The Same Old TABOR: Maine's "Taxpayer Bill of Rights" Proposal Fails To Fix Flaws of Colorado's TABOR

Summary

A ballot initiative proposal in Maine — “An Act to Create a Taxpayer Bill of Rights” — would impose tight limits on state expenditures that would shrink available public services such as education and health care in the same way that Colorado’s TABOR has led to a deterioration in that state.[1] Colorado has the strictest tax and expenditure limit (TEL) in the country: under its TABOR, the annual growth in Colorado’s state budget is limited to the rate of growth of state population plus an inflation factor.

- During the twelve years since TABOR was enacted in that state, there have been sharp reductions in basic public services such as health care, roads, K-12 education and higher education.

- The problems caused by TABOR led Coloradoans to approve in November 2005 a statewide measure to suspend TABOR’s population-growth-plus-inflation formula for five years in order to allow the state to restore a portion of its fundamental public services.

Despite the claims made by the Maine Policy Center and Mary Adams—authors and sponsor of the initiative respectively—that their proposal is a “new and improved version” of Colorado’s TABOR, the differences are minor.

- The Maine proposal still contains the central problem of Colorado’s TABOR: the population-growth-plus-inflation formula. Moreover, despite claims to the contrary, the Maine proposal fails to fix the TABOR “ratchet,” which makes it extremely difficult for state services ever to recover from an economic downturn. If the initiative were to be adopted in Maine, it would likely have the same negative impacts it did in Colorado.

- As in Colorado, Maine families might find themselves paying for educational activities, supplies, and even teachers the state could no longer afford under the limit; more Mainers would likely become uninsured; the possibility of public health emergencies would increase; and companies would find Maine a less hospitable place to do business as infrastructure and education deteriorated.

TABOR proponents in Maine claim a rigid TABOR limit is needed to fix what they claim is the state’s tendency toward excessive spending. But spending has not grown relative to residents’ incomes over the past more than a decade. In 2005, Maine General Fund expenditures equaled 6.81 percent of state personal income, down slightly from 6.95 percent of personal income in 1992.

Maine’s Proposed TABOR Preserves the Central Flaw of Colorado’s TABOR: the Population-Growth-Plus-Inflation Formula

Limiting state budget growth to a population-growth-plus-inflation formula shrinks public services over time and severely limits the state’s ability to respond to residents’ needs. Both elements of the formula hinder a state’s ability to provide a constant level of public services and prevent the state from meeting current and emerging needs.

Inflation

“Inflation” as commonly measured does not accurately reflect growth in the costs to government. The measure of inflation in the Maine TABOR initiative is the nationwide “Consumer Price Index-All Urban Consumers (CPI-U),” which is calculated by the U.S. Bureau of Labor Statistics. The CPI-U measures the change in the total cost of a “market basket” of goods and services purchased by a typical urban consumer. Since a typical urban consumer spends a majority of his or her income on housing, transportation, and food and beverages, those items are the primary drivers of the CPI-U. By contrast, Maine state government spends revenue primarily on education, health care, transportation, and corrections. In short, the market baskets of spending are entirely different.

Moreover, the “goods”— or public services— in Maine government’s basket (and in every other state’s) are in economic sectors that are less likely to reap the efficiency and productivity gains achieved by other sectors of the economy. For example, teachers can only teach so many students, and nurses can only care for so many patients. As a result, the costs of these public services are rising faster than the costs in other sectors. Indeed, the items in the “basket of goods” most heavily purchased by governments — such as health care, education, and prescription drugs — have seen significantly greater cost increases in the past decade than the items in the basket of goods purchased by consumers, and those faster-growing costs are expected to continue. Limiting the growth in government spending to a formula that uses the rate of growth in general inflation will not affect the level or growth of these costs; instead, it will affect the quantity and/or quality of public services the government is able to provide to its citizens.

