Ryan Plan Makes Deep Cuts in Social Security

A new analysis by Social Security’s chief actuary of several possible changes to the program allows one to calculate the size of the benefit reductions that Rep. Paul Ryan’s (R-WI) budget plan would generate. Those cuts are very deep. By 2080, the initial benefit of a medium earner (someone earning $43,000 in today’s terms) would be 39 percent below the currently scheduled amount, the benefit of a higher earner (earning $69,000) would be 51 percent lower, and the benefit of someone who earns the maximum taxable amount (currently $106,800) would be 58 percent lower.

The Roadmap for America’s Future, which Rep Ryan — the ranking Republican on the House Budget Committee — released in late January, calls for a radical redistribution of resources from the broad majority of Americans to the nation’s wealthiest individuals. [1] It provides the largest tax cuts in history for the wealthy, raises taxes on the middle class, ends guaranteed Medicare benefits, erodes health care coverage, partially privatizes Social Security, and makes deep cuts in guaranteed Social Security benefits.[2] This paper explains the full dimension of the cuts in Social Security, using information from the actuary's new analysis.[3]

By way of background, it is important to keep in mind some key facts about Social Security. Social Security benefits are modest; the average Social Security retirement benefit is $1,172 a month, or about $14,000 a year. Most elderly beneficiaries rely on Social Security for a majority of their income. And as traditional pensions become less common, Social Security will be the only defined-benefit, inflation-protected source of retirement income that most people will have.

Starting from this modest base, Rep. Ryan’s Social Security plan would cut benefits for future retirees significantly in two ways: (1) reducing benefits for the top 70 percent of wage earners through price-indexing the benefit formula, and (2) reducing benefits at all earnings levels by further increasing Social Security’s full retirement age.

The first element is price indexing. Under current law, Social Security benefits for new retirees are designed to keep pace with the growth of average wages. Under Rep. Ryan’s plan, initial benefits for 70 percent of earners would instead be related to the growth in prices, which in the long run grow less rapidly than wages.

Rep. Ryan’s indexing proposal imposes the greatest reductions on those with the highest earnings, and it exempts those with the very lowest earnings, so it is sometimes called “progressive” price indexing. Nonetheless, it would affect fully 70 percent of all Social Security beneficiaries — everyone with earnings above $22,000 in today’s terms. Over time, price indexing would turn Social Security into a program that provides only a small retirement benefit — and one that is largely unrelated to prior earnings.

The second benefit reduction is an increase in Social Security’s full retirement age. The full retirement age was 65, is now 66, and will reach 67 for people born in 1960 and later. Rep. Ryan’s plan would accelerate the increase to 67 and would index the full retirement age to life expectancy thereafter. As a result, the full retirement age would reach 68 for people born around 1983 and higher ages for later cohorts. As shown in Table 1, an increase in the full retirement age amounts to an across-the-board cut in benefits. A one-year increase in the full retirement age is equivalent to a roughly 7 percent cut in benefits for a person retiring at any given age, whether a person retires at age 62 or works to age 70 and does not begin drawing benefits until then.

| TABLE 1: Increasing Full Retirement Age Cuts Monthly Benefits Across the Board | |||

| Age at Claiming Benefits | Monthly Benefit of Illustrative Worker | ||

| Full Retirement Age of 65 | Full Retirement Age of 66 | Full Retirement Age of 67 | |

| 62 | $800 | $750 | $700 |

| 63 | 867 | 800 | 750 |

| 64 | 933 | 867 | 800 |

| 65 | 1,000 | 933 | 867 |

| 66 | 1,080 | 1,000 | 933 |

| 67 | 1,160 | 1,080 | 1,000 |

| 68 | 1,240 | 1,160 | 1,080 |

| 69 | 1,320 | 1,240 | 1,160 |

| 70 | 1,400 | 1,320 | 1,240 |

| Note: Assumes Delayed Retirement Credit of 8% a year and Primary Insurance Amount of $1,000. Source: CBPP Calculations | |||

The effects of these two benefit cuts — price indexing and increasing the full retirement age — would be cumulative. Table 2 shows how a medium earner (someone earning $43,000 in today’s terms) would be affected by Rep. Ryan’s plan. By 2080, a retiring medium earner’s benefit would be 39 percent below the currently scheduled amount and 46 percent below today’s wage-indexed level. (The difference between the two figures represents the impact of the increase in the full retirement age that is already scheduled in law.)

