State Revenues and Services Remain Below Pre-Recession Levels

Despite recent reports of rapid state revenue growth and surpluses in some states, most states continue to feel the after-effects of the fiscal crisis. The spurt of current growth is occurring following several years of falling or stagnant revenues. During those years, states cut back on services, drew down rainy day funds, enacted temporary revenues, and used an array of fiscal gimmicks. As a result, state fiscal conditions today are weaker than they were before the last recession.

-

The current high revenue growth is taking place from a substantially depressed base; the rapid growth is more an indication that revenues have not yet returned to their normal levels than it is of strong fiscal conditions. State revenues remain below what would be required to support the pre-recession level of services states provided.

-

Analysis shows that state revenues would have to grow by more than 9 percent per year between now and 2008 in order to generate enough funds simply to restore the level of services that prevailed in fiscal year 2000, before the recession.

-

A budget “surplus” also can be a misleading indicator of whether or not a state’s fiscal situation is strong. Mid-year surpluses occur when revenues come in stronger than the state estimated when the budget was enacted. A state that at budget time cut important services in order to bring its expenditures into balance with what later turned out to be an overly-conservative revenue estimate would still show a mid-year surplus.

Revenues

State taxes have been growing at an annual rate in the range of seven to 11 percent since early 2004. Those rates are extraordinary, and likely unsustainable. Normally, state revenues may be expected to grow at an average annual rate of five percent to six percent.

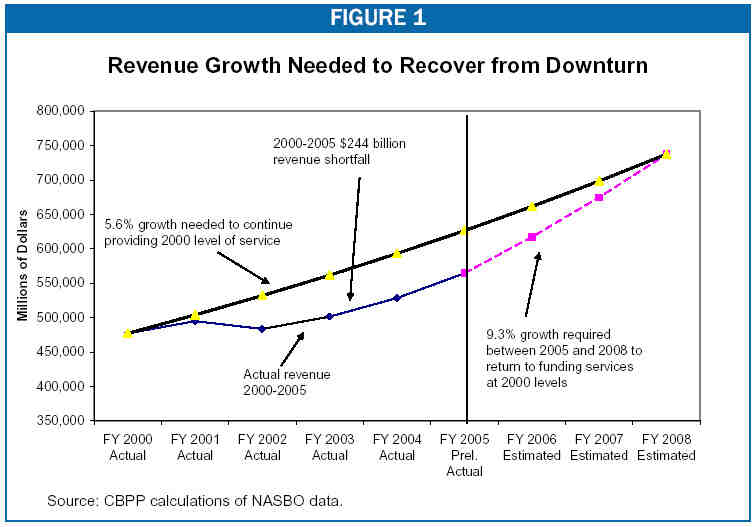

Figure 1 compares the revenues needed to sustain public services at their fiscal year 2000 level with actual revenues from 2000 to 2005 and projected revenues through 2008. The top line assumes that the cost of state government grows at approximately 5.6 percent a year. This growth rate is based on the average annual growth rate of state expenditures between 1989 and 1999. Historically, the 1990s were a period of modest growth in government, largely because health care costs did not grow especially fast that decade. Thus this is a conservative estimate; the actual revenue growth required to restore services in the current period is likely to be higher.

{kind=link}

Click image to enlarge

The bottom line shows revenues. As would be expected, revenues during the economic downturn dropped well below the level required to sustain expenditures. The bottom line of the graph shows actual general fund revenue collections for 2000-2005, which fell about $244 billion below the amount needed to continue funding services at the 2000 level.

Less expected, however, has been the length of time it has taken revenues to recover after the recession. The dotted bottom line shows the growth needed to return by 2008 to funding state services at the 2000 level. Due to the dramatic drop-off in revenue, states will need to experience average revenue growth of 9.3 percent in fiscal years 2006, 2007 and 2008 simply to make up the ground lost during the downturn.

