A Tough Recovery By Any Measure: New Data Show Consumer Expenditures Lag for Low- and Middle-Income Families

Overview

Data on wages, compensation and income paint a disappointing picture of the current economic expansion, especially from the perspective of low- and middle income families. By most measures, real incomes were lower in 2005 than in the recession year of 2001, and real wages, after rising through mid-2003, fell consistently until very recently.

These unfortunate trends have occurred amid strong productivity growth, which implies that wage and income inequality — and in particular, the gaps between what high-income Americans are receiving and what other Americans are getting — has grown. Recently released Census data show that the top fifth of households received 50.4 percent of the nation’s income in 2005, equal to the highest share on record.[1]

Aparna Mathur and Kevin Hassett of the American Enterprise Institute argue in a recent paper that data on consumer spending tell a different — and much rosier — story. They contend that consumer spending data show a rising standard of living for all Americans and a reduction in inequality.[2] Unfortunately, their findings rest on a mistaken use of data on consumer expenditures. (See the box below for an explanation of the flaws in the AEI analysis.)

Measured correctly, the consumer expenditure data are consistent with the basic story that the income and wage data tell. The consumer spending data show that disparities in consumption expenditures between high-income households and other Americans are widening and that many Americans are treading water or falling further behind.

Indeed, the data on consumer spending — including newly released data for 2005 — add an important element to the story. They show that while households in all income categories saw their average before-tax incomes decline between 2000 and 2005 in inflation-adjusted terms, high-income families were able to increase their consumption levels through a combination of generous tax cuts, borrowing, and drawing down (or reducing) saving. In contrast, low-income families have not been able to weather the storm and have had to cut back on their expenditures, with little help from their modest tax cuts and with little recourse to borrowing. The evidence indicates that for middle-class families, consumer spending is roughly unchanged from its level in 2000 (or 2001).

Specifically, the consumer expenditure data show the following:

- From 2000 (the year of the previous business-cycle peak) to 2005, consumer expenditures grew more quickly among high-income households than among middle-income households — for which consumer spending has slowed dramatically — and declined among low-income households. As a result, the already large inequality that marks consumer spending increased further.[3] Moreover, the increase between 2000 and 2005 in the percentage of consumer expenditures that are made by the top fifth of households was the largest five-year increase since these data began being collected in 1984.[4] The percentage of consumer expenditures made by the bottom 20 percent of households and the percentage of expenditures made by the bottom 80 percent of households both declined.

- The disparities in consumer expenditures among households at different income levels were greater in 2005 than in any year on record (again, the data go back to 1984). The top fifth of households made 39 percent of all consumer expenditures in 2005. This was the highest share on record. The bottom fifth was responsible for 8.2 percent of the expenditures, tied with 2004 for the lowest share on record.

- Consumer expenditures by low-income households are down over this expansion, while expenditures by high-income households remain high. By any measure, consumer spending by low-income households is down substantially since 2001, even though the economy has grown, while consumer spending by higher-income households remains robust. High-income households appear to have been able to use tax cuts, a portion of their savings and additional borrowing to finance strong consumption.

- Consumer spending by the middle class has grown more slowly in the current economic expansion than in previous years and may even have declined. Some consumer expenditure data show a decline between 2000 (or 2001) and 2005 in consumer spending by the middle class, while other data show an increase. But all of these data show that during the current recovery, the growth in consumer spending by the middle class has been substantially weaker than historical norms. During the current recovery, middle-class consumption has grown significantly more slowly than consumption by high-income households (if it grew at all among middle-class households — the data are unclear on this point).

- Tax cuts have boosted consumption by the top quintile while doing virtually nothing for the bottom quintile. Tax cuts can result in an increase in household consumption even as pre-tax incomes fall. Since 2000, however, the tax cuts have provided much more help to high-income families than to low-income families. Analysis by the Urban Institute-Brookings Institution Tax Policy Center shows that households in the bottom income quintile received an average tax cut of $18 in 2005, which was enough to boost their annual consumption growth rate from 2000 to 2005 by only 0.01 percentage point. In contrast, families in the top quintile received an average tax cut of $4,845, enough to add 0.69 percentage points to their annual consumption growth rate and to help prevent their standard of living from declining despite a drop in their average pre-tax income.[5]

The consumption statistics do not paint a complete picture of how the economy is doing for American families. Total consumption has been boosted in recent years by a decline in savings rates, substantial borrowing by households (including home equity withdrawals), and tax cuts that have been financed by increased federal borrowing. The personal savings rate in 2005 was -0.4 percent, the first time that it has been negative since the 1930s, as consumers effectively consumed the rise in the value of some of their assets while also borrowing heavily to offset such developments as declining real median income for non-elderly households. Future consumption is likely to be reduced as a consequence, as debts are repaid and savings return to a more normal level.

