State Taxes on Capital Gains

A historically large share of the nation’s wealth is concentrated in the hands of a few. As a result, millions of American families have less wealth, and therefore fewer opportunities, than they otherwise would. Further, since wealthy people are overwhelmingly white, this extreme wealth concentration reinforces barriers that make it harder for people of color to make gains. One way states can build more broadly shared prosperity is by strengthening their taxes on capital gains — the profits an investor realizes when selling an asset that has grown in value, such as shares of stock, mutual funds, real estate, or artwork.

One way states can build more broadly shared prosperity is by strengthening their taxes on capital gains — the profits an investor realizes when selling an asset that has grown in value, such as shares of stock, mutual funds, real estate, or artwork.

Most state and local tax systems are upside down: the wealthy pay a smaller share of their income in these taxes, on average, than low- and middle-income people do, even though they are best able to afford to pay more. Capital gains, which go overwhelmingly to the wealthiest households, receive special tax preferences, such as a partial exemption, in a number of states. States with such preferences should eliminate them. States also have several options to boost capital gains revenue to support investments that benefit the state as a whole.

How Are Capital Gains Taxed?

While the value of an asset can increase in each year that it is owned, the capital gain is taxed only when the asset is sold. For example, consider a taxpayer who bought 100 shares of stock for $10 each (total cost of $1,000) and sold them for $15 each (total value of $1,500). The increase in value of $500 is the amount of capital gains income “realized” by the taxpayer. If the sale occurs within a year of the purchase, these are considered short-term capital gains for tax purposes; if more than a year after purchase, they are considered long-term gains. Under current state and federal law, these capital gains are reported and taxed as income in the year that they are realized.

The amount of capital gains (and thus, the revenue generated by taxing them) varies by state, depending in large part on the state’s relative wealth. (See Table 1.)

Some States Have Tax Preferences for Capital Gains

The federal government taxes income generated by wealth, such as capital gains, at lower rates than wages and salaries from work. The highest-income taxpayers pay 40.8 percent on income from work but only 23.8 percent on capital gains and stock dividends.[1]

While most states tax income from investments and income from work at the same rate, nine states — Arizona, Arkansas, Hawaii, Montana, New Mexico, North Dakota, South Carolina, Vermont, and Wisconsin — tax all long-term capital gains less than ordinary income.[2] These tax breaks take different forms. Typically, these states allow taxpayers to exclude some or all of their capital gains income from their taxable income, but others levy a lower rate than the state tax on ordinary income or provide a credit equal to a percentage of the taxpayer’s capital gains. (See Table 2.) In addition, a handful of states (including Colorado, Idaho, Louisiana, and Oklahoma) provide breaks only for capital gains on investments in in-state businesses, and a few states target preferences to investments in specific industries, like farming in Iowa and Wisconsin.[3]

