Federal Spending and the Debt Limit

Testimony of Chad Stone, Chief Economist,

Center on Budget and Policy Priorities,

Before the Subcommittee on Oversight and Investigations

of the Financial Services Committee

U.S. House of Representatives

Chairman Duffy, Ranking Member Green, and other members of the subcommittee, thank you for the opportunity to testify at today’s hearing. In my testimony I want to make two broad points. The first is the need to focus not just on spending but also on revenues in addressing our long-term budget challenges. The second is to caution strongly against thinking that the statutory limit on federal debt has any constructive role to play in addressing those challenges.

Budget deficits result from an imbalance between spending and revenue; rising debt relative to the size of the economy results from persistent large deficits, not from too much spending per se. Any plausible amount of spending to meet society’s needs is sustainable if there are sufficient revenues to avoid large deficits.

CBO projects that under current tax and spending policies, rising debt will ultimately prove unsustainable. This poses a serious challenge to policymakers. At the same time, as I discuss in the first part of this testimony, there is not an immediate crisis. Policymakers, however, will have to make hard choices in setting a future course that is both fiscally responsible and realistic about the levels of spending and taxes appropriate to the country’s needs.

These decisions need to be kept separate from the debt limit. As I discuss in the second part of the testimony, the debt limit encourages reckless brinkmanship that makes it harder to work out the compromises necessary to achieve a sustainable deficit-reduction agreement. As former Federal Reserve Chairman Ben Bernanke says in his recent book: “Refusing to raise the debt limit takes the economic well-being of the country hostage [and] ought to be unacceptable no matter what the underlying issue being contested.”

I’ll elaborate on these themes in the remainder of my testimony.

Trends in Government Spending and Debt

1. Temporary Factors Drove Deficits and Debt in the Great Recession

The sharp increases in deficits and debt during the financial crisis and Great Recession certainly caught policymakers’ and the public’s attention, but looking over a longer time span shows they were not unprecedented. Deficits were larger and the run-up in debt much sharper in World War II.

The surge in deficits after 2008, in fact, was temporary and resulted from economic weakness in the Great Recession as revenues shrank with the decline in economic activity, spending on unemployment insurance and other programs rose, and emergency tax cuts and spending increases were enacted to combat the recession. After peaking in 2009, the budget deficit fell as a share of GDP each year through 2015 as the economy slowly recovered, stimulus programs phased out, and policymakers enacted new deficit-reduction policies.

That decline is now over, and CBO’s latest projections see deficits beginning to widen again and debt reaching 86 percent of GDP in 2026 — which, it is worth noting, is still well short of 1946’s 106 percent.

2. The Aging of the Population and Rising Health Care Costs Are the Drivers of Longer-term Spending Increases

Even before the Great Recession, budget experts recognized that long-term deficits and debt were on an unsustainable path after about 2020 due to the aging of the population and expected increases in health care costs.[1] These factors are the drivers of projected future deficits and debt, not the temporary policies enacted to combat the recession,[2] which, in fact, kept economic conditions from being even worse than they were.[3]

In other words, in the lead-up to the debt-limit crisis and enactment of the Budget Control Act of 2011, policymakers faced a known long-term fiscal sustainability problem but not an immediate deficit or debt crisis. Notwithstanding policymakers’ failure at that time to come up with a comprehensive long-term budget plan, things are substantially better now than they were then due to a combination of policy actions and projected slower growth in health care costs.

In 2010, budget experts were projecting that under plausible baseline assumptions, debt would rise well above 200 percent of GDP by 2040. CBO now projects that with no further action it could rise to 155 percent of GDP in 2046, citing the aging of the population and growth in per capita health care spending as main drivers. As CBO says, such a trend is ultimately unsustainable.

