Risky Business: South Carolina's Medicaid Waiver Proposal

On June 7, 2005, South Carolina requested federal permission to undertake what would constitute the most radical changes ever made in a state Medicaid program. The request, which took the form of a proposed waiver of federal Medicaid rules, would affect more than 700,000 low-income South Carolina children, parents, seniors, and people with disabilities. [1]

South Carolina proposes to replace Medicaid with a system of state-funded “personal health accounts,” which beneficiaries would use either to purchase health care services directly from providers or to enroll in private insurance plans or private health care networks.

For beneficiaries — the vast majority of whom have incomes below the poverty line — the result would be much less health coverage at considerably greater cost. Private plans would not be required to provide the range of benefits now offered under Medicaid. All beneficiaries, including pregnant women and children, would face a significant increase in out-of-pocket costs for health care.

In addition, flaws in the state’s proposed method for determining the size of each individual’s personal health account would leave many people unable to afford the health services they need, even as other people had money left over in their accounts. Within every category of beneficiaries, each individual’s account size would be based on the average cost of health care for people in that category. Thus, individuals with above-average health care costs for their category would have accounts that are too small for them. The accounts would be especially inadequate for individuals with serious disabilities or chronic conditions such as asthma, diabetes, or HIV, since their health care costs are many times the costs of healthy individuals.

Put simply, the biggest losers from South Carolina’s proposal would be people who have the greatest health care needs and are at the greatest risk of harm if those needs are not met.

Furthermore, the waiver proposal relies on a delivery system of private insurance plans and medical home networks that does not currently exist in South Carolina. The proposal simply assumes, with no supporting evidence, that such a system will emerge and be able to provide beneficiaries with access to the health care services they need.

Finally, the proposal is based on a series of assumptions about Medicaid — that it costs more than private insurance, encourages people to use more health services than they need, and is administratively inefficient — that are demonstrably incorrect. While the state apparently believes that it can save money by replacing a public health insurance program with private programs, the evidence suggests that the state’s proposal would increase the costs of providing health care to covered beneficiaries rather than reduce those costs.

For all these reasons, South Carolina should reconsider this highly risky proposal, which could cause considerable harm to many of the state’s most vulnerable residents, before it proceeds further.

Outline of the Proposal [2]

Under the South Carolina proposal, each Medicaid beneficiary would receive a capped personal health account to use to purchase health coverage. The state would deposit funds in an individual’s account each quarter. [3] The amount of the deposits would depend on the individual’s age, sex, eligibility category, and (in some cases) health status.

Individuals could use their personal health accounts in one of three ways:

- Self-directed care : For individuals who choose this option, an amount would be deducted from their personal account to cover inpatient hospital care and “related” services; these individuals would purchase all other necessary health care services directly from providers at Medicaid fee-for-service rates with the funds remaining in their personal account. When the funds in the account were exhausted, these individuals would have to purchase any other needed health care services with their own money.

- Private insurance : Individuals who choose this option would use the funds in their personal accounts to purchase coverage from private managed care organizations or other insurance companies and from pharmacy or dental plans. Any remaining funds in the personal accounts could be used for co-payments and deductibles, as well as for health care services not covered by the plan.

The benefit package provided by these private insurers would not have to include important services now covered under the state’s Medicaid program; the only standard for determining the adequacy of the benefits that are covered would be whether the benefits would meet the needs of most users. Inevitably, then, the minority of people who are in poorest health and require the most health care services would not receive all of the services they need. Also, if insurers found over time that they were not making sufficient profit, they could reduce benefits unilaterally, without having to secure the state’s permission. - Medical home networks : Under this option, individuals would use their entire personal accounts to join medical home networks, which are groups of health care providers that would be organized to serve the state’s Medicaid beneficiaries. Each beneficiary would be assigned to a primary care provider, who would be responsible for authorizing any needed services that the primary care provider could not supply. Like the private insurers in the option above, the medical home networks would be allowed to provide a more limited package of benefits than is currently offered by the state’s Medicaid program and would be allowed to scale back covered benefits unilaterally.

