Raising Medicare’s Eligibility Age Would Increase Overall Health Spending and Shift Costs to Seniors, States, and Employers

Raising Medicare's eligibility age from 65 to 67, which the new Joint Select Committee will likely consider this fall as a deficit-reduction measure, would not only fail to constrain health care costs across the economy; it would increase them.

While this proposal would save the federal government money, it would do so by shifting costs to most of the 65- and 66-year-olds who would lose Medicare coverage, to employers that provide health coverage for their retirees, to Medicare beneficiaries, to younger people who buy insurance through the new health insurance exchanges, and to states.

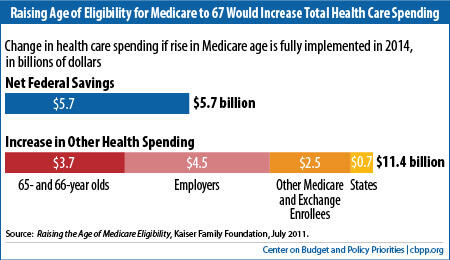

The principal study of the effects of raising the Medicare eligibility age, by the Kaiser Family Foundation, estimates that its increased state and private-sector costs would be twice as large as the net federal savings. If the proposal were fully in effect in 2014, Kaiser estimates, it would generate $5.7 billion in net federal savings but $11.4 billion in higher health care costs to individuals, employers, and states.

The fundamental purpose of deficit reduction is to strengthen the economy over the long term. The relentless rise in health care costs is the key driver of projected long-term deficits that policymakers must address. But reducing federal health care costs by raising state and private-sector health care costs even more makes little sense, as it only increases the burden that health care costs place on the economy as a whole. The goal should be to slow the growth of health care costs system-wide, while extending coverage to all Americans. This proposal does just the opposite on both fronts — raising costs system-wide and increasing the ranks of the uninsured.

The Kaiser report found that if policymakers raised the Medicare eligibility age to 67:

- 65- and 66-year-olds would face higher out-of-pocket health care costs, on average. Two-thirds of this group — 3.3 million people — would face an average of $2,200 more each year in premiums and cost-sharing charges.

- State Medicaid costs would rise as some of those who lost Medicare coverage (those with the lowest incomes) would obtain coverage through Medicaid instead.

Scheduled Increase in Social Security's Full Retirement Age Is Not a Sound Reason to Raise Medicare Eligibility Age

Some people contend that policymakers should raise Medicare's eligibility age to 67 to match the scheduled increase in Social Security's "full retirement age" to 67. This argument may seem plausible at first blush. But in reality, it reflects a misunderstanding of how Social Security works.

Most Social Security beneficiaries do not begin drawing benefits at Social Security's "full retirement age." To the contrary, about half of Social Security retirement beneficiaries begin to draw benefits at age 62, and two-thirds begin to draw benefits before 65.a

If a beneficiary does not claim benefits at 62, his or her monthly benefit is increased on an actuarial basis for each month that the beneficiary delays claiming, up through age 70, so that the expected lifetime value of benefits remains about the same. Indeed, Social Security's "full retirement age" (sometimes called the "normal retirement age"), now 66 and scheduled to increase to 67, has become a misnomer. It is not the age at which most retired workers claim benefits, nor is it the age of claiming that produces the highest monthly benefit.

Raising the age of eligibility for Medicare thus would not better align Medicare and Social Security. The programs are not currently aligned, since there is a lag of up to three years between when most people claim Social Security and when they become eligible for Medicare. And raising the Medicare eligibility age would push the two programs further out of alignment, rather than bringing them closer together.

a Owen Haaga and Richard W. Johnson, "Social Security Claiming and the Business Cycle," paper prepared for the annual conference of the Retirement Research Consortium, August 4, 2011.

- Employer costs would rise as more 65- and 66-year-olds whose employers offered coverage to their retirees received primary coverage through their employer rather than Medicare.

- All Medicare beneficiaries would pay higher premiums because the removal of 65- and 66-year-olds, who are typically healthier than the overall Medicare beneficiary population, would leave the Medicare beneficiary population costlier, on average, to cover.

- People under age 65 who buy coverage through the new health insurance exchanges would face higher premiums to help cover the cost of insuring the many 65- and 66-year-olds who would enter the exchanges; the 65- and 66-year-olds would be less healthy, and more costly to cover, on average, than other people who bought coverage through the exchanges.