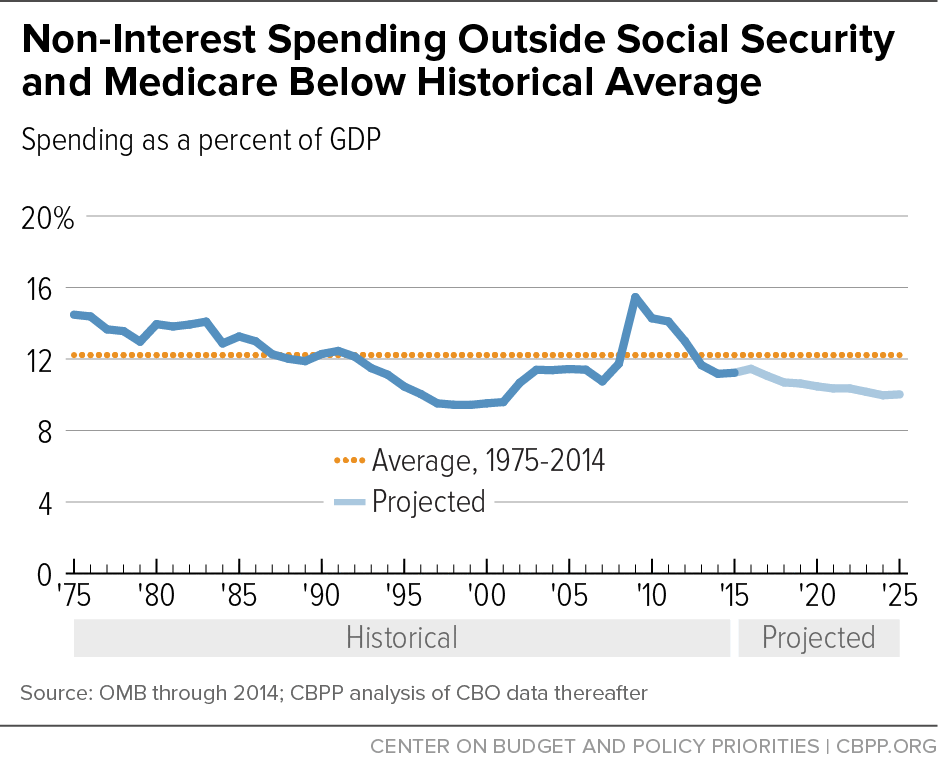

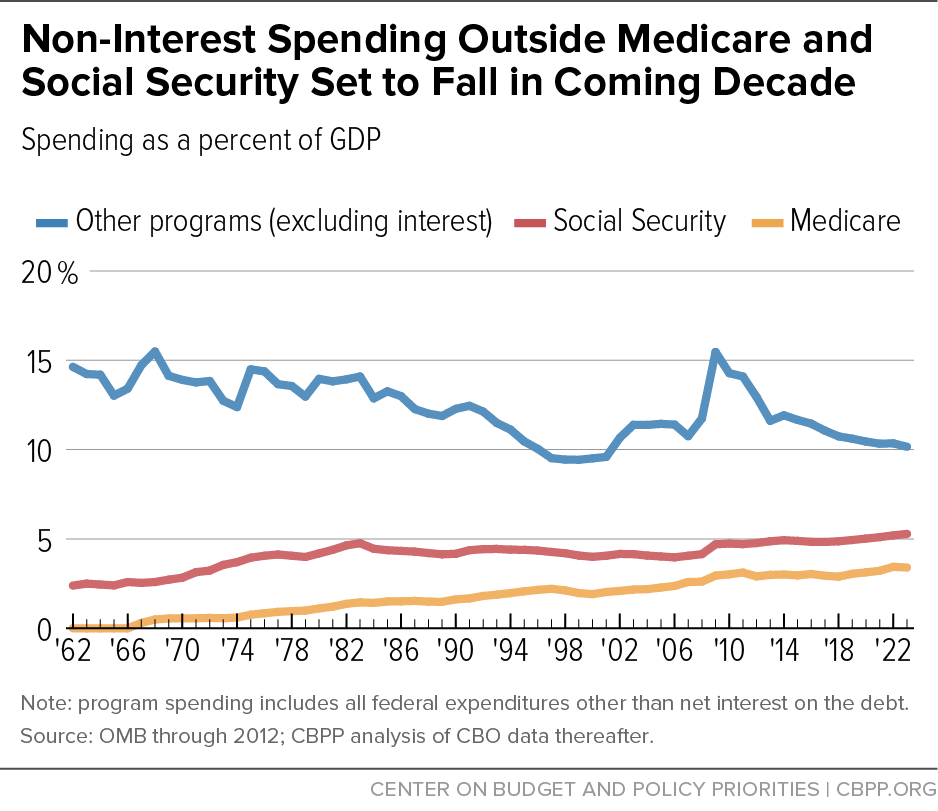

We should be clear, however, that we don’t have a general problem of spending growing faster than the economy throughout the government. Program (non-interest) spending outside of Social Security and Medicare is running below its historical average, as a percent of GDP and is expected to fall further. The nearby charts show a distinct but temporary bump in such spending during the Great Recession and ensuing recovery, but that spending has already come down to below its historical average and is projected to decline further.