Waiver Proposal Based on Faulty Assumptions

South Carolina’s waiver proposal is based on several faulty assumptions: that Medicaid is less efficient than private health plans, largely because it encourages people to use too many health services; that the state can accurately predict each individual’s need for health care services and thereby set aside an appropriate amount of funds in his or her personal health account; and that private managed care plans and provider networks will emerge in the state to serve Medicaid beneficiaries.

The success of the state’s proposal hinges on these assumptions. However, the state has not offered evidence to support them.

Medicaid Provides Comparable Services at Less Cost than Private Insurance

A recent 13-state study contradicts the notion that Medicaid beneficiaries use more health care than they need, finding instead that adult Medicaid beneficiaries use about the same level of health care services as adults with private insurance. [4] A study of mothers in low-income families found similar results.[5] Among children, Medicaid has been found to provide better access to preventive services for children than private health insurance does; this is a desirable outcome that likely reflects the success of Medicaid in facilitating preventive services for children. [6]

Moreover, Medicaid is not costlier than private health insurance. A recent study by Urban Institute researchers for the Kaiser Family Foundation found that Medicaid’s cost per beneficiary is lower than that of private insurance. [7] A separate study by Urban Institute researchers finds that Medicaid’s per-beneficiary costs have been rising more slowly than those of private insurance in recent years. [8]

The two principal reasons why Medicaid costs less than private health insurance are that its payment rates to providers tend to be lower than the rates that private insurance plans pay, and its administrative costs are about half those of private plans. According to estimates by the Centers for Medicare and Medicaid Services, Medicaid’s administrative costs average 6.9 percent of total program costs, while the administrative costs of private health plans average 13.9 percent.

South Carolina has done a particularly good job of keeping its Medicaid costs down. The state recently reported that its administrative costs were only 4.6 percent of total program costs,[9] well below the national average, and in 2004 the state’s Medicaid expenditures grew substantially more slowly than the national average (5.8 percent versus 9.3 percent). In addition, South Carolina’s Medicaid payment rates to physicians are, on average, about 75 percent of Medicare’s payment rates, and about 65 percent of what the South Carolina state employee health plan pays. [10]

It should be noted that administrative expenses would rise under the proposed waiver. South Carolina would have to hire a company to counsel beneficiaries on their coverage options, as well as a company to oversee the medical home networks. Also, each private insurance plan would have to set up and maintain its own administrative structure. As the amount of funding going for administration increased, the amount available for actual health care services would decrease. This could put further pressure on provider payment rates that are already low and could thereby affect the willingness of providers to participate in the program.

Finally, the notion that Medicaid beneficiaries do not bear any of the financial responsibility for their health care is incorrect. Recent studies show that, on average, adults on Medicaid pay a larger percentage of their income in out-of-pocket medical expenses than do non-low-income individuals with private insurance. Studies also demonstrate that in recent years, the share of Medicaid beneficiaries’ income that is consumed by out-of-pocket medical expenses has been rising twice as fast as their incomes. Medicaid beneficiaries who have disabilities bear especially high out-of-pocket costs.[11]

“Risk Adjustment” Cannot Predict an Individual’s Need for Health Care Services

A fundamental question regarding South Carolina’s proposal is whether the state would deposit sufficient funds in each beneficiary’s personal health account to enable the beneficiary to purchase necessary health care services. The state says it would determine the amount of funding for each account through a process known as “risk adjustment.” An individual’s need for health care is inherently unpredictable, however, and no system of risk adjustment has ever been developed that can accurately predict what a specific individual will need for health care from one year to the next.

Under the South Carolina proposal, the state would begin by assigning each Medicaid beneficiary a “rate category” based on his or her age, sex, eligibility category, and (in some instances) health status. For each rate category, the state then would determine the average amount that Medicaid spent on beneficiaries in that category in a base year. That average amount, adjusted upward to reflect the increase in health care costs since the base year, would be deposited in the personal health account of each person in the rate category.

