Stalled Proposal to Cut Estate Tax Further Is Deeply Flawed and Should Not Be Revived

Reportedly Uses Gimmicks to Mask True Costs

A proposal that several senators were developing — before negotiations stalled this week — to cut the estate tax beyond the generous parameters in place in 2009 was deeply flawed, relying on two budget gimmicks to mask its unaffordable cost.

“The details [of the proposal] are pretty well resolved,” the leading Republican participant, Senator Jon Kyl (R-AZ), announced on May 11, before the negotiations halted, at least for the time being, apparently as a result of a lack of agreement over how and when to move the proposal in the Senate. [1] The senators with whom Kyl was working included Max Baucus (D-MT) and Charles Grassley (R-IA), chairman and ranking Republican on the Senate Finance Committee, respectively, and Blanche Lincoln (D-AR). All four have supported repealing the estate tax in the past.

The shelved proposal closely mirrors an earlier proposal from Senators Lincoln and Kyl to shrink the estate tax beyond the 2009 parameters. The main difference between the Lincoln-Kyl proposal and the shelved proposal apparently is the two budget gimmicks described below.

In 2001, President Bush and Congress cut the estate tax so that by 2009, the value of estates exempt from taxation rose to $3.5 million for individuals and effectively $7 million for couples, up from $1 million for individuals and $2 million for couples scheduled under prior law, and the marginal tax rate on the value of an estate above these thresholds fell from 55 percent to 45 percent. As a result, by 2009, a tax that previously affected only the largest 2 percent of estates in the country touched only the largest one-quarter of 1 percent of estates. Due to the peculiarities of the 2001 law, the estate tax expired this year but is scheduled to return next year under the rules set by the pre-2001 law, unless Congress acts.

President Obama has proposed making the already-generous estate tax parameters of 2009 permanent, at a cost of $253 billion over the next decade compared to current law. He also has proposed offsetting $24 billion of that cost, by closing some loopholes within the estate tax, bringing the net cost to $229 billion. The actual impact on the deficit would be greater, since this figure does not include the higher interest payments on the debt that would result from the deficit-financing of these measures.

The shelved proposal from the group of senators would go further and cost considerably more. It reportedly would raise the exemption level to $5 million for individuals and $10 million for couples and cut the tax rate on the value of estates above those thresholds to 35 percent. That would cost at least $60 billion more over ten years than making the 2009 rules permanent, despite soaring federal budget deficits. Moreover, the larger the estate, the greater the tax cut for wealthy heirs would be.

Senator Kyl said last week that the shelved proposal would comply with congressional pay-as-you-go (PAYGO) rules by offsetting the costs of reducing the estate tax beyond the 2009 parameters.[2] Reportedly, however, the proposal accomplished this through two classic budget gimmicks that reduce its costs within the ten-year “budget window” to which PAYGO applies, but do not reduce (and, in fact, even increase) its long-term costs, which are the true test of a measure’s fiscal responsibility. The reported gimmicks are:

- The higher exemption level and lower tax rate would be phased in over the coming decade rather than provided up front, thereby lowering the bill’s cost in the first ten years without reducing its cost after that. In that way, the legislation resembles a bill that Rep. Shelly Berkley introduced in the House last year.

- A wealthy individual would be enticed to “prepay” his or her estate taxes now at a discounted rate, rather than have his or her estate pay the taxes upon the individual’s death. That would generate revenue for the federal government in the short run but cost the government even more revenue in the long run, because it would push into the next ten years taxes that would have been paid in subsequent decades at a higher rate.

With these two gimmicks (and likely some other offsets), the proposal might be scored as having no higher cost over the first ten years than extending the tax at its 2009 level. (Alternatively, according to some reports, the proposal might, as a result of the gimmicks, have a ten-year cost equal to the combined cost of extending the 2009 parameters and indexing the 2009 exemption levels.) But even if that is the case, the proposal would cost considerably more in subsequent decades, enlarging deficits and the debt precisely in the periods when they are already projected to reach unsustainable levels that pose risks for the U.S. economy.

Moreover, even in the absence of such gimmicks, cutting the tax beyond the 2009 parameters is neither necessary nor prudent. Enacting the 2009 parameters alone is quite expensive. Congress should focus instead on eliminating estate tax loopholes or including a surtax on estates in excess of $20 million (or some other such amount) to mitigate this cost.