It is also important to remember that Social Security and Medicare are not bloated, unpopular programs. Large majorities of Americans say that they don’t mind paying for Social Security because they value it for themselves, their families, and millions of others who rely on it. While Social Security benefits are more modest than many people realize, for most workers Social Security will be their only source of guaranteed retirement income that is not subject to investment risk or financial market fluctuations.[4]

Medicare is similarly popular and effective. In a nationally representative survey, more than three-quarters of respondents (77 percent) say Medicare is a very important program, ranking just below Social Security (83 percent).[5] Medicare’s benefits, too, are not overly generous: they are less comprehensive than a typical employer-sponsored health plan, and Medicare households spend a substantially larger share of their budgets on out-of-pocket health costs and do non-Medicare households.

Increasing generosity of benefits is not what’s driving the increase in Social Security and Medicare spending. Rather it’s the rising share of the population eligible for benefits, and in Medicare, rising health care costs — which affect public and private health care spending alike. Relatively modest changes would place Social Security on a sound financial footing for 75 years and beyond. The cost controls and delivery system reforms in the Affordable Care Act (ACA), plus other developments in health care delivery, are expected to curb (though not eliminate) health care cost pressure.

3. Spending for Low-Income Programs Is Not Driving Deficits and Debt

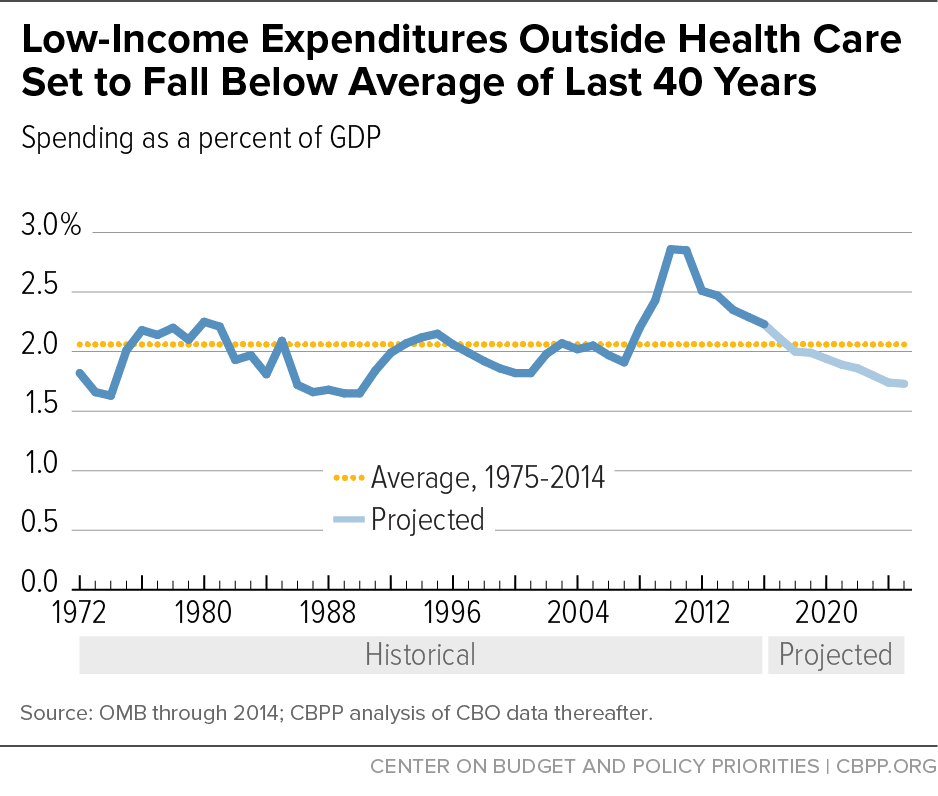

A similar theme applies with regard to low-income programs. Spending on the most vulnerable among us rose sharply in the Great Recession and the years immediately thereafter, but CBPP analysis finds that spending on such programs outside health care has been falling and is projected to fall further. Specifically, outside of health care, federal spending for low-income programs (including refundable tax credits such as the Earned Income Tax Credit) averaged about 2.1 percent of GDP over the past four decades (see chart). These expenditures are on track to fall below that level in coming years.