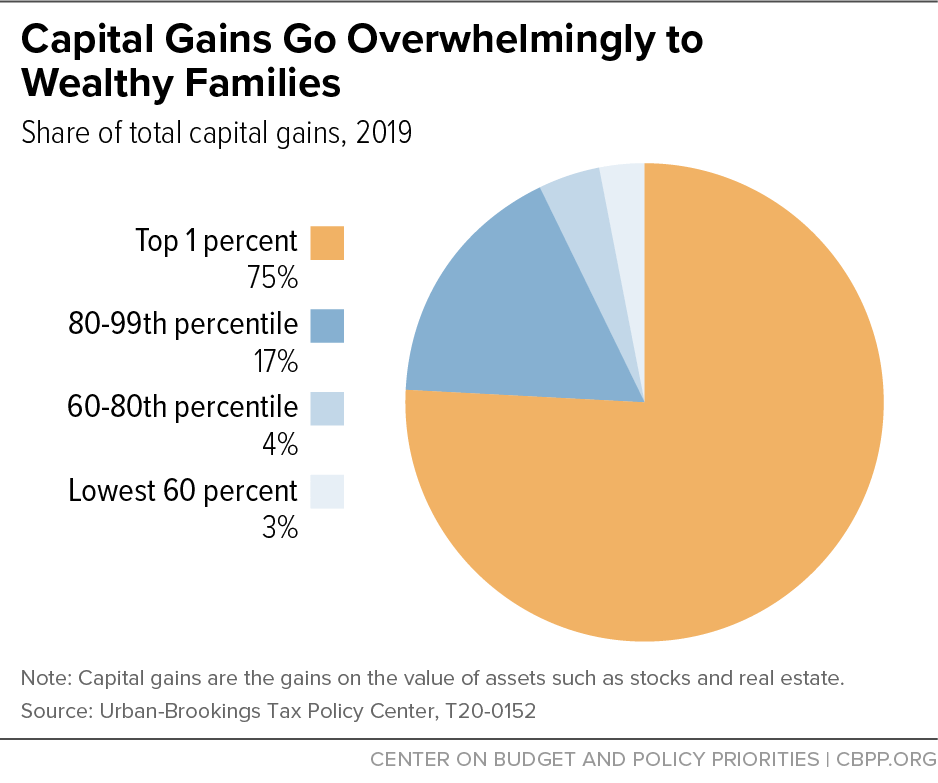

Capital Gains Go Overwhelmingly to Wealthy, White Households

Capital gains are generated by wealth. Because wealth is highly concentrated, so is capital gains income. About 85 percent of capital gains go to the wealthiest 5 percent of taxpayers; 75 percent go to the top 1 percent of taxpayers.[4] (See Figure 1.) Wealthy households are disproportionately white: white families are three times likelier than families of color to be in the top 1 percent.[5]

Capital Gains Tax Breaks Don’t Drive State Economic Growth

Proponents of capital gains tax breaks often argue that they spur economic growth by encouraging investment. But historically, “there is no obvious connection between tax rates on capital gains and economic growth” at the national level, tax policy expert Leonard Burman notes.[6] There is even less reason to expect a state tax break on capital gains to boost a state’s economy. The companies, bonds, and other assets generating capital gains for a state’s residents could be located anywhere in the country or the world, so any possible economic benefit wouldn’t necessarily go to the state giving the tax break.

Moreover, capital gains taxes generate revenue to support three major building blocks of thriving communities: K-12 and higher education, health care, and transportation. And, by increasing the share of state revenues paid by the wealthy, they allow states to keep taxes lower on people with moderate incomes, who spend (rather than save) a larger share of their incomes to boost local economies.

How to Address Volatility in Capital Gains

Capital gains income — and thus capital gains tax revenue — can rise or fall rapidly in response to economic changes. States can manage this volatility by, for example, relying on a variety of taxes, some of which respond less dramatically to swings in the business cycle.[7]

The best way to address volatility in capital gains and other taxes is to establish a rainy day fund and make deposits when strong economic growth boosts revenues, so these funds can smooth out revenue downturns.[8] States can tie these provisions directly to capital gains taxes, if desired. For example, Massachusetts deposits all capital gains revenue above a specific threshold ($1 billion) into its rainy day fund.[9] Similarly, in Connecticut, when income taxes collected through quarterly payments from taxpayers and at the time of filing (as opposed to those withheld during the year) exceed a specified threshold, the “surplus” is deposited into the state’s reserves. These are mainly taxes on investment income.[10]

States With Capital Gains Preferences Should Eliminate Them

States that tax capital gains income at a lower rate than wage, salary, and other ordinary income should eliminate this special treatment. Taxing capital gains at the same rate as ordinary income would mitigate the increase in wealth concentration and could raise significant revenues.

Eliminating capital gains preferences in the eight states that had them in 2011 would raise some $500 million per year, the Institute on Taxation and Economic Policy estimates.[11] Rhode Island’s elimination of its capital gains preference in 2010 brings in over $50 million in additional revenue per year.[12] Vermont and Wisconsin scaled back their preferences to raise revenue in the wake of the Great Recession.[13] New Mexico reduced, from 50 percent to 40 percent, the share of capital gains that are exempt from taxation in 2019.[14]

Only one state without an income tax (New Hampshire) currently taxes capital gains at all. Washington State recently enacted a tax on extraordinary profits from the sale of financial assets of over $250,000 per year, which will take effect in 2022.[15] The remaining non-income-tax states could levy a tax on just this type of income.

Ways to Boost State Revenues From Capital Gains

The remaining 41 states and the District of Columbia, which currently tax capital gains at the same rate as ordinary income, should resist cutting these taxes and instead raise them to generate revenue they can invest in broadly shared prosperity. They have several options:

Raise the capital gains income tax rate. States could simply levy a higher rate on capital gains income than on income from wages, salaries, and other sources, or raise the rate just on short-term capital gains.

