New Congressional Budget Office Estimates Show Continued High Deficits and Further Fiscal Deterioration

Executive Summary

On September 7, the Congressional Budget Office released new estimates showing that the budget deficit will grow to $422 billion in fiscal year 2004. [1] This is $46 billion higher than the 2003 deficit, which stood at $375 billion.

Despite the economic recovery, the deficit has continued to rise. 2004 will be the fourth consecutive year of fiscal deterioration, following eight consecutive years of fiscal improvement. Moreover, outside the surplus in the Social Security Trust Fund, CBO estimates the 2004 deficit at $571 billion.

CBO’s latest figures reinforce a number of concerns.

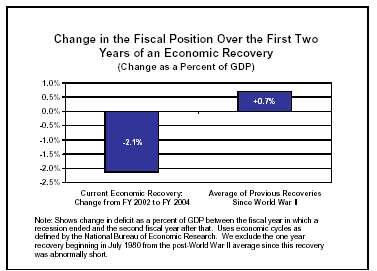

- The deficit is rising when it should be falling, indicating the emergence of a structural deficit: At this point in previous economic recoveries, deficits have almost invariably begun to shrink rather than continued to rise. The current economic recovery, however, is different; it has featured the largest deterioration in the government’s fiscal position of any recovery since World War II. A substantial “structural” deficit has developed that will persist as the economy grows, unless policies change.

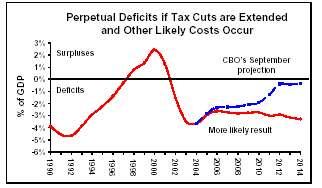

- Realistic assumptions indicate deficits will total $4.4 trillion over the next decade: Although CBO’s official projections show deficits declining over the next ten years to $65 billion by 2014, CBO notes that its official projections do not reflect the costs of extending the tax cuts beyond their scheduled expiration dates. As CBO director Douglas Holtz-Eakin testified in July, “...baseline revenue projections are made less reliable by the existence of expirations that few people expect to occur as written in current law.” [2] In addition, while CBO’s projections overstate likely future costs of military operations and reconstruction in Iraq and Afghanistan, they otherwise include defense levels below those CBO estimates to be needed to fully fund the Administration’s multi-year defense plan.

CBO’s new report and other CBO documents include additional estimates indicating that if the tax cuts are continued and projected defense expenditures are adjusted to make them more realistic (including both a downward adjustment to reflect an assumption that operations in Iraq and Afghanistan will phase down over the next few years and an upward adjustment to reflect the full cost of the Administration’s multi-year defense plan), projected deficits will not fall below $340 billion in any year, will average more than $440 billion per year over the next decade, and will total approximately $4.4 trillion over the ten-year period. (A recent Goldman-Sachs analysis concludes that the ten-year deficit is likely to be higher and could total between $5 trillion and $6 trillion.) - The fiscal picture has deteriorated markedly since 2001: The 2004 deficit of $422 billion reveals a budget in much worse shape than CBO projected in early 2001. At that time, CBO projected a surplus in 2004 of $380 billion.[3] As can be seen, the actual result for 2004 is $800 billion worse than projected in 2001. Nor is this result peculiar to 2004: over the ten-year period from 2002 to 2011, our current projections are about $870 billion worse on average each year than the projections issued in early 2001, or $8.7 trillion worse over the decade as a whole.

Calculations based on CBO and Joint Tax Committee data show that of the $8.7 trillion deterioration over the 2002-2011 period, $5.5 trillion is attributable to tax cuts, defense funding increases, and domestic program increases enacted by Congress. (The rest is due to economic or technical factors.) Tax cuts account for the majority of the $5.5 trillion deterioration that is due to the actions of policymakers. In other words, the tax cuts have increased the deficit more than all program increases combined. -

New figures do not reflect the return of fiscal discipline or stronger economic growth: Earlier this year, CBO projected a deficit of $477 billion; the new projection is $422 billion. The lower projection is not an indication of a return of fiscal discipline; no policy changes have been enacted since February that would reduce the deficit this year by more than a marginal amount. Nor does the lower projection stem from stronger economic growth; real GDP growth has been 4.8 percent over the first three-quarters of the fiscal year, which is exactly what CBO earlier projected. [4] While the factors accounting for the lower deficit projection are not entirely clear, some of the change is likely be due to adverse economic developments — higher-than-expected inflation and greater-than-expected concentration of income among those high on the income scale. Both of those developments result in somewhat higher tax revenues than would otherwise be collected.