4. Long-Run Fiscal Sustainability Does Not Require Balanced Budgets

The budget does not have to be balanced to reduce the economic burden of the debt. Increases in the dollar amount of debt are not a serious concern as long as the economy is growing at least as fast. For example, as the earlier chart shows, even though there were deficits in almost every year between World War II and the early 1970s, debt grew much more slowly than the economy, so the debt-to-GDP ratio fell dramatically.

Now, however, CBO projects that without policy changes, deficits and debt will rise as a share of GDP. Generally, the debt-to-GDP ratio should rise only during hard times or major emergencies and then decline during good times. That enables the government to combat recessions through temporary tax cuts and spending increases and to alleviate hardship during bad times, while creating a presumption against policies that markedly increase the debt during good times.

A stable debt-to-GDP ratio rather than a balanced budget is a key test of fiscal sustainability. Some suggest that certain debt-to-GDP ratios have a particular meaning in terms of their effect on the economy. In reality, there are no absolute thresholds.

Until a few years ago, for instance, many pointed to a 2010 analysis by economists Carmen Reinhart and Kenneth Rogoff suggesting that debt-to-GDP ratios of 90 percent or more are associated with significantly slower economic growth. But the authors have acknowledged computational errors in their original work and clarified that there is no “magic threshold” for the debt ratio above which countries suddenly pay a marked penalty in terms of slower economic growth. To the extent that countries with higher levels of debt experience slower growth, there is not much evidence that the high debt caused the slow growth; the reverse is just as likely to be true — that the slow growth caused the high debt — or some combination of the two effects.

Similarly, some analysts call for a debt ratio of 60 percent of GDP or less, a goal that the European Union and the International Monetary Fund (IMF) adopted in the 1990s. No economic evidence supports this or any other specific target, however, and IMF staff have made clear that the 60 percent criterion is arbitrary and should not guide near-term fiscal policy in the wake of the recent financial crisis, which drove up government debt worldwide. The IMF recently stated, “Our results do not identify any clear debt threshold above which medium-term growth prospects are dramatically compromised.”

All else being equal, a lower debt-to-GDP ratio is preferred because of the additional flexibility it provides policymakers facing economic or financial crises and the lower interest burden it carries. But all else is never equal. Lowering the debt ratio comes at a cost, requiring larger spending cuts, higher revenues, or both. That is why it is important to look at not only the quantity but also the quality of deficit reduction, which should not hinder the economic recovery, cut spending in areas that can boost future productivity, or harm vulnerable members of society.

The Debt Limit Plays No Constructive Role in Budget Policy

Policymakers who want to improve the country’s economic and budget outlook should scrap the debt limit (also known as the debt ceiling), which plays no constructive role in enforcing budget discipline. Rather, it encourages reckless brinkmanship that makes it harder to work out the compromises necessary to achieve a sustainable deficit-reduction agreement.

As CBO explains in a 2010 report:[6]

By itself, setting a limit on the debt is an ineffective means of controlling deficits because the decisions that necessitate borrowing are made through other legislative actions. By the time an increase in the debt ceiling comes up for approval, it is too late to avoid paying the government’s pending bills without incurring serious negative consequences.

CBO does go on to say, “However, because increases in the debt limit have been essential, the process of considering such increases tends to bring debt levels to the forefront of policy debate.” That was in 2010. But “debt levels” were already prominent in fiscal policy debates and remain there now, as this hearing shows.

5. Debt Subject to Statutory Limit Has No Economic or Financial Significance

Table 1-3 in CBO’s report shows projections for several measures of federal debt. Its featured measure is debt held by the public — basically, the sum of all past deficits minus surpluses. This measure tells us what the federal government owes to outside lenders such as corporations, households, and other governments here and abroad. Changes in government borrowing from the public are significant because they can affect national saving and credit markets.

The debt limit applies to a different measure. In addition to debt held by the public, debt subject to limit includes money that the federal government owes to itself — such as the money the Social Security and Medicare trust funds have lent to the Treasury in years when their revenues exceeded their spending for benefits and other costs. Debt subject to limit is a close cousin of “gross debt” (the debt shown in those scary debt clocks). These are seriously flawed and analytically meaningless measures of the debt.

Between 1998 and 2001, for example, debt subject to limit continued to grow — even though the country was running budget surpluses and retiring some of the debt held by the public — because the Social Security trust fund was running large surpluses and lending them to the Treasury. Likewise, a policy aimed at improving long-term fiscal stability by shoring up the Social Security trust funds would reduce the deficit without reducing the debt subject to limit or the gross debt.