Deterioration in Colorado

A growing body of evidence shows that Colorado’s Taxpayer Bill of Rights, or TABOR, has contributed to a significant decline in that state’s public services. Colorado voters recently chose to suspend TABOR for five years, in part to restore some of the service cuts induced by TABOR. These developments in Colorado have serious implications for the residents of Maine, because the proposed spending caps would lead to similar outcomes in Maine, as it did in Colorado.

The strict TABOR limits in Colorado have contributed to deterioration in the availability and quality of nearly all major government services.

- Since its enactment in 1992, TABOR contributed to declines in Colorado K-12 education funding. Under TABOR, Colorado declined from 35th to 49th in the nation in K-12 spending as a percentage of personal income. Colorado’s average per-pupil funding fell by more than $400 relative to the national average. And Colorado’s average teacher salary compared to average pay in other occupations declined from 30th to 50th in the nation.

- TABOR has played a major role in the significant cuts made in higher education funding. Under TABOR, higher education funding per resident student dropped by 31 percent after adjusting for inflation. College and university funding as a share of personal income declined from 35th to 48th in the nation. As a result, tuitions have risen. In the last four years, system-wide resident tuition increased by 21 percent after adjustment for inflation.

- TABOR has led to drops in funding for public health programs. Under TABOR, Colorado declined from 23rd to 48th in the nation in the percentage of pregnant women receiving adequate access to prenatal care, as defined by the federal Centers for Disease Control and Prevention. Colorado plummeted from 24th to 50th in the nation in the share of children receiving their full vaccinations. Only by investing additional funds in immunization programs was Colorado able to improve its ranking to 43rd in 2004. At one point, from April 2001 to October 2002, funding was so low that the state suspended its requirement that school children be fully vaccinated against diphtheria, tetanus, and pertussis (whooping cough) because Colorado, unlike other states, could not afford to buy the vaccine.

- TABOR has hindered Colorado’s ability to address the lack of medical insurance coverage for many children and adults in the state. Under TABOR, the share of low-income children lacking health insurance has doubled in Colorado, even as it has fallen in the nation as a whole. Colorado now ranks last among the 50 states on this measure. TABOR has also affected healthcare for adults. Colorado has fallen from 20th to 48th for the percentage of low-income non-elderly adults covered under health insurance. In 2002, Colorado ranked 49th in the nation in both the percentage of low-income non-elderly adults and low-income children covered by Medicaid.

Source: David Bradley and Karen Lyons, A Formula for Decline: Lessons from Colorado for States Considering TABOR, Center on Budget and Policy Priorities, October 2005. Available at: https://www.cbpp.org/10-19-05sfp.htm

Population

The second part of the population-growth-plus-inflation formula is inherently flawed as well. The subpopulations that state governments serve tend to grow more rapidly than the overall population used in the formula. An example is senior citizens, who already account for a disproportionately large share of Maine’s Medicaid costs. According to the U.S. Census Bureau, Maine’s total population is projected to increase by 11 percent from 2000 to 2030, while Maine’s population aged 65 and older is projected to more than double from 2000 to 2030.[2] As Maine’s elderly population begins to increase, so will the cost of providing the current level of health services and other types of services to them. The allowable state spending limit, though, would not accommodate this emerging need as it would be calculated using the much slower growing total population.

Changing Priorities and Shifting Costs

There is a further problem with the population-growth-plus-inflation formula. Even if existing services could be financed under the formula, the formula would be insufficient to allow for funding of new priorities that may be embraced by Maine’s citizens, such as reduced class sizes or more stringent corrections policies. It would also prohibit Maine from adopting current federal mandates that require states to spend more in areas such as security and education, or any future mandates that the federal government might enact. Lastly, it would not provide for sufficient emergency spending for natural disasters or other unanticipated problems.