This process is similar to the way in which states set per capita payments for their Medicaid managed care programs. Risk adjustment works relatively well in the managed care context because each plan enrolls a mix of individuals: while some individuals will cost the company more than the amount that it receives from the state to cover them, other individuals will cost the company less than that amount. Thus, if the plan receives a flat payment per person that represents average costs over all of its enrollees, the plan will come out behind on some people and ahead on others — and be able to cover its costs overall.

But using risk adjustment for personal health accounts, as South Carolina proposes, is very different. Since each account covers only a single individual, account funds cannot be shifted from people with relatively low health costs to people who turn out to have relatively high health costs. As a result, some people will likely use up the money in their accounts and be unable to afford health care services that they need, while at the same time, other people may have leftover funds in their account that they do not need.

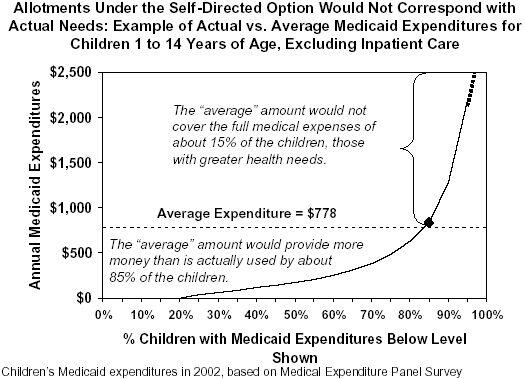

For example, the graph below (which was developed using a process similar to the one that South Carolina proposes to use to set the average payment amounts to deposit in the personal health accounts) shows that average annual Medicaid expenditures per child exceed actual expenditures for about 85 percent of children and are less than actual expenditures for the remaining 15 percent of children, based on analyses of the 2002 Medical Expenditure Panel Survey (MEPS), a federally sponsored national survey of health care costs and usage. Since under the South Carolina proposal the average amount would be allocated to each individual child’s personal health account, this means that approximately 15 percent of children — those with the most serious health problems and health care needs — would have insufficient funds to purchase necessary health care services. These children’s health could suffer, in some cases seriously.

Further evidence that some people have much greater health care needs and costs than others can also be found in another analysis of the 2002 MEPS, which reported that 10 percent of the individuals surveyed accounted for 72 percent of health care costs. [12] Indeed, South Carolina’s waiver proposal itself acknowledges that 5 percent of the state’s Medicaid beneficiaries account for 55 percent of Medicaid expenditures. That is why basing the size of each individual’s health account on the average expenditure for an entire category of people does not work: the average amount will always be less than some people need to purchase adequate health care services, and much less than the sickest, most vulnerable people need.

South Carolina claims it will take individuals’ health status into account when assigning them to rate categories. Yet this often will not be possible: many individuals will not have been on Medicaid long enough for the state to obtain a history of their usage of health care services. [13] Even when the state can determine an individual’s health care needs, the accounts still will be insufficient for people whose costs are above average for those in their rate category. Furthermore, over the course of a year, some people who have used relatively few health care services in the past will become ill with chronic diseases such as cancer, heart disease, or diabetes; as a result, their health accounts will be too small to pay for the health care they now need.

State Lacks Needed Managed Care Plans and Medical Home Networks

The South Carolina proposal implicitly recognizes the danger of leaving individuals with chronic health care conditions on their own to purchase health care, stating that those with a “history of unstable expensive acute care crises” would not be permitted to choose the self-directed care option. Others who would be foreclosed from this option are those who do not have a primary care physician and those who are unable to “demonstrate a reasonable understanding of their family’s health care needs and how they are to be met.”

One shortcoming of the state’s approach in this area is that some people who do not have a history of poor health at the time they enter the program — and thus are not barred from choosing the self-directed care option — will develop chronic conditions or will suffer an event, such as an injury, that requires substantially more care. If they have opted for self-directed care, they likely will find themselves unable to pay the much larger health care costs that they encounter when those conditions develop.