Eliminate “stepped-up basis.” Under current state and federal law, people who inherit assets such as stocks, bonds, or real estate pay no taxes on any appreciation of those assets that occurred before they inherited them. (Technically, the value of those assets is “stepped up” from the original purchase price to their value on the date of inheritance.) As a result, a large share of capital gains is never taxed.

For example, consider a taxpayer who bought 100 shares of stock for $10 each and held them until their death, when the value had risen to $50 per share. They left them to their daughter, who sold them a number of years later, after the value had risen to $55 per share. Under current law, the daughter’s taxable capital gains would reflect the $5-per-share increase that occurred while she owned the stock, not the $45-per-share increase that occurred since their mother bought it.

State estate taxes used to help compensate for stepped-up basis by taxing assets at the time they were inherited. But most states no longer have an estate tax, and the tax thresholds in states that do have the tax are generally so high that very few estates owe it.[16]

Stepped-up basis primarily benefits the wealthiest families because they have the most unrealized capital gains. They can also afford to hold on to their assets until they die and pass them on to their heirs rather than use them to pay expenses in retirement. Families of color have lower savings than white families and are less likely to have pension income, therefore, they are less likely than white families to benefit from this tax break. Around two-thirds of Black and Latino working-age households own no assets in a retirement account, compared to 37 percent of white households.[17]

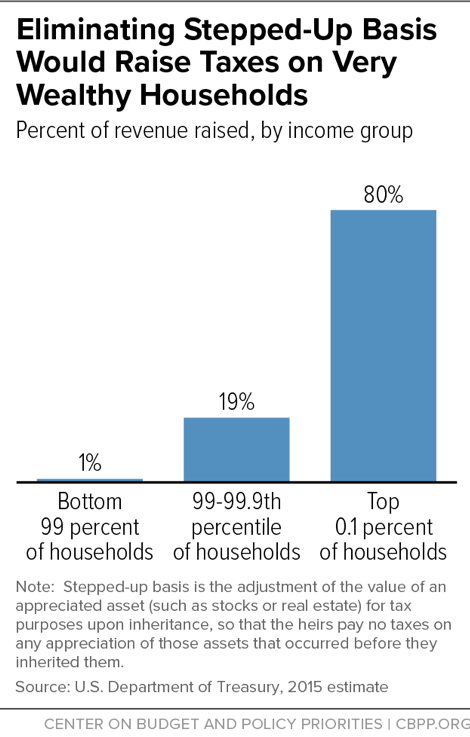

Eliminating stepped-up basis would result in taxation of the asset’s full increase in value since its original purchase. This would have a very progressive impact: 99 percent of the revenue from eliminating stepped-up basis would come from the top 1 percent of filers, and 80 percent would come from the top 0.1 percent, according to the Treasury Department.[18] (See Figure 2.)

Another way states could tax the full increase in value of capital assets is by taxing capital gains each year as they are earned, instead of waiting until the assets are sold. This would be relatively easy for assets like publicly traded stocks and bonds, but applying this type of tax to other assets, such as real estate, might prove unworkable due to the difficulty of estimating their annual increase in value.[19]

Close the “carried interest” loophole. Managers of private equity and hedge funds, many of whom are among the highest-income taxpayers in the country,[20] benefit from special treatment of a large share of their income. Typically, they receive both a management fee, or a percentage of the value of the assets they manage, and a performance fee, which equals a share of the gains they have generated for their clients. The latter is called carried interest.

The federal tax code taxes carried interest at the same rate as capital gains income rather than the higher rate imposed on ordinary income, even though carried interest is compensation for work the managers perform in managing the investments, not a return on capital of their own that they invested.

States could offset this federal tax preference and generate more capital gains revenue by levying a separate tax on carried interest. If an individual state imposed such a tax, fund managers could fairly easily move their businesses to evade it, so some states have formed regional compacts. For example, New Jersey lawmakers adopted a bill in 2017 to tax carried interest that would only take effect if neighboring states adopt a similar provision. Lawmakers in California, Connecticut, Illinois, Massachusetts, New York, and Rhode Island have also considered bills to tax carried interest.[21] State initiatives to tax carried interest would not only raise revenue directly but also encourage the federal government to eliminate this loophole by calling attention to the issue. Federal action would eliminate the problem of tax evasion by moving and would increase revenue for many states that link their definition of taxable income to the federal tax code.[22]

| TABLE 1 | ||||||

|---|---|---|---|---|---|---|

| Capital Gains as Share of Residents’ Total Adjusted Gross Income (AGI), by State | ||||||