- The growth of deficits has largely reflected stunning revenue declines: Some tax-cut advocates continue to claim that the deficit problem is caused primarily or exclusively by spending increases. The CBO data show this is not the case; as just noted, the tax cuts enacted since the beginning of 2001 have contributed more to the deficit than the spending increases. The CBO data also show that federal spending in 2004, measured as a percentage of the economy (i.e., of the Gross Domestic Product), is slightly below its average level of the last four decades. The deficits thus cannot be said to be due to unusually high levels of spending.

What the data show instead is that the emergence of large deficits stems largely from a stunning drop in revenues. The CBO data indicate that federal tax revenues this year will be at their lowest level, measured as a share of the economy, since 1959. (Under CBO’s projection of last spring, revenues this year would have been at their lowest level, as a share of the economy, since 1950.)

Goldman-Sachs on OMB’s Deficit Estimates

“The Office of Management and Budget has perfected the art of under-promising and outperforming in terms of its near-term budget deficit forecasts. For example, in its semiannual review, the OMB lowered its deficit forecast for fiscal 2004 to $445 billion from $521 billion. This creates the impression that the deficit is narrowing when, in fact, it will be up sharply from the $375-billion imbalance of a year earlier. This process is likely to continue in October, when the fiscal 2004 deficit turns out to be lower than the current OMB forecast.

“In contrast, the OMB’s longer term forecasts — a deficit that falls in half in five years — appear to be too optimistic for two reasons. First, spending will almost certainly be higher than projected, both due to the added funds needed for Afghanistan and Iraq and because the assumed freeze in real domestic discretionary spending has no historical precedent. Second, some of the tax law changes sought by the administration, such as relief from the Alternative Minimum Tax (AMT), are not built into the current projections.”

Source: Goldman Sachs, “US Economic Analyst,” August 6, 2004, p. 3

Is the Administration Being Straightforward with its Deficit Forecasts?

Finally, the new CBO figures raise fresh concerns about how straightforward the Administration is being with its budget estimates. The Administration appears to have massaged its deficit estimates. Last February, the Administration produced an overstated deficit estimate of $521 billion for the current fiscal year. When the Administration issued its most recent estimate on July 30 — an estimate of a $445 billion deficit for 2004 — the Administration claimed that the drop from $521 billion to $445 billion was good news that showed its policies were working. As noted, however, economic growth has not exceeded earlier expectations. Moreover, the long-term budget picture has failed to improve. The change in the projected level of the deficit in 2004 only indicates that short-term deficits were overestimated to begin with.

Moreover, the Administration’s current official estimate — that the deficit will be $445 billion in the current fiscal year — itself appears to be overstated. Only three days after OMB issued the $445 billion estimate, the Treasury quietly issued an estimate that the deficit would be $418 billion this year, about the same level CBO is projecting. When the actual deficit is announced at about $422 billion shortly before the election, the Administration may contend that the $422 is “good news” that shows further progress has been made since July, because the 2004 deficit has been “reduced” further from $445 billion to $422 billion.

Has Economic Growth Been Unexpectedly Strong?

The Administration is portraying the drop in the projected 2004 deficit from the $477 billion level that CBO projected in March to the newer estimate of $422 billion as a sign of unexpectedly strong economic growth, which the Administration also claims vindicates its tax-cut policies. Such a conclusion, however, is misguided. Overall economic growth has been no faster than expected earlier this year.