Another serious shortcoming of the state’s approach is that South Carolina lacks sufficient private insurers to handle the many Medicaid beneficiaries who would be directed into the private insurance or medical home network options. In 2004, only 6.1 percent of all South Carolina residents were enrolled in health maintenance organizations,[14] and the state’s Medicaid program ranks 47th in the nation in managed care participation:

- Only 8.4 percent of South Carolina Medicaid beneficiaries are currently enrolled in Medicaid managed care plans. [15]

- There are only two Medicaid managed care plans in the state, and these plans currently cover just 28 of the state’s 46 counties. [16]

- Adults with disabilities and children with special health care needs are not currently enrolled in managed care at all in South Carolina.

- South Carolina has only just begun to develop medical home networks.

Given the very low rate of managed care participation in South Carolina, the state’s health care delivery system is not likely to be able to meet the needs of the many Medicaid beneficiaries who would choose (or be required to enroll in) private insurance or medical home networks.

In recognition of this problem, the South Carolina waiver proposal states that the new program would rely on private market development that “should result in quality health care through yet undesigned models” and that the “greatest value from this demonstration will be attained through the new creative models yet to come.” This rosy scenario — that a sufficient number of new private health plans will somehow arise to compete for Medicaid customers in an extremely short timeframe in a state with extremely low managed care participation — is not justified by the current marketplace for health care in the state. If the state’s optimism proves unfounded, as may very well be the case, the consequences would be especially severe for sicker Medicaid beneficiaries, who would fare particularly badly with self-directed accounts.

Children Would Lose Access to Needed Health Services — Including EPSDT Services

As the waiver is currently drafted, children would no longer be guaranteed all of the health care services they need for their healthy development as currently provided through Medicaid’s Early and Periodic Screening, Diagnosis and Treatment (EPSDT) program. Under EPSDT, children receive regular preventive health care and all necessary follow-up diagnostic and treatment services without any limitations, including services that may not otherwise be covered by a state’s Medicaid program for adults. EPSDT is of critical importance for children in Medicaid because they tend to be in poorer health than children with private coverage.[17]

After the waiver was submitted, the South Carolina Department of Health and Human Services posted answers to frequently asked questions on its website. In response to a question about EPSDT, the Department claimed it was not seeking to waive EPSDT because “the State Health Plan for state employees is very similar to EPSDT.” The Department also stated that it would change the “description” in the waiver if the comparison of EPSDT and the State Health Plan does not guarantee children EPSDT benefits.

The state employees’ health plan does not, in fact, provide coverage comparable to EPSDT; the EPSDT guarantee goes well beyond the coverage the state employee health plan offers in a number of respects. Under EPSDT, children are entitled to all preventive, diagnostic and treatment services that are medically necessary for them, without limitations on the amount, duration or scope of the particular service. For example, EPSDT covers treatment that helps a child with a chronic illness or disability even if the child’s condition may never markedly improve. [18] The state employee health plan does not provide comparable assistance. In addition, EPSDT covers services such as wheel chairs, hearing aids, and medical supplies for children with asthma and other health care conditions. Private plans generally do not cover such items either.

Despite the fact that the state employee health plan clearly does not provide coverage comparable to EPSDT, no change to reinstate the EPSDT guarantee has yet been made in either the proposal that the state submitted to the federal government or the version of the proposal posted on the Department’s website.

The bottom line here is that children evidently would experience substantial reductions in health care benefits under all three of the coverage options set forth in the South Carolina proposal:

- For children in the self-directed care option, there appear to be no benefit standards whatsoever. Other than inpatient care and related services, the benefits that children would receive would be limited to whatever health care services their parents could afford to purchase with the funds placed in the child’s personal health account.

- The private plans and medical home networks would be free to define their own benefit packages — including the benefit packages for children — as long as the packages were “actuarially equivalent” to one of three designated benchmark plans: the state employee health plan, the federal employees health benefit plan, or the largest managed care plan in the state. None of these benchmark plans includes the benefits afforded to children under EPSDT. [19] Children on Medicaid consequently would lose access to benefits that EPSDT covers fully but private plans cover only partially or not at all, such as wheelchairs, hearing aids, and speech therapy.

