Proposed Cap on Federal Spending Would Force Deep Cuts in Medicare, Medicaid, and Social Security

Would Likely Require Radical Changes Such As Medicare Privatization, a Medicaid Block Grant, and Repeal of Health Reform

Summary

A prominent proposal by Senators Bob Corker (R-TN) and Claire McCaskill (D-MO) to limit total federal spending to no more than 20.6 percent of the Gross Domestic Product (GDP), which is attracting increasing attention, may sound benign, but it would inevitably force enormous cuts in Medicare, Medicaid, and possibly Social Security.

The Corker-McCaskill bill would impose automatic, across-the-board cuts (a “sequester”) to close the gap between projected spending and the proposed cap if the cap would otherwise be breached. If the cuts needed to reach the cap were achieved entirely through this mechanism, the estimated cuts would total about $1.3 trillion in Social Security, $856 billion in Medicare, and $547 billion in Medicaid over the first nine years that the cap was in effect, from 2013 through 2021. These figures are based on Congressional Budget Office (CBO) projections of spending over the next decade under current policies and on the Corker-McCaskill formula for how across-the-board cuts would be imposed.

The cuts in Social Security, Medicare, Medicaid, and other programs would grow much larger in subsequent decades. For one thing, the 20.6 percent cap would phase in gradually and would not be fully in effect until 2023 and thereafter. [1] For another, Social Security, Medicare, and Medicaid costs are projected to rise substantially in future decades due to the aging of the population and rising health care costs and, thus, would have to be cut by increasingly severe amounts to meet the Corker-McCaskill level.

Policymakers could avoid across-the-board cuts by making specific cuts in specific programs to meet the Corker-McCaskill cap before a sequester would occur. But to do so, they almost certainly would have to enact the kind of radical policies for Medicare and Medicaid that are included in House Budget Committee Chairman Paul Ryan’s sweeping budget plan. Those policies include replacing traditional Medicare with a voucher for purchasing private insurance, converting Medicaid to a block grant, and eliminating most or all of health reform’s provisions that extend coverage to an estimated 34 million more Americans, including the Medicaid expansion and subsidies to make insurance affordable for working families. Indeed, even the cuts in the Ryan plan — which also includes very sharp reductions in non-security discretionary spending, one-third of which would be eliminated by 2021 — would not be quite deep enough in some years to meet the Corker-McCaskill cap. The Ryan plan produces total federal spending of 20 ¾ percent of GDP in 2030.[2] (See the box below.)

The negative effects of a cap on total spending would be even more severe under another recent and prominent proposal. A proposed balanced-budget amendment to the U.S. Constitution that Senate Republican leaders unveiled on March 31 would cap federal spending in any fiscal year at 18 percent of what GDP was in the prior calendar year, which is equivalent to a cap on spending of about 16.7 percent of the current year’s GDP. That would necessitate even deeper cuts in Medicare, Medicaid, and Social Security.

Proposals such as Corker-McCaskill and the Senate Republican leaders’ constitutional amendment also seem intended to ensure that increases in revenues will not play any part in the effort to bring long-term deficits under control.

Cap Would Drive Substantial Cuts in Medicare, Medicaid, And Social Security Over the Next Decade

Under Corker-McCaskill, the cuts required to close the gap between projected total spending and the proposed cap would be large from the outset and would grow much larger over time. They would start at about $110 billion in the first year (2013), and rise to about $670 billion in 2021. [3] If the cuts came entirely through the sequester, Medicare, Medicaid, Social Security, and other mandatory programs all would be cut 19 percent in 2021. (Under the bill’s sequester mechanism, all mandatory programs would be cut by the same percentage, as explained further in the appendix.) In dollar terms, mandatory programs would be cut by nearly $630 billion in 2021. Social Security would be cut by $237 billion, Medicare by $161 billion, and Medicaid by $105 billion. As noted earlier, from 2013 through 2021, the cumulative cuts would total about $1.3 trillion in Social Security, $856 billion in Medicare, and $547 billion in Medicaid (see Table 1).

