Testimony: Robert Greenstein, President, on “Deficit Reduction: A Review of Key Issues”

Before the Senate Committee on Finance United States Congress

Mr. Chairman and members of the Committee, thank you for the invitation to testify here today. As you well know, the nation is on an unsustainable fiscal course, and substantial changes in policy will be needed to right the ship. As a number of bipartisan commission have recommended over the past year, policymakers should aim to stabilize the debt as a share of the economy (the Gross Domestic Product) so that the debt does not rise relentlessly as a share of the economy. Stabilizing the debt would put the nation on what economists define as a sustainable budget path. To stabilize the debt, budget deficits will need to be reduced to no more than about 3 percent of GDP.[1]

Policymakers should meet this goal in a reasonable period of time. But it isn’t necessary — or desirable — to meet it in the next few years. As Federal Reserve Chairman Bernanke noted last week, it would be unwise to put strong austerity measures into effect right away, while the economy is still growing too slowly to bring unemployment down to more normal levels. Putting substantial deficit-reduction measures into effect now would risk the loss of hundreds of thousands of jobs over the next year or two by slowing the already inadequate rate of economic growth. What policymakers really should do is to act in the weeks or months ahead to enact both temporary measures to strengthen the flagging recovery now and broader legislation that begins to take effect once the economy is stronger (probably in fiscal year 2013) and puts us on track to stabilize the debt as a share of GDP by the end of this decade. Doing so would involve tough choices, both substantively and politically, but would represent a huge accomplishment and allay fears in financial markets. As Chairman Bernanke cautioned, however, reducing the deficit more precipitously is neither necessary nor sound as policy.

In pursuing this goal, policymakers should follow a series of principles that would make deficit-reduction efforts both more equitable and more likely to be effective and sustainable over time. They also should avoid steps that would make deficit-reduction measures enacted now harder to sustain, and subsequent deficit-reduction legislation (which will clearly be needed) harder to enact, as explained later in this testimony. I would recommend that policymakers:

- Craft a deficit-reduction plan that is balanced and inclusive, affecting domestic programs, defense, and revenues alike. As explained below, to be effective in stabilizing the debt in the years ahead, deficit reduction likely will need to rely more heavily on revenue increases in the early years and more heavily on program savings — especially in health care programs — over the longer run. A substantial share of the new revenues should come from scaling back “tax expenditures,” the more than $1 trillion a year in tax breaks that the tax code provides each year for particular taxpayers or groups of taxpayers.

- Enact annual caps on funding for discretionary programs, but in the context of an overall deficit-reduction plan that includes increases in revenues and savings in mandatory programs. The caps should be reasonable and attainable, with separate caps for security and non-security discretionary programs and with a goal of splitting discretionary savings roughly 50-50 between those two categories, as the Bowles-Simpson Commission plan does.

- Recognize that, while the single largest spending contribution to deficit reduction over the long run must come from slowing the growth of health care costs system-wide (in both the public and private sectors), policymakers will not be able to secure big savings from federal health care programs over the next five to ten years without causing serious damage to the ability of Americans of modest means to have access to care. The health reform law includes most (although certainly not all) of the steps we know how to take now to slow health care cost growth without reducing health care quality or access to care or pushing more people into the ranks of the uninsured; going further now by just slashing Medicare and Medicaid would be ill-advised. Similarly, although steps to restore Social Security’s long-term solvency can contribute to deficit reduction in future decades, policymakers should not expect to reap significant savings from Social Security over the coming decade; there is broad bipartisan agreement that changes in benefits should not significantly affect anyone who is now at least 55 years old and that any changes in Social Security benefits and revenues should be phased in gradually.

- Meet the goal of reducing deficits to 3 percent of GDP over the coming decade through a combination of letting all of President Bush’s tax cuts expire on schedule at the end of 2012 or paying for those parts of the tax cuts that are extended, however politically unachievable that seems at the moment, and securing reasonable savings from discretionary programs, reforms in entitlement programs, and curbing unproductive tax breaks. Over time, a growing share of the public may conclude that alternatives that do not include letting the tax cuts expire would produce outcomes more undesirable than returning to the tax rates of the Clinton era (when the economy performed quite well).