Over the first three quarters of fiscal year 2004, the economy grew at the same rate that CBO forecast in January. The real gross domestic product — the overall measure of the economy — was 4.8 percent larger in the first three quarters of this fiscal year than in the same period last year. In its January Budget and Economic Outlook, CBO projected an annual GDP growth rate of 4.8 percent for this period. (Further, in its new September report, CBO revised downward its estimate for GDP growth for all four quarters of fiscal year 2004. There has not been an unforeseen economic boom.)

To be sure, CBO now expects revenues to be $54 billion higher than it projected earlier in the year, accounting for essentially all of CBO’s re-estimate of the 2004 deficit. Factors that help to explain the higher revenues include the following:

- According to CBO, the Treasury has received an additional $30 billion as a result of taxpayers receiving smaller refunds and making larger tax payments this year when they filed their 2003 income tax returns than the Treasury had expected. This $30 billion in additional revenue comes from 2003 tax returns; essentially none of this can be attributed to unexpected economic growth in 2004.

- Inflation has increased, which tends to push up revenue collections. Over the first three quarters of the fiscal year, inflation has proceeded at a 3.0 percent annual pace. Last spring, CBO expected inflation to proceed at a 1.5 percent annual pace over this period.

- High-income individuals and corporations may be receiving a greater share of the income in the nation than previously anticipated, with ordinary workers receiving a smaller share. The federal tax system collects a higher percentage of income from high-income households than from typical workers. As a result, increases in income disparities tend to increase federal revenues.

Trends in tax receipts provide some evidence this is occurring. So far in 2004, personal income tax receipts have been modestly higher than expected and corporate tax revenues have enjoyed an unanticipated increase (although they remain well below their historical norm). At the same time, payroll tax receipts, which come disproportionately from the wages of ordinary workers, appear to be lower than CBO had anticipated. Income tax revenues come in higher and payroll tax revenues lower when income disparities widen.

CBO does not yet have enough data to know exactly why revenues are higher than expected, and other factors also may help to explain the revenue increase. But it is clear that faster-than-expected overall economic growth is not among them.

Is a Growing Deficit Good News?

In its just-released Summer Update, CBO projects a deficit of $422 billion for 2004, an increase of $46 billion over last year’s level of $375 billion. The Administration is likely to portray a deficit of this size as good news, claiming its policies are working to reduce federal borrowing and that the deficit is “manageable.” The Administration will point out that a deficit in the vicinity of $422 billion is lower than the Administration’s $521 billion estimate of last February, CBO’s estimate of $477 billion of last March, and the Administration’s $445 billion estimate of July 30. Does the new estimate represent real progress?

As noted above, at this point in previous economic recoveries, deficits have almost invariably begun to shrink. The new CBO projections show that in 2004, however, the deficit has increased again. In only one other recovery since World War II have deficits expanded as a share of the economy over the first two years of an economic recovery.[5] In previous recoveries, the government’s fiscal position improved by an average of 0.7 percent of GDP between the fiscal year in which the recession ended and the second fiscal year after that. By contrast, CBO’s new estimates show that in the current recovery, deficits have deteriorated by 2.1 percent of GDP between fiscal year 2002, when the recession ended, and fiscal year 2004. A substantial structural deficit has emerged that will persist as the economy grows. This does not represent an advance.

Since March, CBO’s deficit estimate for 2004 has fallen by $56 billion, but this should not be considered a victory. The deficit will still grow significantly from 2003 to 2004, just not as much as previously expected. Further, the reduction in the projected 2004 deficit does not reflect newfound fiscal discipline or unexpectedly strong economic growth. No policy changes have been enacted this year that would reduce the 2004 deficit by more than a marginal amount, and economic growth has been modestly below previous expectations. As explained in the box above, the drop in CBO’s projected 2004 deficit could reflect certain adverse economic trends, such as higher-than-expected inflation and increased disparities in income between high-income Americans and the rest of the population.

Some policymakers may overstate the improvement in the estimated 2004 deficit by focusing on the drop of about $100 billion in the 2004 deficit from the $521 billion level the Administration projected last February to the current CBO estimate of $422 billion. A substantial share of this $100 billion difference, however, stems from the Administration having noticeably overstated the likely 2004 deficit when it issued its budget in February (a development that we reported at that time).