If, instead of following the Corker-McCaskill formula for automatic cuts, all programs were cut by the same percentage, then all programs would be cut 14 percent in 2021 — or one of every seven dollars. Over the 2013-2021 period, the cuts would total $904 billion in Social Security, $602 billion in Medicare, and $386 billion in Medicaid.

| Table 1: Cuts in Medicare, Medicaid, and Social Security Over Next Decade Under Corker-McCaskill’s Automatic Mechanism (in billions of dollars) | ||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2013-2021 | |

| Medicare | -28 | -47 | -66 | -93 | -97 | -101 | -122 | -141 | -161 | -856 |

| Medicaid | -14 | -27 | -41 | -59 | -64 | -67 | -80 | -91 | -105 | -547 |

| Social Security | -41 | -71 | -100 | -138 | -147 | -157 | -184 | -210 | -237 | -1,285 |

| Percentage Cut | -5% | -8% | -11% | -15% | -15% | -15% | -16% | -18% | -19% | |

| Source: CBPP analysis based on Congressional Budget Office data. | ||||||||||

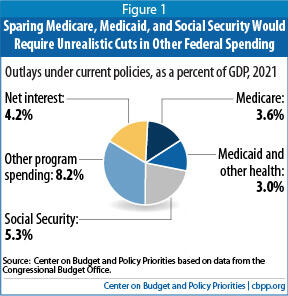

There is little possibility that Medicare, Medicaid, and Social Security all would be exempted from these cuts. To do that would require cutting everything else — including defense, veterans’ programs, education, scientific research, and the like — by unthinkable amounts. In 2021, under current policies, spending for Medicare, Medicaid (and other health programs), and Social Security will be 45 percent higher than spending for all other programs (except interest payments) combined. (See Figure 1.) Thus, to meet the tight Corker-McCaskill target, cuts in those programs would be simply unavoidable. If policymakers decided to exempt Social Security from cuts, they would have to make even deeper cuts in Medicare and Medicaid as well as in areas like education, veterans’ health care, and transportation, among others.

Moreover, the cuts would have to be even larger if the economy faltered. The costs for a number of key programs as currently structured — such as unemployment insurance, food stamps, and Medicaid — rise significantly during an economic downturn, as people lose their jobs, wages, and employer-based health coverage. Similarly, interest rates can rise unpredictably due to a variety of economic developments; if that occurred, it would push up the federal government’s interest costs — and require commensurately deeper budget cuts (since interest payments would count as federal spending that is included under the cap). In addition, if federal policymakers chose to further cut taxes, that would increase the government’s borrowing and hence its interest costs, necessitating still deeper budget cuts to keep total federal expenditures within the cap.

Policymakers, of course, could avoid automatic cuts by making the necessary policy changes to reduce spending. But the steps they would have to take would be dramatic, to say the least. In a sense, the Ryan budget plan serves as a useful guide to the types of changes that would inevitably occur. As noted, in some years, even the radical proposals in the Ryan plan would barely prove sufficient or fall a bit short of meeting the Corker-McCaskill target.

The Ryan plan, which would cut Medicaid by $1.4 trillion over the next decade and cut non-security discretionary programs by a stunning 33 percent by 2021, would shrink total federal spending to 20 ¼ percent of GDP in 2022. But, under the Ryan plan, federal spending would be 20 ¾ percent of GDP in 2030, slightly above the Corker-McCaskill cap, even though Ryan’s Medicaid and non-security discretionary cuts would be even deeper by then and his massive Medicare cuts would have begun to kick in with force. A typical Medicare beneficiary who turned 65 in 2022 would pay more than twice as much — or $6,350 a year more — for health care out of his or her own pocket under the Ryan plan than under current law. Rather than paying an average of $6,150 out of pocket in 2022, he or she would pay an average of $12,500. [4]

Historical Spending Averages Bear Little Relevance for the Future

Corker-McCaskill’s proponents often note that its 20.6 percent target equals the average share of GDP that federal outlays represented over the last three decades of the previous century and the first years of this one. But that average bears little relevance to the circumstances that we will face in the decades ahead, due to the aging of the population, the fact that health care costs are far higher than they were several decades ago, and several important decisions and developments of recent years.