- Avoid proposals such as those that would place a statutory cap on total annual federal spending or write a balanced budget requirement into the U.S. Constitution — either of which would diminish the government’s ability to respond effectively to recessions (and, in fact, would make recessions worse and probably more frequent) while largely or entirely shielding taxes (including spending done through the tax code) from deficit-reduction efforts.

- Avoid making the problems of poverty and inequality, both of which are higher in the United States than in most other Western industrialized nations, worse. Policymakers should adopt and adhere to the principle espoused in the Bowles-Simpson deficit-reduction plan to protect the disadvantaged and achieve deficit reduction in ways that don’t increase poverty or inequality. In late April, a group of Christian leaders — from the Catholic bishops to various evangelical leaders — called on policymakers to honor this principle and to draw a “Circle of Protection” around programs for the poor. This week a group of leaders of charities and nonprofit organization — including the heads of the United Way, Feeding America, and Independent Sector, as well as the nation’s leading civil rights organizations — added their voices to this call; a letter they issued on Monday takes note of the unusually high levels of poverty and inequality in the United States and states: “Any agreement on deficit reduction should neither cut low-income assistance programs directly nor subject these programs to cuts under automatic enforcement mechanisms.” Virtually all major deficit reduction or fiscal responsibility laws of the past quarter-century — the 1985 and 1987 Gramm-Rudman-Hollings laws, the 1990, 1993, and 1997 deficit-reduction packages, and the 2010 Pay-as-you-go law —abided by these principles.

A Basic Principle for Deficit Reduction

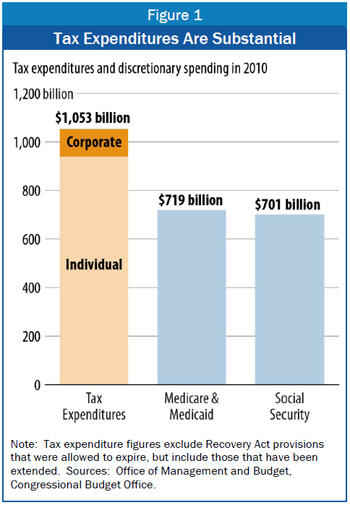

In 2010, the tax code included over $1 trillion a year in tax expenditures. This substantially exceeded the cost of Medicare and Medicaid combined ($719 billion), or Social Security ($701 billion), or non-security discretionary programs, which stood at $589 billion or a little over half the cost of tax expenditures. (See Figure 1.) Martin Feldstein, the Harvard economist who served as Chairman of President Ronald Reagan’s Council of Economic Advisers, wrote last summer that tax expenditures are the single largest source of wasteful and low-priority spending in the federal budget and should be the first place that policymakers go to restrain spending.

In my view, policymakers should aim for deficit-reduction packages that, over time, are split about 50-50 between outlay reductions (i.e., reductions in programs) and revenue increases, with much of the new revenues coming from scaling back tax expenditures. [2] This is the approach taken in the plan produced in November by the Bipartisan Policy Center commission co-chaired by former Senator Pete Domenici and former OMB director Alice Rivlin. As noted above and explained further below (and as former OMB Director Peter Orszag has explained in various venues), the mix probably should lean more heavily on revenue-raising measures than on budget cuts in the early years (achieved in substantial part by allowing the 2001 and 2003 tax cuts to expire) and more heavily on the expenditure side of the budget (especially in the health care area) than on revenues in future decades.

Caps on Discretionary Spending

To ensure that adequate, balanced deficit reduction is achieved, policymakers also need to avoid certain steps. For example, multi-year caps on discretionary spending will need to be part of a deficit-reduction package; enacting such caps on their own, separate from a larger deficit-reduction package that also includes measures to raise revenues and secure savings in mandatory programs, would likely prove ill-advised. Enacting multi-year caps by themselves would undercut broader deficit reduction in the future by making subsequent deficit reduction packages harder to pass. If policymakers who oppose raising any revenues for deficit reduction can secure sizeable cuts in discretionary programs through multi-year discretionary caps without those caps being part of a broader package that raises revenues as well, they will have much less incentive to subsequently agree to a larger, more inclusive package.

