BEYOND THE NUMBERS

Technical Change Doesn’t Fix Real Flaws With House Approach to Tax Extenders

House Republicans have scrambled to make a technical change to the first of six “tax extender” bills that the Ways and Means Committee has approved to ensure that it won’t lead to a new round of sequestration budget cuts. But this change doesn’t fix the serious flaws with the House approach toward the extenders.

The bill, which would expand and make permanent the research and experimentation tax credit, doesn’t offset its cost of $156 billion over 2014-2024. Thus, it violates the “pay-as-you-go” law requiring policymakers to pay for all entitlement expansions and tax cuts — which means the bill raises the possibility of an eventual sequestration of certain mandatory spending programs (including Medicare and student loans) to generate offsetting savings.

To address this problem, House Republicans changed the bill to specify that its costs wouldn’t count for “pay-as-you-go” purposes.

But this change only confirms what we had already assumed about the House bill — that it did not offset its costs — and does nothing to address the underlying problems our report identified with the House approach toward the extenders. The extenders bills still would:

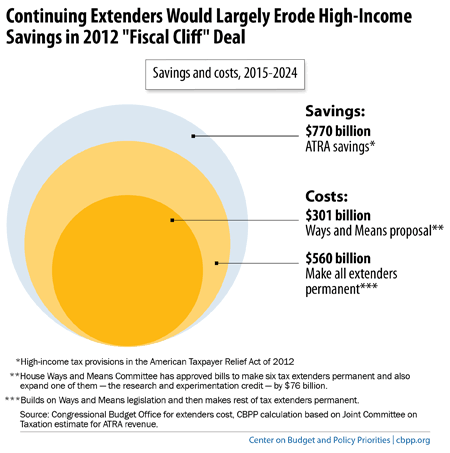

- Undo a sizeable share of the savings from recent deficit-reduction legislation. At a combined ten-year cost of $301 billion (or $310 billion over 11 years, 2014-2024), the six bills would give back two-fifths of the $770 billion in revenue raised by the 2012 “fiscal cliff” legislation. If policymakers go further and make permanent all of the roughly 80 extenders, the ten-year cost would rise to about $560 billion, cancelling nearly three-quarters of the “fiscal cliff” savings (see chart).

Image

- Constitute a fiscal double standard. Failure to pay for making the extenders permanent would contrast sharply with congressional demands to pay for other budget priorities, from easing the sequestration cuts to providing permanent relief from cuts in doctor payments under Medicare to restoring emergency federal unemployment insurance.

- Leave out other priorities. The process to date cherry picks several of the most heavily lobbied corporate tax extender provisions, while leaving behind expired provisions for hard-hit homeowners, teachers, and distressed communities, as well as alternative energy. Moreover, the push for permanence would mean that these corporate provisions would leap-frog over more important tax provisions that are scheduled to expire in coming years — notably key improvements to the Earned Income Tax Credit and Child Tax Credit for low-income working families and the American Opportunity Tax Credit for college students.

- Bias future tax reform efforts against reducing deficits. If policymakers make the extenders permanent in advance of tax reform, a future tax reform plan would no longer have to offset the extenders’ cost to achieve revenue neutrality (much less meet the more appropriate goal of raising revenue to reduce deficits). This would free up hundreds of billions of dollars in tax-related offsets over the decade that policymakers could then channel towards lowering the top tax rate, while still claiming revenue neutrality, even though deficits would be higher.

- Violate budget enforcement rules. As noted, the House bill specifies that its costs wouldn’t count for “pay-as-you-go” purposes. But, both last December’s Murray-Ryan deal and the House-passed budget resolution also require policymakers to pay for any tax extenders that they continue or for any new tax cuts. The Ways and Means bills violate this requirement as well, and they also undercut a widely touted feature of the House-passed budget — its claim to balance the budget in 2024 — by adding to deficits.