Furthermore, such a cut in the estate tax is not needed to protect small businesses and farms, nearly all of which already are exempt under the 2009 rules. Only 110 small business and farm estates in the nation would owe any estate tax in 2011 under the 2009 rules, according to the Urban Institute-Brookings Institution Tax Policy Center, and virtually none would have to be sold to pay the tax. [3] While small businesses and farms are often used as “poster children” for cutting the estate tax further, they would gain little from doing so.

Finally, the shelved proposal reportedly included another “offset” that could squeeze state revenues that support education, public safety, and other vital services.[4] That provision would end the federal deduction that taxpayers can take for their state-level estate and inheritance tax payments. If wealthy taxpayers can no longer deduct those state-level taxes, they almost certainly will pressure state lawmakers to reduce or repeal the taxes, thereby draining state revenues and exacerbating state budget problems. [5]

Background

In 2001, President Bush and Congress phased out the estate tax as part of major tax-cut legislation. Between 2001 and 2009, the amount of an estate’s value that is entirely exempt from the tax was more than tripled, while the top marginal rate was cut by about one-fifth. Whereas about 98 percent of estates were fully exempt from the estate tax in 2001, more than 99.7 percent of estates were entirely tax-free by 2009.

In addition, because of the exemption level and other special tax breaks built into estate tax law, taxable estates pay less than 20 percent of their value in taxes under the 2009 parameters, well below the top marginal rate of 45 percent.[6] It also should be noted that much of the value of large estates consists of unrealized capital gains that have never been taxed. [7]

The estate tax disappeared entirely in January 2010, but if Congress does not act this year, the pre-2001 estate tax law will return next year, with a $1 million per-person exemption and a top marginal tax rate of 55 percent.

Last December, the House passed a bill sponsored by Rep. Earl Pomeroy that would have made permanent the exemption of $3.5 million per person (effectively $7 million per couple) and the 45 percent rate that were in effect in 2009.[8] But estate tax opponents have blocked action in the Senate.

Fiscal Conditions Have Deteriorated Sharply Since 2001 Tax Cut

The country’s fiscal circumstances have dramatically reversed during the decade since policymakers last made major changes in the estate tax. Massive deficits have replaced record surpluses. The revenue loss from the shrinking of the estate tax contributed to this fiscal reversal.

Congress is likely to face wrenching budget decisions in coming years to keep deficits and debt from growing to unsustainable levels over time. The President’s 2011 budget proposes a three-year freeze on overall non-security discretionary spending, which funds programs such as education, health research, and law enforcement, among many others. Some policymakers, analysts, and pundits are discussing significant changes in Social Security and Medicare, and the President’s recently appointed fiscal commission has begun to explore ways to rein in long-term deficits. It is in this context that the future of the estate tax must be considered.

Even Extending 2009 Estate Tax Rules Would Be Costly

President Obama has proposed making the 2009 estate tax rules permanent. This would lock in all of the estate tax cuts implemented between 2002 and 2009: the exemption level would be $3.5 million per individual and, effectively, $7 million per couple, and the top marginal rate would be 45 percent. As analysis by the Tax Policy Center has shown, taxable estates would pay an average of less than 20 percent of their value in tax.

This proposal is more than reasonable from the perspective of the wealthiest estates. A wealthy couple with two children could pass on a trust fund worth $3.5 million per child entirely tax free when the couple dies. This is more money than a middle-class family making $70,000 a year would make in a lifetime, and the middle-class family would pay taxes on that income every year. Furthermore, the wealthy couple could give additional sums to its children as tax-free gifts each year while the couple is still alive.

The cost of the President’s proposal would be large: $253 billion over the next decade. The President has proposed $24 billion in estate tax loophole-closers to offset a modest part of the cost.[9] Until negotiations stalled this week, however, a group of senators had been moving in the opposite fiscal direction, developing a proposal that would cost significantly more over time than extending the generous 2009 rules.