| 2018 | Net Capital Gains | 2018 | Net Capital Gains | |||

| Millions | Percent of AGI | Millions | Percent of AGI | |||

| WY | $2,930 | 13.4% | GA | $20,151 | 6.5% | |

| NV | $14,241 | 13.4% | NE | $3,927 | 6.4% | |

| FL | $93,024 | 12.4% | MI | $19,702 | 6.2% | |

| MA | $35,525 | 10.3% | HI | $2,828 | 6.0% | |

| NY | $88,012 | 10.1% | NC | $18,540 | 6.0% | |

| CT | $17,678 | 9.9% | NJ | $24,379 | 6.0% | |

| CA | $154,271 | 9.5% | ME | $2,454 | 6.0% | |

| CO | $21,344 | 9.4% | OK | $6,135 | 6.0% | |

| SD | $2,589 | 9.1% | SC | $8,371 | 5.9% | |

| WA | $29,191 | 9.0% | VA | $19,302 | 5.9% | |

| MT | $2,671 | 8.4% | RI | $2,217 | 5.9% | |

| IL | $40,424 | 8.3% | MN | $12,605 | 5.8% | |

| DC | $2,966 | 8.0% | MO | $10,594 | 5.8% | |

| NH | $4,529 | 7.8% | ND | $1,507 | 5.7% | |

| TX | $71,991 | 7.8% | NM | $2,934 | 5.6% | |

| UT | $7,586 | 7.7% | WI | $11,045 | 5.6% | |

| VT | $1,628 | 7.7% | OH | $19,609 | 5.4% | |

| ID | $3,798 | 7.6% | IA | $5,139 | 5.3% | |

| AZ | $15,456 | 7.4% | MD | $12,948 | 5.2% | |

| AR | $5,527 | 7.3% | LA | $6,001 | 5.0% | |

| TN | $14,099 | 7.1% | DE | $1,626 | 4.9% | |

| OR | $10,030 | 7.1% | IN | $9,177 | 4.7% | |

| PR | $216 | 6.8% | AL | $5,545 | 4.5% | |

| PA | $30,349 | 6.7% | AK | $1,044 | 4.1% | |

| KY | $7,723 | 6.7% | MS | $2,385 | 3.8% | |

| KS | $6,157 | 6.7% | WV | $1,239 | 2.9% | |

| US | $924,693 | 8.0% | ||||

| TABLE 2 | |

|---|---|

| State Tax Preferences for Capital Gains | |

| Arizona | Only 75% of capital gains are taxed |

| Arkansas | Only 50% of capital gains are taxed |

| Hawai‘i | Capital gains are taxed at 7.2%, lower than rate for ordinary income of up to 11% |

| Montana | Credit of 2% of capital gains |

| New Mexico | Deduction of 50% of capital gains or up to $1,000, whichever is greater |

| North Dakota | 40% of capital gains are excluded from taxation |

| South Carolina | 44% of capital gains are excluded from taxation |

| Vermont | 40% of gains from certain assets held more than three years or up to $5,000 of capital gains are excluded from taxation |

| Wisconsin | 30% of capital gains (60% for farms) are excluded from taxation |

End Notes

[1] The 23.8 percent figure includes the top tax rate on capital gains plus the 3.8 percent tax on investment income for high-income taxpayers, which helps fund the Affordable Care Act’s health coverage expansions.

[2] Marco Guzman, “State Taxation of Capital Gains: The Folly of Tax Cuts & Case for Proactive Reforms,” Institute on Taxation and Economic Policy, September 2020, https://itep.sfo2.digitaloceanspaces.com/092520-State-Taxation-of-Capital-Gains_ITEP.pdf.

[3] The legality of limiting capital gains tax reductions to in-state investments has been questioned, as it may violate the U.S. Constitution’s interstate commerce clause.

[4] Tax Policy Center, T18-0231 - Distribution of Long-Term Capital Gains and Qualified Dividends by Cash Income Percentile, 2018, November 16, 2018, https://www.taxpolicycenter.org/model-estimates/distribution-individual-income-tax-long-term-capital-gains-and-qualified-30.

[5] “[W]hile 1.2 percent of White families earn enough to place them among the top 1 percent of earners, just 0.4 percent of Latino and Black families are members of this group.” Meg Wiehe et al., “Race, Wealth, and Taxes,” Institute on Taxation and Economic Policy and Prosperity Now, https://prosperitynow.org/sites/default/files/resources/ITEP-Prosperity_Now-Race_Wealth_and_Taxes-FULL%20REPORT-FINAL_5.pdf.