To date, no state in the nation has eliminated the EPSDT guarantee for children in families with incomes below the poverty line. The American Academy of Pediatrics recently reaffirmed its staunch support of the EPSDT standards, declaring that all eligible children should continue to receive the comprehensive care afforded under EPSDT.[20]

The loss of the EPSDT guarantee would be especially harmful for children with disabilities or other special health care needs. Such children often require services that commercial managed care plans do not provide or require services at a level of intensity that goes beyond the limits of most benefit packages. Without EPSDT, the health and well-being of many disadvantaged children would be at risk.

For Adults, Some Health Care Services Would Be Eliminated, Others Curtailed

As noted, there appear to be no benefit standards for self-directed care, so adults who choose this option would be limited to whatever health care services they could afford to purchase from the funds in their personal health account. Beneficiaries who suffer injuries or unexpected illness would likely be left with insufficient resources to purchase the health care they need.

For adults who choose the private insurance or medical home network options, the minimum benefit package would be limited to services that federal Medicaid law designates as “mandatory,” as well as to prescription drugs and durable medical equipment. It is important to note that the list of “mandatory” Medicaid services is not — and was not intended to be — a comprehensive list of all important health care services. It was always intended that state Medicaid programs also offer a number of other services, and every state’s Medicaid program does so. For example, prescription drugs are not included in the list of “mandatory” medical services, but they surely are essential to health.

South Carolina’s current Medicaid program covers a number of “optional” services, including emergency dental services, vision care, and hearing aids, as do the Medicaid programs of the vast majority of states. Under South Carolina’s waiver proposal, however, private insurance plans and medical home networks would not need to cover any “optional” services other than prescription drugs and durable medical equipment.

Moreover, even “mandatory” services (as well as prescription drugs and durable medical equipment) would be limited, since the private plans would be allowed to restrict their coverage of these benefits as long as the coverage “meets all of the need of most of their users of each service.” For example, if most beneficiaries use fewer than three prescriptions per month or five physician visits per year, the plan could restrict all beneficiaries to three prescriptions per month or five physician visits per year, even though some very sick beneficiaries would need more than that. This provision would allow the health plans to restrict some benefits significantly.

This aspect of the state’s proposal would be especially dangerous for people with serious disabilities or chronic conditions such as asthma, diabetes, or HIV. Such people generally require a higher level of health care services than most other Medicaid beneficiaries. They can land in the hospital — or worse — if needed medications are not obtained or they are unable to visit the doctor whenever necessary.

All Beneficiaries Would Pay Significantly More for Health Care

Currently, most Medicaid beneficiaries in South Carolina are charged co-payments, ranging from $1 to $3 per service for most medical services. Federal Medicaid law exempts pregnant women and children from co-payments and other forms of “cost-sharing,” however, in recognition of the critical importance of preventive and primary health care services to successful birth outcomes and children’s development.

Under the waiver proposal, out-of-pocket costs would increase significantly for all beneficiaries, regardless of which of the three options they choose (self-directed care, private insurance, or medical home networks). Children and pregnant women would face co-payments for the first time.

- Those selecting the self-directed care option would have to pay $100 for each hospitalization. In addition, if they exhausted the funds in their personal health accounts, they would have to pay the full cost of any additional health care services they needed.

- For those electing the private insurance option, the insurer would set its own co-payment and deductible charges. While there would be a limit on total out-of-pocket costs, South Carolina’s waiver proposal does not specify what that limit would be.

- For those electing a medical home network, co-payments would be set well above the levels Medicaid currently allows. Beneficiaries would be charged $100 per inpatient hospital visit, $25 per outpatient visit, $5 per physician visit, $10 per brand name drug, and $5 per generic drug prescription.

The vast majority of Medicaid beneficiaries in South Carolina have incomes below the poverty line ($798 per month for an individual and $1,341 per month for a family of three).[21] Faced with substantially increased cost sharing charges, along with the loss of coverage for certain medical needs that Medicaid now covers, a large number of low-income families, seniors, and people with disabilities likely would likely lose access to some health care services that they needed.