The problems with the population-plus-inflation growth formula are described in more detail in a Center on Budget and Policy Priorities paper entitled The Flawed “Population Plus Inflation” Formula: Why TABOR’s Growth Formula Doesn’t Work. Available at https://www.cbpp.org/1-13-05sfp3.htm

It is also important to note that all programs in the Maine General Fund — not just those with cost pressures exceeding the population-growth-plus-inflation level — are threatened by a rigid population-growth-plus-inflation limit.[3] This is because under the Maine TABOR initiative, the population-plus-inflation limit would apply to the General Fund as a whole. So, if one spending area were to grow faster than the rate allowed under the limit (for instance due to cost pressure, court order, federal mandate or popular demand), then another spending area would have to grow at a slower pace — which would mean a reduced level of services in this second area.

In order to avoid such a situation, the state government might shift costs elsewhere. For example, state policymakers might decide to reduce state aid to local governments and school districts — requiring localities to pick up a greater share of the cost of education and local services. The expenditures of local governments and school districts, however, would also be limited by TABOR. Unless these local limits were successfully overridden at the ballot, school funding and other local services could face severe cuts.

The Reality of Spending in Maine

Advocates of TABOR in Maine claim that the state needs a strict spending limit because Maine’s government “has not only exceeded the growth of people’s ability to pay, it has also exceeded the growth of our economy.”[4] They further claim that TABOR “asks government to spend within its means and only spend what the current tax base can afford” and encourages “government spending to grow, but not faster than the economy can support.”[5]

There are two problems with these and similar statements. First, Maine’s spending is not growing faster than the economy. Second, TABOR goes far beyond curbing growth; it shrinks public services over time, requiring progressively more severe cuts each year.

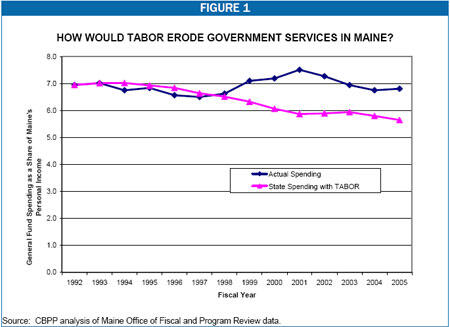

The spending problem TABOR proponents tout does not exist. Maine state spending has not been growing faster than the economy — as measured by the state’s total personal income. Comparing state spending to personal income is the best indicator of a state’s “means” because it measures the ability of the residents and businesses of the state to pay for government services.[6] In 1992, the year TABOR was introduced in Colorado, Maine General Fund spending was 6.95 percent of personal income; in 2005, it was 6.81 percent. Thus, relative to the ability of the state’s citizens to pay for government services, Maine’s spending has remained stable (See Figure 1).

It is the case, as can be seen in Figure 1, that there was an increase in expenditures relative to personal income between 1998 and 2001. But expenditures soon returned to their historical levels. Often particular needs or circumstances will temporarily raise a state’s level of spending, and then normal pressures of the business cycle combined with political expression will usually restore long-term balance. A rigid spending cap is not necessary for that restoration to occur.

TABOR would reduce spending relative to the state’s means, rather than keep it stable, and would require severe cuts in services. If state spending had been limited to changes in population plus inflation from 1992 to 2005, spending would have declined from 6.95 percent of personal income to 5.65 percent of personal income. The cumulative required spending cuts would have totaling $2.7 billion (See Figure 1). [7] In 2005 alone, the state would have had to cut $470 million, or 17 percent of actual expenditures, from its budget in order to adhere to the TABOR limit. Rather than forcing the state to “spend within its means” and grow with the economy, TABOR would have forced Maine to devote fewer and fewer of its resources to public services and to cut deeply into education, health care, public safety and other services on which Maine residents depend.

Maine’s TABOR Proposal Does Not Meaningfully Improve on Colorado’s Design

Proponents of the Maine initiative seek to distance themselves from the problems TABOR has caused in Colorado. Thus they claim that they have created “TABOR 2.0,” which improves on Colorado’s TABOR. As noted above, the fundamental problem with TABOR is the growth formula, which “TABOR 2.0” does not change. The other, smaller differences between “TABOR 2.0” and Colorado’s TABOR, such as the budget stabilization fund, will not make a meaningful difference in the operation of the limit.