The percentage of Americans who are 65 or older will grow by more than half over the next 25 years, and increases in costs across the health care system — both public and private — will raise the cost of providing health coverage to seniors, people with disabilities, and people with low incomes. In addition, the federal government faces costs that it did not face in most of the previous decades — for homeland security (after the September 11 terrorist attacks), for health care and other benefits and services to veterans of the Iraq and Afghanistan wars, for the Medicare prescription drug benefit enacted in 2003, and for interest on a federal debt that has grown dramatically due to these other factors as well as the very costly 2001 and 2003 tax cuts and the costs of addressing the most severe recession since the Great Depression.

As a result, there would be no practical way to meet Corker-McCaskill’s target without making extremely large cuts in Medicare, Medicaid, and Social Security – the programs that, together, will account for about 45 percent of non-interest spending this year and are scheduled to account for nearly 60 percent by 2021.

That is why budget experts have warned that a spending cap at 20 or 21 percent of GDP is extremely unrealistic and would be impossible to achieve without draconian budget cuts.[5]

For example, a report issued a year ago by a National Academy of Sciences expert committee on deficits outlined four possible paths to stabilize the debt.[6] As panel co-chair and former CBO director Rudolph Penner explained, the panel designed paths at two “extremes” — one that achieved all of its deficit reduction by cutting programs and another that achieved nearly all of it by raising taxes — and two intermediate paths (which Penner and most other panel members saw as more realistic) that blended program and tax changes. The extreme low-spending path — the one that achieved all of its deficit reduction by cutting programs — included very deep cuts in Social Security, Medicare, and Medicaid, plus cuts of about 20 percent in all other spending, including defense, veterans’ programs, education, and the like. Even under this extreme path, total spending would be about 21 percent of GDP.

Indeed, federal spending under President Ronald Reagan averaged 22 percent of GDP, at a time when no baby boomers had yet retired and health care costs were more than a third lower as a share of GDP than they are today. As commentator and former OMB official Matt Miller has written, “As a matter of math, if you run the government at a smaller level than did Ronald Reagan while accommodating this massive increase in the number of seniors on our health and pension programs, you have to decimate the rest of the budget.” [7]

These realities make it impossible to impose the type of spending cap that the Corker-McCaskill bill and the Senate Republican balanced-budget amendment would erect without budget cuts of almost unimaginable depth.

What the Corker-McCaskill Cap Would Mean for Medicare, Medicaid, Health Reform, and Social Security

Medicare and Medicaid: Cuts of the depth that the cap would require would necessitate radical restructuring of Medicare and Medicaid. Limited changes to Medicare and Medicaid could not produce anything close to the amount of savings that would be needed. The only practical way to generate savings of that magnitude would be to replace traditional Medicare with a voucher for the purchase of private insurance and to convert Medicaid to a block grant, as the Ryan plan would do. Both the amount of the Medicare voucher and the Medicaid block grant level would have to be set so they increased from year to year at rates well below the rate of increase in health care costs, making these programs increasingly inadequate over time for the tens of millions of Americans who rely on them. These changes would shift costs substantially to beneficiaries, health care providers, and states. They almost certainly would lead to large increases in the ranks of the uninsured and to reduced access to needed health care services and treatments and to long-term care services and supports.

Health reform: The cap would preclude the increased federal expenditures that would result from insuring more Americans under the Affordable Care Act, even though that law more than offset its increased expenditures through a combination of increased revenues and other spending reductions. To keep federal spending below the cap, Congress would have to eliminate most or all of the law’s provisions extending coverage to an estimated 34 million Americans who would otherwise be uninsured.

Social Security: Current Social Security beneficiaries and those close to retirement would likely face substantial benefit reductions. The coming growth in Social Security benefit expenditures — chiefly associated with providing benefits to the growing numbers of retirees as the population ages — would have to be addressed, either through cuts in Social Security benefits or through even deeper cuts in other programs, likely including Medicare and Medicaid.