Numerous studies have been conducted of the effects of even modest cost-sharing charges. The studies show that for people with low incomes, increased co-payments result in significantly reduced access to care and often in a deterioration of patients’ health.

- The RAND Health Insurance Experiment, considered the definitive study of this issue, found that while co-payments did not adversely affect the health of middle- and high-income people, they did lead to poorer health for those with low incomes. The Rand study found that co-payments led to a marked reduction in “episodes of effective care” among low-income adults and children. As a consequence, health status was considerably poorer among those low-income adults and children who had to make co-payments to obtain care than among comparable low-income adults and children who were not subject to co-payments. As one example, co-payments were found in the RAND experiment to increase the risk of death by about 10 percent for low-income adults who were at risk of heart disease. [22]

- Recent research also has shown that when the Utah Medicaid program imposed small co-payments of $2 or $3 per prescription or service, the co-payments led to a significant reduction in the number of physician visits by beneficiaries with incomes below the poverty line. About two-fifths of beneficiaries reported the co-payments caused them “serious” financial hardships. [23]

- A recent small survey in Minneapolis’ main public hospital that examined the effects of modest co-payments instituted in that state’s Medicaid program produced similar findings. Slightly more than half of those surveyed reported being unable to obtain their prescriptions at least once in the last six months because of the co-payment charges. Those who failed to obtain their prescriptions at least once experienced a marked increase in subsequent emergency room visits and hospital admissions, including admissions for strokes and asthma attacks. [24]

- Still another such piece of research, published in the Journal of the American Medical Association, found that after Quebec imposed co-payments for prescription drugs on adults who were receiving welfare, these individuals filled fewer prescriptions for essential medications, and emergency room use subsequently climbed by 88 percent among these individuals. In addition, the number of “adverse events” such as death and hospitalization rose by 78 percent. [25]

The problem is that after paying for food, clothing and shelter, low-income individuals often have little money left to meet the costs of health care services. When the cost of health care services increases, these individuals often respond by doing without them. [26] The impact of facing a higher charge each time that a health care service or medication is used is especially severe for beneficiaries with serious health problems, such as diabetes, heart disease, mental health problems, or HIV. These individuals require more health care services and medications and consequently face a larger volume of co-payments.

Federal Funding Limitations Could Weaken Coverage Further

South Carolina has not released its proposal for financing its waiver, but waivers submitted under Section 1115 of the Social Security Act (as South Carolina’s has been) must be “budget neutral.” This means that the federal government will not spend more under the waiver than it would spend in the waiver’s absence.

South Carolina apparently is proposing to achieve budget neutrality by imposing a spending cap per beneficiary. This would represent a sharp departure from Medicaid’s current financing system, which guarantees beneficiaries all covered services that they need and guarantees federal matching funds to states to cover a specified share of the costs of those services.

Under the proposed cap, federal Medicaid funding per beneficiary would be allowed to increase at a rate that is based on the rate of growth in prior years of the state’s costs in serving the beneficiary population that the waiver would cover. This means that if the state’s Medicaid enrollment increased, the state would receive additional federal funds to serve the added beneficiaries but that the state would not receive additional federal funds to help pay for unanticipated increases in health care costs, such as those that could result from the development of new drugs, advances in medical technology, or a natural disaster or flu epidemic. [27] In such cases, South Carolina would be forced to choose between covering the added costs entirely with state funds, cutting eligibility or benefits, or reducing health care coverage indirectly by shrinking the size of beneficiaries’ personal health accounts.

Exacerbating this problem, the language in the waiver proposal suggests that South Carolina also may seek a “global” spending cap. Unlike a per-beneficiary cap, a global cap would impose a ceiling on the total amount of federal funds that South Carolina would receive for the parts of its Medicaid program that were under the waiver. [28] A global cap would put the state and its beneficiaries at even greater risk than a per-beneficiary cap. Not only would the state receive no additional federal funds to deal with unanticipated increases in health care costs, but it also would receive no additional federal funds to deal with unanticipated increases in Medicaid enrollment, such as those that would result from an economic slowdown (when more people lose their jobs and private health coverage and consequently qualify for Medicaid). A global cap would make future additional cuts in health care services in South Carolina more likely.

