Tax Foundation Figures Do Not Represent Middle-Income Tax Burdens

As in past years, the Tax Foundation has released a report projecting “Tax Freedom Day,” which it describes as the day when “Americans will finally have earned enough money to pay off their total tax bill for the year.” Over the years, pundits and policymakers often have misinterpreted the Tax Foundation’s report as reflecting the tax burdens that the broad swath of middle-income families must shoulder. In fact, however, according to data from authoritative sources such as the nonpartisan Congressional Budget Office, middle-income Americans pay significantly less in taxes as a share of their income than the Tax Foundation’s report implies.

In its latest report, the Tax Foundation finds that, since 2004, Tax Freedom Day is estimated to occur later in the year. It attributes this shift to “the rising tax payments that accompany economic growth,” rather than to changes in tax policies that have increased the tax burden. But the “rapid growth of the total tax burden” that the Tax Foundation highlights in its report paints a misleading picture of the tax burden faced by most Americans.

Under the Tax Foundation’s method, increased tax payments by high-income taxpayers appear to increase the taxes that “Americans” pay and thereby advances Tax Freedom Day to later in the year. Its methodology produces particularly sharp distortions when income gains are concentrated at the top of the income spectrum and there are large increases in capital gains income. These trends were pronounced in the late 1990s and may be occurring again since 2004.

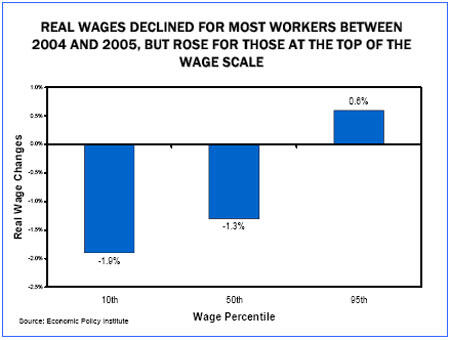

Tax Foundation President Scott Hodge explained its findings by noting that, as a result of the economic growth since 2003, “growing incomes are pushing people into higher tax brackets.”[1] Yet the phenomenon of higher incomes pushing people into higher tax brackets — often referred to as “bracket creep” — is not something that has affected most Americans. Although no official data on household income trends are available past 2004, it appears that wage and income growth during this economic recovery has so far flowed primarily to higher-income households. The Economic Policy Institute, for instance, finds that middle-income Americans saw inflation-adjusted wages fall between 2004 and 2005. Only high-wage workers saw their incomes rise (see figure). Further, the increase in capital gains realizations since 2003 has overwhelming benefited those at the top of the income spectrum, according to estimates of the Urban Institute-Brookings Institution Tax Policy Center. As a result, it is likely that income disparities in the nation have widened, continuing trends that have pushed income inequality to near-record levels.[2]

Under the progressive structure of the federal income tax, those with higher incomes face higher tax rates. As more of the nation’s income is concentrated in the hands of these high-income households, who pay income tax at a higher rate, then total income tax revenues rise relative to total income. So while the tax burden of those with higher incomes may have increased, commensurate with their growing incomes, households with lower incomes that have not seen their incomes rise during this recovery would not have experienced the increasing tax burdens highlighted by the Tax Foundation.

The Problems with the Methodology

In computing the nation’s tax burden,” the Tax Foundation divides what it says are total tax receipts by what it says is the total amount of income in the nation. The Tax Foundation method suffers from the following problems.

Average Tax Figure Is Misleading

Under our progressive tax system, high-income taxpayers pay significantly larger percentages of their income in federal income taxes than middle-income families do. Under the Tax Foundation methodology, the higher taxes that high-income taxpayers pay make the taxes that average Americans pay look considerably larger than they actually are.

Suppose four families with incomes of $50,000 each pay $2,500 in income tax — five percent of their income — while one wealthy family with $400,000 in income pays $80,000 in income tax, or 20 percent of its income. If one averages these figures, one finds that 15 percent of the total income of these five families goes to pay federal income taxes. (Dividing the families’ total tax payments of $90,000 by their total income of $600,000 shows that 15 percent of their total income is paid in income taxes.)

| Percentage of Income Paid in Federal Taxes | |||

|

| 1998 | 2000 | 2003 |

| Congressional Budget Office | 16.8% | 16.6% | 13.6% |

| Tax Foundation (average) | 22.4% | 23.1% | 18.7% |

| * CBO estimates for 1998-2003 are from “Historical Effective Federal Tax Rates: 1979 to 2003,” December 2005. | |||

Under the Tax Foundation methodology, this 15 percent figure would imply that the average family in this group pays 15 percent of its income in income taxes and must work until 15 percent of the year has passed to pay its income tax bill. Yet the 15 percent figure is highly misleading as an indicator of the typical tax burden of families in this group. The four moderate-income families in the group pay five percent of their income in income tax, or one-third of the average 15 percent rate.