Consider, for example, what would have happened if the discretionary caps included in the 1990 bipartisan deficit-reduction package had been enacted on their own in 1989 — the 1990 package likely never would have been passed. President George H.W. Bush and Republican congressional leaders wouldn’t have agreed to the tax increases in the package if doing so hadn’t gotten them the discretionary caps in return, and Democratic congressional leaders wouldn’t have agreed to cuts in Medicare and other entitlements without the revenue increases. For the same reason, enacting multi-year caps now on their own would likely prove counterproductive to large-scale, long-term deficit reduction. Nor would it be likely to assure financial markets, which rightly understand that cuts in discretionary programs alone can’t yield the amount of deficit reduction that will be needed. In short, discretionary caps in isolation are not a step in the right direction, as they are likely to make it harder to subsequently secure the enactment of a large-scale deficit reduction package.

It also is important that multi-year discretionary caps instituted as part of a larger deficit-reduction package be set at reasonable, attainable levels. Because such caps come with no specifics regarding the actual cuts to be made (the specific cuts come when subsequent annual appropriation bills are enacted), it can be tempting for policymakers to set very severe caps that require overly deep cuts in discretionary programs in the years that follow. History shows that such an approach is self-defeating. In 1990 and 1993, Congress enacted multi-year discretionary caps as part of larger deficit-reduction packages and set the caps at levels that produced substantial savings but were reasonable and achievable. Those caps were adhered to, and the savings were realized. In 1997, however, policymakers gave in to the temptation to write caps into that year’s deficit-reduction legislation that would require deep discretionary cuts in order to show very large discretionary savings on paper. Cuts of that magnitude proved unsustainable, and subsequent Congresses — on a bipartisan basis — chose not to adhere to the caps. [3]

Another critical issue in fashioning multi-year caps on discretionary programs is to make sure that sizeable savings in both non-security and security programs are included, as the Bowles-Simpson, Rivlin-Domenici and Gang of Six plans would do. If this is done, there should be separate caps on security and non-security discretionary programs.

Finally, any caps should continue to carve out or “fence” appropriations for program integrity activities — funding that pays for itself a number of times over by improving revenue collections and reducing fraud or inappropriate costs in Medicare and disability programs. For example, last week CBO and the Joint Committee on Taxation concluded that the Administration’s plan to earmark $13 billion for tax enforcement over the next decade would generate an additional $42 billion in revenues over the same period. Every set of statutory caps on discretionary funding from 1990 on has included such carve-outs.[4] History teaches that without them, the added funding needed to generate many billions of deficit reduction simply does not materialize.

The Timing of Health Care Savings

In the long run, the single largest contribution to deficit reduction will need to come from slowing the rate of growth of health care costs throughout the U.S. health care system, in the public and private sectors alike. A slower rate of health care cost growth will produce substantial budgetary savings in areas ranging from Medicare and Medicaid to the tax exclusion for employer-based health coverage.

We need to recognize, however, that major savings are not likely to be achievable here in the next five or ten years. The recently enacted health reform law includes most of the steps we know how to take now to reduce expenditures in these areas; that is how the Affordable Care Act is able to produce modest deficit reduction even as it extends coverage to 34 million uninsured Americans. There are some further steps we can take now (in areas such as Medicare and Medicaid payments for pharmaceuticals and durable medical equipment), but the savings they produce are modest compared with the savings we’ll need over the long run. We will need to identify and institute ways to slow the growth of health care costs per beneficiary throughout the health care system.

For over 30 years, Medicare, Medicaid, and private-sector health care costs have generally grown at about the same rate per beneficiary, which shouldn’t be surprising since they all use the same doctors, hospitals, and medical procedures. (Over the past decade, Medicare and especially Medicaid costs per beneficiary actually have grown more slowly than private-sector health costs.) Trying to hold Medicare and Medicaid to much lower rates of cost growth than private-sector health care on a permanent basis would ultimately lead to either or both of two undesirable outcomes: 1) our health care system becomes more of a two-tier system, in which Medicaid and Medicare beneficiaries (except for those Medicare beneficiaries who can afford to buy ample supplemental coverage) are denied some needed treatments and medical advances that other Americans get, and health care is thus increasingly rationed on the basis of income; and 2) extensive cost shifting occurs from Medicare and Medicaid to private payers, with the result that costs for employer-based coverage and other private coverage go up substantially to cross-subsidize doctors and hospitals who are underpaid by Medicare and Medicaid.

