BEYOND THE NUMBERS

New York Times Calls Senate Finance Committee “Extenders” Vote Fiscally “Imprudent”

The Senate Finance Committee has voted to reinstate dozens of temporary tax breaks that expired at the end of 2013 — without offsetting their cost. A recent must-read New York Times editorial called the vote “imprudent.” Indeed, we find it fiscally unsound.

The Senate Finance Committee bill would cost more than $85 billion to extend the so-called “tax extenders,” which are mostly corporate tax breaks that Congress has routinely extended year after year. But that misrepresents the true cost of these tax breaks, because the bill would extend them for only two years.

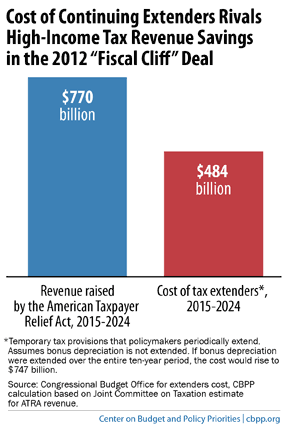

Indeed, if Congress repeatedly renewed the extenders without offsets, they would cost $484 billion over the next decade. That’s the equivalent of “giving back” more than half of the revenue from the “fiscal cliff” budget deal of late 2012, when policymakers raised tax rates on very high-income taxpayers (see chart).

This total excludes the costs of continuing of bonus depreciation, a provision that allows businesses to take bigger upfront tax deductions for certain new investments, on the assumption that Congress would let this stimulus measure expire, as it has in the past, once the economy strengthens. That would be the right step, as we’ve explained.

If instead, Congress continued this provision, the ten-year cost of making the tax extenders permanent would rise to $747 billion — eroding nearly all of the fiscal cliff revenue savings. (The Finance Committee bill includes a two-year extension of bonus depreciation.)

Policymakers’ current approach to extenders is not only fiscally unsound, but the New York Times highlights that it also represents a fiscal double standard:

For the past few years, Democrats have gone along with the Republicans’ refusal to incur debt for programs that are far more effective than tax cuts at boosting the economy and far more urgent — like jobless benefits and spending on education and infrastructure. Instead of borrowing to pay for such needs, lawmakers have coupled most new outlays with spending cuts elsewhere in the budget. . . . In contrast, borrowing to finance the tax cuts basically transfers money to corporate owners and executives, with no reduction demanded in other forms of government aid to business and with future taxpayers left to pay the bill.

Congress has better choices: for example, House Ways and Means Committee Chairman Dave Camp’s tax plan includes provisions that limit or eliminate dozens of special interest revenue raisers, providing a roadmap on how to pay for any extenders that policymakers think are worth continuing.