Similarly, the tax cuts have provided a temporary boost to consumption but have been financed by substantial federal borrowing. When the tax cuts eventually are paid for, as they ultimately must be (most likely in large part through a combination of higher taxes and reductions in benefits for programs such as Social Security and Medicare), the result here, too, will be lower future consumption. And to the degree that Social Security, Medicare or other government spending is reduced, the adjustments made in the future to cover the costs of the tax cuts are likely to fall disproportionately on low- and moderate-income households.

In sum, the American economy has been spending well beyond its means, borrowing more than $2 billion a day from abroad, an amount equivalent to more than 6 percent of the Gross Domestic Product. Yet even this level of borrowing has not been enough to prop up standards of living (as reflected in consumption levels) for low-income and middle-income families.

The Advantages and Pitfalls of Analyzing Consumer Expenditures

In some respects, consumption is a more accurate measure of a person’s lifetime income than annual income is. Some college students or senior citizens, for example, may have low current incomes but be spending substantial amounts based on their expected or actual higher lifetime incomes. Similarly, a person who experiences a transitory shock to his or her income may be able to “smooth” his or her consumption by borrowing or drawing down savings.

In addition, consumption spending reflects the effects of tax cuts and tax increases, which are not included in the standard income and wage statistics, since those statistics typically reflect income and wages before taxes. Consumption statistics also pick up the effects of some forms of compensation and government transfers — like employer contributions to health insurance premiums or government programs like Medicare and Medicaid — that generally are not reflected in the standard income and wage data.

Consumption data, however, suffer from limitations of their own because they may reflect temporary factors that are not sustainable over the long run. The amount by which annual incomes rise or fall provides the best measure of the change in a person’s lifetime consumption possibilities.[6] If a person earns $50,000 in a year, he or she can spend $50,000 (in present value) over the course of his or her life. If the person’s income falls to $40,000 (and stays there), his or her lifetime consumption possibilities also decline, even if the person’s consumption does not immediately fall by the full $10,000 because he or she initially borrows or draws down savings to make up the difference. This type of “temporary financing” has been widespread in recent years, masking the long-term impact of stagnant or declining real incomes on people’s standards of living. Few analysts believe that the current negative personal savings rate in the United States can persist over time.

What the Consumer Expenditure Survey Data Show

The Bureau of Labor Statistics surveys 15,000 households per quarter on consumer expenditures. Data from the survey are available for 1984 through 2005. The following are among the findings that emerge from the Consumer Expenditure Survey.

Consumption Inequality Has Increased

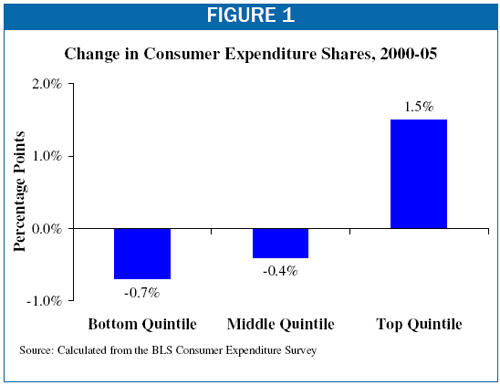

From 2000 to 2005, the share of consumer expenditures made by the 20 percent of households with the highest pre-tax incomes rose by 1.5 percentage points, from 37.5 percent of all consumer expenditures to 39.0 percent of those expenditures. This is the largest five-year rise on record since these data began to be collected in 1984. Correspondingly, the share of consumption for which the bottom 80 percent of households is responsible fell by a larger amount than over any other five-year period. Figure 1 shows the changes in consumption shares between 2000 and 2005.

These developments contrast with what occurred during the comparable phase of the previous economic recovery from 1991 to 1994. In that period, the consumption shares of the various income groups remained relatively stable.