To help address the need to slow systemwide cost growth, the Affordable Care Act contains an extensive array of demonstration projects, pilots, and research to test and identify cost-saving reforms in health care delivery and payment systems that could produce substantial savings throughout the health care system. (It also includes important mechanisms, including the Independent Payment Advisory Board, to help assure implementation of cost-saving reforms.) But these reforms will take time to identify, test, and then institute on a broad scale. There is a potential for large and growing savings here in future decades, and these efforts need to be nurtured and adequately funded so they can produce the needed results. But there’s not much prospect of large savings here in the coming decade.

Measures to restore long-term Social Security solvency also can make a contribution to deficit reduction in future decades, but here, too, significant savings will not be secured in the decade ahead. There is bipartisan agreement both that changes in Social Security benefits generally should not affect people now 55 and over and that changes in both Social Security benefits and taxes generally should be phased in gradually over a considerable period of time.

How to Address the Timing Problem

How then can sufficient savings be achieved in the coming decade to stabilize the debt as a share of the economy and thereby buy us time for the reforms — especially in health care delivery and payment systems — that are the most important component of longer-term deficit reduction? There is an answer to this question, which stands out when one examines recent analyses of the nation’s fiscal problems that the Congressional Budget Office has issued.[5]

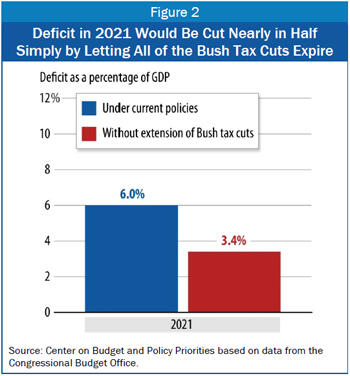

CBO reports show that if we continue on the current policy path (including extension of all of the current tax cuts, relief from the Alternative Minimum Tax, and relief from the scheduled deep cuts in Medicare physician fees), deficits will run close to 6 percent of GDP even after the economy recovers, reaching 6.0 percent of GDP in 2021 — and the debt will climb by 2021 close to 95 percent of GDP. [6]

To stabilize the debt, deficits need to be reduced to no more than about 3 percent of GDP. A combination of reasonable savings in discretionary programs, various entitlement reforms that can be put into effect in coming years (including some savings in Medicare that can be secured now), and the curbing of some unwarranted, inefficient, or low-priority tax expenditures — in conjunction with letting the Bush tax cuts expire after 2012, or paying for those elements of the tax cuts that policymakers wish to extend — would succeed in stabilizing the debt and achieving primary budget balance in the coming decade.

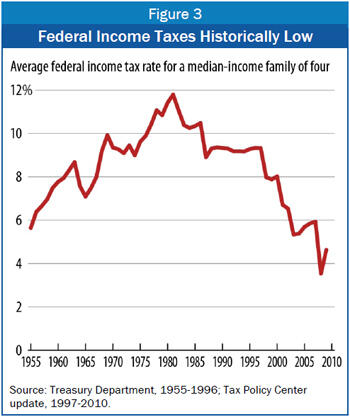

Federal taxes are now at historically low levels (see Figure 3). Needless to say, letting all the Bush tax cuts expire enjoys scant political support at the moment. Yet this is likely to be the only way to stabilize the debt as a share of the economy over the coming decade without draconian cuts that would cause serious damage — and that the public likely would not stand for and would eventually stop from taking full effect.

It is worth noting that revenue increases have been important ingredients of almost all of the major deficit-reduction packages enacted over the past 30 years, including those enacted in 1982, 1984, 1987, 1990, and 1993. Presidents and lawmakers of both parties have concluded that a mix of program cuts and revenue increases has been desirable (or acceptable) on policy grounds, and essential on political grounds to achieve major deficit-reduction success.

