The AMT's Growth Was Not "Unintended"

How the Administration and Congressional Leaders Anticipated the AMT Problem and Knowingly Made it Worse

Various Administration officials, senators, and House members are urging Congress to waive its Pay-As-You-Go rules and deficit-finance the Alternative Minimum Tax (AMT) “patch.” The AMT’s explosive growth, they argue, was unanticipated and unintended, and so measures to prevent that growth should not have to be paid for. Even if the AMT’s growth were unanticipated, this would not justify waiving PAYGO for AMT relief. But the claim is also false.

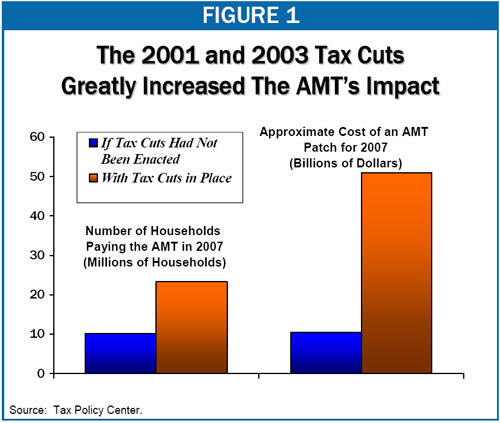

To the contrary, lawmakers not only anticipated the AMT’s explosive growth, they counted on it to mask the cost of the 2001 tax cuts. The Administration and congressional tax writers were well aware that the legislation they pushed in 2001 would force millions more taxpayers to pay the AMT, which would take back part or all of their tax cuts and thereby reduce the 2001 tax bill’s apparent cost. More than two thirds of the cost of this year’s AMT patch is due to actions taken by Congress and the Administration in designing the 2001 (and 2003) tax cuts (see Figure 1).

As Charles Grassley, then Chairman of the Senate Finance Committee, said in 2001, “President Bush’s plan [will] bring millions more Americans into the AMT process; the Joint Tax Committee estimates that the Bush tax plan will nearly double the number of American taxpayers affected by the AMT.”

(For more such comments from 2001, as well as some quite different recent comments by Senator Grassley and the Administration, see the box below.)

Were Congress to waive the Pay-As-You-Go rules now and deficit-finance the AMT patch, lawmakers would merely be rewarding the budget gimmickry of 2001.

Was the AMT’s Growth Unanticipated?

Now

Treasury Assistant Secretary for Tax Policy Eric Solomon, November 1, 2007:

“The Administration’s position is that the AMT is going to affect another 21 million taxpayers, and this was an unanticipated tax.”

Senator Charles Grassley, January 4, 2007:

“It’s ridiculous to rely on revenue that was never supposed to be collected in the first place… It’s unfair to raise taxes to repeal something with serious unintended consequences like the AMT.”

Then

Senator Charles Grassley, March 8, 2001:

“Roughly one in seven taxpayers will come under the shadow of the Alternative Minimum Tax by the end of the decade… That figure will significantly be higher if President Bush’s tax plan is adopted, and that is according to the Joint Tax Committee of the Congress.”

Senator Charles Grassley, February 28, 2001:

“In addition, President Bush’s plan [will] bring millions more Americans into the AMT process; the Joint Tax Committee estimates that the Bush tax plan will nearly double the number of American taxpayers affected by the AMT.”

Then-Treasury Secretary Paul O’Neill, February 13, 2001:

“The Treasury Department estimates that the Administration’s tax cut proposals would (1) increase tax receipts from the AMT by $262 billion over the 2002-2011 period, and (2) increase the number of taxpayers in 2011 who have additional tax liability because of the AMT from 20.4 million to 34.7 million.”

Treasury Department economist Jerry Tempalski, November 10, 2001:

“Before EGTRRA, the number of AMT taxpayers was expected to grow from 1.4 million in 2000 to 18.0 million in 2010… It is projected that EGTRRA will increase that number to 35.1 million in 2010…. EGTRRA will similarly increase AMT liability significantly… Before EGTRRA, AMT liability was expected to grow from $9 billion in 2000 to $45 billion in 2010… EGTRRA will increase AMT liability in 2010 to an estimated $133 billion…”

The AMT – A Gimmick Used to Help Enact the 2001 Tax Cut

If Congress had not enacted the 2001 and 2003 tax cuts, 10 million taxpayers would owe the AMT in 2007, according to estimates by the Urban Institute-Brookings Institution Tax Policy Center; reducing the number of affected taxpayers to several million, as the House-passed AMT “patch” bill would do, would have cost less than $15 billion.[1] But, with the 2001 and 2003 tax cuts in place, an estimated 23 million taxpayers will owe AMT in 2007, and reducing that figure to 2-3 million will cost $51 billion —more than three times as much.