Problems with the Mathur-Hassett Estimates of Consumption

Recently, AEI economists Aparna Mathur and Kevin Hassett have argued that “When you look at the most accurate measures of how the middle class is doing, the answer is that things that are good, maybe even terrific… The middle class is even doing better than the upper crust.” They base this claim on an analysis of consumption data by income quintile (or income fifth). Unfortunately, their analysis is marred by a number of shortcomings, including the following:

- Use of the wrong starting date. The Mathur-Hassett article asks, “So are we better off today than we were in 2001?” Their article then shifts to discussing consumption growth “between 2000 and 2005.” But its key findings are based on consumption growthfrom 1999 to 2005. These data do not answer the question that Hassett-Mathur pose and do not coincide with the current economic recovery, which started in 2001. These data are of little value in determining what has happened to consumption during the current recovery. In contrast, the analysis in this paper compares consumption in 2005 to consumption both in 2000 (the peak year of the previous business cycle) and in 2001 (the recession year). (Both of these comparisons yield similar results.) Moreover, the analysis in this paper uses 1984 to 2000 as a control to establish how recent performance differs from historical performance.

- Use of an inaccurate projection for 2005 that mistakenly assumed no increase in consumption inequality. Mathur and Hassett released their analysis before the BLS released its data on consumption by quintile for 2005. As they explain in an appendix to their paper, “shares in 2005 are artificially replicated to be equal to 2004 BLS shares.” The subsequent release of the BLS data for 2005 shows, however, that this assumption was inappropriate, since the share of consumption made by the top quintile jumped again in 2005, while the share of consumption made by the middle quintile fell. As a result, even using the Mathur-Hassett measure and comparing consumption in 1999 to consumption in 2005, their statement that “the middle class is even doing better than the upper crust” now is seen to be incorrect.

- Mathur and Hassett do not discuss potential biases and shortcomings in the measure they employ. Mathur and Hassett use a hybrid measure of consumption that is based on their own combination of consumer expenditure shares from the Consumer Expenditure Survey data and aggregate consumption data from the GDP statistics. This method mixes two data sets that: a) are quite different from each other in terms of which consumption expenditures they include; and b) also differ significantly in terms of how much consumption they capture (even when they are adjusted to be comparable), a difference that has been growing over time.

For example, a study by Garner et al* shows that the ratio of expenditures in the CE to expenditures in the PCE fell from 67 percent in 1992 to 60 percent in 2002. To the extent that this growing difference is attributable to expenditures made by a particular income class, the hybrid measure will reflect a growing bias. If, for example, expenditures by high-income families are increasingly missing from the CE but are present in the PCE, then the Mathur-Hassett hybrid measure will understate the growth in the share of expenditures that the top fifth makes. In fact, some expenditure categories shown in Garner et al, Table C-1, reflect such a bias: the CE/PCE ratios are found to have fallen at a faster-than-average rate for entertainment, food away from home, and vehicle purchases — all of which constitute expenditures made disproportionately by higher-income households — but to have fallen at a slower-than-average rate for purchases of food at home and public transportation, which are made disproportionately by people in the middle and bottom of the income spectrum.

* Garner, Janini, Passero, Paszkiewicz, Vendemia. The CE and the PCE: a Comparison. Monthly Labor Review, September 2006.

Consumption Inequality Was the Highest Ever Recorded in 2005

As noted, in 2005, the top fifth of households made 39.0 percent of all consumption expenditures, which was the highest share on record. By contrast, the bottom fifth of households was responsible for 8.2 percent of consumption, tied with 2004 for the lowest share on record.[7] Note that because of consumption “smoothing” — i.e., the tendency of families to use borrowing and savings to smooth out consumption as incomes rise and fall over a lifetime — consumption in any year is less unequal than income in that year.[8]

As with income equality, consumption inequality — the gap between the share of consumer expenditures made by higher-income households and the share made by lower-income households — is growing as well. This finding is consistent with the findings of a number of academic studies.[9]

Middle-Class Consumption Growth Has Been Weak In This Expansion

Growth in consumption by middle-class households has been weak in the current economic expansion. It is difficult to use existing data to measure precisely the changes that have occurred in consumption by households at different income levels. The Consumer Expenditure Survey data indicate that consumer expenditures declined slightly between 2000 and 2005 for the 20 percent of households exactly in the middle of the income spectrum. (These expenditures declined at an average rate of 0.1 percent per year). That stands in contrast to the 1.2 percent average annual growth in consumption by these households under data from the same survey for the years from 1984 to 2000.[10] (See Table 1.)

