BEYOND THE NUMBERS

Putting Housing Money Where the Need Is

The artificial distinction between tax expenditures (credits, deductions, and other tax breaks) and spending programs “make[s] it harder to gauge the impact of the federal budget on such crucial activities as housing,” a recent New York Times story explains, noting that the mortgage interest deduction — which mostly helps high-income people — costs far more than spending programs to help low- or moderate-income people afford housing. The story continues:

“If someone said, ‘Let’s have a voucher program on the spending side, giving high-income families vouchers to subsidize their mortgages,’ ” said Glenn Hubbard, the dean of Columbia Business School and a prominent Republican economist, referring to the home mortgage interest deduction, “I don’t think that would get through Congress.”

That’s why we’ve called for rebalancing federal housing policy by creating a renters’ tax credit to help low-income families afford housing.

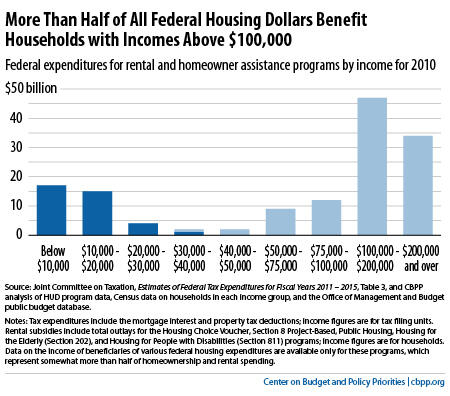

Policymakers have focused for decades on policies to increase homeownership, and most federal housing dollars benefit families with relatively little need for assistance. More than half of federal dollars for housing benefit households with incomes above $100,000 (see chart).

Meanwhile, the nation’s lowest-income renters are far likelier to struggle to pay for housing — and their affordability problems are growing.

A renters’ credit, administered by states and capped at $5 billion a year, could:

- Assist about 1.2 million of the lowest-income renter households;

- Reduce each household’s rent by an average of $400; and

- Lift 250,000 families out of poverty and lift four of five of the poorest families it assists out of deep poverty (defined as having income below half of the federal poverty guidelines).

It’s the right time to consider such a credit, as policymakers consider restructuring tax expenditures as part of tax reform. Proposed changes to the mortgage interest deduction (such as converting it to a credit) could make homeownership-related tax expenditures more efficient and raise added revenues to reduce the deficit. And, by directing a modest share of the savings from these or other tax reforms to the renters’ credit, policymakers could make the nation’s housing dollars fairer and more effective.