax Revenues Could Be Used to Address Social Security Shortfall

Most current proposals to restore long-term Social Security solvency include substantial reductions in Social Security benefits for future retirees. An alternative that would moderate the depth of the benefit cuts or payroll tax increases that otherwise will be needed to restore solvency would retain a meaningful (although relatively modest) estate tax and dedicate the revenues from it to the Social Security Trust Fund.

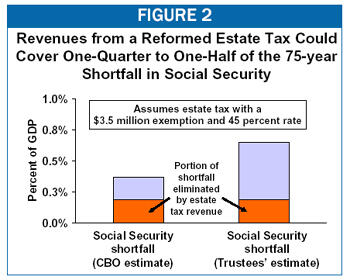

For instance, Robert Ball, who served as Social Security Commissioner under Presidents Kennedy, Johnson, and Nixon, has proposed maintaining the estate tax at its 2009 level — with $3.5 million exemption per individual ($7 million per couple) and a 45 percent top rate — and dedicating the revenues to Social Security. Under this approach, the estates of only three one-thousands of all people who die would owe any estate tax at all. Yet according to the Social Security actuaries, this would raise enough revenue to close more than one-quarter of the Social Security shortfall over the next 75 years. (Under CBO’s projections of the Social Security shortfall, this proposal would close about half of the shortfall.)

Dedicating estate tax revenues to the Social Security trust fund is just one example of how the estate tax can serve as a substantial and important source of revenue. This revenue could also be used to reduce the deficit or to address other critical national needs. In any event, the upcoming vote on estate tax repeal will occur at a time when tradeoffs such as these can no longer be ignored.

End Notes

[1] Dustin Stamper, “Frist Files Estate Tax Amendment, But Repeal Will Hinge on Compromise,” Tax Notes, June 23, 2005.

[2] This figure includes extension of the tax cuts that were passed in 2001 and 2003, including relief from the Alternative Minimum Tax, and the normal “tax extenders” such as the research and experimentation tax credit. It also contains funding for military operations in Iraq and Afghanistan. These assumptions are discussed in further detail below.

[3] Analyses at the time of the 2002 budget outlook indicated that CBO potentially was being overly optimistic in projecting a long-term surplus. See, for example, Richard Kogan, Robert Greenstein, and Joel Friedman, “The New CBO Projections: What Do They Tell Us?” Center on Budget and Policy Priorities, January 29, 2002.

[4] This figure is CBO’s estimate of the President’s budget, which includes extension of estate tax repeal.

[5] Goldman Sachs, “Deficit Reduction: Don’t Pass Up This Investment!” June 10, 2005.

[6] Previous CBPP analyses on the Congressional budget resolution have measured cuts against the official CBO baseline, which includes emergency funding; the estimates used in this paper adjust the CBO baseline to take out the continuation of emergency funding, and thus show somewhat lower reductions.

[7] All of the cuts discussed in this section are relative to last year’s levels, adjusted for inflation. All of the programs mentioned are being cut in nominal terms as well.