Congress would not be able to avert this result or soften the blow by increasing Social Security revenues, such as by raising the level of earnings subject to the Social Security payroll tax — because that would have no bearing on whether total federal expenditures fit within the spending cap. Likewise, the existence of Social Security’s trust fund — which currently has assets of $2.7 trillion and is still growing — would have no effect on the required cuts. If other programs could not be cut enough to offset the projected increase in Social Security benefits, as likely would be the case, Social Security benefits would have to be cut. The cuts needed to comply with the spending cap could be much larger than those in any current proposal to restore Social Security’s long-term solvency and probably would have to apply to current beneficiaries and those who are now nearing retirement, since the cap would begin hitting in 2013 and would grow tighter each year after that.

Capping Spending at or Below the Historical Average Would Necessitate Even More Severe Cuts in Future Decades

The Corker-McCaskill spending cap would first take effect in 2013. It would then steadily tighten, dropping to 20.6 percent of GDP in 2023 and beyond. This 20.6-percent level is the historical average for fiscal years 1970 through 2008 (although spending fluctuated during this period). But as explained below, this target ignores long-term demographic shifts and trends in health care costs and also fails to take into account important recent fiscal and economic developments.

Two trends drive the long-term growth in federal health programs and Social Security:

- The U.S. population is aging. The proportion of the population aged 65 and over will grow from 13 percent in 2010 to 20 percent by 2035, before beginning to level off. That will significantly increase the number of people who are eligible for Medicare, Medicaid, and Social Security over the next 25 years.

- Costs throughout the U.S. health care system are expected to continue to grow considerably faster than the economy. [8] Although the Affordable Care Act takes important steps to begin to slow this growth, overall health care costs will almost certainly continue to rise faster than GDP— and hence, so will Medicare and Medicaid costs — as new technologies and treatments emerge that improve health but increase costs.

Because the aging of the population will eventually stabilize, Social Security expenditures will level off as a share of the economy after 2035. In contrast, Medicare and Medicaid (and other major federal health programs) will continue rising as a percentage of GDP.

The idea of capping total federal spending at the average of previous decades, as the Corker-McCaskill bill would do, ignores these demographic and health-cost trends. It also ignores the greater responsibilities that the federal government has assumed over the last decade, including sharply increased spending for homeland security following the terrorist attacks, increased spending to provide health care to veterans of the wars in Iraq and Afghanistan, and new costs for the Medicare prescription drug benefit.

The cap would require total federal expenditures to remain constant year after year as a share of GDP, even as the share of the population that is elderly grows substantially. Although further steps must be taken to slow the rise of health care costs, those costs are still very likely to rise faster (throughout the U.S. health care system) than overall inflation. To comply with the cap, therefore, Congress would effectively have to eliminate most or all of the expected growth in Medicare, Medicaid, and Social Security that results from these factors. That would require imposing cuts of stunning depth in Medicare, Medicaid, and Social Security, with the cuts growing steadily deeper over time.

Cap Would Require Radical Restructuring of Medicare and Medicaid

To stay below the cap, Congress would have to enact steep budget cuts over the next ten years and much deeper cuts in subsequent decades. If it did not, automatic budget cuts would be applied to federal spending to produce the needed reductions.

As noted, the principal programs slated to grow significantly faster than GDP are Medicare and Medicaid. Limited changes to these programs could not produce budget cuts of the magnitude that would be needed to freeze total federal expenditures as a share of GDP. The only way to generate savings of the magnitude required would be to radically restructure these programs.

Eliminating Traditional Medicare

As discussed above, Medicare could face cuts of 14 to 19 percent by 2021 and much deeper cuts after that. Due to the aging of the population, the number of Medicare beneficiaries is projected to rise from 47 million in 2010 to 85 million by 2035. [9] In addition, Medicare costs per beneficiary are expected to continue to outpace growth in GDP per capita in the decades ahead. And while the aging of the population and, hence, Medicare enrollment growth should stabilize after 2035, costs per beneficiary will continue to grow, in significant part because baby boomers will become older and more frail in subsequent decades. Medicare beneficiaries aged 85 and older cost more than twice as much to cover as beneficiaries aged 65-74, because of their poorer health.[10] This means that Medicare would have to be cut in coming decades severely enough to entirely offset the higher costs that would result both from the large increases in enrollment as the population ages and from continued health care cost growth. The cuts that would be required would be so massive as to be almost unimaginable.