There also is not a basis for portraying as “progress” the shift from OMB’s July 30 estimate of $445 billion to CBO’s new estimate of $422 billion. OMB’s $445 billion estimate was simply another overstatement of the 2004 deficit. Both CBO and Treasury figures indicated at the time that the $445 billion estimate was too high. OMB documents admitted as much.

- On August 5, just six days after OMB issued its $445 billion estimate of the 2004 deficit, CBO reported that it expected the deficit to be $422 billion, the same as its current estimate.

- On August 2, just three days after OMB issued its $445 billion estimate, the Treasury Department issued data indicating a deficit of $418 billion. [6]

- Moreover, OMB admitted in the fine print of its July 30 Mid-Session Review that its forecast of $445 billion was overstated. OMB acknowledged that its 2004 spending estimate was based on figures supplied by the various federal departments and agencies, which “tend to overestimate actual outlays.” OMB concluded, “history suggests that the final deficit outcome for this year is likely to be different from [the $445 billion] estimate — most probably lower.” [7]

In summary, the deficit that is now forecast for 2004 exceeds the 2003 deficit and is unusually high for a time when the economy is on the rebound. The deficit is still expanding. With this year’s deficit projected to equal 3.6 percent of GDP, the federal debt — which is the sum of all past deficits and surpluses — will continue growing at an unsustainable rate. It will grow almost 11 percent in 2004 alone and has grown nearly one-third in the last three years.[8]

These developments would be of little concern if deficits of this size were temporary and they had succeeded in producing a robust economic rebound. But they are not temporary. The nation faces a large structural deficit, little of which is caused by temporary phenomena such as economic cycles or the war in Iraq. Large deficits loom “as far as the eye can see.”

Will Deficits Shrink Over Time?

CBO’s official long-term estimates substantially understate future deficits. The new projections show deficits shrinking from $422 billion in 2004 to $65 billion in 2014 and totaling $2.3 trillion over the ten-year period from 2005 to 2014.

Unfortunately, the official deficit projections for future years are not realistic; they omit the costs of a number of policies already in place that are likely to be extended. A more realistic projection that takes these omitted costs into account shows deficits averaging above $440 billion per year over the next ten years and totaling $4.4 trillion over the ten-year period.

CBO recognizes that its official baseline projections follow certain mechanical rules that are unrealistic in current circumstances. Accordingly, CBO included in the Summer Update, as it did in earlier CBO documents, additional budget information that analysts can use to obtain more realistic results. Adjustments that are needed to obtain realistic projections include:

- Including the costs of extending expiring provisions of the 2001 and 2003 tax cuts. The Administration has repeatedly argued for continuation of nearly all of the tax cuts enacted over the past three years except for the “bonus depreciation” provision. The official CBO projections assume that three so-called “middle-class” tax cuts (the 10 percent bracket, the increase in the child tax credit to $1,000 per child, and tax breaks for married couples) revert to a less generous form next year and that all of the 2001 and 2003 tax cuts then expire after 2010.

- Including the large costs associated with continuing to provide relief from the individual Alternative Minimum Tax . The Administration has repeatedly said it plans to propose extending AMT relief and will submit a proposal to do so next year. The Republican platform adopted last week also pledges the party to an AMT fix. No costs for this are reflected in the official CBO projections (or in the Administration’s budget estimates). Unless AMT relief is continued, the AMT will explode into the middle class, something no observer believes will occur.

- Including the costs of continuing an array of other tax breaks. These are the so-called tax “extenders,” which are tax cuts that Congress and the White House always renew for one or a few years at a time, on a bipartisan basis, when the tax cuts are slated to expire. Noting that most extenders are very likely to remain in effect, CBO director Douglas Holtz-Eakin recently testified, “…most of the expiring provisions were enacted as a step toward making them permanent or extending them indefinitely.”[9]

- Reflecting the full cost of the Administration’s own “Future Year Defense Plan” but assuming that costs in Iraq and Afghanistan phase down . The official CBO projections overstate the cost of military operations and reconstruction in Iraq and Afghanistan, but otherwise understate the likely course of defense spending in future years. The official projections carry forward the $115 billion in fiscal year 2004 supplemental appropriations for military operations and reconstruction in Iraq and Afghanistan for each of the next ten years. CBO also provides a more optimistic alternative, in which those costs ramp down in coming years; we reduce baseline costs by assuming CBO’s alternative scenario.