That should not surprise congressional supporters of the 2001 tax cut, who knowingly used the AMT to mask the tax cut’s true cost. In the spring of 2001, when congressional leaders were formulating their tax cut package, they faced an obstacle. Congress’ budget resolution of that year allowed for tax cuts of up to $1.35 trillion over 10 years. But the combined cost of all the tax cuts that the Administration and the congressional leadership sought was much higher. Former Ways and Means Committee Chairman Bill Thomas described the “problem” as getting “a pound and a half of sugar into a one-pound bag.” [2]

To do so, Congressional tax writers resorted to various gimmicks. Among the largest was using the AMT to dramatically reduce the tax cut’s official cost.

Taxpayers owe the AMT when their tax liability is higher as calculated under the AMT than under the regular income tax. Therefore, substantially reducing households’ tax liability under the regular income tax without changing what they owe under the AMT subjects more households to the AMT — and increases the amount of revenue the AMT collects.

The Joint Committee on Taxation (JCT) explicitly brought this issue to Congress’s attention in the spring of 2001:

JCT provided lawmakers with various estimates of how the proposed tax cuts would dramatically increase the number of taxpayers hit by the AMT. One such estimate showed that the tax cuts would nearly double the number of AMT taxpayers by 2010.[3] As the box above illustrates, the Administration and congressional leaders were well aware of these estimates.

In addition, then-JCT Chief of Staff Lindy Paull testified before the Senate Finance Committee in April 2001, explaining, “Any of these proposals that reduce tax rates, without any adjustment to the Alternative Minimum Tax, are going to cause people to be subject to the Alternative Minimum Tax.”[4]

Congressional leaders could have acted on the information and used some of the $1.35 trillion available for the tax bill to modify the AMT so that it did not affect rapidly increasing numbers of households and so that taxpayers would receive the full value of whatever new tax cuts were enacted. But then they would have had fewer dollars to enact other tax cuts. So congressional leaders took advantage of the fact that, without a permanent AMT fix, the Joint Tax Committee would have to assume that the AMT would cancel a substantial portion of the new tax cuts of 2001. This assumption made the bill look much cheaper, allowing many more tax cuts to be squeezed in.

Waiving PAYGO Would Reward This Budget Gimmickry

Designers of the 2001 tax cuts used this maneuver with full confidence that Congress would come back in future years and enact AMT relief without paying for it. That is, they anticipated that they would ultimately get tax cuts costing far more than $1.35 trillion, while masking the true dimensions of the tax cut’s drain on the Treasury.

As noted above, more than two thirds of the cost of the 2007 AMT patch simply reflects the deferred cost of the 2001 (and 2003) tax cuts. Waiving PAYGO now on the grounds that the AMT’s growth was “unanticipated” would accept a false claim — that the growth of the AMT was not expected or intended — and would reward the budget gimmickry used in designing the 2001 and 2003 tax cuts.

[1] This estimate reflects what it would have cost to index the 2001 AMT exemption for inflation before the 2001 tax cut. Doing so would have reduced the number of AMT taxpayers in 2007 to 2-3 million, which is actually below the level the House-passed AMT patch bill would achieve.

[2] “News conference with Representative Bill Thomas, Chairman of the House Ways and Means Committee,” Federal News Service Transcript, March 15, 2001.

[3] Joint Committee on Taxation, “Estimated Revenue Effects of a Chairman’s Mark of the ‘Restoring Earnings to Lift Individuals and Empower Families (Relief) Act of 2001,’” JCX-41-01, May 11, 2001, http://www.house.gov/jct/x-41-01.pdf, page 8.

[4] “Tax Code Complexity: New Hope for Fresh Solutions,” Hearing Before the Committee on Finance, United States Senate, April 26, 2001.

End Notes

Sources:

“Mark-Up of H.R. 3996, The Temporary Tax Relief Act of 2007 and H.R. 3997, The Heroes Earnings Assistance and Relief Act of 2007,” Hearing Before the Committee on Ways and Means, United States House of Representatives, November 1, 2007; “Baucus, Grassley Tackle Alternative Minimum Tax Relief on First Day of 110th Congress,” Press Release, January 4, 2007; “Easing the Family Tax Burden,” Hearing Before the Committee on Finance, United States Senate, March 8, 2001; “Revenue Proposals and Tax Cuts in the President’s Budget,” Hearing Before the Committee on Finance, United States Senate, February 28, 2001; “President’s Tax Relief Proposals: Individual Income Tax Rates,” Hearing Before the Committee on Ways and Means, House of Representatives, February 13, 2001; Jerry Tempalski, “The Impact of the 2001 Tax Bill on the Individual AMT,” National Tax Association Proceedings: 94th Annual Conference on Taxation, November 10, 2001.

More from the Authors