Replacing Medicare’s guaranteed benefit with a voucher for the purchase of private health insurance, as the Ryan budget plan would do, would be a likely way to force Medicare costs to grow no faster than the economy. Initially, the voucher could be set at (or perhaps somewhat below) average current Medicare spending per beneficiary. But to keep Medicare expenditures from growing faster than the economy, the amount of the voucher would have to be increased each year at a rate much slower than the economic growth rate — and well below the rate of growth in U.S. health care costs — in order to compensate for the added Medicare costs that will result from the rising number of beneficiaries. The Ryan plan, for example, would adjust the vouchers only by the general inflation rate, which is about three percentage points per year less than the rate at which health care costs have been growing. [11]

Beneficiaries would find that their voucher would not allow them to purchase health coverage comparable to what Medicare provides. The value of the voucher would have to decline each year relative to the costs of a reasonable health insurance package. Medicare benefits already are less comprehensive than a typical employer-sponsored health plan. With Medicare vouchers designed to keep Medicare costs relatively flat as a share of GDP even as health care costs increased and the elderly population grew, coverage would become increasingly skimpy over time. Seniors and people with disabilities who could afford to supplement the coverage that their voucher would buy would do so. Many seniors, however, would not be able to afford that. (The typical Medicare beneficiary had total household income of $22,800 a year in 2006. [12]) Seniors of modest means would increasingly face rationed or second-class health care.

Making this problem more acute, the privatization of Medicare — i.e., switching to vouchers that people would use to purchase coverage from private insurance companies — would, by itself, significantly raise costs per beneficiary. Traditional Medicare generally pays less to providers and incurs lower administrative and marketing costs than private insurance does. [13] Indeed, CBO estimates that in 2022, when the Ryan budget plan’s vouchers would first take effect for new beneficiaries, the cost per beneficiary of a private plan offering comparable benefits would be 40 percent higher than the cost of the traditional Medicare program. [14] As a result, not only would the voucher amounts fall steadily farther behind health care costs, but each dollar the government spent on a voucher would tend to buy less in actual health care services than each dollar in the traditional Medicare program. Seniors and people with disabilities who could not afford to buy additional coverage would receive only whatever benefits the private insurers offered to provide for the voucher amount, which as noted would fall further in health care purchasing power each year.

Over time, many Medicare beneficiaries would become underinsured. Beneficiaries also would be likely to face significantly higher deductibles and co-insurance payments, which many could have difficulty affording given their limited incomes. Some beneficiaries could end up uninsured if they could not afford their share of the premium.

Block-Granting Medicaid

Medicaid, too, would have to be cut deeply to keep federal spending within the cap. Policymakers likely would find little alternative to converting the program to a block grant, as the Ryan budget plan would do. Under current law, the federal government pays a fixed percentage of states’ Medicaid costs; under a block grant, it would pay only a fixed dollar amount, irrespective of state needs, with states responsible for all costs above that amount.

A block grant could help ensure that total federal spending stayed under the cap by capping federal Medicaid funding and adjusting the block grant amounts only to keep pace with growth in the economy. This would result in deep and rapidly growing reductions in federal Medicaid funding over time, relative to current law. Block-granting Medicaid thus would shift large costs to states as the population ages and health care costs continue to rise. [15] The federal funding reductions (relative to current law) would be especially severe in years when states experience higher enrollment due to a recession or greater medical costs due to an epidemic or new disease (such was the case when the HIV/AIDS epidemic struck in the late 1980s and 1990s) or a medical breakthrough (such as the anti-retroviral drugs developed to deal with HIV/AIDS), since federal funding would no longer respond automatically to those higher costs as it does today.