CBO has estimated elsewhere the cost of funding the Administration’s Future-Year Defense Plan, which essentially serves as the Administration’s multi-year defense blueprint. The Center on Strategic and Budgetary Assessments has converted the CBO funding figures into estimates of expenditures each year if the Future-Year Defense Plan is fully funded. This results in an increase in the official projections, which assume defense funding rises no faster than inflation.[10] Taking both the overstatement and understatement of defense costs into account, we conclude that the official CBO projection modestly overstates likely future Pentagon budgets, and accordingly make a downward adjustment.

| Table 1: | |

| 2005-2014 total | |

| Cumulative 10-year Deficit Shown in Summer Update | $2,294 |

| Costs not included in Summer Update: | |

| Extension of 2001-2003 tax cuts (except AMT relief)* | $1,652 |

| Relief from the Alternative Minimum Tax | $603 |

| Future-Year Defense Plan and ongoing war on terrorism | -$113 |

| Subtotal, costs not included in Summer Update | $2,142 |

| Resulting Cumulative 10-year Deficit | $4,435 |

These various adjustments increase projected deficits over the next ten years by an average of $215 billion per year — to an average level of about $440 billion per year. Over ten years, projected deficits total $4.4 trillion. (See Table 1.)

It may be noted that this $4.4 trillion total is likely to understate the size of future deficits, because it leaves in place the official baseline assumption that funding for domestic discretionary programs will grow no faster than inflation over the coming decade, and thus will fail to keep pace with population growth. History strongly suggests that over time, domestic discretionary programs will at least keep pace with inflation plus population growth. If an adjustment were made to these projections to reflect the assumption that overall funding for domestic discretionary programs will keep pace with inflation plus population growth, the projected deficits would average $465 billion per year and total almost $4.7 trillion over ten years.

In a recent analysis, the investment firm Goldman-Sachs estimated that deficits over the next ten years could total between $5 trillion and $6 trillion. Like us, Goldman-Sachs adjusted CBO’s projections by assuming that the tax cuts would be made permanent and that the AMT would be indexed. Goldman-Sachs also made its own mid-term economic forecast, assumed defense spending would average 4.0 percent of GDP, and assumed that expenditures for annually appropriated non-defense programs would grow faster than inflation by two percent per year. [11]

In short, the official CBO baseline significantly understates expected deficits in future years, as CBO itself has explained. The deficit will certainly shrink to some extent in the years immediately after 2004 as the economy recovers more fully and as the “bonus depreciation” provision of the 2003 tax cut expires, but realistic projections suggest the deficit will not fall below $340 billion in any year. Even this modest reduction in deficits will not last. As the baby-boom generation begins retiring after 2008 and additional tax cuts such as estate-tax repeal take effect, deficits will start mounting again and eventually surpass the 2004 level.

How Did Projected Surpluses Turn to Deficits

In January 2001, the nation seemed to be awash in surpluses. In his first address to Congress, President Bush devoted considerable attention to setting forth domestic initiatives such as increases in funding for education and biomedical research. The President said that after all of his domestic initiatives, including a prescription drug benefit, were taken into account and a large contingency reserve was set aside, the nation would still run large surpluses. As a result, he declared, the government was collecting excess revenue and large tax cuts were warranted. He also said that even with his tax cuts and spending initiatives, the nation would be able to pay off nearly all of the publicly held debt by the end of the decade.