As noted above, the Consumer Expenditure Survey data report less consumption than the PCE data, and the magnitude of the understatement appears to have increased over time. As a result, estimates of consumption growth based on the Consumer Expenditure Survey may be too low.

Table 1 presents two alternative, “hybrid” measures similar to the measure that the AEI paper features. These measures apply the consumption shares from the Consumer Expenditure Survey to the level of aggregate consumption expenditures estimated by the Bureau of Economic Analysis.[11] The first hybrid measure shows consumption growth per “consumer unit”[12] and is more comparable to the other measures we are using, while the second hybrid measure shows consumption growth per capita, the measure used in the AEI study.

| TABLE 1: | ||||

| 2000 – 2005 | 2001 – 2005 | 1984 – 2000 | Change in growth rate 2000-05 vs. 1984-2000 | |

| Consumer Expenditures (CE Measure, Per Consumer Unit) | ||||

| Bottom Quintile | -1.2% | -2.1% | 0.3% | -1.5 percentage points |

| Middle Quintile | -0.1% | -0.1% | 0.8% | -0.9 percentage points |

| Top Quintile | 1.2% | 1.6% | 0.8% | 0.4 percentage points |

| Consumer Expenditures (Hybrid Measure, Per Consumer Unit) | ||||

| Bottom Quintile | -0.4% | -1.2% | 1.7% | -2.0 percentage points |

| Middle Quintile | 0.8% | 0.8% | 2.1% | -1.3 percentage points |

| Top Quintile | 2.1% | 2.5% | 2.2% | -0.1 percentage points |

| Consumer Expenditures (Hybrid Measure, Per Capita) | ||||

| Bottom Quintile | 0.1% | -0.7% | 1.7% | -1.7 percentage points |

| Middle Quintile | 1.3% | 1.4% | 2.2% | -1.0 percentage points |

| Top Quintile | 2.5% | 3.0% | 2.3% | 0.2 percentage points |

| Money Income (Per Household) | ||||

| Bottom Quintile | -1.5% | -1.2% | 1.1% | -2.6 percentage points |

| Middle Quintile | -0.7% | -0.4% | 1.1% | -1.8 percentage points |

| Top Quintile | -0.2% | -0.2% | 2.4% | -2.6 percentage points |

| Source: Consumer Expenditures are taken directly from the BLS’s Consumer Expenditure Survey, adjusted for inflation using the CPI-U-RS. The hybrid measures apply the Consumer Expenditure Survey’s consumption shares to the BEA’s aggregate real personal consumption expenditures measure. Money income is taken from the Census Bureau’s Current Population Survey data on household income by income quintile. | ||||

Although these hybrid measures correct the underreporting problems of the pure Consumer Expenditure Survey measure, they introduce problems of their own. First, the definitions of consumption in the two data series that are used to construct the hybrid measures differ from each other in important ways, which is why no government agency produces hybrid statistics of this nature. Second, these estimates are sensitive to changes in underreporting of consumption by income. It appears that at least from 1984 through 2000, underreporting by high-income families grew, biasing the hybrid measure toward showing too much relative consumption growth for lower-income families and too little relative consumption growth for high-income families.[13]

Even with their shortcomings, however, the hybrid measures tell a similar story to the other consumption measure: from 2000 to 2005, consumption rose at a much slower average annual rate for the middle quintile than for the top quintile and fell for the bottom quintile. Moreover, annual consumption growth was much slower in the 2000-2005 period for the bottom and middle quintiles than it had been in the 1984-2004 period, but was just as rapid for the top quintile as in the 1984-2004 period.

For example, under the hybrid measure that tracks consumption by consumer units, spending by the middle quintile rose at an average annual rate of 0.8 percent between 2000 and 2005, substantially below the 2.1 percent average growth rate over this period for the top quintile and also well below the average growth rate in consumer spending by the middle quintile over the 1984-2000 period.

Low- and Moderate-Income Families Have Had the Hardest Time Coping with Falling Incomes

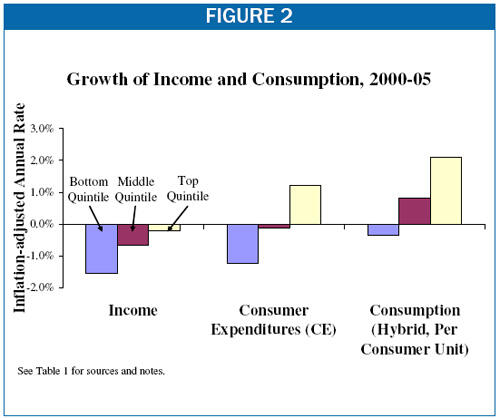

Figure 2 indicates that average real incomes for low-, middle-, and high-income households all fell between 2000 and 2005 (although the top quintile experienced the smallest decline, which is consistent with rising inequality). But poor households had to reduce their standard of living more than the other income groups did. The middle-class had to make a smaller adjustment, and households in the top income fifth were able to continue increasing their consumer spending.