Expenditures

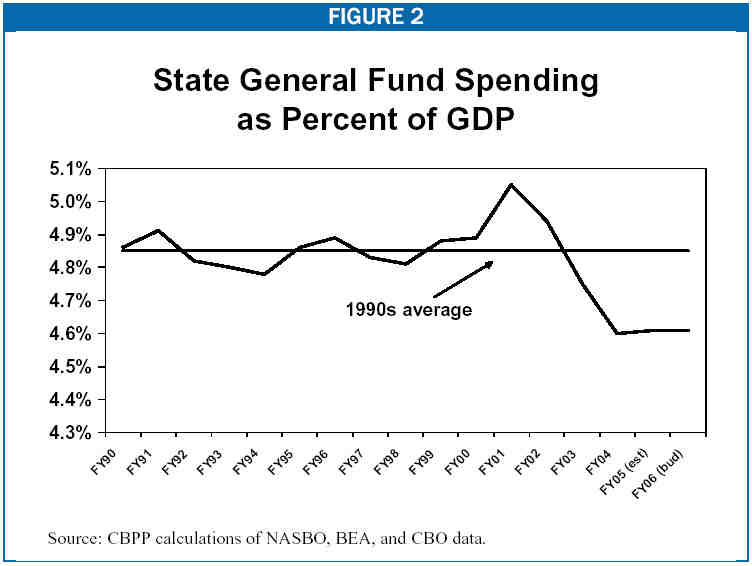

A similar picture emerges if the expenditure side of state budgets is examined. At the end of fiscal year FY 2005 (June 30, 2005 in most states) state spending as a share of the economy was at its lowest level in 15 years. Expenditures stood at 4.61 percent of GDP, well below the average during the 1990s of 4.85 percent of GDP.

{kind=link}

Click image to enlarge

A recent survey by the National Conference of State Legislatures of budgets adopted for fiscal year 2006 found that budgets are expected to grow by 5.7 percent on average. At this rate of growth, state budgets would remain flat as a share of GDP. Thus states will not yet be able to begin restoring the very substantial reductions in services that took place during the downturn and its aftermath.

Surpluses

A number of states have begun to report budget surpluses. Accounts of these surpluses often imply that such money is “extra” and thus potentially available for enactment of a new round of tax cuts. The concept of surplus, however, is misleading.

The mid-year surpluses that states are experiencing reflect only the difference between estimated and actual revenue collections. Understandably, states were cautious in their current budgets and assumed relatively low revenue growth. Because they are required to balance their budgets, they set their expenditure levels based on these overly-conservative revenue estimates — in some cases cutting services to reach balance. As revenues come in more strongly than estimated, the states are said to have a surplus. But a surplus does not mean that states have more money than they need to reverse recent service cuts, make progress toward restoring programs to pre-recession levels, or even to fund the ongoing costs of state programs as they stand in fiscal year 2006.

-

For example, California is one of the states that recently made news with large budget surpluses, but the press has mischaracterized the meaning of the surplus. The Legislative Analyst’s Office has found that while revenues are significantly higher than the estimates used in the fiscal year 2006 budget, the state continues to face operating deficits in the current budget (2005-06) and beyond — even if no existing programs are expanded and all of these unanticipated revenues are set aside and used to address future year budget gaps.

-

Revenues are coming in above forecasts in Minnesota as well. As of November 2005, the state increased its projection of the amount of general fund revenues expected by 2.3 percent. This would have resulted in a balance of $701 million at the end of the state’s two-year budget. The state needs these ‘surplus’ funds, however, to reverse a school aid payment shift that the state employed to balance its budget during the fiscal crisis. During the fiscal crisis, the state delayed some of its aid payments to school districts in order to achieve savings in its 2002- 2003 and 2004-2005 biennial budgets. The current budget requires that these payments be made on their original date if sufficient revenues became available. Undoing this shift improves the state’s fiscal situation in two ways. It will result in a budget with a better alignment between the state’s expenses and revenues and provides a cushion for future downturns by restoring the opportunity to delay this payment again if needed in the future.

States Have Not Restored the Majority of Budget Cuts Enacted During the Downturn

During the fiscal crisis states cut education, health and other programs.

For example, spending on elementary and secondary education did not kept up with inflation or enrollment increases. School districts in 35 states got less money per student, after adjustment for inflation, from state revenue in fiscal year 2004 than they did in fiscal year 2002. In 17 states, the declines exceeded five percent. *

State support for higher education was cut significantly; states budgeted 7 percent less on higher education for fiscal year 2005 compared to 2002 after adjusting for inflation.** One result of these higher education cuts is that average tuition and fees at public institutions are 35 percent higher than they were four years ago after adjustment for inflation.***

In addition, during the depths of the fiscal crisis, states made cuts to Medicaid and the Child Health Insurance Program that caused more than one million people to lose eligibility for health insurance coverage — much of which has not been restored.

* Andrew Reschovsky, The Impact of State Government Fiscal Crisis on Local Governments and Schools, Robert M. La Follette School of Public Affairs, University of Wisconsin-Madison, December 2003.

** CBPP calculations of data from the Center for the Study of Education Policy, Illinois State University, http://coe.ilstu.edu/grapevine/table4_05.htm.

*** The College Board, Trends in College Pricing 2004, Oct. 19, 2004.

In these and many other states, the reported surpluses mask operating deficits, unrestored service reductions, and other problems that have to be addressed before a state can be said to have fully recovered from the downturn.

More from the Authors

Areas of Expertise