Pension Bill Conference Report May Make Some 2001 Tax Cuts Permanent without Offsetting Their Costs

Bill Could Set Precedent for Other Unpaid-For Tax-Cut Extensions

Summary

Pension legislation passed by the House late last year included provisions that would make permanent the higher contribution limits for tax-preferred retirement savings accounts enacted in 2001. The pension bill conferees reportedly are considering including these provisions in the pension bill conference report, without offsetting their cost.

According to Joint Committee on Taxation estimates, making the higher contribution limits permanent would cost about $34 billion between 2007 and 2016. Moreover, that ten-year cost estimate reflects only six years of the cost of extending these tax cuts, because they do not expire until the end of 2010.

Of greater concern, making the pension-related provisions of the 2001 tax cut permanent could set a precedent for extending other tax cuts enacted since 2001 without paying for them, an approach that ultimately could add as much as $3.3 trillion to deficits over the next decade. Extending the pension-related 2001 tax cuts now would contravene the principle, laid out by former Federal Reserve Chair Alan Greenspan among others, that expiring tax cuts should be extended only if offset.

It also would be irresponsible to rush to extend these tax cuts for several additional reasons:

-

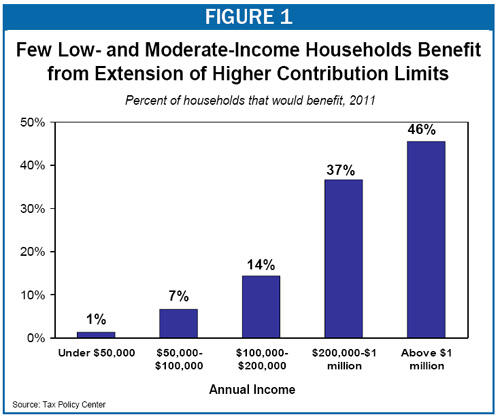

First, these provisions primarily benefit high-income households and provide little or no assistance to low- and moderate-income taxpayers attempting to save for retirement. According to the Urban Institute-Brookings Institution Tax Policy Center, only 6 percent of all households — and only 1 percent of households with incomes below $50,000 — would benefit at all from the extension of these provisions. In contrast, nearly half of the households with incomes above $1 million would benefit. And overall, about three-quarters of the tax benefits would go to the less-than-one-sixth of taxpayers with incomes over $100,000 a year.

-

Second, although the purported goal of raising the contribution limits for tax-preferred savings accounts is to increase personal saving, there is no evidence that higher contribution limits actually have this effect. The data needed to assess the impact of the 2001 pension tax cuts on saving is not yet available. Moreover, as the Congressional Research Service recently reported, broader research on tax-preferred savings accounts has found that such accounts “appear to be relatively ineffective in inducing new saving,” and that when their effects in increasing the budget deficit are taken into account, “the long-term effect on national savings and economic growth is likely negative.” [1] In acting now to extend the 2001 provisions, Congress would be spending billions of dollars to make these tax cuts permanent without waiting for evidence on their effects, and in the face of evidence that other, similar provisions have proven ineffectual.

-

Finally, conferees are reportedly considering making the increases in contribution limits permanent while only temporarily extending the saver’s credit, the one provision of the 2001 tax cut that was intended to provide low- and moderate-income households with incentives to save. This approach is not only inequitable; it also ignores evidence that savings incentives targeted to low- and moderate-income households are effective.

The Cost of Extending the 2001 Increases in Savings Account Contribution Limits

The major tax legislation enacted in 2001 included several provisions that expanded tax incentives for retirement saving. One of these provisions, discussed below, created a tax credit to encourage saving among low- and moderate-income households. Other provisions increased the contribution limits for Individual Retirement Accounts (IRAs) and employer-sponsored defined contribution retirement plans (such as 401(k)s). The 2001 legislation gradually increased the contribution limit for IRAs from the existing limit of $2,000 per person per year to $5,000 by 2008; after 2008, the $5,000 limit will be increased each year to reflect inflation. Similarly, the 2001 legislation increased the contribution limit for how much employees may contribute to their 401(k)s each year from $10,500 to $15,000 by 2006, with this limit, too, indexed for inflation in years after that.[2]