Even apart from the possibility of unanticipated increases in health care costs or enrollment, a funding cap would place growing pressure on South Carolina’s Medicaid program over time if the cap failed to keep pace with the program’s normal increases in costs. If the percentage by which the cap was adjusted upward each year was smaller than the percentage increase in program costs, the state would be forced to impose deeper budget cuts each year to make up for the mounting loss of federal funds.

Recent experience suggests that South Carolina could end up with a funding cap that would fail to keep pace with the costs of treating the state’s Medicaid beneficiaries. In negotiations with the federal government over a previous waiver that covered prescription drugs for elderly Medicaid beneficiaries, South Carolina agreed to a federal funding cap that was adjusted upward each year at a substantially slower rate than the rate at which the health care costs of those beneficiaries were rising in the years prior to the waiver. South Carolina agreed to that limit on the rate of growth of its federal Medicaid funding even though the limit was set lower than the comparable limit imposed on the other three states that secure similar waivers.[29]

End Notes

[1] The waiver would not affect those beneficiaries who are eligible for both Medicaid and Medicare. A June 7 letter from the South Carolina Medicaid Director, which transmitted the waiver proposal to CMS, states that the waiver also does not affect long-term care and behavioral health care services, including mental health and substance abuse treatment. The Carolina waiver proposal and related documents, including answers to frequently asked questions, can be found at http://www.dhhs.state.sc.us/dhhsnew/HealthyConnections/index.asp

[2] This analysis is based on the proposal submitted to CMS in June. A slightly different version that removes the section requesting waivers of specific federal provisions was posted on the South Carolina Department of Human Services web site in July.

[3] Balances in the account at the end of a quarter would roll over to the next quarter within a benefit year. According to the waiver proposal, a portion of unexpended funds may be allowed to roll over to the following year.

[4] Teresa Coughlin, Sharon Long and Yu-Chu Shen, “Assessing Access to Care Under Medicaid: Evidence for the Nation and Thirteen States,” Health Affairs, 24(4):1073-1083, July/August 2005.

[5] Sharon K. Long, Teresa Coughlin and Jennifer King, “How Well Does Medicaid Work in Improving Access to Care?” Health Services Research, 40(1): 39-58, February 2005.

[6] Lisa Dubay and Genevieve M. Kenney, "Health Care Access and Use Among Low-income Children: Who Fares Best?" Health Affairs 20(1): 112-21, January/February 2001

[7] Jack Hadley and John Holahan, “Is Health Care Spending Higher under Medicaid or Private Insurance?” Inquiry, 40 (2003/2004): 323-42.

[8] John Holahan and Arunabh Ghosh, “Understanding the Recent Growth in Medicaid Spending, 2000-2003,” Health Affairs web exclusive, January 26, 2005

[9] Medicaid and SCHIP Budget Estimates, Forms CMS-37 and CMS-21B, May 2005 submission.

[10] South Carolina Medicaid, Annual Report for State Fiscal Year 2004.

[11] Leighton Ku and Matthew Broaddus, “ Out-Of-Pocket Medical Expenses For Medicaid

Beneficiaries Are Substantial And Growing , “(Washington, DC: Center on Budget and Policy Priorities, 2005)

[12] Andy Schneider and others, “Medicaid Cost Containment: The Reality of High-Cost Cases,” (Washington, DC: Center for American Progress, 2005).

[13] One large study found that 35 percent of beneficiaries were enrolled for a year or less. Pamela Farley Short and others, “Churn, Churn, Churn: How Instability of Health Insurance Shapes America’s Uninsured Problem,” (New York, NY: The Commonwealth Fund, 2003)

[14] Managed Care Penetration by State and Region, 2004 from InterStudy Competitive Edge: Managed Care Industry Report Fall 2004 at http://www.mcareol.com/factshts/factstat.htm.