As CBO has noted in its analysis of the Ryan plan, states would have to compensate for the large federal funding reductions either by contributing substantially more of their own funds (by raising taxes or cutting other programs) or — as is much more likely — by using the greater flexibility they would receive under a block grant to roll back coverage for hundreds of thousands or millions of low-income children, seniors, people with disabilities, and/or working parents who rely on the program, and to cut already-low payments to providers still lower. [16] A block grant typically allows states to override most federal requirements related to eligibility and benefits; many states undoubtedly would use this flexibility to institute major reductions in eligibility and benefits, and/or to sharply raise premiums and cost-sharing charges, in response to the sharp reductions in federal Medicaid funding they would face.

Seniors and people with disabilities would likely be at the greatest risk. They constitute one-quarter of Medicaid beneficiaries — but account for two-thirds of all Medicaid expenditures because of their greater health care needs and because Medicaid is the primary funder of long-term care services and supports, including nursing home care.

States almost certainly would also institute substantial cuts in reimbursement rates for hospitals, physicians, nursing homes, pharmacies, managed care plans, and other providers that furnish care to Medicaid beneficiaries. Many of these providers would likely respond by withdrawing from the program. The end result would likely be much greater numbers of poor Americans who are uninsured or underinsured.

Spending Cap Would Likely Require Repeal of Major Coverage Elements of Health Reform

Setting a federal spending cap at or below 20.6 percent of GDP would not allow for expenditures that would result from the Affordable Care Act (even though the Act more than offset those increased costs through a combination of increases in revenues and other spending reductions). To keep total federal expenditures within the cap, Congress would almost certainly have to repeal (as the Ryan budget plan would do) or cut deeply most or all of the spending related to the two major elements of the law that will reduce the number of uninsured people — the premium and cost-sharing subsidies for the purchase of coverage in the new health insurance exchanges, and the law’s Medicaid expansion. [17]

If the premium and cost-sharing subsidies were eliminated or sharply reduced, health coverage offered through the new exchanges would become increasingly unaffordable for many. That would make it impossible to continue to require people to obtain health insurance or pay a penalty. Healthier people would be the most likely to decline to purchase coverage without adequate subsidies and without an individual mandate. And if large numbers of healthier people opted not to participate in the exchanges, that would drive up overall premiums for people in the exchanges, encouraging even more people to go without exchange coverage. The exchanges would be at grave risk of failing over time.

In addition, the sharp decline in federal Medicaid funding under a federal spending cap would render the health reform law’s Medicaid expansion unworkable. It is hard to see how the federal government could still require states to institute that expansion.

In short, enactment of the federal spending cap would provide a backdoor way to make repeal of health reform virtually inevitable. Instead of declining, the number of uninsured people likely would rise — and by a considerable amount over time.

Spending Cap Would Require Large Cuts in Social Security Over Both the Near and Long Term

The proposed cap on total federal spending also would likely lead to significant cuts in Social Security benefits within a few years.

Social Security benefits are projected to grow from 4.8 percent of GDP today to 6.2 percent of GDP in 2035 as the members of the post-World War II baby boom generation move into their retirement years. Under current law, that increase in costs will be partly financed by drawing down Social Security’s $2.7-trillion trust fund, which has been accumulated since 1983 for exactly that purpose. Under an overall spending cap, however, any rise in spending for Social Security would have to be offset by a corresponding decrease in other spending — even if the Social Security program itself is adequately financed. The option of raising the level of earnings subject to the Social Security payroll tax — or adopting other measures to increase Social Security revenues — to cover growing Social Security costs would be taken off the table. If other spending could not be reduced by enough to offset the rise in Social Security benefits, as would very likely be the case, Social Security benefits themselves would have to be cut to fit within the cap.

The resulting cuts in Social Security benefits would be sharper and more immediate than those under any current proposal to ensure the program’s long-term solvency. As explained earlier, the Corker-McCaskill bill would likely require cuts of 14 percent to 19 percent in 2021 in expenditures for mandatory programs (other than interest payments), and sparing Social Security, Medicare, and Medicaid would likely not prove feasible.

This timetable would allow little time to phase in Social Security benefit cuts in a way that would spare current beneficiaries and those close to retirement. In contrast, all major proposals to reduce Social Security benefits to help achieve long-term Social Security solvency promise to protect everyone currently over age 55.