The House pension bill would make these provisions permanent, at a cost of $34 billion between 2007 and 2016, according to Joint Committee on Taxation estimates. The Joint Tax Committee’s ten-year figures, however, reflect only six years of the cost of extending the measures, which do not expire until the end of 2010. Of the projected $34 billion ten-year cost of extending these tax cuts, $32 billion — or over 90 percent of it — falls in the second five years of the budget window. The annual cost reaches almost $8 billion by 2016.[3]

Of even greater concern from a fiscal standpoint, making the 2001 pension tax cuts permanent without offsetting their cost could initiate a process by which many provisions of the 2001 and 2003 tax-cut legislation (and other expiring tax cuts) are made permanent in a piecemeal fashion over several years. If various tax cuts are each extended separately, less consideration likely will be given to their combined effect on long-term deficits. But, according to the Congressional Budget Office, making all expiring provisions permanent would reduce revenues by $2.8 trillion over the next ten years, adding $3.3 trillion to deficits when the increased interest on the debt is taken into account.

Such an addition to deficits does not become any more affordable simply because it is done piece by piece instead of all at once. Former Federal Reserve Chairman Alan Greenspan, among others, has stressed the importance of paying for tax-cut extensions when they are enacted, rather than allowing the fiscal impacts to mount.[4] It is not fiscally responsible to start down a path of making expiring tax cuts permanent without considering where that path could lead, and without reaching agreement on which tax cuts we can afford to extend and what offsets should be adopted to cover the costs.

Who Benefits from Increasing Savings Account Contribution Limits?

The pension provisions of the 2001 tax cut are often mistakenly perceived to be “middle-class” tax cuts, perhaps because many middle-income taxpayers contribute to 401(k)s, and smaller but still significant percentages contribute to IRAs. What is important to remember, however, is that the 2001 changes benefit only those IRA and 401(k) participants who would otherwise have maxed out their allowable contributions. Thus, in reality, the substantial cost of extending these provisions would be spent on tax cuts for high-income households, who are evidently the least in need of incentives and assistance to save.

Studies by the Treasury Department, the Congressional Budget Office, and the Employee Benefit Research Institute all indicate the that percentage of households that would otherwise have maxed out their allowable contributions is small, and tiny at low- and moderate-income levels.[5] A recent CBO study finds that, as of 2000, only about 6 percent of employees made the maximum allowable contribution to IRAs, and only about 2 percent made the maximum allowable contribution to 401(k)s. Further, a Treasury Department study, authored by current Deputy Assistant Secretary for Tax Analysis Robert Carroll, found that taxpayers who did not contribute at the maximum prior to an increase in contribution limits “would be unlikely to increase their IRA contributions if contribution limits were increased.”[6] For these reasons, a General Accounting Office study estimated in 2001 that increasing the contribution limits for 401(k)s would directly benefit fewer than 3 percent of those employees who participate in 401(k)s.[7]

CBO analyses also show that high-income taxpayers are far more likely to contribute the maximum amounts than low- and moderate-income taxpayers. Among workers with incomes above $160,000 who contributed to 401(k)s in 2000, CBO found that about 40 percent contributed the maximum amount. In contrast, of the far smaller percentage of workers with incomes below $40,000 who contributed to 401(k)s at all, only 1-2 percent made the maximum allowable contribution. [8]

CBO’s study of retirement account participation confirms the conclusions reached by the Urban Institute-Brookings Institution Tax Policy Center. TPC finds that only 6 percent of all households would receive any benefits from extending the higher contribution limits enacted in 2001. Yet more than one-thirdof households with incomes between $200,000 and $1 million — and nearly half of households with incomes above $1 million — would benefit, in contrast to about 1 percent of households with incomes under $50,000 (see Figure 1). The Tax Policy Center also estimates that three-quarters of the benefits of extending the provisions would go to the 16 percent of households with incomes above $100,000, while only 6 percent of the benefits would go to the 60 percent of households with incomes below $50,000.

Has Lifting Contribution Limits Boosted Retirement Saving?

The available evidence suggests that tax-preferred savings accounts are relatively ineffective in spurring additional saving and that raising contribution limits for these accounts may be especially ineffectual.