A problem in Colorado’s TABOR as it was initially enacted was the “ratchet.” Colorado’s TABOR applied its population-growth-plus-inflation formula to the lower of two figures: actual revenues in the previous year, or the amount of revenues permitted by TABOR in that year. During the recession, revenues fell, and those reduced revenues became the base for calculating allowable revenue growth in all subsequent years. Colorado would have had to continue making deep reductions in public services even as the economy recovered and revenue collections returned to normal growth. Public services would have been cut even more deeply than would have occurred under the normal operation of the formula.

To avoid this problem, Coloradans in November 2005 enacted Referendum C, which suspends TABOR refunds for five years. It also permanently fixes the ratchet at the end of those five years by always applying the population-growth-plus-inflation formula to the previous year’s limit, rather than actual revenues.

Proponents of the Maine proposal claim to also have fixed the ratchet effect. But the proposal does not eliminate the ratchet. There are two differences between Colorado’s TABOR and Maine’s proposal. Maine’s proposal includes a budget stabilization fund “that would smooth out budget shortfalls in lean economic years.” [8] And Maine’s proposal is an expenditure limit, while Colorado’s TABOR is a revenue limit. Neither of these differences fixes the ratchet, and neither would lighten the long-term damage TABOR would do to the state.

Maine TABOR supporters claim that their proposal “creates a rainy day fund and forces state and local government to set aside a portion of surplus revenue in order to fund it.”[9] But Maine already has a budget stabilization fund (BSF), so TABOR would not create anything new. Indeed, the TABOR proposal would reduce the effectiveness of the current BSF by lowering the amount of funds it could hold and limiting the amount of annual year-end transfers it receives.

The “TABOR 2.0” budget stabilization fund would be capped at 10 percent of General Fund revenues from the previous fiscal year. To fill the BSF, it would require that 20 percent of the General Fund unappropriated surplus be transferred into it at the end of each fiscal year. [10] The existing budget stabilization fund, however, has a higher cap—12 percent of General Fund revenues from the previous fiscal year— and is funded by a year-end transfer of 32 percent of the unappropriated General Fund surplus. Thus, rather than creating a more adequate reserve fund for Maine, the TABOR proposal would weaken the existing budget stabilization fund and would leave Maine less equipped to deal with future revenue shortfalls.

This is of particular concern because the current, more generously funded BSF has proven inadequate in the past. For example, the cumulative shortfall in the Maine General Fund from 2001 to 2003 was $570 million, while the budget stabilization fund balance in 2001 was only $144 million — well short of allowing spending to maintain a constant level during the downturn.

A budget stabilization fund can — under the best of conditions — significantly alleviate the “ratchet effect” in a TABOR. [11] But Maine’s proposal is not designed to allow that to happen.

Under the Maine TABOR proposal, the population-growth-plus-inflation formula would apply to the previous year’s expenditures. Transfers from the budget stabilization fund would be allowed when revenues are insufficient to allow spending up to the TABOR limit. For example, suppose that the spending limit for FY 2010 was set at $2.5 billion, but that due to poor economic conditions, revenue came in only at $2.0 billion. A transfer would then be made from the BSF to the General Fund in an amount of $500 million, so the state could spend up to the limit in FY 2010.

These provisions do not fix the ratchet, however, because the transfers from the BSF are not counted in the base for calculating the next year’s limit.[12] The calculation for the 2011 limit would use the $2.0 billion, and not the $2.5 billion, as the base. So while the state would not face cuts of the same magnitude in 2010, the limit for 2011 would still be ratcheted down and major cuts would be required in that year. Since most state fiscal crises in recent years have lasted for at least two or three years, this design does not solve the problem it claims to solve. The ratchet would still exist.