As shown in the last column of Table 1, all three of the consumption measures essentially tell the same story: the lowest quintile has had to cut back its rate of consumption growth quite substantially, relative to the 1984-2000 period, and the middle quintile as well has experienced a sizeable reduction in its rate of consumption growth. Yet consumer spending by high-income families has continued to grow at roughly the same average pace as it did in the earlier period.

(Note that these data do not capture the large increases in inequality at the very top end of the income distribution, among the top 1 percent or even the top 0.1 percent of households.[14])

Explaining the Disconnect Between Income Growth and Consumption Growth

Some of the reduction in real incomes from 2000 to 2005 (and from 2001 to 2005) was the result of transitory factors such as the run-up in energy prices. High-income households are the households most able to “smooth” their consumption when faced with temporary declines in income or temporary spikes in energy costs. They can do so by reducing the percentage of income they save, by drawing down savings, or by borrowing against their homes or other assets.

In contrast, even if low-income households expect future increases in their incomes or future declines in energy costs, they are much less likely to be able to maintain their standard of living when faced with reductions in income or hikes in prices for items like energy. This common-sense notion is consistent with a large volume of economic research, which finds that lower-income households are more liquidity constrained (i.e., less able to finance current consumption by drawing down savings or borrowing) and less able to “smooth” their consumption.[15] Middle-class households fall between these two poles.

The tax cuts of recent years constitute another significant factor. The tax cuts have provided much more aid to high-income households than to other households in helping them smooth consumption. As noted above, the tax cuts have been financed by government borrowing that cannot continue indefinitely; eventually, higher taxes, lower government benefits, or lower government spending in other areas will be necessary to offset the costs of the tax cuts. Measures to raise taxes or cut government programs will reduce future consumption. In this way, the tax cuts are like personal borrowing — they boost consumption today at the expense of consumption in the future.

| TABLE 2: | ||

| Average Tax Cut in 2005 | Added Consumption Growth in 2000-05 If All of the Tax Cuts Were Spent (Annual Rate)* | |

| Bottom Quintile | $18 | +0.01% |

| Middle Quintile | $742 | +0.24% |

| Top Quintile | $4,845 | +0.69% |

| *These estimates combine data from the Consumer Expenditure Survey and data from the Urban Institute-Brookings Institution Tax Policy Center. Due to definitional differences, these two sources are not fully comparable. Source: Tax cuts are from Tax Policy Center, T05-0059 - Effect of the 2001-2004 Tax Cuts Without Financing, Distribution of Federal Tax Change by Cash Income Percentiles, 2004, April 4, 2005. Other numbers are the authors’ calculations, based on the Consumer Expenditure Survey and personal consumption expenditures data. Note that “tax cuts” include the refundable portion of tax credits, which are technically scored as an increase in outlays under the budget rules. | ||

The borrowing by the federal government to finance the tax cuts has temporarily boosted consumption the most among high-income households — the households that already are most able to smooth consumption on their own — while doing the least to boost consumption among low-income households. As Table 2 shows, the tax cuts have provided significant support to consumption by high-income households while doing little to raise consumption among those on the lower rings of the income ladder.

When the tax cuts are eventually paid for — as they will have to be — the measures adopted to pay for the tax cuts will reduce consumption. If the tax cuts are paid for by cutting transfers like Social Security and Medicare or most other forms of government spending, the disparities shown in Table 2 will become still larger.[16]

Conclusion

Any way that you slice the data, most American families are failing to benefit much from the current economic expansion. There is legitimate debate about why this is so and what can be done about it. But the facts themselves are beyond dispute, and the consumption data confirm this basic proposition. The consumption data also show that households in the top quintile have been better able to shield themselves from declining average incomes and to maintain their standards of living than low- and middle-income households.

