off the charts

POLICY INSIGHT

BEYOND THE NUMBERS

BEYOND THE NUMBERS

SNAP Spending and Caseloads Falling

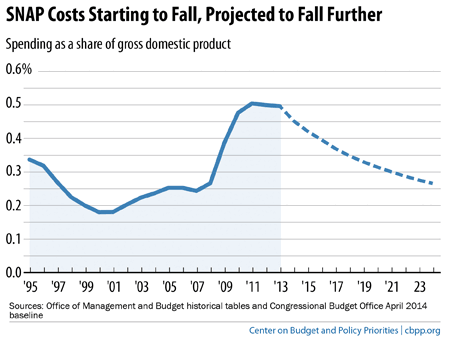

SNAP spending, which doubled as a share of the economy (gross domestic product or GDP) in the wake of the Great Recession, has begun to decline, as the Congressional Budget Office (CBO) and other experts expected, our updated report explains. Here are its main points:

- SNAP spending as a share of GDP was stable in fiscal years 2012 and 2013 and is on track to fall substantially in 2014 and thereafter. Government data show that spending on SNAP (formerly food stamps) fell slightly as a share of GDP in 2012 and 2013 and is expected to fall by 9 percent in 2014. As the economic recovery continues and fewer low-income people qualify for SNAP, CBO expects SNAP spending to fall further in future years, returning to its 1995 levels as a share of GDP by 2019. (See graph.)Image

- The end of the Recovery Act’s benefit increase has contributed to the large drop in SNAP spending in 2014. U.S. Department of Agriculture (USDA) data show that due to the November 1, 2013 expiration of a SNAP benefit increase in the 2009 Recovery Act, average benefits fell by about 7 to 8 percent, or over $400 million, in November. Over the first six months of fiscal year 2014 (October 2013 through April 2014), SNAP outlays were 7 percent lower than the same period of fiscal year 2013 on a nominal basis, rather than as a share of GDP.

- The number of SNAP participants has started to fall. SNAP caseload growth slowed in 2011 and 2012. Caseloads held steady in 2013 and have now begun to decline: fewer people participated in SNAP in each of the last six months for which data are available (September 2013 through February 2014) than in the same months one year earlier; 1.6 million fewer people participated in SNAP in February 2014 than when participation peaked in December 2012. SNAP participation has fallen in 47 states and, in the other states, the rate of growth has slowed substantially. This trend of falling caseloads follows the pattern of recovery from previous recessions.

Topics:

CBPP

Receive the latest news and reports from the Center