Thus the Tax Foundation’s conclusions about federal tax burdens cannot be generalized and applied to typical Americans in the middle of the income spectrum. This can be seen when Tax Foundation’s findings are compared with estimates prepared by the Congressional Budget Office that look specifically at the tax burdens of middle-income families. For instance, in 2003 (the most recent year covered in the CBO analysis), CBO found that that the middle fifth of American households — those in the middle of the income spectrum — paid 13.6 percent of their income in federal taxes. In contrast, in its report from last year, the Tax Foundation estimated that the “average” American paid 18.7 percent of income in federal taxes in 2003. This is higher than what CBO found the middle fifth of households paid in federal taxes as a percentage of their income in 2000, before any of the Bush tax cuts were enacted.

The flaws in the Tax Foundation methods were particularly evident in the late 1990s and in 2000. During those years, the Tax Foundation showed that the tax burden was rising, while CBO showed that burdens for middle-income Americans were flat or declining (see table above). This divergence occurred because, during this period, those at the top of the income spectrum experienced significant income gains, resulting in higher income taxes, even as households in the middle of the income spectrum saw much more moderate income growth. The circumstances of households at the top influenced the Tax Foundation’s “average” figure, pushing it higher, even though it was not representative of the circumstances of middle-income households. This appears to be very similar to the current situation, where income gains concentrated at the top of the income spectrum appear to be driving the changes in the Tax Foundation’s estimates.

To be sure, an average figure similar to the one calculated by the Tax Foundation can yield some useful information. Revenues as a share of the economy (i.e., as a share of GDP) is one of the best indicators for assessing the amount of the nation’s income that is devoted to the public sector. The fundamental problem occurs when the mathematical average that the Tax Foundation calculates is used to refer to the normal or typical American, creating the impression that its figures represent the tax burdens of ordinary American families.

That the Tax Foundation reports create this misleading impression can be seen in the way that journalists present Tax Freedom Day. For instance, last year, ABC News explained that Tax Freedom Day is “the date when average Americans have earned enough money to pay their 2005 federal, state and local taxes (emphasis added).”[3] This year, the Connecticut Post reported that “the average American will have to work until April 26 to pay all their local, state and federal taxes”[4] Yet, as described above, the Tax Freedom Day calculation is highly inappropriate for assessing individual tax burdens and substantially exaggerates the burden that the typical American faces.

Greenspan Warns Against Seriously Flawed Approach Tax Foundation Uses

In a 2002 Congressional hearing, Federal Reserve Chairman Alan Greenspan warned that the type of approach the Tax Foundation uses — dividing total tax receipts by the Gross Domestic Product (or a similar measure), to determine the overall average tax rate (i.e., to determine the percentage of total income in the nation that is paid in taxes) — is simply not valid. Greenspan flatly stated: “you can't use tax receipts over nominal GDP as a tax rate."

Chairman Greenspan explained one reason that such an approach is improper: although capital gains taxes are counted as part of federal tax receipts, the capital gains income on which such taxes are paid is not counted in GDP. The Tax Foundation uses a closely related Commerce Department income measure — NNP, or Net National Product — that also omits capital gains income. Counting capital gains taxes as part of tax receipts, while failing to count as income the very capital gains income on which these taxes are paid, distorts — and inflates — average tax rates.

Misusing Available Data

The Tax Foundation often defends its methodology by emphasizing that it uses official data from the Commerce Department’s Bureau of Economic Analysis. The problems with the Tax Foundation approach are not with the underlying data, however, but rather with how the Tax Foundation uses these data and then presents the results.

For instance, Tax Foundation counts capital gains taxes in total taxes but excludes capital gains income as part of the total income. Former Federal Reserve Chairman Alan Greenspan stated in a Congressional hearing in 2002 that this is one of the reasons that the approach used by the Tax Foundation is not valid (see the box above).

The Tax Foundation also counts as taxes certain items that are not taxes. For instance, it includes Medicare premiums that older Americans elect to pay if they wish to receive coverage for physician’s services and prescription drugs under Medicare. These payments are not taxes.

Tax Levels versus Expenditures on Food, Clothing, and Medical Care

Finally, the Tax Foundation claims that families must pay more in taxes than they pay for food, clothing, and medical care combined. This Tax Foundation claim, which apparently compares total tax payments in the nation to total food, clothing, and medical care expenditures, is likely to create further misimpressions.

The Tax Foundation’s State-by-State Data Also Are Seriously Flawed

In past years, the Tax Foundation's reports have included a list of the dates described as representing “Tax Freedom Day” for each state. The serious flaws that mar the Tax Foundation's estimates of tax burdens nationally also plague its state-by-state estimates.

- About two-thirds of the tax burdens in the Tax Foundation calculations are federal tax burdens. The amount of federal taxes paid by the residents of a state thus has a large impact on that state’s “Tax Freedom Day.” Since, as this analysis explains, the Tax Foundation methodology substantially overstates the federal tax burden of middle-class families, the Tax-Freedom-Day figures for each state also substantially exaggerate the tax burdens of middle-class families in that state.