Moreover, the ability to avoid budget cuts in the first year assumes that the budget stabilization fund would have the funds necessary to make up for the budget shortfall and that these funds would actually be used. Neither of these is necessarily true. Also as mentioned above, the new BSF in “TABOR 2.0” is actually smaller than the existing one, increasing the likelihood of insufficient funds.

Even if the BSF had sufficient funds to allow for spending up to the limit, there is no provision in Maine’s TABOR proposal that requires the funds be transferred to the General Fund for their use. Instead, the language reads “the Legislature may authorize transfers.” If the political will doesn’t exist to make these transfers, the existence of sufficient funds becomes a moot point.

Regardless of the details concerning the “fixes” Maine TABOR proponents claim to have made, they have not altered the core feature of Colorado’s TABOR that led to large declines in the quality and quantity of public services in Colorado — the population-growth-plus-inflation limit.

Conclusion

The proposed TABOR in Maine would significantly hinder the state’s ability to cope with unanticipated changes, initiate policy changes, accommodate voter and court mandates, or even maintain current service levels. Despite assertions that Maine’s TABOR is an improved version of Colorado’s TABOR, the Maine proposal retains TABOR’s central flaw — its formula. If the Maine TABOR proposal becomes law, the decline in the quality and amount of public services experienced in Colorado is likely to be experienced in Maine as well.

End Notes

[1] “An Act to Create a Taxpayer Bill of Rights” has qualified for the November 2006 ballot. Unlike Colorado's TABOR, Maine's proposal is statutory rather than constitutional. Maine does not permit constitutional amendments by initiative. Nevertheless, while legislators have the power to override an initiated bill it is politically difficult and risky to do so. Moreover, the proponents of the TABOR initiative in Maine have declared clearly their intention to use the initiative as only the first step toward persuading the next legislature to adopt a constitutional provision.

[2] U.S. Census Bureau, State Interim Population Projections by Age and Sex: 2004-2030, Table 4. Available at http://www.census.gov/population/projections/PressTab4.xls

[3] The Maine TABOR proposal requires expenditure limits to be calculated separately for the General Fund, Highway Fund, and Quasi-governmental agencies and Other Special Revenue funds, “for which separate individual limitations must be applied.” The General Fund is the largest of the funds subject to TABOR and funds a greater diversity of programs than the other funds.

[4] “TABOR Puts Taxpayers in Charge,” Bill Becker, Maine Heritage Policy Center, January 2006.

[5] Ibid and “Support Growth with TABOR 2.0,” Jason A. Fortin, Maine Heritage Policy Center, January 2006.

[6] The size of the “economy” is typically measured by Gross Domestic Product for the U.S. or by total personal income for individual states. State personal income is the sum of wage and salaries, proprietors’ income, rental income, personal dividend income, personal interest income, and personal current transfer receipts received by all individuals residing in a state. The measure is computed quarterly and annually by the U.S. Bureau of Economic Analysis.

[7] Spending data in Figure 1 is from the Maine State Legislature, Office of Fiscal and Program Review. To calculate state spending with a TABOR, the previous year’s allowable spending limit was multiplied by the sum of the percent growth in population plus inflation.

[8] Becker, “TABOR Puts Taxpayers in Charge,” ibid.

[9] Becker, “TABOR Puts Taxpayers in Charge,” ibid.

[10] The remaining surplus would be deposited into the “tax relief reserve fund,” which would provide rebates to taxpayers.

[11] There are two ways to fully eliminate the ratchet: 1) base each year’s spending limit on the prior year’s limit, rather than on actual expenditures in the prior year; or 2) require that the BSF contain enough money to fully offset any revenue shortfall, that any revenue shortfall be fully offset with funds from the BSF, and that the transfers be included in the base for calculating the next year’s limit. Meeting these criteria would be very difficult.

[12] An independent legal analysis by Richard Spencer from the law firm of Drummond, Woodsum, & MacMahon also concluded that transfers from the BSF fund would not be counted in calculating Maine’s expenditure limitation.

More from the Authors