For example, the Bowles-Simpson proposal (which CBPP analyses have found to be too harsh to low- and modest-income seniors and people with disabilities) would largely shield people now 55 or older. [18] Bowles-Simpson would reduce aggregate Social Security benefits by less than 2 percent in 2021. This is a fraction of the likely benefit cuts under the Corker-McCaskill bill.

Appendix: How Would the Corker-McCaskill Cuts Be Enforced?

The outlay targets in the Corker-McCaskill bill would require large budget cuts. Congress could meet the targets by enacting reductions in specific programs. If such cuts were not enacted, automatic cuts would be triggered — a practice known as “sequestration.”

Under the bill, if the Office of Management and Budget determined that the spending cap would be exceeded and sequestration was therefore required, automatic cuts would be instituted that fell most heavily on the fastest-growing categories of spending. The bill divides non-interest outlays into three categories — discretionary (appropriated) security spending, discretionary non-security spending, and mandatory spending. The bill requires that separate budget-cut percentages be applied to each of these three program categories in proportion to that category’s share of total expenditure growth from one year to the next. As a result, the brunt of the automatic cuts would fall on mandatory spending. The discretionary spending categories, which are growing fairly slowly, would bear much smaller reductions.

| Table 2: Spending Cuts by Major Category Over Next Decade Under Corker-McCaskill Automatic Mechanism (in billions of dollars) | ||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2013-2021 | |

| Defense discretionary | 0 | 0 | 0 | -2 | -3 | -3 | -9 | -13 | -18 | -47 |

| Nondefense discretionary | 0 | -1 | -4 | -8 | -9 | -9 | -13 | -18 | -23 | -84 |

| Mandatory | -110 | -189 | -267 | -377 | -397 | -413 | -490 | -557 | -629 | -3,429 |

| TOTAL | -110 | -190 | -271 | -387 | -408 | -425 | -512 | -588 | -670 | -3,561 |

| Percentage cuts | ||||||||||

| Defense discretionary | 0 | 0 | 0 | * | * | * | -1 | -2 | -3 | |

| Nondefense discretionary | 0 | * | -1 | -1 | -1 | -1 | -2 | -3 | -3 | |

| Mandatory | -5 | -8 | -11 | -15 | -15 | -15 | -16 | -18 | -19 | |

| TOTAL | -3 | -5 | -7 | -10 | -10 | -10 | -12 | -13 | -14 | |

| *less than 0.5 percent. Source: CBPP analysis based on data from the Congressional Budget Office. The current-policy projections used by CBPP adjust the CBO baseline projections to assume extension of expiring tax cuts and relief from the Alternative Minimum Tax, phasedown of operations in Iraq and Afghanistan, and continuation of the 2011 Medicare physician-payment rates (instead of the 28 percent reduction in 2012 required under the program’s Sustainable Growth Rate formula). See James R. Horney and Kathy A. Ruffing, “Federal Debt on Unsustainable Path Under Current Policies,” Center on Budget and Policy Priorities, January 31, 2011. The baseline used in this paper reflects minor changes to those earlier projections to incorporate CBO’s March 2011 update. | ||||||||||

Within each category, a uniform percentage reduction would apply to all programs. There would be no exemptions. Many programs that were exempt from automatic cuts under the Gramm-Rudman-Hollings sequestration procedures and remain exempt today under the Pay-As-You-Go law’s sequestration rules — including Social Security, Medicaid, the Supplemental Nutrition Assistance Program (food stamps), unemployment insurance, the Earned Income Tax Credit, and veterans’ benefits —would fall under the ax here.

Complying with the Corker-McCaskill caps would require large cuts starting in 2013. In 2021, total non-interest outlays would need to be cut by 14 percent, compared with current policies. If those savings were accomplished through sequestration (or by congressional actions that mimic the effects of sequestration) cuts of 19 percent would be required in mandatory programs (including Medicare, Medicaid, and Social Security). Cuts of 3 percent would be triggered in discretionary programs (see Table 2).