Unfortunately, this 2001 view of the world proved far removed from subsequent budgetary reality. Calculations based on CBO and Joint Tax Committee data show how projected surpluses have turned to actual or projected deficits. As can be seen in Table 2, the 2004 budget has turned out to be $800 billion worse than the 2004 budget projected in 2001. Adjusted for comparability, CBO projected at that time that we would run a $380 billion surplus in 2004; this has now turned into an estimated $422 billion deficit. Over the ten-year period from 2002 to 2011, the budget deteriorated by an average of about $870 billion per year, for a total deterioration of $8.7 trillion over the period. [12]

| Table 2: | ||

| In 2004, in billions of dollars | Ten-year cumulative total, 2002-2011, in trillions of dollars | |

| CBO’s Projected Surpluses, January 2001 (a) | $380 | $5.0 |

| Over-optimism about the economy and “technical” factors | -298 | -3.2 |

| Tax cuts, assuming extension of expiring provisions (b) | -293 | -2.8 |

| Increases for defense, homeland security, and international programs (c) | -148 | -1.9 |

| Increases for Rx drugs and other entitlement programs | -45 | -0.7 |

| Increases in domestic appropriations | -18 | -0.1 |

| Total deterioration in the projections | -802 | -8.7 |

| Actual or projected deficits, including assumptions about tax cut extensions and defense funding discussed in previous section (d) | -422 | -3.7 |

| CBPP calculations from CBO and JCT data. Columns may not add due to rounding. All amounts include both direct costs and the increased interest payments caused by those direct costs. (a) Adjusted for comparability with current projections, e.g. by assuming that expiring tax “extenders” that existed in 2001 would be continued. (b) The “bonus depreciation” business tax cut enacted in 2002 and increased in 2003 is assumed to expire on schedule at the end of this year; the President has not requested its extension. Tax-cut figures include the costs of increases in “refundable” tax credits. (c) This category also includes funds for the reconstruction of New York City after September 11, 2001. (d) The ten-year total of $3.7 trillion covers the years 2002-2011, while the ten-year total of $4.4 trillion shown in Table 1 is calculated on the same basis but covers the years 2005-2014. | ||

The original projections were too optimistic about the economy and the level of revenues that any given size economy would produce. In addition, Congress and the President enacted substantially more tax cuts than President Bush originally proposed. Each year, he asked for additional costly tax cuts and generally got them. Program increases, especially for defense and homeland security, also have been substantial. Table 2 shows the amount of budget deterioration attributable to each of these causes.

As can be seen, the tax cuts that have been enacted by Congress and the President since 2001 (which are assumed to be extended) account for more of the budget deterioration than all of the program increases combined. For 2004, the tax cuts account for 58 percent of the deterioration. The budget increases for defense, international affairs, and homeland security account for 29 percent of the slippage. Increases for all other domestic programs account for the remaining 12 percent.

Is the Deficit “Spending Driven”?

Some people imply that since a deficit means expenditures exceed revenues, by definition “excess spending” must be the cause of deficits. This makes little sense. If spending is cut but taxes are cut still more, deficits rise. Does this make the resulting deficits “spending driven” because spending now exceeds revenues by a greater degree?

An honest assessment of the relative role that tax cuts and program increases have played in contributing to the deterioration of the budget over the past 3½ years requires examining the cost of all legislation enacted since the start of 2001. As mentioned, Table 2 shows that tax cuts account for 58 percent of the budget deterioration in fiscal year 2004 that has been caused by the enactment of legislation. (It also is of note that contrary to recent claims that domestic spending has exploded, as of 2004 some 70 percent of the spending increases enacted since the start of 2001 have come in the area of defense, homeland security, and international affairs.)

If the deficits truly were “spending driven,” with tax cuts playing little role, one would expect federal expenditures to be high today in historical terms. They are not. The new CBO figures for 2004 show that federal spending, measured as a share of the economy, is below its 1962-2001 average. Federal spending is below the average for the previous four decades even though operations in Iraq have proved costly and policymakers have had little choice but to enact funding increases to strengthen homeland security and rebuild after 9/11. As Table 3 indicates, the current deficits primarily stem not from unusually high levels of expenditures but from unusually low levels of revenue.

| Table 3: | |||

| 2004 | Average, 1962-2001 | Comments on 2004 fiscal position | |

| Expenditures | 19.8% | 20.4% | Lower than average |

| Revenues | 16.2% | 18.3% | Lowest since 1959 |

| Deficits | 3.6% | 2.1% | Above average |

| Columns may not add due to rounding. Source: CBO for 2004, OMB for historical data | |||

Revenues will remain at historically low levels after the economy recovers. If the Administration’s tax cuts and relief from the Alternative Minimum Tax are extended, revenues will be at a lower average level over the next ten years than the average revenue levels for the decades of the 1960s, 1970s, 1980s, and 1990s.