Under the health reform law (the Affordable Care Act, or ACA), seniors no longer eligible for Medicare could obtain coverage through Medicaid or the exchanges. But raising the age of eligibility for Medicare would substantially boost out-of-pocket costs for 65- and 66-year-olds, which many of them with modest incomes could have difficulty affording, prompting some to become uninsured and others to forgo needed care. It also would raise health care costs overall. Policymakers could take some steps, outlined below, to limit — but not eliminate — these harmful impacts. Moreover, if Congress repealed health reform, as the House has voted to do, large numbers of 65- and 66-year-olds who lost Medicare coverage would likely wind up uninsured.

Change Would Produce Net Federal Savings

The Congressional Budget Office (CBO) has examined an option that would raise Medicare's eligibility age by two months every year starting with people born in 1949 (who will turn 65 in 2014) until it reaches 67 for people born in 1960 (who will turn 67 in 2027), remaining at 67 thereafter. [1] Under this option, CBO assumes that Congress would make 65- and 66-year-olds with incomes below 138 percent of the poverty level eligible for Medicaid, to match the new Medicaid income limit for other adults that the Affordable Care Act establishes starting in 2014.

CBO estimates that this option would reduce federal spending by $125 billion over the ten-year period from 2012 through 2021. Medicare spending would drop by $162 billion, while other federal spending — primarily Medicaid and subsidies to purchase health insurance in the new health insurance exchanges — would increase by a net of $38 billion. By 2035, according to CBO, this option would reduce projected Medicare spending by about 7 percent, from 5.9 percent to 5.5 percent of gross domestic product. (Note: The option that CBO examined does not include the costs of several steps that should be taken to reduce some of the proposal's adverse impacts; these steps, which are outlined below and should be regarded as essential aspects of the proposal if policymakers decide to pursue it, would reduce the federal savings.)

Cost Increases for Individuals, Employers, and States Would Far Exceed Federal Savings

Raising the age of eligibility for Medicare would have ramifications far beyond the federal budget. People who lost Medicare would have to seek health coverage from other sources. This would affect not only their own personal budgets but also employers' costs, state budgets, and the premiums paid by Medicare beneficiaries and participants in the new health insurance exchanges.

Kaiser estimates that raising the eligibility age would save the federal government $5.7 billion in 2014. The savings reflect $24 billion in lower Medicare spending net of beneficiaries' premiums, largely offset by $18 billion in higher spending for Medicaid and subsidies for low-income participants in the health insurance exchanges. The estimated increase in costs to seniors, employers, states, and others, however, would total $11.4 billion — twice the net savings to the federal government. (See figure.)

Many Who Lost Medicare Coverage Would End Up Uninsured

The Kaiser study assumes for the sake of simplicity that everyone who would lose Medicare coverage would obtain health insurance coverage elsewhere. Under this assumption, Kaiser estimates that 42 percent of 65- and 66-year-olds would obtain coverage from employer-sponsored plans (either as retirees or active workers), 38 percent would enroll in the new health insurance exchanges, and 20 percent would become covered under Medicaid.

In reality, however, many of these 65- and 66-year-olds are likely to end up uninsured. Some of those eligible for premium credits in the exchanges would not enroll because they would regard the required premium contribution as too high; people with incomes between 300 and 400 percent of the poverty level (about $34,500 to $46,000 for an individual in 2014) will have to pay 9.5 percent of their income — $3,300 to $4,400 — for exchange coverage. Even some of those eligible for more generous premium credits or for Medicaid would likely fail to obtain coverage; participation in means-tested programs like Medicaid falls far short of that in social insurance programs like Medicare, in part because of the difficulties navigating the application process.

In addition, many 65- and 66-year-olds who would be ineligible for Medicaid or premium credits because their incomes exceeded $46,000 would find unsubsidized coverage in the exchange to be out of reach. According to Kaiser, half of 65- and 66-year-olds who would have to rely on the exchange would have incomes too high for premium credits. Because exchange plans could charge the oldest workers three times as much as the youngest, unsubsidized premiums could reach $10,000 to $12,000 (in 2014 terms) for 65- and 66-year-old individuals and twice that for couples. [3]

Out-of-Pocket Costs Would Rise for 65- and 66-Year-Olds

Two-thirds of 65- and 66-year-olds — 3.3 million people — would incur an average of $2,200 more in out-of-pocket health spending for premiums and cost-sharing if Medicare's eligibility age were raised, according to Kaiser. The remaining one-third — 1.6 million people with incomes below 300 percent of the poverty level, who would be eligible for Medicaid (if everyone up to 138 percent of poverty was covered) or larger premium subsidies — would pay $2,300 less, on average. Overall, 65- and 66-year-olds would pay an average of $700 a year more, or $3.7 billion more in total in 2014.