Repeal Advocates Working on Proposal to Shrink Tax Further

Proponents of repealing the estate tax entirely, having failed to gain the necessary support in Congress, have since advanced various proposals to eliminate as much of the tax as is politically possible. Last April, Senators Lincoln and Kyl introduced a plan to raise the exemption to $5 million for an individual and $10 million per couple (indexed for inflation) and lower the rate to 35 percent. Over the ten-year budget window, the proposal would cost about $130 billion more than making the 2009 rules permanent — and about $380 billion more than allowing the tax to return to its level under the pre-2001 law, based on estimates from the Joint Committee on Taxation. All of the approximately $130 billion in tax-cut benefits would go to the wealthiest one-quarter of 1 percent of estates (i.e., the largest one out of every 400 estates).

| TABLE 1: | ||

| Year | Tax-Free Per-Person Exemption | Tax Rate |

| 2009 | $3,500,000 | 45% |

| 2010 | $3,650,000 | 44% |

| 2011 | $3,800,000 | 43% |

| 2012 | $3,950,000 | 42% |

| 2013 | $4,100,000 | 41% |

| 2014 | $4,250,000 | 40% |

| 2015 | $4,400,000 | 39% |

| 2016 | $4,550,000 | 38% |

| 2017 | $4,700,000 | 37% |

| 2018 | $4,850,000 | 36% |

| 2019 and thereafter | $5,000,000 | 35% |

In recent weeks, a group of senators who have supported estate tax repeal in the past — including Senators Kyl, Baucus, Grassley, and Lincoln — worked to develop a modified version of the Lincoln-Kyl proposal, until that emerging deal stalled this week. [10] The new proposal reportedly cost $60 to $80 billion more over the first ten years than making the 2009 rules permanent. The senators apparently were contemplating two budget gimmicks that would shrink the plan’s cost’s in the ten-year budget window without reducing — and in fact, while likely increasing — its cost in subsequent decades. Their proposal was also reportedly designed to include a provision that would likely exacerbate state budget problems, as described later in this report.

Gimmick #1: Slow Phase-In

Legislation that follows the Berkley bill’s phase-in path would cost about $320 billion over the next ten years — around $60 billion less than Lincoln-Kyl but about $60 billion more than making the 2009 rules permanent.[12] But this estimate does not reflect the Berkley plan’s true cost, because the proposal would not fully phase in until the tenth year. The proposal’s true cost impact would be felt only in future decades, which conveniently lie outside the ten-year budget window for which the Joint Committee on Taxation provides cost estimates.

Yet it is precisely in those future decades that the nation’s fiscal situation will become grave. Virtually every fiscal analyst across the political spectrum regards the nation’s long-term fiscal path as unsustainable, with our fiscal problems growing significantly worse over time and with an increasing risk to the economy with each passing decade.[13]

By 2019, the year that the estate tax cuts in the Berkley proposal would reach their full dimensions, annual interest on the debt is expected to exceed $800 billion — about as much as the projected cost of Medicare and far more than total appropriations for all non-defense discretionary programs in that year. Over the long run, the Berkley proposal would have the same detrimental fiscal effects as Lincoln-Kyl. Accordingly, it ultimately would either necessitate larger tax increases on middle-class families or steeper cutbacks in important federal programs (or both) than otherwise would be needed, or it would compromise economic growth to a still greater degree by adding to already-unsustainable deficits and debt.

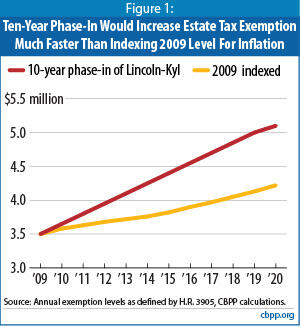

It may be noted that during the Berkley plan’s ten-year phase-in period, the estate tax exemption would grow twice as fast as if the 2009 exemption of $3.5 million were indexed for inflation and would become more costly as a result (see Figure 1). Under CBO’s economic projections, a $3.5 million exemption indexed for inflation after 2009 would not reach $5 million until 2029.

Gimmick #2: Timing Shift

Reportedly, the senators developing the shelved proposal were also seriously considering a provision that would raise revenue within the ten-year budget window but lose revenue in subsequent years — a “timing shift.” While details are unavailable, press reports indicate that the provision would give wealthy people the option of setting up a “prepayment” trust, paying a lesser amount of estate tax now, and eliminating all estate tax obligations on their estates when they die. This option would be worth the most to the very largest estates.

For example, if the top estate tax rate were reduced over time to 35 percent, wealthy elderly individuals could put their assets into a trust and pay an alternative tax on those assets at a still-lower marginal rate, possibly receiving a five or ten percentage point discount. The assets in the trust would then be transferred to heirs tax free when the individuals died.