- Because the federal income tax system is progressive, states with relatively wealthy residents end up under the Tax Foundation’s methodology with a higher federal tax burden than other states. The fact that one state has higher-income residents than another state has nothing to do with the level of state and local taxes in the state. Yet by trumpeting state-level Tax Freedom Days that differ across the states, the Tax Foundation presentation is likely to lead to the misimpression that differences in burdens imposed by state and local taxes account for the differences across states in the Tax Foundation’s “average tax burden.”

- The Tax Foundation uses a procedure to allocate state corporate, severance, and tourism taxes based on the residence of the consumers who purchase products that businesses sell (adjusted for taxes that tourists pay). This is likely to lead to further misimpressions about the role of a state’s tax policies on the tax burdens its residents are said to face. For example, when Alaska collects taxes from oil companies based on the amount of oil they produce in the state, the Tax Foundation does not count those taxes as part of Alaska’s revenue. Rather, they add those taxes to the tax burden in the states where oil is consumed. Maine residents, for example, consume a significant amount of fuel and so get allocated a large share of these Alaska taxes. Yet state legislators in Maine cannot have much impact on the level of taxes that Alaska or other oil-producing states levy on oil.

Further, the Tax Foundation highlights the tax burden for the current calendar year, making its own estimates of the taxes that will be collected during the year in the thousands of state and local jurisdictions around the country. Despite presenting these estimates as definitive, they are in fact speculative projections that have often proven to be significantly off-target when the actual data on state and local taxes are subsequently collected and published by the Census Bureau. For example, the Tax Foundation’s 2002 report claimed that tax burdens had risen since 2000 in 38 states, that five states had lower tax burdens, and seven had no change. By 2005, the Tax Foundation had revised its 2002 estimates to show that only eight states (rather than 38) had higher tax burdens in 2002 than in 2000, while 39 had lower tax burdens and three had no change. And when the Census Bureau released its data for 2002, it found that only four states’ tax burdens had risen, while tax burdens in 43 states had fallen (burdens were unchanged in three states). In its reports, the Tax Foundation does not adequately acknowledge the possibility that its data may be erroneous, relying instead on the reader to recognize the approximate nature of the results. Nor does the Tax Foundation give prominent attention to the revisions it makes in subsequent years when its previous estimates prove to have been faulty.

As a result, the Tax Foundation’s proclamations of state Tax Freedom Days are misleading and do little to inform legitimate debates over levels of state and local taxes and the services that those taxes support.

* See Nicholas Johnson, Iris Lav, and Joseph Llobrera, “Tax Foundation Estimates of State and Local Tax Burdens Are Not Reliable,” Center on Budget and Policy Priorities, April 10, 2006.

Even if total tax payments exceed total expenditures for food, clothing and medical care, this says little about the relationship between taxes and spending for typical families. It is no doubt true that upper-income families pay more in taxes than they spend for these items. It also is true that low- and moderate-income families pay significantly less in taxes than they spend for such items; necessities consume most of their income.

The precise family income level at which taxes typically exceed expenditures for food, clothing and medical care is unclear. In discussing last year’s Tax Freedom Day report, however, Scott Hodge, President of the Tax Foundation, stated, “taxes are becoming the largest share of any household budget in America (emphasis added).”[5] Such comments reinforce the mistaken impression that the Tax Foundation’s estimates reflect ordinary American’s tax burdens.

Conclusion

Given its methodology, the Tax Foundation’s conclusions regarding the nation’s tax burden are not an accurate reflection of the tax burden facing a typical American in the middle of the income spectrum. Authoritative institutions that study tax burdens, such as the Congressional Budget Office and the Urban Institute-Brookings Institution Tax Policy Center, show that Tax Foundation’s estimates are higher than the tax burden that middle-income families face. Further, its latest estimates that show a rising tax burden in part reflect the income growth experienced by high-income households over the past few years, continuing long-standing trends in income inequality. It is these higher-income households who are likely paying more in taxes, commensurate with their higher incomes, not the typical American worker, whose wages have been stagnant or declining in recent years.

End Notes

[1] Tax Foundation, “America Celebrates Tax Freedom Day,” Press Release, April 12, 2006.

[2] Isaac Shapiro and Joel Friedman, “New CBO Data Indicate Growth in Long-Term Income Inequality,” Center on Budget and Policy Priorities, January 30, 2006.

[3] ABC News, “The Average American Will Work Until Mid-April to Pay Off His or Her Taxes,” April 11, 2005, http://abcnews.go.com/Business/Taxguide/story?id=652937&page=1

[4] Peter Urban, “State Taxpayers Hit Hardest In Country,” Connecticut Post, April 13, 2006.

[5] CNBC News Transcripts, Kudlow & Company, April 12, 2005.

More from the Authors