Certainly, a casual look at the historical record would lead one to suspect that tax-preferred savings accounts may have failed to achieve their goals. Over the past 20 years, Congress has repeatedly expanded tax-preferred savings accounts, and the cost of these tax expenditures has risen. Over the same period, the personal savings rate has fallen. In 2005, the personal savings rate turned negative for the first time since the Great Depression.[9]

Of course, it is possible that personal savings would have fallen even further without tax incentives. That is not, however, the general finding of careful empirical studies. Research suggests that increases in IRA and 401(k) contributions, especially by people at high-income levels, frequently represent shifts in assets to take advantage of the tax-preferred accounts, not new saving. For example, economists Eric Engen of the American Enterprise Institute and William Gale of the Brookings Institution found that high-income families tend to shift existing assets into 401(k)s to take advantage of pension tax breaks without increasing their current saving. Engen and Gale write that, “In the top earnings group [i.e. people with incomes above $75,000 in 1991], there appears to be no impact of 401(k)s on financial assets or wealth, and a significant reduction in other assets due to 401(k)s.”[10]

On the basis of this and other evidence, a recent Congressional Research Service report concludes that tax incentives “appear to be relatively ineffective in inducing new saving — many of the families benefiting from the tax incentives likely shifted funds from other saving accounts into the tax-preferred accounts.”[11] Such asset shifting is of particular concern in the case of the measures enacted in 2001. As discussed above, the increases in contribution limits enacted in 2001 primarily affect high-income households — the households most likely to simply shift assets — and thus are likely to be doing little to boost private saving even though they add to the deficit and thereby reduce public saving.

The data needed to directly assess the effects of the increases in contribution limits enacted in 2001 are not yet available, and it is possible that these changes will turn out to have had surprising positive consequences. But since the provisions do not expire until the end of 2010, there is simply no reason to rush to extend them now rather than waiting for more evidence to become available.

Furthermore, some analysts have warned that some of the pension provisions enacted in 2001 may reduce pension coverage for low- and moderate-income workers, by reducing incentives for small business owners to offer retirement plans for their employees. Because of the 2001 law, business owners will, by 2008, be able to put away $10,000 a year in IRAs for themselves and a spouse — $12,000 a year if the business owner is 50 or older — without having to set up an employer-sponsored retirement plan that also covers their employees. Prior to enactment of the 2001 tax law, business owners who wished to place more than $4,000 a year in a tax-advantaged retirement account for themselves and their spouse had to set up a plan that covered their employees as well. Some pension experts expect that this change in pension law will, over time, reduce the proportion of small business owners who offer retirement plans for their workers. This concern provides yet another reason to wait for more information to become available, rather than rushing to make the 2001 provisions permanent.

Inequitable Treatment of Low- and Moderate-Income Savers

As noted, the 2001 tax cut included one retirement saving incentive targeted to low- and moderate-income households: the saver’s credit. Taxpayers with incomes below $50,000 for a married couple (below $25,000 for an individual) are eligible to receive a tax credit of up to 10 percent, 25 percent, or 50 percent of the contributions (up to $2,000) that they have made during the year to employer-sponsored retirement plans or IRAs. (The credit rate depends on the taxpayer’s income.)

Considerable evidence suggests that tax incentives for low- and moderate-income taxpayers, unlike incentives directed at high-income taxpayers, can successfully spur new saving. A study by the Retirement Security Project, for example, found that, if appropriately designed, tax credits can induce increases in retirement saving by low- and moderate-income families, with larger credits resulting in more savings.[12]

The saver’s credit enacted in 2001 is limited, however, in several key respects. It is not refundable, which means that many low-income taxpayers cannot use it. For example, a couple with two dependent children that makes retirement contributions cannot benefit from this credit in 2006 unless its income surpasses $24,100. In addition, the credit rate phases down abruptly with income, and the limits are not indexed for inflation. Over time, therefore, families who use the saver’s credit and whose income merely keeps pace with inflation would experience reductions, often significant, in the value of their credit and would consequently face higher income taxes. In contrast, the higher contribution limits for IRAs and 401(k)s enacted in 2001 are indexed for inflation.