6. The Debt Limit Is Harmful

A recent report by the Government Accountability Office (GAO)[7] reinforces the conclusion that we would be better off without a debt limit.[8]

GAO found that in October 2013, when the Treasury was close to breaching the debt limit, “investors reported taking the unprecedented action of systematically avoiding certain Treasury securities.” That cost the Treasury “from roughly $38 million to more than $70 million” in higher interest costs — amounting to, in essence, nothing more than a waste of taxpayers’ money.

GAO also interviewed budget and policy experts (including some of us at CBPP) and identified three alternative ways to handle the debt limit if we were not willing to scrap it:

- Let the debt limit rise automatically or at a minimum, force an immediate vote on a “clean” debt limit increase — that is, one that’s not attached to any other legislative proposals — whenever Congress adopts a new budget resolution. Congress could no longer pass a budget plan but not set a debt limit consistent with it.

- Allow the President to raise the debt limit as needed to cover bills incurred under existing budget law, while giving Congress a special, fast-track procedure to pass a law disapproving any such action.

- Allow the Treasury to borrow as needed to cover bills incurred under existing budget law.

Any of these alternatives is better than the current approach, in which Congress enacts spending and tax laws but doesn’t have to permit the borrowing needed to cover the nation’s resulting bills — and so raises the risks of what could be a catastrophic default.

GAO’s conclusions mirror those of a distinguished and bipartisan group of top economists who overwhelmingly agreed in 2013, “Because all federal spending and taxes must be approved by both houses of Congress and the executive branch, a separate debt ceiling that has to be increased periodically creates unneeded uncertainty and can potentially lead to worse fiscal outcomes.”[9]

And, as the Financial Times opined a few years ago, “Sane governments do not cast doubt on the pledge to honor their debts — which is why, if reason prevailed, the debt ceiling would simply be scrapped.”

The 2011 debt-limit showdown was not pretty, and even though a default was averted, the economy and the budget did not escape unharmed. As Urban Institute Fellow Donald Marron, a former acting CBO director and a member of President George W. Bush’s Council of Economic Advisers, testified in 2013 before the Joint Economic Committee, “brinksmanship does not come free.”[10]

Through accident or miscalculation, games of chicken can sometimes end in a crash, and the costs to the United States of actually defaulting on its financial obligations could be very high. If prolonged, a situation in which the Treasury is required to match payments to available cash would have an economic effect like sequestration on steroids and would likely plunge the economy back into recession. Even if the debt limit were subsequently raised, the damage to the U.S. credit rating likely would harm us for years to come.

To my knowledge, only one other developed country, Denmark, has a statutory debt limit anything like ours. Both countries have put a dollar limit on how much debt the government can issue. There’s a crucial difference, however, between our debt limit and Denmark’s: the Danes do not play politics with theirs, as Jacob Funk Kirkegaard of the Peterson Institute for International Economics explains:[11]

The Danish fixed nominal debt limit — legislatively outside the annual budget process — was created solely in response to an administrative reorganization among the institutions of government in Denmark and the requirements of the Danish Constitution. It was never intended to play any role in day-to-day politics.

When the financial crisis caused a sharp increase in government debt in 2008-2009, the Danes raised their debt ceiling — a lot. The 2010 increase doubled the existing ceiling, which was already well above the actual debt, to nearly three times the debt at the time. As Kirkegaard reports, “The explicit intent of this move — supported incidentally by all the major parties in the Danish parliament — was to ensure that the Danish debt ceiling remained far in excess of outstanding debt and would never play a role in day-to-day politics.”

The Constitution gives Congress power over federal borrowing, which it has exercised for decades through the statutory limit on federal debt. But the government is also legally bound to honor its financial obligations. Holding the debt limit hostage risks provoking a governance crisis in which the President is forced to choose between breaking the law by ignoring the debt ceiling or breaking the law by not paying government obligations in a timely manner. In terms of limiting economic damage, the former is by far the better choice.

7. Debt Prioritization Proposal Is Extremely Dangerous

Legislation like H.R. 692 that would allow Treasury to borrow funds to pay bondholders and Social Security recipients if there’s a prolonged standoff over raising the debt ceiling is extremely dangerous. By appearing to make a default legitimate and manageable, it would heighten the risk that one will actually occur.