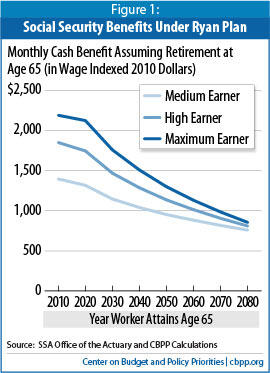

Figure 1 compares wage-indexed benefit levels in future years for a medium earner, a high earner (earning $69,000), and a person who earns the maximum taxable amount (currently $106,800). As the figure shows, benefits relative to wages would decline at all earnings levels, but especially for higher earners. By 2080, the maximum earner would receive little more than the medium earner, despite paying much higher payroll taxes over his or her career.

| TABLE 2: Effect of Ryan Plan on Medium Earner Change in Monthly Cash Benefit (in Wage Indexed 2010 Dollars) | |||||

| Year Attain Age 65 | Present Law Benefit | Percentage Change | Benefit Under Ryan Plan | ||

| Price Indexing | Increase in FRA | Both Combined | |||

| 2010 | $1,397 | --- | --- | --- | $1,397 |

| 2020 | 1,318 | --- | --- | --- | 1,318 |

| 2030 | 1,248 | -6% | -2% | -8% | 1,147 |

| 2040 | 1,245 | -12% | -5% | -16% | 1,041 |

| 2050 | 1,249 | -17% | -8% | -24% | 953 |

| 2060 | 1,251 | -21% | -11% | -29% | 882 |

| 2070 | 1,251 | -25% | -13% | -35% | 818 |

| 2080 | 1,249 | -28% | -15% | -39% | 759 |

| FRA = Full Retirement Age Source: SSA Office of the Actuary and CBPP Calculations | |||||

Although nominally open to all workers, the private accounts would be structured so that only high earners would benefit. The proposal encourages high-wage workers to choose private accounts by making their pay-outs entirely exempt from income taxation, while most of their Social Security benefits would continue to be subject to tax. The Ryan plan would also make the Social Security trust funds responsible for guaranteeing that individuals who opted for private accounts would get back at least as much as they contributed, plus an adjustment for inflation. This guarantee could require Social Security to bail out private accounts when the stock market performed poorly.

Rep. Ryan’s plan would thereby turn Social Security into a two-track system and undermine its broad base of support. Higher earners would choose private accounts. Lower earners would remain in Social Security. The Congressional Budget Office projects that 95 percent of college graduates would ultimately opt for private accounts, but only 5 percent of those who never attended college.[4]

One further point about Rep. Ryan’s Roadmap for America’s Future deserves emphasis. Although described by its author as a plan that “lifts the huge projected debt burden,” the plan’s numbers don’t, in fact, add up. The Urban Institute-Brookings Institution Tax Policy Center has found that the plan would result in very large revenue losses relative to current policies.[5] The Roadmap would give the most affluent households a new round of very large, costly tax cuts by reducing income tax rates on high-income households; eliminating income taxes on capital gains, dividends, and interest; and abolishing the corporate income tax, the estate tax, and the alternative minimum tax. As a result, despite its steep cuts in Social Security, Medicare, and other programs, the Roadmap would allow the federal debt to continue growing for decades to come.

End Notes

[1] Paul D. Ryan, A Roadmap for America’s Future, Version 2.0, January 2010, http://www.roadmap.republicans.budget.house.gov/UploadedFiles/Roadmap2Final2.pdf . The proposal has been introduced in the House as H.R. 4529.

[2] For a comprehensive analysis of the proposal, see Paul N. Van de Water, The Ryan Budget’s Radical Priorities, Center on Budget and Policy Priorities, Revised July 7, 2010.

[3] Stephen C. Goss, Chief Actuary, Social Security Administration, Letter to the Honorable Earl Pomeroy, October 18, 2010, http://waysandmeans.house.gov/media/pdf/111/SSA_Actuary_BenefitsExample_Letter.pdf .

[4] Douglas W. Elmendorf, Director, Congressional Budget Office, Letter to the Honorable Paul Ryan, January 27, 2010, page 19, http://www.cbo.gov/ftpdocs/108xx/doc10851/01-27-Ryan-Roadmap-Letter.pdf .

[5] Joseph Rosenberg, Preliminary Revenue Estimate and Distributional Analysis of the Tax Provisions in “A Roadmap for America’s Future Act 2010,” Tax Policy Center, March 9, 2010, http://www.taxpolicycenter.org/UploadedPDF/412046_ryan_taxplan.pdf .

More from the Authors