In some states, 65- and 66-year-olds could receive less adequate coverage in Medicaid and the exchanges than they would have from Medicare. While Medicaid generally offers a more comprehensive benefits package than private insurance and Medicare, with only nominal cost-sharing, state Medicaid programs can limit both the number of prescriptions covered per month and the number of physician visits covered each year.

For some individuals made newly eligible for Medicaid by the health reform law — a group that would encompass many 65- and 66-year-olds under this proposal — states can opt to provide a much less generous benefit package than the regular Medicaid package, so long as they provide the "essential benefits" available through the exchanges. The Department of Health and Human Services has yet to specify the essential benefits package; depending on the flexibility it gives states in this area, 65- and 66-year-olds may lose coverage of some benefits or have them covered to a lesser degree than they would under Medicare. Finally, because of Medicaid's low reimbursement rates to health care providers, some Medicaid beneficiaries are likely to have more difficulty obtaining physician services, particularly from specialists, than they would have under Medicare.

Costs Would Shift to States, Employers, and People in Medicare and the Exchanges

As well as increasing out-of-pocket health costs for 65- and 66-year-olds, raising Medicare's eligibility age would shift costs to states, employers, Medicare beneficiaries, and participants in the health insurance exchanges.

- State spending would increase by $0.7 billion in 2014, Kaiser estimates, because Medicaid would cover all health care expenses for 65- and 66-year-olds who would otherwise have been fully eligible for both Medicaid and Medicare and for whom Medicare would have been the primary payer. State spending would increase by significantly larger amounts in later years as states gradually assume a portion of the costs of 65- and 66-year-olds who would not become fully eligible for Medicaid until health reform's Medicaid expansion is in effect. The federal government will pay the entire cost of these individuals in 2014, but states must pay 10 percent of their costs by 2020.

- States would have to pay an even larger share of the cost of covering 65- and 66-year-olds newly eligible for Medicaid — something like 40 percent or more — under a proposal for a "blended" Medicaid matching rate. The proposal, floated in vague terms by the Administration this spring but never formally issued, would replace the various matching rates at which the federal government reimburses states for their Medicaid costs with a single "blended" rate for each state.[4] A state's blended rate would be set at a level that provides the state with less federal funding overall than under current law. Because states would have to pay a much greater share of the cost of insuring individuals who are newly eligible for Medicaid as a result of the health reform law, states would have much less incentive to assure that eligible people enroll. As a result, the number of 65- and 66-year-olds who became uninsured would be higher.

- Employers' costs would increase by an estimated $4.5 billion in 2014 as more 65- and 66-year-old retired workers whose employers offered coverage to their retirees received primary coverage through their employer rather than Medicare.

- Medicare beneficiaries would pay a total of $1.8 billion in higher premiums because relatively healthy 65- and 66-year-old beneficiaries would be removed from Medicare's insurance risk pool. At present, these younger Medicare beneficiaries cost less than older beneficiaries but pay the same premiums, thereby holding down premiums for everyone else. The Kaiser study estimates that premiums for other Medicare beneficiaries would rise by about 3 percent if 65- and 66-year-olds could no longer participate in the program.

- Adding 65- and 66-year-olds to the health insurance exchanges would raise premiums for everyone else in the exchanges by about 3 percent, or $700 million in 2014. The reason is that under the ACA, insurers may not charge the oldest enrollees more than three times as much as the youngest, but the average cost of covering the oldest enrollees is over five times that of the youngest, so insurers would raise premiums for enrollees under age 65 to cover the difference. As premiums for everyone in the exchange rose because of the influx of 65- and 66-year olds, some of the healthiest unsubsidized participants likely would drop coverage, further pushing up premiums for everyone else.