[6] Chye-Ching Huang, “The Myth That Low Capital Gains Rates Are Very Important to the Economy,” Center on Budget and Policy Priorities, September 20, 2012, https://www.cbpp.org/blog/the-myth-that-low-capital-gains-rates-are-very-important-to-the-economy.

[7] Elizabeth McNichol, “Strategies to Address the State Tax Volatility Problem,” Center on Budget and Policy Priorities, Center on Budget and Policy Priorities, April 18, 2013, https://www.cbpp.org/research/strategies-to-address-the-state-tax-volatility-problem.

[8] Pew, “Rainy Day Funds: Best Practices to Mitigate Revenue Volatility,” June 7, 2017, https://www.pewtrusts.org/en/research-and-analysis/articles/2017/06/rainy-day-funds-best-practices-to-mitigate-revenue-volatility. Elizabeth McNichol and Ed Lazere, “States Should Improve the Design of Their Rainy Day Funds,” Center on Budget and Policy Priorities, June 3, 2021, https://www.cbpp.org/research/state-budget-and-tax/states-should-improve-the-design-of-their-rainy-day-funds.

[9] Massachusetts General Laws Chapter 29, Section 5G, https://malegislature.gov/Laws/GeneralLaws/PartI/TitleIII/Chapter29/Section5G.

[10] Connecticut’s “volatility cap” requires that all income tax revenue collected when taxpayers file their tax returns that exceeds a specific threshold ($3.15 billion in 2017) be deposited in the state’s rainy day fund. The income tax revenue collected at the time of filing is called “estimates and finals,” as distinguished from the income taxes withheld during the year. See http://www.ctvoices.org/blog?page=1#volcap.

[11] Institute on Taxation and Economic Policy, “A Capital Idea: Repealing State Tax Breaks for Capital Gains Would ease Budget Woes and Improve Tax Fairness,” January 2011, https://itep.org/wp-content/uploads/capitalidea0111.pdf.

[12] Institute on Taxation and Economic Policy estimate, November 2018.

[13] Guzman.

[14] Erica Williams, “New Mexico Investing in Children, Advancing Equity,” Center on Budget and Policy Priorities, April 16, 2019, https://www.cbpp.org/blog/new-mexico-investing-in-children-advancing-equity.

[15] Washington State Budget & Policy Center, “Lawmakers act to balance state tax code by passing capital gains tax,” April 24, 2021, https://budgetandpolicy.org/schmudget/lawmakers-act-to-balance-state-tax-code-by-passing-capital-gains-tax/.

[16] Center on Budget and Policy Priorities, “2017 Tax Law Weakens Estate Tax, Benefiting Wealthiest and Expanding Avoidance Opportunities,” June 1, 2018, https://www.cbpp.org/research/federal-tax/2017-tax-law-weakens-estate-tax-benefiting-wealthiest-and-expanding-avoidance; Elizabeth McNichol, “State Estate Taxes: A Key Tool for Broad Prosperity,” Center on Budget and Policy Priorities, May 11, 2016, https://www.cbpp.org/research/state-budget-and-tax/state-estate-taxes-a-key-tool-for-broad-prosperity.

[17] Nari Rhee, “Race and Retirement Insecurity in the United States,” National Institute on Retirement Security, December 2013, https://www.nirsonline.org/reports/race-and-retirement-insecurity-in-the-united-states/.

[18] Lily Batchelder, “The ‘silver spoon’ tax: how to strengthen wealth transfer taxation,” Washington Center for Equitable Growth, October 31, 2016, https://equitablegrowth.org/silver-spoon-tax/.

[19] Washington Center for Equitable Growth, “Taxing Capital: Paths to a fairer and broader U.S. tax system,” Section 3, August 10, 2016, https://equitablegrowth.org/research-paper/taxing-capital/?longform=true.

[20] Ashley Adams-Mott, “How Much Do Hedge Fund Managers Make?” Chron, updated August 27, 2018, https://work.chron.com/much-hedge-fund-managers-make-23556.html.

[21] PwC, “Recent carried interest proposals in New Jersey, Rhode Island and Illinois,” January 2018.

[22] States with income differ in how they conform to the federal tax code. This Federation of Tax Administrators table summarizes those connections: https://www.taxadmin.org/assets/docs/Research/Rates/stg_pts.pdf.

More from the Authors