Unsound Measures That Should be Avoided

Some measures that have been proposed would, in my view, be ill-advised. These include proposals to place a statutory cap on total federal spending and proposals to write a balanced budget requirement into the U.S. Constitution. Many economists warn that such proposals would risk doing significant damage to the economy.

To be sure, proposals for a cap on total federal spending or a balanced budget amendment often contain mechanisms allowing the cap or the balanced budget requirement to be suspended upon the vote of a supermajority of both the House and Senate. But such supermajorities could prove impossible to obtain until long after the economy had begun to weaken; hard data on the economy come with a lag, and it could take many months after the economy has begun to weaken before sufficient data are available to convince three-fifths of both houses of Congress that economic conditions warrant waving the balanced budget requirement, if three-fifths could be convinced to waive the requirement at all. Moreover, a determined minority in the House or Senate could demand fiscally harmful measures — potentially including new, permanent tax cuts that increase deficits and ultimately necessitate even deeper budget cuts — as the price for their votes to waive the balance-budget rule in a recession.

Measures capping total federal spending at 20 percent or 21 percent of GDP (or lower) also are designed to serve another function: such proposals would largely or entirely shield revenues — including tax expenditures — from making any significant contribution to deficit reduction by focusing solely on the expenditure side of the budget. They are inconsistent with the goal of producing a balanced, equitable deficit-reduction package.

That this is the case is shown by a report issued in early 2010 by an expert committee on the deficit convened by the National Academy of Sciences, which outlined four possible paths to stabilize the debt. As panel co-chair and former Congressional Budget Office director Rudolph Penner explained, the panel designed paths at two “extremes” — one that achieved all of its deficit reduction by cutting programs and another that got nearly all of its deficit reduction by raising taxes — and two intermediate paths (which Penner and most other NAS panel members saw as more realistic) that blended program and tax changes. The extreme low-spending path — which got all of its deficit reduction by cutting programs, while including tax changes that would reduce revenues over the long run — included very deep cuts in Social Security, Medicare, and Medicaid, and cuts of about 20 percent inall other spending including defense, veterans’ programs, education, and the like. Under this extreme path, federal spending would be 21 percent of GDP.

Indeed, federal spending under President Ronald Reagan averaged 22 percent of GDP at a time when no baby boomers were retired and health care costs were more than one-third lower as a share of the economy than they are today. As Matt Miller, the commentator and former OMB official, has written, “As a matter of math, if you run the government at a smaller level than did Ronald Reagan while accommodating this massive increase in the number of seniors on our health and pension programs, you have to decimate the rest of the budget.”[7]

In short, measures like imposing a cap on total federal spending or trying to write fiscal policy into the Constitution are likely to do more harm than good. Such approaches also suffer from being devoid of any specific policy changes to actually achieve deficit reduction. There is no substitute for making the specific changes in discretionary and mandatory programs and the tax code that will move us to a sustainable fiscal course.

If policymakers cannot reach agreement now on enough specific policy changes to reach the goal of stabilizing the debt, they may elect to include some sort of automatic fiscal enforcement mechanism in a deficit-reduction package. If so, probably the best approach is to express any annual fiscal targets in terms of annual requirements for a specified dollar amount of annual deficit reduction. This is the “SAVEGO” concept that the Bipartisan Policy Center has recommended. Its advantage over annual debt or deficit targets is that it represents less dangerous economic policy. Under fixed debt or deficit targets, the amount of deficit reduction required in a given year goes up when the economy weakens and down when the economy strengthens — precisely the opposite of what sound economic policy entails. Under a SAVEGO-type approach, the amount of deficit reduction does not increase when the economy falters; neither does the amount of required deficit reduction diminish under a temporary boomlet or with rosy budget estimates.

Finally, it is essential that any automatic enforcement mechanism affect both spending and revenues. The goal of an automatic mechanism is not for it actually to be used to achieve deficit reduction. Just the reverse: the goal is for the deficit reduction measures that would be triggered automatically (if fiscal targets are missed) to be so unpalatable to both parties that the threat of these measures brings everyone to the table to work out deficit reduction packages, which then eliminates the need for the automatic deficit reduction measures to be used. To achieve this goal and get everyone to the table, the automatic mechanism must include both cuts in programs and increases in tax revenues (which could be realized through trims in tax expenditures, surtaxes, or other approaches).

