BEYOND THE NUMBERS

Austerity Bites

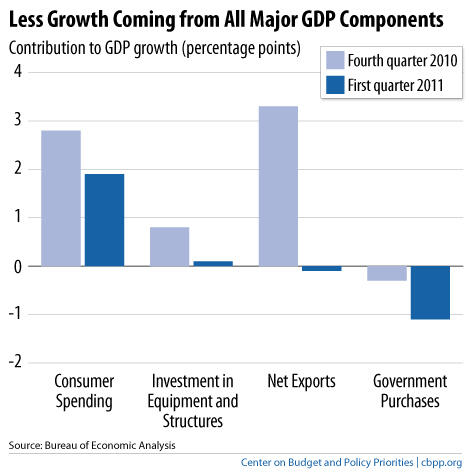

U.S. economic growth slowed to an annual rate of 1.8 percent in the first quarter of 2011, according to new Commerce Department data. Declines in federal and local government purchases of goods and services subtracted 1.1 percentage points from the growth rate (see chart). Consumer spending, investment spending, and net exports all decelerated, making smaller contributions to growth in Gross Domestic Product than in the previous quarter.

My hope three months ago that strong growth in final sales (often a better measure of underlying demand than GDP) in the fourth quarter of 2010 indicated that the recovery was gathering steam hasn’t been borne out. Final sales in the first quarter of 2011 rose an anemic 0.8 percent, as unsold goods piled up on the shelves.

Is this really the time for Congress to be debating how fast it can cut government spending, rather than how to keep the economic recovery from losing momentum? Is this really the time for Fed Chairman Bernanke to act as though inflation concerns preclude any further monetary stimulus, even though the Fed’s announcement yesterday pointed to the economy’s “low rates of resource utilization, subdued inflation trends, and stable inflation expectations”?

The United States is not as far down the road as the UK in pursuing the dubious “expansionary austerity” policy prescription of sharp cuts in government spending to quickly reduce the deficit, and all the evidence is not yet in on the UK experiment. But it sure isn’t looking good: the British economy is stagnating, and there is no evidence that a commitment to austerity measures can override weak current economic conditions. Why should we think the results would be different here?