The revenue generated by these “prepayments” would reduce the proposal’s overall cost in the first ten years. But the provision would increase revenue losses in subsequent decades, for two reasons: first, the added revenue in the first ten years would constitute revenue that otherwise would have been collected in subsequent decades but was accelerated into the first ten years in order to reduce the scored cost of the legislation. Second, those who chose to take advantage of this option would pay tax at a lower rate.

In addition, as with all proposals to reduce the tax rate used in the estate tax, the provision would confer the largest tax cuts on the biggest estates. The greater the value of an estate, the larger the size of the tax cut that this option would provide, because the lower tax rate would apply to a larger amount of assets.[14]

Considered together, the two likely gimmicks would shrink the cost of an estate tax cut within the budget window while increasing its cost outside the budget window, when deficits already are projected to be at or approaching dangerous levels.

Virtually No Small Businesses or Farms Would Benefit from Further Estate Tax Cuts

Some lawmakers argue that shrinking the estate tax below its already-modest 2009 level is necessary to protect small businesses and farms. This claim is without foundation, however, for the simple reason that nearly all small farms and businesses are already exempt from the estate tax under the 2009 parameters.

A Tax Policy Center analysis of a proposal similar to the Lincoln-Kyl proposal found that less than one quarter of 1 percent of its cost, relative to making the 2009 rules permanent, would go for tax cuts for estates that consist primarily of small businesses or farms.

In addition, Tax Policy Center estimates show that if policymakers extend the 2009 rules, only 110 small business and farm estates in the entire nation would owe any estate tax in 2011 and thus would benefit from weakening the tax beyond its 2009 level.

Moreover, virtually none of the few small business and farm estates that would owe any tax would have to be liquidated to pay it. A Congressional Budget Office study found that all but a handful of the farm estates that would owe any tax under the 2009 parameters would have sufficient liquid assets on hand (such as bank accounts, stocks, and bonds) to pay the tax without having to touch the farm or business.a And those very few small business and farm estates that might conceivably face a liquidity problem would have other options — such as spreading their payments over a 14-year period — that would allow them to pay the tax without selling off any of the business or farm assets.

In 2001, when the estate tax affected many more estates and had a substantially higher effective rate than it does today, the American Farm Bureau Federation acknowledged to the New York Times that it could not cite a single example of a farm having to be sold to pay estate taxes.

a Congressional Budget Office, “Effects of the Federal Estate Tax on Farms and Small Businesses,” July 2005.

b David Cay Johnston, “Talk of Lost Farms Reflects Muddle of Estate Tax Debate,” New York Times, April 8, 2001.

Possible Elimination of Deduction Could Harm State Budgets

In addition, the senators developing the shelved proposal reportedly contemplated eliminating the federal deduction for state estate taxes paid. The Berkley proposal contained this provision, which would reduce the proposal’s overall cost — but at the expense of exacerbating states’ serious budget problems.

If wealthy taxpayers who face state estate or inheritance taxes no longer can get a federal deduction against those taxes, they almost certainly will pressure state lawmakers to reduce or repeal those taxes. Loss of the federal deduction would lead to charges of unfair double taxation, because the federal estate tax would be leveled on a portion of estates that had already been taxed away at the state level.

Endangering these state revenues is particularly ill-advised, given states’ troubled fiscal outlooks. State estate and inheritance taxes are an important revenue source for the 21 states that levy them, bringing in approximately $4.5 billion per year. Most of these dollars are deposited in state general funds, which principally pay for education, health care, and public safety. Protecting these funds is always important, and is particularly so now: the worst recession since the 1930s has caused the steepest decline in state tax receipts on record. As a result, even after making deep cuts in education, health care, human services, and aid to local governments — and raising taxes in more than 30 states — states continue to face large budget gaps.

For that reason, states may not be in a position to repeal their estate or inheritance taxes immediately. But if this provision is enacted, then once state budgets begin to recover from the recession, states may face the choice of restoring deep cuts they were forced to institute in K-12 education, higher education, public safety and other basic services — or eliminating or reducing their estate or inheritance taxes.

End Notes

[1] Jay Heflin, “Kyl: Deal on the estate tax in the offing,” The Hill’s On The Money blog, May 11, 2010, http://thehill.com/blogs/on-the-money/domestic-taxes/97239-kyl-deal-on-the-estate-tax-in-the-offing . After the negotiations stalled, Senator Baucus said “there’s no agreement on the estate tax, neither on substance nor on process.” Martin Vaughan, “US Senate Effort to Reduce Estate Tax Hits Turbulence,” Dow Jones Newswires, May 18, 2010.