The consumer spending data also illustrate a significant problem with the recent tax cuts. In one sense, the tax cuts enacted since 2001 are essentially temporary because they will have to be financed in the future by tax increases or benefit reductions. Temporary tax cuts can sometimes be justified; for example, such tax cuts can help lift the economy out of a downturn by stimulating aggregate demand.[17] Temporary tax cuts also can help families weather hard times, such as when families experience declines in real incomes and wages as a result of an economic downturn or transitory increases in energy prices. In effect, deficit-financed temporary tax cuts can allow the government to borrow on behalf of people who would not have access to capital markets themselves, in order to achieve the desired amount of consumption-smoothing during hard times.

From this perspective, however, the recent tax cuts have been upside down. They have effectively borrowed from the future to boost consumption today among higher-income families that would be able to borrow on their own anyway, while doing little for low- and moderate-income families.

End Notes

[1] Statistically, this share is not significantly different than the share in recent years.

[2] See Aparna Mathur and Kevin Hassett, “Conspicuous Consumption: How to Measure Economic Well-Being,” National Review, September 25, 2006. Available at: http://www.aei.org/publications/pubID.24942,filter.all/pub_detail.asp.

[3] Note that what we (and AEI) are calling “consumption inequality” differs from the usual concept in that we are looking at changes in the distribution of expenditure shares by income quintile. Typically, consumption inequality would be examined by tracking the changes in expenditure shares by expenditure quintiles. Also, before 2004, expenditure share data are available only for so-called “complete income reporters,” leaving out a significant number of consumer units that failed to report income data. In 2004, the BLS began to impute the missing income data.

[4] The four-year increase (from 2001) and the three-year increase (from 2002 to 2005) also were the largest on record.

[5] Although average income for the top quintile as a whole declined slightly between 2000 and 2005, those at the pinnacle of the top quintile saw their income rise. Census data shows that income for households at the 95th percentile increased between 2000 and 2005.

[6] Technically, income measures should include not just wages and salaries but also accrued capital gains in the form of higher values of stocks, houses and other assets. The standard income statistics only include a portion of capital income and neglect most accrued, and even realized, capital gains.

[7] To reduce measurement error, some analysts average consumption shares over several years. The average share of consumption expenditures made by the top fifth of households over the years from 2003 through 2005 was the largest share recorded for any three-year period, while the average share for the lowest fifth was the lowest on record.

[8] By way of comparison, the bottom fifth of the income distribution received 3.4 percent of the nation’s income in 2005, while the top fifth received 50.4 percent of the income.

[9] E.g., Dirk Krueger and Fabrizio Perri, “Does Income Inequality Lead to Consumption Inequality,” Federal Reserve Bank of Minneapolis Research Department Staff Report 363, June 2005.

[10] Note that we show consumption growth here from 1984 — the earliest period available in the sample — to 2000. Similar results obtain if one examines consumption growth either over the last business cycle (1991 to 2000) or over the comparable phase of the last business cycle (1990 to 1994), as a control.

[11] The BEA estimate is reflected in the personal consumption expenditures component of the BEA’s estimate of the Gross Domestic Product.

[12] “Consumer units” are similar to households.

[13] Table 1 shows that from 1984 to 2000, consumption growth for the middle quintile under the hybrid measure was 1 percentage point per year faster than income growth. For this to have occured, there would need to have been massive levels of borrowing. Although borrowing likely has increased, an increase of this magnitude is implausible. This suggests that the hybrid measures are biased toward showing too much consumption growth among those in the middle of the income spectrum. Conversely, these data show an increase in savings by the top quintile, also a potential artifact of systematic measurement error.

[14] For example, the Census data show that from 2000 to 2005, income for households at the 80th percentile fell, while income for households at the 95th percentile rose. In addition, since 2002 income growth has been particularly strong for high-income households.

[15] E.g., Tullio Jappelli, “Who Is Credit Constrained in the U.S. Economy?” Quarterly Journal of Economics, February, 1990, pp. 219-234.

[16] William G. Gale, Peter R. Orszag, and Isaac Shapiro, “The Ultimate Burden of the Tax Cuts,” Center on Budget and Policy Priorities, June 2, 2004.

[17] Substantial evidence suggests the Bush tax cuts were poorly designed as stimulus, with relatively low “bang-for-the-buck.” See Mark M. Zandi, Assessing President Bush’s Fiscal Policies, Dismal Scientist, July 2004 and Jane G. Gravelle “Economic and Revenue Effects of Permanent and Temporary Capital Gains Tax Cuts” Congressional Research Service updated January 29, 2003.

More from the Authors