End Notes

[1] CBO, “The Economic and Budget Outlook: Summer Update,” September 7, 2004.

[2] Testimony of Douglas Holtz-Eakin before the House Budget Committee, July 22, 2004.

[3] In 2001, CBO projected a surplus of $397 billion for fiscal year 2004. That projection, after adjustment to make it comparable to other projections used here (e.g., after adjustment to assume continuation of certain expiring tax provisions), equals $380 billion.

[4] This calculation compares the average size of the economy in the first three quarters of this fiscal year with the average size of the economy in the first three quarters of the previous fiscal year. Alternatively, one could compare the size of the economy in the third quarter of fiscal year 2004 with the size of the economy in the last quarter of fiscal year 2003. By this method, the economy has grown at a real annual rate of 4.0 percent, noticeably slower than CBO’s earlier projection for a real annual rate of growth of 4.4 percent through the third quarter.

[5] In our comparison, we exclude the recovery period that began in July 1980 and ended in July 1981. That expansion was unusually short-lived (it was part of a “double-dip” recession), and is not comparable to other post-World War II economic cycles.

[6] The Treasury reported that the actual fiscal 2004 deficit through June 30 was $327 billion. It projected a deficit of $91 billion for the period July through September. Combining those two figures produces a total fiscal 2004 deficit of $418 billion. See U.S. Treasury, “Monthly Treasury Statement, June 2004,” July 13, 2004. Also see Office of Debt Management, U.S. Treasury, “Charts (Quarterly Refunding),” August 2, 2004.

[7] OMB, “Fiscal Year 2005 Mid-Session Review,” page 4.

[8] In addition, CBO projects that the publicly held debt will grow from 33 percent of GDP in fiscal year 2001 to 37.5 percent of GDP in fiscal year 2004. Under the realistic budget assumptions, the debt will climb to almost 50 percent of GDP over the next decade.

[9] Douglas Holtz-Eakin, “CBO Testimony: Statement of Douglas Holtz-Eakin Before the Committee on the Budget, U.S. House of Representatives,” July 22, 2004, p. 2.

[10] CBO, “The Long-Term Implications of Current Defense Plans: Detailed Update for Fiscal Year 2004,” February 2004; Steven M. Kosiak, “Cost Growth in Defense Plans, Occupation of Iraq and War on Terrorism Could Add Nearly $900 Billion to Projected Deficits” Center for Strategic and Budgetary Assessments, March 9, 2004; Steven M. Kosiak, unpublished estimates, Center for Strategic and Budgetary Assessments.

[11] Goldman-Sachs, “US Budget Outlook — Better Now, Worse Later,” Daily Financial Market Comment, September 8, 2004.

[12] To use the January 2001 projection as a basis for comparison with the current projection, we need to make sure that both projections are made on a comparable basis. Since we have incorporated certain likely or inevitable costs into the current deficit projection, similar costs (such as the continuation of “tax extenders”) also must be incorporated into CBO’s January 2001 projection before the projections can be compared. Adjusting for comparability reduces the surpluses reflected in the January 2001 projection by about $16 billion in 2004 and $642 billion over the 2002-2011 period.

More from the Authors

David Kamin is Professor of Law at New York University School of Law.

Kamin was a Research Assistant with the Center from 2003 through July 2005. Kamin's focus was on federal tax and budget policy, especially with regards to the cost and impact of federal tax bills. Kamin graduated from Swarthmore College with a B.A. in Economics and Political Science. Prior to joining the Center, he worked as a Research Associate at the Committee for Economic Development focusing on federal budget policy.