According to Kaiser's estimates, the additional costs to 65- and 66-year-olds, state governments, employers, Medicare beneficiaries, and exchange participants would total $11.4 billion — twice the net savings to the federal budget. Thus, like the House Republican budget fashioned by Rep. Paul Ryan, raising the age of eligibility for Medicare would increase — not reduce — economy-wide health care spending. [5]

Finally, by shrinking Medicare's share of the health insurance market, the proposal would reduce Medicare's market power and weaken its ability to serve as a leader in controlling health care costs.

Modifications to Proposal Could Ameliorate — But Not Solve — Its Core Problems

Most of the problems discussed above would occur under any proposal to raise Medicare's eligibility age to 67. Total health care costs would rise, some seniors would end up uninsured, and many would face unaffordable out-of-pocket costs. Should the Joint Committee nevertheless choose to recommend this proposal, it should include certain modifications that would limit — but not eliminate — the adverse effects on many beneficiaries and on the states:

- Raise the age cutoff for health reform's Medicaid expansion to 67 . Under the Affordable Care Act, the Medicaid expansion for people with incomes below 138 percent of poverty extends only to age 65. If Congress fails to raise that age limit to 67, some 65- and 66-year-olds with incomes below 100 percent of poverty who lost Medicare eligibility would be eligible for neither Medicaid nor premium credits. Both the CBO and Kaiser analyses assume that policymakers would make this essential change as part of raising the Medicare eligibility age.

- Require states to provide the regular comprehensive Medicaid benefits package to 65- and 66-year-olds. This would ensure that states provide benefits that are at least as comprehensive as under Medicare to 65- and 66-year-olds with incomes below 138 percent of the poverty line. However, it would not address gaps in Medicaid coverage that exist today. Nor would it deal with the problems that some Medicaid beneficiaries have with access to health care providers. It also would not address potential differences in benefits between those available under Medicare and those that will be available through the exchanges.

- Hold states harmless for all of the additional cost of covering 65- and 66-year-olds through Medicaid . As noted, states would see higher Medicaid costs for 65- and 66-year-olds under this proposal. States should permanently receive a 100-percent federal match for this population to ensure that the federal government does not shift a large share of the costs to the states. If Congress adopts the proposal for a blended Medicaid matching rate, it should either exclude 65- and 66-year-olds from the blended rate and provide a full 100-percent match or increase the blended rate to take into account the phase-in of the higher eligibility age. [6]

- Make all 65-and 66-year-olds who qualify for premium credits eligible for cost-sharing subsidies as well . Under the ACA, cost-sharing subsidies are available only to individuals with incomes below 250 percent of the poverty line, and the subsidies for those between 200 and 250 percent of poverty are very modest. People aged 65 or 66 require more health care, on average, and hence incur greater cost-sharing expenses than younger people. Some 65- and 66-year-olds — especially those who are in poor health — could face significantly higher cost-sharing charges in the exchange than under Medicare. Therefore, if Congress raises the Medicare eligibility age, it should increase the cost-sharing subsidies for 65- and 66-year-olds between 200 and 250 percent of poverty and extend the subsidies to income levels somewhat above 250 percent of poverty, which is now only $27,225 for an individual living alone.

End Notes

[1] Congressional Budget Office, Reducing the Deficit: Spending and Revenue Options, March 2011, pp. 45-6.

[2] Tricia Neuman, Juliette Cubanski, and others, Raising the Age of Medicare Eligibility: A Fresh Look Following the Implementation of Health Reform, Kaiser Family Foundation, July 2011, http://www.kff.org/medicare/8169.cfm.

[3] Kaiser Family Foundation, Health Reform Subsidy Calculator, http://healthreform.kff.org/subsidycalculator.aspx.

[4] Edwin Park and Judith Solomon, Proposal to Establish Federal Medicaid "Blended Rate" Would Shift Significant Costs to States, Center on Budget and Policy Priorities, June 24, 2011, https://www.cbpp.org/sites/default/files/atoms/files/6-24-11health.pdf.

[5] Paul N. Van de Water, "Ryan Budget Would Increase Health Care Spending for Medicare Beneficiaries," Off the Charts blog, April 8, 2011, http://www.offthechartsblog.org/ryan-budget-would-increase-health-care-spending-for-medicare-beneficiaries/ .

[6] For an analysis of the problems with the blended rate proposal, see Park and Solomon,

.More from the Authors