2017 Tax Law Weakens Estate Tax, Benefiting Wealthiest and Expanding Avoidance Opportunities

The 2017 tax law doubles the estate tax exemption — the value of estates that is exempt from the estate tax — from $11 million to $22 million per couple.[1] The few estates large enough to remain taxable — fewer than 1 in 1,000 estates nationwide — will receive a tax cut of $4.4 million per couple. The estate tax cut will also create several tax planning opportunities for wealthy Americans and allow them to transfer millions of dollars in additional untaxed wealth to their heirs because the law retains the “stepped-up basis” loophole.

This doubling of the estate tax-free amount is a prime example of the 2017 tax law’s three fundamental flaws: it is heavily tilted toward the wealthy, loses significant revenue, and makes it easier for wealthy people to game the tax system. Policymakers should not only repeal the estate tax cut but also strengthen the estate tax beyond its 2017 rules. At a minimum, they could restore the estate tax to the 2009 rules, when the exemption was about $8.2 million per couple in today’s dollars and the tax rate was 45 percent.

Benefits Only Heirs of the Wealthiest Estates

The 2017 tax law doubles the amount of an estate’s value that’s exempt from the estate tax, from $11 million per couple ($5.5 million per individual) to $22 million per couple ($11 million per person). That will:

-

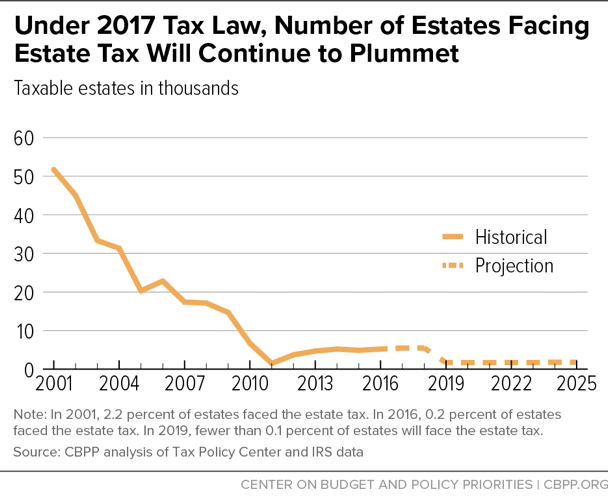

Reduce the share of estates facing the tax to fewer than 1 in 1,000. Even before the tax law was enacted, only the wealthiest 2 in 1,000 estates faced the estate tax. Policymakers have dramatically raised the exemption level in recent decades (from $675,000 per person in 2001), so very few estates are large enough to be taxable. Now only the largest 1,800 estates each year will face the estate tax. (See chart.)

- Give each of the 1,800 very largest estates a tax cut of $4.4 million per couple. Doubling the exemption will eliminate the estate tax for estates worth between $11 million and $22 million per couple, and give the remaining 1,800 estates worth over $22 million per couple a tax cut of $4.4 million (40 percent of the additional $11 million in assets that would be exempt).[2]

The estate tax is the most progressive part of the U.S. tax code because it affects only those who are most able to pay. Large inheritances play a significant role in the concentration of wealth; inheritances account for about 40 percent of all household wealth and are extremely concentrated at the top. Weakening the estate tax, therefore, exacerbates wealth inequality. Proponents of cutting the estate tax argue it will help non-wealthy Americans by increasing growth, but cutting it likely has little or no impact on wealthy donors’ savings and actually discourages wealthy heirs from working. The estate tax is an efficient way to raise revenue without imposing burdens on low- and middle-income Americans.[3]

Loses Much-Needed Revenue, Reflecting Flawed Priorities

The 2017 tax law will cost a total of $1.9 trillion from 2018 to 2027, according to the Congressional Budget Office (CBO). The law could generate additional economic growth to offset a small share of this revenue loss, CBO estimates, but when adding interest costs from the new debt that the law will incur, it will still cost $1.9 trillion. The estate tax cut costs $83 billion over ten years, the Joint Committee on Taxation estimates. Like other elements of the law, it is set to expire after 2025, but Republican lawmakers say they want to make it permanent without offsetting its cost. This would cost about $13 billion in 2026 and 2027 alone.

These large revenue losses are irresponsible given the fiscal challenges the nation will face over the next several decades, such as the aging of the population, health care costs likely continuing to rise faster than the economy, interest rates returning to more normal levels, potential national security threats, and challenges such as large infrastructure needs that cannot be deferred indefinitely. The nature and magnitude of these fiscal pressures will require revenue to rise as a percentage of gross domestic product to prevent an unsustainable rise in the nation’s debt ratio over coming decades.

2017 Tax Law Kept Estate Tax Loophole

Wealthy Americans have only begun to explore the possibilities for gaming of the tax system that the weakening of the estate tax creates. A recent article in Tax Notes, for example, showed how the estate tax cut creates a potential avenue for wealthy Americans to reduce their capital gains taxes.[4]

Perhaps most significantly, the doubling of the estate tax exemption will allow vast sums of untaxed wealth to transfer to heirs. One reason wealth can go untaxed is the “stepped-up basis” loophole, which the 2017 tax law retained. Capital gains tax is due on the appreciation of assets, such as real estate or stock, only when the owner “realizes” the gain (usually by selling the asset). But the loophole allows someone who inherits an asset to not owe taxes on the appreciation of the asset that occurred during the previous owner’s lifetime. Therefore, the increase in the value of an asset is never subject to income tax if the owner holds on to the asset until death — unless they have to pay the estate tax on it.

These unrealized capital gains account for a significant proportion of the assets held by wealthy estates — ranging from 32 percent for estates worth between $5 million and $10 million to as much as 55 percent for estates worth more than $100 million. Combined with retaining step-up basis, the estate tax cut will raise the amount of income wealthy people can pass along tax-free to their heirs. Moreover, the 2017 tax law also retains the ability to exchange similar real estate assets without triggering capital gains tax on the increase in the value of those assets before the exchange.

This problem of untaxed wealth transfers is compounded by the law’s other gaming opportunities and an IRS whose 2018 enforcement funding will be 23 percent below its 2010 levels in inflation-adjusted terms. This invites the wealthy and profitable corporations to push the boundaries of the law in order to extract savings that go beyond the tax law’s large, explicit tax cuts. As one tax lawyer put it, the IRS is unlikely to deal with these loopholes because it will be busy implementing the tax law and it’s unlikely Congress will “go back and tighten up the estate tax, because after all, they wanted to repeal it altogether.”[5]

End Notes

[1] For further information, see Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law is Fundamentally Flawed and Will Require Basic Restructuring,” CBPP, April 9, 2018, https://bit.ly/2HmWnzD.

[2] Chye-Ching Huang, “Weakening the Estate Tax Is a Bad Idea – So Is Repealing It,” CBPP, December 12, 2017, https://bit.ly/2iFg621.

[3] Chye-Ching Huang and Chloe Cho, “Ten Facts You Should Know About the Federal Estate Tax,” CBPP, updated October 30, 2017, https://bit.ly/2uvD5DL.

[4] Jonathan Curry, “TCJA Supercharges ‘Upstream’ Estate Tax Planning Techniques,” Tax Notes, March 23, 2018, http://www.taxanalysts.org/content/tcja-supercharges-upstream-estate-tax-planning-techniques. For an explanation, see Roderick Taylor, “New Estate Tax Cut Encourages More Wealthy Individuals to Skirt Capital Gains Tax,” CBPP, May 17, 2018, https://www.cbpp.org/blog/new-estate-tax-cut-encourages-more-wealthy-individuals-to-skirt-capital-gains-tax.

[5] Curry 2018.