[15] Centers for Medicare and Medicaid Services, “Medicaid Managed Care Penetration Rates as of December 31, 2004,” available at http://www.cms.hhs.gov/medicaid/managedcare/mmcpr04.pdf.

[16] According to the waiver proposal, expansion of managed care into three additional counties is awaiting approval.

[17] Leighton Ku and Sashi Nimalendran, “Improving Children’s Health: A Chartbook About the Roles of Medicaid and SCHIP,” (Washington, DC, Center on Budget and Policy Priorities, January 2004).

[18] The revised version of the waiver posted on the website on July 15 did not change the description of covered benefits for children that would eliminate EPSDT.

[19] Sara Rosenbaum and others, “Public Health Insurance Design for Children: The Evolution from Medicaid to SCHIP,” Journal of Health and Biomedical Law, 1: 1-47 (2004).

[20] American Academy of Pediatrics Medicaid Policy Statement, Pediatrics, 116(1)(2005):1-7.

[21] The only major exception are pregnant women and infants, who can be eligible for Medicaid if they have incomes up to 185 percent of the poverty line, and children from one to age six, who can be eligible if they have incomes up to 133 percent of the poverty line. In South Carolina, children with incomes up to 150 percent of the poverty line are included in Medicaid, although their coverage is financed under the State Children’s Health Insurance Program.

[22] Joseph Newhouse, Free for All? Lessons from the Rand Health Insurance Experiment, Harvard University Press, 1996.

[23] Leighton Ku, Elaine Deschamps and Judi Hillman, “ The Effects of Copayments in the Use of Medical Services and Prescription Drugs in Utah’s Medicaid Program ,” Center on Budget and Policy Priorities, November 2004. It should be noted that an analysis of the identical Utah data by the Utah Department of Health concluded that, “In most cases, the utilization analyses show that co-pay requirements had no statistically significant impact on utilization.” Office of the Executive Director, Utah Department of Health, “Medicaid Benefits Change Impact Study,” in 2003 Utah Public Health Outcome Measures Report, Salt Lake City, UT: Dec. 2003. A detailed response explaining why the Utah Department of Health analysis is technically flawed is included in the technical appendix to the paper by Ku, et al.

[24] Melody Mendiola, Kevin Larsen, et.al., “Medicaid Patients Perceive Copays as a Barrier to Medication Compliance,” Hennepin County Medical Center, Minneapolis, MN, presented at the Society of General Internal Medicine national conference, May 2005.

[25] Robyn Tamblyn, et al., “Adverse Events Associated with Prescription Drug Cost-Sharing among Poor and Elderly Persons,” Journal of the American Medical Association, 285(4): 421-429, January 2001. In this study, the low-income people were adults who were on welfare.

[26] Leighton Ku, “The Effect Of Increased Cost-Sharing In Medicaid: A Summary Of Research Findings”, Center on Budget and Policy Priorities, revised July 7, 2005, Bill Wright, Matthew Carlson, Tina Edlund, Jennifer DeVoe, Charles Gallia and Jeanene Smith, “The Impact of Increased Cost-sharing on Medicaid Enrollees,” Health Affairs, 24(4):1107-15, July/August 2005.

[27] Cindy Mann and Joan Alker, “Federal Medicaid Waiver Financing: Issues for California,” (Washington, DC: Kaiser Commission on Medicaid and the Uninsured, 2004).

[29] In the three years prior to approval of that waiver, health care costs for elderly Medicaid beneficiaries in South Carolina rose at an average annual rate of 11.1 percent. As a result, federal matching funds for those costs also rose at an 11.1 percent rate. South Carolina accepted as part of its waiver, however, a cap of 7.4 percent on the annual rate of growth of federal matching funds for the Medicaid costs of these beneficiaries. See Jocelyn Guyer, “The Financing of Pharmacy Plus Waivers: Implications for Seniors on Medicaid of Global Funding Caps,” (Washington, DC: Kaiser Commission on Medicaid and the Uninsured, 2003)

More from the Authors