Also, unlike the other pension-related provisions of the 2001 tax cut, the saver’s credit is scheduled to expire at the end of this year. The House pension bill would make the saver’s credit permanent, but without fixing any of its limitations, and in particular, without indexing its income limits for inflation. Because of this flaw, the House bill — which might seem to permanently protect the credit — would, in fact, scale it back sharply over time and cause it eventually to disappear altogether.[13]

Moreover, the pension bill conferees reportedly are considering extending the saver’s credit only for a very brief period — possibly just one year — and doing so without addressing its flaws, even as they contemplate making the other 2001 pension tax cuts permanent, with their full inflation adjustments. A more logical strategy would be to respond to the recent research on low-income saving incentives by addressing at least one critical problem with the saver’s credit — the lack of inflation indexing — while deferring consideration of the other pension-related tax cuts, which do not expire for four years, until more information becomes available on their effects and until some consideration has been given to how to pay for them.

End Notes

[1] Thomas Hungerford, “Saving Incentives: What May Work, What May Not,” Congressional Research Service, June 20, 2006.

[2] The 2001 bill also included additional increases in allowable contributions for taxpayers age 50 or older. In the case of IRAs, individuals in this age range can contribute an additional $1,000 per year to an account; in the case of 401(k)s, they can contribute an additional $5,000 (by 2006), with that amount indexed for inflation in future years. Thus, individuals age 50 or older now can place $20,000 a year in a 401(k). Their employers’ contributions are on top of this.

[3] Extending the higher contribution limits for IRAs would also add substantially to the cost of a tax cut included in the tax reconciliation bill enacted in May. That provision lifted the income limits on conversions from IRAs to Roth IRAs, allowing high-income households to roll their traditional IRAs into Roth IRAs, from which withdrawals are tax exempt. Extending the 2001 provisions would enable high-income households to accumulate more funds in traditional IRAs and would thereby raise the cost of the rollover measure. See Aviva Aron-Dine and Robert Greenstein, “Provision in Tax Cut Bill Effectively Eliminates Income Limits on Roth IRAs: Establishes Major New Tax Shelter for High-Income Households,” Center on Budget and Policy Priorities, revised May 15, 2006.

[4] For instance, at a Joint Economic Committee hearing on November 3, 2005, then-Chairman Greenspan responded to a question about extending the reduced tax rate on dividends, saying: “I would like to see the extension of that provision in the tax law, but I would insist that it be done in the context of PAYGO [“pay-as-you-go” rules], which is not currently on the books.”

[5] Craig Copeland, “IRA Assets and Characteristics of IRA Owners,” EBRI Notes, December 2002; David Joulfaian and David Richardson, “Who Takes Advantage of Tax-Deferred Savings Programs? Evidence from Federal Income Tax Data,” Office of Tax Analysis, Department of Treasury, 2001; Robert Carroll, “IRAs and the Tax Reform Act of 1997,” Office of Tax Analysis, Department of Treasury.

[6] Congressional Budget Office, “Utilization of Tax Incentives for Retirement Saving: An Update,” February 2006.

[7] General Accounting Office, “Private Pensions: Issues of Coverage and Increasing Contribution Limits for Defined Contribution Plans,” GAO-01-846, September 2001.

[8] Congressional Budget Office, “Utilization of Tax Incentives for Retirement Saving: An Update,” February 2006.

[9] For comparisons between tax expenditures for savings and the personal saving rate, see Elizabeth Bell, Adam Carasso, and Eugene Steuerle, “Retirement Saving Incentives and Personal Saving,” Urban Institute, December 20, 2004.

[10] Eric Engen and William Gale, “The Effects of 401(k) Plans on Households Wealth: Differences Across Earnings Groups,” National Bureau of Economic Research Working Paper No. 8032, December 2000.

[11] Thomas Hungerford, “Saving Incentives: What May Work, What May Not,” Congressional Research Service, June 20, 2006.

[12] See Esther Duflo, William Gale, Jeffrey Liebman, Peter Orszag, and Emmanuel Saez, “Savings Incentives for Low- and Middle-Income Families: Evidence from a Field Experiment with H&R Block,” Retirement Security Project 2005-5, May 2005.

[13] The credit eventually would disappear because the income levels below which households do not owe income tax are indexed for inflation, while the income levels above which households are ineligible for the saver’s credit would be frozen under the House bill. Eventually, all households that owe income tax would have incomes too high to qualify for the credit. See Robert Greenstein and Joel Friedman, “Saver’s Credit for Moderate-Income Families Would Fade Away Over Time If Not Indexed for Inflation,” Center on Budget and Policy Priorities, revised July 17, 2006.

More from the Authors