Millions of people beyond bondholders and Social Security beneficiaries depend on timely federal payments. H.R. 692 says nothing about how the Treasury can pay veterans, troops, doctors and hospitals that treat Medicare patients, state and local governments, private contractors, and recipients of unemployment insurance, SNAP, and Supplemental Security Income.

The Treasury makes roughly 80 million separate payments each month, so deciding which bills to pay would be extremely difficult, even if interest and Social Security benefits could be pulled out and paid. And domestic and foreign lenders would hardly be reassured at the sight of Treasury grappling with how to meet its legal obligations when cash is short.

During a standoff over raising the debt ceiling in early 2013, one rating agency explicitly warned that honoring interest and principal payments but delaying payment on other obligations would trigger a review and possible downgrade of the nation’s creditworthiness. At that time, the Economist called failing to raise the debt limit and attempting to prioritize payments an “instrument of mass financial destruction.”

Conclusion

I respectfully disagree with the view that unsustainable federal spending is the sole force driving projected future deficits and debt, that balancing the budget is necessary to achieve fiscal sustainability, or that the debt ceiling has any constructive role to play in budget policy.

New revenues will have to be a part of any realistic effort to achieve fiscal sustainability and meet 21st century national needs. Policymakers will have to be willing to buckle down and make compromises. Revenues were a part of every major deficit reduction package in the 1980s and 1990s until the Balanced Budget Act of 1997.[12]

Holding budget negotiations hostage to the debt limit and trying to pretend that it is legitimate and manageable to do so is a new and dangerous tactic. Congress should take away that temptation by following one of the GAO’s recommendations or, better yet, scrapping the debt limit altogether.

End Notes

[1] Richard Kogan, et al., “The Long-Term Fiscal Outlook is Bleak,” Center on Budget and Policy Priorities, January 29, 2007, https://www.cbpp.org//sites/default/files/atoms/files/1-29-07bud.pdf.

[2] Kathy Ruffing and Joel Friedman, “Economic Downturn and Legacy of Bush Policies Continue to Drive Large Budget Deficits,” Center on Budget and Policy Priorities, February 28, 2013, https://www.cbpp.org/research/economic-downturn-and-legacy-of-bush-policies-continue-to-drive-large-deficits.

[3] Alan S. Blinder and Mark Zandi, “The Financial Crisis: Lessons for the Next One,” Center on Budget and Policy Priorities, October 15, 2015, https://www.cbpp.org/research/economy/the-financial-crisis-lessons-for-the-next-one.

[4] “Policy Basics: Top Ten Facts About Social Security,” Center on Budget and Policy Priorities, updated August 13, 2015, https://www.cbpp.org/research/social-security/policy-basics-top-ten-facts-about-social-security#_ftn28.

[5] “Medicare and Medicaid at 50,” The Henry J. Kaiser Family Foundation, July 17, 2015, http://kff.org/medicaid/poll-finding/medicare-and-medicaid-at-50/.

[6] Federal Debt and Interest Costs, Congressional Budget Office, December 2010, p. 23, http://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/119xx/doc11999/12-14-federaldebt.pdf.

[7] “Debt Limit: Market Responses to Recent Impasses Underscores Need to Consider Alternative Approaches,” GAO-15-476, U.S. Government Accountability Office, July 9, 2015, http://www.gao.gov/products/GAO-15-476.

[8] Richard Kogan, “Federal Debt Limit’s Harmful, Report Shows,” Center on Budget and Policy Priorities, July 16, 2015, https://www.cbpp.org/blog/federal-debt-limits-harmful-report-shows.

[9] “Debt Ceiling,” IGM Forum, January 15, 2013, http://www.igmchicago.org/igm-economic-experts-panel/poll-results?SurveyID=SV_555sdN4BXmfNKCN.

[10] Donald Marron, “The Costs of Debt Limit Brinksmanship,” Tax Policy Center, September 18, 2013, http://www.taxpolicycenter.org/publications/url.cfm?ID=904601.

[11] Jacob Funk Kirkegaard, “Can a Debt Ceiling Be Sensible? The Case of Denmark II,” Peterson Institute for International Economics, July 28, 2011, http://www.piie.com/blogs/realtime/?p=2292.

[12] Kathy Ruffing, “The Composition of Past Deficit-Reduction Packages – And Lessons for the Next One,” Center on Budget and Policy Priorities, November 15, 2011, https://www.cbpp.org/research/the-composition-of-past-deficit-reduction-packages-and-lessons-for-the-next-one?fa=view&id=3617.

More from the Authors