End Notes

[1] The Corker-McCaskill bill (S. 245) sets a cap on federal outlays for fiscal years 2013 through 2022, but the sponsors clearly intend their 20.6 percent of GDP target to continue permanently.

[2] House Committee on the Budget, “The Path to Prosperity: Restoring America’s Promise,” April 2011, budget.gop.gov; Congressional Budget Office, “Long-Term Analysis of a Budget Proposal by Chairman Ryan,” April 8, 2011.

[3] Spending cuts of $850 billion would be needed in 2021. If policymakers complied with the Corker-McCaskill cap in all years and enacted no new, unpaid-for tax cuts, interest costs would be about $180 billion lower in 2021 than under current policies. This would leave $670 billion to be cut from federal programs in that year. See the appendix for further details.

[4] See Paul N. Van de Water, “Ryan Budget Would Increase Health Care Spending for Medicare Beneficiaries,” OfftheCharts blog, April 8, 2011.

[5] See Paul N. Van de Water, “Corker-McCaskill Spending Cap Doesn’t Account for Basic Changes in Society and Government,” Center on Budget and Policy Priorities, February 1, 2011.

[6] National Research Council and National Academy of Public Administration, “Choosing the Nation’s Fiscal Future,” January 2010.

[7] Matt Miller, “A spending goal too small for aging America,” Washington Post, July 28, 2010.

[8] Between 1975 and 2008, annual growth in federal health spending per beneficiary, on average, exceeded annual growth in GDP per capita by 1.9 percentage points, though the difference declined to 1.4 percentage points over the last two decades (1990-2008). Notably, Medicaid costs per beneficiary have grown substantially slower than Medicare and other federal health programs since 1990 and have grown, on average, nearly three percentage points per year more slowly than private insurance premiums over the last decade. Congressional Budget Office, “The Long-Term Budget Outlook,” op. cit. and John Holahan et al., “Medicaid Spending Over the Last Decade and the Great Recession,” Kaiser Commission on Medicaid and the Uninsured, February 2011.

[9] “2010 Annual Report of the Board of Trustees of the Federal Hospital Insurance and Federal Supplementary Insurance Trust Funds,” August 2010.

[10] Lisa Potetz, Juliette Cubanski, and Tricia Neuman, “Medicare Spending and Financing: A Primer,” Kaiser Family Foundation, February 2011.

[11] Robert Greenstein, “CBO Report: Ryan Plan Specifies Spending Path That Would Nearly End Most of Government Other Than Social Security, Health Care, and Defense by 2050,” Center on Budget and Policy Priorities, April 7, 2011.

[12] Juliette Cubanski and others, “Medicare Chartbook,” Kaiser Family Foundation, 2010, p. 15.

[13] Douglas W. Elmendorf, Director, Congressional Budget Office, Letter to the Honorable Paul D. Ryan, November 17, 2010.

[14] Congressional Budget Office, “Long-Term Analysis of a Budget Proposal by Chairman Ryan,” April 5, 2011.

[15] See Edwin Park and Matt Broaddus, “Medicaid Block Grant Would Shift Financial Risks and Costs to States,” Center on Budget and Policy Priorities, February 23, 2011. See also Edwin Park, “Medicaid Block Grant or Funding Caps Would Shift Costs to States, Beneficiaries, and Providers,” Center on Budget and Policy Priorities, January 6, 2011.

[16] Congressional Budget Office, “Long-Term Analysis of a Budget Proposal by Chairman Ryan,” April 5, 2011.

[17] The premium subsidies are provided as tax credits, but more than two-thirds of the premium subsidy costs will count as federal spending because credits provided on a “refundable” basis (i.e., credits that exceed a household’s federal income tax liability) are considered outlays rather than reduced revenues. The cost-sharing subsidies are not provided as tax credits, so all of those costs would be considered federal spending.

[18] Kathy Ruffing and Paul N. Van de Water, “Bowles-Simpson Social Security Proposal Not a Good Starting Point for Reforms,” Center on Budget and Policy Priorities, February 17, 2011.

More from the Authors

Areas of Expertise

Areas of Expertise