BEYOND THE NUMBERS

House GOP Restarts Effort to Make “Tax Extenders” Permanent

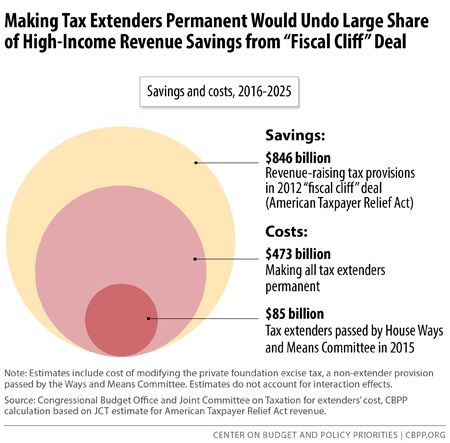

The House is scheduled to vote tomorrow on the first of an expected series of bills to make permanent many large “tax extenders” — tax breaks, mostly for corporations, that policymakers routinely extend a year at a time — without offsetting the cost. Tomorrow’s bill would make popular charitable-related tax provisions permanent, which many lawmakers support on policy grounds. But, as our paper explains, doing so now without offsetting the costs would open the door for making other, costlier extenders permanent. Making all of the extenders permanent would cost $473 billion over the next decade (see graph).

Ways and Means Committee Chairman Paul Ryan has made clear that House Republican leaders are simply “picking up where we left off last year,” when the House passed a series of permanent tax-extender bills, along with a bill to expand and permanently extend the “bonus depreciation” tax break, without offsetting any of the cost. The President and many House members opposed that effort, and the President has properly threatened to veto tomorrow’s bill to make permanent the charitable provisions that Ways and Means approved last week.

Making the extenders permanent without paying for them would:

- Undo most of the savings from recent deficit-reduction legislation. Together, last year’s House-passed measures would have given back nearly three-quarters of the revenue raised by the 2012 “fiscal cliff” legislation. The seven bills that Ways and Means has already approved in 2015 begin the same process anew, costing $85 billion over 2016-2025.

- Bias tax reform against reducing deficits. Policymakers are expected to attempt corporate tax reform this year. If they make the extenders permanent in advance of tax reform, a reform plan wouldn’t have to offset the extenders’ cost to be considered revenue neutral. This would free up hundreds of billions of dollars over the decade that policymakers could use to lower the corporate tax rate more sharply or close fewer dubious corporate tax breaks, while still claiming revenue neutrality. The result would be much larger deficits than under revenue-neutral corporate tax reform that pays for any extenders it keeps.

- Place corporate tax extenders ahead of other, more critical tax provisions slated to expire. Most notably, if key elements of the Earned Income Tax Credit and Child Tax Credit for low-income working families expire as scheduled at the end of 2017, more than 16 million people in low-income working families, including 8 million children, would fall into — or deeper into — poverty. Some 50 million Americans would lose part or all of their credits. A growing body of evidence links income from these credits to improvements in children’s health, educational attainment, and employment and earnings later in life.