BEYOND THE NUMBERS

Policymakers Should Reject Calls to Make Business Tax Credits Refundable

Some policymakers are considering whether to make certain business tax credits temporarily refundable — that is, available to firms that don’t have enough taxable income to otherwise qualify — saying that would give cash to struggling small businesses to help them weather the recession. But the policy would likelier deliver a windfall to large corporations that have other ways to access cash than help struggling firms, and it likely wouldn’t generate significant new investment this year to boost the economy. Policymakers should reject the proposal and opt for measures likelier to benefit struggling businesses and strengthen the economy.

Business tax credits are typically intended to encourage certain investments, like research and development and low-income housing. The research credit is already refundable for small businesses, so they wouldn’t benefit from the proposed change. Most other business credits in a given year are non-refundable. That means businesses can’t use the credits to get a federal cash payment if they don’t have enough taxable income against which to apply the credits that year, either because they don’t have significant profits that year or because they use other tax breaks to reduce their tax liability. In that case, however, businesses can “carry the credits back” (i.e., apply them to taxes they owe for the prior year) or carry them forward and use them to lower their tax obligations for up to 20 years in the future. Making these credits temporarily refundable so businesses can get a refund now will give the most help to firms that have large unused credits they’re carrying forward, which is most likely large, financially stable corporations.

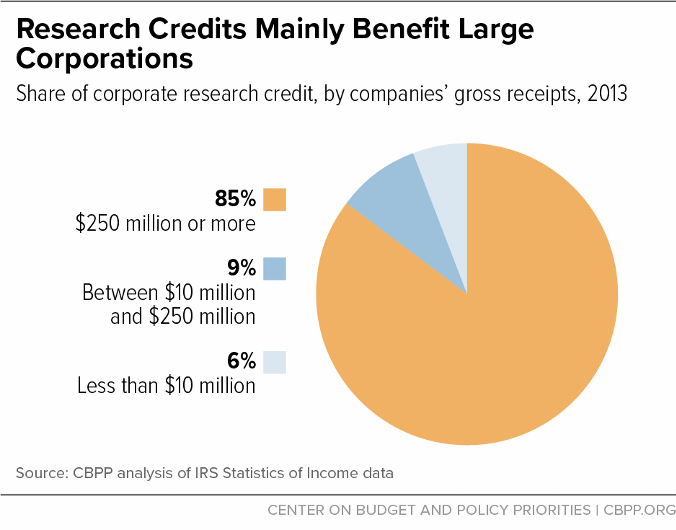

The research credit is the largest of these business credits, at a cost of around $150 billion over ten years, and it mainly flows to large manufacturers. Some 85 percent of corporate research credits went to companies with more than $250 million in gross receipts, with the manufacturing industry as the largest beneficiary, according to IRS data for 2013 (the latest year for which we have available data). Of all general business credits that corporations carry forward to future years, more than 60 percent go to manufacturers and financial firms. With or without refundability, these businesses are better placed to weather the crisis; for instance, they typically have ready access to other sources of cash such as low-interest loans from the Federal Reserve’s new lending program.

Refundability could also be quite costly. While draining federal revenues upfront (by allowing companies to claim credits now that they otherwise would carry into the future), it also would give cash payments to a number of corporations now for credits that otherwise would eventually expire without the corporations ever using them. A substantial portion of these business credits remain unused in the year that companies make the qualifying investment, and some ultimately expire. Thus, refundability would provide an expanded subsidy to these corporations, raise federal costs, and, at best, provide only uncertain economic benefits. In addition, large, upfront tax benefits could provide opportunities for individuals to create fraudulent companies, file falsified tax returns claiming refundable tax credits, and then liquidate the companies — with an under-funded, over-worked IRS left to try to recover lost revenues via audits.

Despite supporters’ claims, temporary refundability likely wouldn’t encourage significant new investment or job creation above what would occur anyway. Generally, businesses are less likely to invest during economic downturns, “when they have idle capacity and when they are less confident about the future demand for their products and services,” former Congressional Budget Office Director Douglas Elmendorf has noted. Upfront refundable credits for certain kinds of investment will have little effect on such investment if there’s still little demand for the products and services that the investments would produce. And the 2017 tax law already gives businesses significant tax benefits for investing, letting them deduct 100 percent of the cost of equipment in the year they buy it — which is the most aggressive version of a tax break called “bonus depreciation.”

Moreover, letting businesses both fully expense investments and claim unlimited refundable business credits at the same time would give them significant windfalls, compared to what policymakers did in the 2009 Recovery Act. During the Great Recession of a decade ago, policymakers enacted temporary measures to make it easier for businesses to claim research credits, while also limiting other tax breaks. Businesses could get a refundable research tax credit (of up to $30 million) in lieu of bonus depreciation (which at the time was worth up to 50 percent of the cost of equipment and other purchases). If policymakers were to let corporations now claim both full 100 percent expensing and refundable research credits at the same time, firms would get much larger tax breaks than what the Recovery Act provided.

As policymakers consider more economic relief and stimulus legislation, they should reject proposals that would give unneeded windfalls to large business owners and do little to boost demand for goods and services or strengthen the economy. Instead, they should enact better-targeted measures to get cash to struggling businesses, such as by improving policies in the CARES Act of March to increase small business liquidity, and measures to enable workers who have lost their jobs and others who are struggling to get by to maintain their consumption.