A Key Principle: Deficit Reduction Should Not Increase Poverty or Inequality

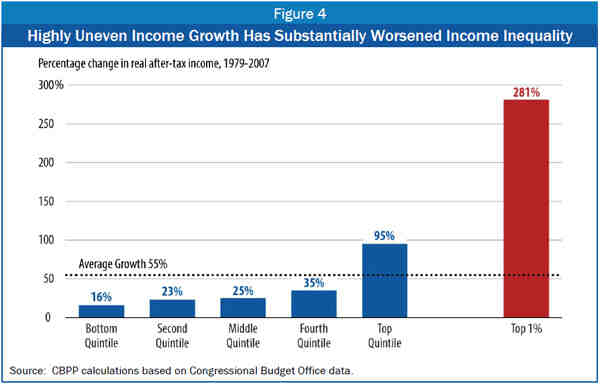

The United States has higher degrees of poverty and inequality than most other Western industrialized nations. Deficit reduction ought not to make these problems worse. (The United States also has more modest retirement benefits and larger burdens from out-of-pocket health costs than most other Western nations.) Erskine Bowles and Alan Simpson made the need to protect the disadvantaged and to avoid increasing poverty and inequality (see Figure 4) one of the fundamental principles of their commission’s work.

History shows this principle can be honored if there is a will to do so. The three major deficit-reduction packages of the last two decades — the 1990, 1993, and 1997 packages — all adhered to this principle. (In fact, all three of these packages reduced poverty and inequality even as they shrank deficits, as a result of their inclusion of increases in the Earned Income Tax Credit in the 1990 and 1993 packages and in food stamps in the 1993 package, and the creation of the Children's Health Insurance Program as part of the 1997 package.) This principle was also reflected in the Gramm-Rudman-Hollings law, the Budget Enforcement Act of 1990, and last year’s Pay-As-You-Go law — all of which exempted means-tested entitlement programs from the automatic across-the-board cuts triggered when deficit targets were missed or pay-as-you-go standards were violated.

End Notes

[1] The size of deficits that will stabilize the debt-to-GDP ratio depends on the starting level of debt, real economic growth, and real interest rates. Under projected circumstances, total deficits of about 3 percent of GDP starting in the middle of this decade would keep the debt from increasing relative to the size of the economy. Since interest payments are expected to total about 3 percent of GDP after the economy is back to normal, the primary budget would be roughly in balance if the total deficit is equal to 3 percent of GDP.

[2] For a further discussion of how tax expenditures can be reformed in ways that increase economic efficiency and improve tax progressivity while contributing to deficit reduction, see the testimony of Robert Greenstein, President, Center on Budget and Policy Priorities, before the Senate Budget Committee, March 9, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3426.

[3] The achievement of a balanced budget starting in 1998 made evading the caps almost inevitable, but many observers of the 1997 agreement believed that the caps were set so low that Congress and the President were unlikely to comply with them, whether or not the budget actually reached balance.

[4] Congressional Budget Office and Joint Committee on Taxation, “Additional Information on the Program Integrity Initiative for the Internal Revenue Service in the President’s Budgetary Proposals for Fiscal Year 2012,” June 23, 2011.

[5] Congressional Budget Office, The Economic and Budget Outlook: Fiscal Years 2011 to 2021, January 2011; An Analysis of the President’s Budgetary Proposals for Fiscal Year 2012, April 2011; CBO’s 2011 Long-Term Budget Outlook, June 2011

[6] These current-policy projections adjust the CBO March 2011 baseline to assume extension of expiring tax cuts, continuation of AMT relief, phasedown of operations in Iraq and Afghanistan, and a freeze in Medicare’s physician payment rates. For more explanation of the CBPP current-policy baseline, see the technical note in Kathy Ruffing and James R. Horney,Economic Downturn and Bush Policies Continue to Drive Large Projected Deficits, Center on Budget and Policy Priorities, May 10, 2011.

[7] Matt Miller, “A spending goal too small for aging America,” Washington Post, January 28, 2010.