[2] Jay Heflin, “Kyl: Deal on the estate tax in the offing,” The Hill’s On The Money blog, May 11, 2010, http://thehill.com/blogs/on-the-money/domestic-taxes/97239-kyl-deal-on-the-estate-tax-in-the-offing .

[3] 2 See Tax Policy Center, “$3.5 Million Exemption and 45 Percent Rate: Distribution of Gross Estate and Net Estate Tax by Size of Gross Estate, 2011,” October 6, 2009, http://www.taxpolicycenter.org/numbers/displayatab.cfm?Docid=2473&DocTypeID=7 . We follow the Tax Policy Center definition of a small business or farm estate as one in which more than half of the value of the estate is in a farm or business and the farm or business assets are valued at up to $5 million.

[4] Martin Vaughan, “US Senate Effort to Reduce Estate Tax Hits Turbulence,” Dow Jones Newswires, May 18, 2010.

[5] Elizabeth McNichol, “Stalled Estate Tax Proposal Could Threaten State Revenues That Support Education, Public Safety, and Other Key Services,” Center on Budget and Policy Priorities, May 20, 2010.

[6] According to the Tax Policy Center, taxable estates would pay an average effective tax rate of 18.9 percent in 2011 if the 2009 estate tax rules were made permanent. In other words, the taxes they pay would equal 18.9 percent of the estates’ value, on average.

[7] According to a 2000 study, unrealized capital gains comprise 56 percent of the value of estates worth more than $10 million. See James Poterba and Scott Weisbenner, “The Distributional Burden of Taxing Estates and Unrealized Capital Gains At the Time of Death,” NBER, July 2000, p. 19.

[8] The Joint Committee on Taxation estimated that the bill, H.R. 4154, would cost $234 billion over 2010-2019. This cost would be higher in the current ten-year budget window, as it would include revenue losses in 2020. JCT has estimated that an identical proposal would cost $253 billion over the current budget window.

[9] The largest of these would tighten the rules governing valuation discounts for assets, saving $18.7 billion over ten years. Another would require that assets be valued consistently for transfer (i.e., estate and gift) and income (capital gains) tax purposes, saving $2.1 billion. A third provision would restrict Grantor Retained Annuity Trusts, which allow some assets to escape estate and gift taxation altogether, saving $3 billion.

[10] For instance, Richard Rubin, “Revenue-Raising Offsets Seen as Bridge for Gap Between Estate Tax Bills,” CQ Today, May 10, 2010.

[11] Peter Cohn, “Although Still Priority, Estate Tax Fix Deadlines Uncertain,” Congress Daily AM, April 27, 2010.

[12] Tax Policy Center, “Revenue Impact of Various Estate Tax Reform Proposals, 2010-2019,” October 27, 2009, http://www.taxpolicycenter.org/numbers/displayatab.cfm?Docid=2491&DocTypeID=5 .

[13] See Kathy Ruffing, Kris Cox, and James Horney, “The Right Target: Stabilize the Federal Debt,” Center on Budget and Policy Priorities, January 12, 2010.

[14] The windfall that the prepayment option would confer on very large estates could be even greater, depending on how the prepayment tax is structured. It is possible that the tax would apply only to the portion of assets placed in the trust that consists of unrealized capital gains. (That is, if an asset purchase for $100 had appreciated to $150 at the time the decedent placed it in the trust, the tax would apply only to the $50 of appreciation, not the asset’s full $150 value.) Either way, the tax would only apply to the asset’s value at the time it was placed in the trust; if the asset’s value further appreciated before the transfer of the estate, that appreciation would be totally untaxed unless the heir later sold the asset, in which case it would be taxed at the regular (lower) capital gains rate. Under the regular estate tax, in contrast, the estate would pay tax on the full value of the asset at the time the estate was transferred to the heirs.

For a discussion by Tax Policy Center analysts of additional problems this proposal raises, including its complexity (which likely would lead to more resources being consumed by estate-tax planning), see Bob Williams, “An Estate Tax Deal: Pay Now, Die Later,” the Tax Policy Center’s TaxVox blog, May 19, 2010, http://taxvox.taxpolicycenter.org/blog/_archives/2010/5/19/4532511.html.

More from the Authors