Limiting Itemized Deductions for Upper-Income Taxpayers Would Have Little Effect on Small Business, Charities, Housing

Criticisms of Proposal Are Overblown

Despite persistent claims to the contrary, the President’s proposal to cap the value of itemized deductions at 28 percent would have only small effects on small business, charitable giving, and homeownership.

That’s because the proposal, which would save $318 billion over the next ten years to help finance health care reform, would affect only those tax households with incomes over $250,000 that face tax rates of either 35 or 33 percent and that itemize their deductions. Such taxpayers represent fewer than 1.2 percent of all taxpayers.

Some critics charge that the proposal would hurt small business by raising taxes on many small business owners, and that it would hurt charities and housing by reducing the incentives to make charitable donations and to buy homes. These charges are overblown, however. Because the proposal would affect such a small percentage of taxpayers, it would likely have no substantial effect on small business, it would reduce charitable giving in the United States by only an estimated 1.3 percent, and it would have little impact on home-buying across America (and an even more negligible impact on home construction). Furthermore, the proposal would return the top value of itemized deductions to what it was during the latter Reagan years, after Congress cut the top tax rate to 28 percent.

Other critics charge that the proposal would place a further drag on an economy that is already in recession. This charge is unfounded. The proposal would not apply to taxes on income earned before January 2011 and would not impose its full effect on taxes actually paid until 2012, when the economy should be in recovery. If the economy is still not recovering at that time, policymakers surely will delay the proposal’s implementation, as Administration officials indicated in congressional testimony last week. Under those economic circumstances, it would be difficult politically for them not to do so.

Meanwhile, the relatively modest effects of this proposal on small business, charities, and housing would be more than offset by its benefits. By helping to finance health care reform, this proposal would address two of the most important issues facing the nation: ensuring that all Americans have health coverage and slowing the growth in costs throughout the U.S. health care system — the principal factor driving the projected, and unsustainable, long-term growth in federal deficits and debt.

Moreover, the proposal would make the tax system fairer. Itemized deductions effectively provide federal subsidies that have greater value for taxpayers in higher tax brackets. By capping the value of such deductions at 28 percent, this proposal would make itemized deductions less regressive and the tax system as a whole more equitable.

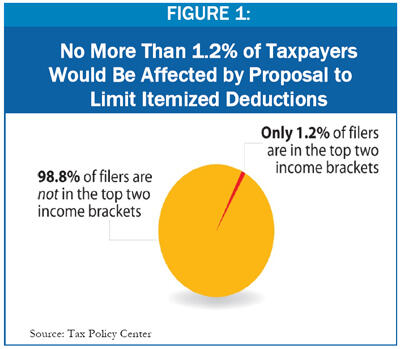

Only About 1 Percent of Taxpayers Would Be Affected

The President’s proposal to cap the value of itemized deductions at 28 percent would affect no more than 1.2 percent of filers.

Under the President’s proposal, the limitation will not affect anyone with income below $250,000 ($200,000 for singles). This immediately rules out over 95 percent of filers, as Urban Institute-Brookings Institution Tax Policy Center data show.[1] Among the remaining 5 percent of filers, the proposal would not affect anyone who does not face the top two marginal tax rates (36 percent and 39.6 percent under the Obama tax plan) because they already would be receiving a benefit from itemized deductions that is no more than 28 percent of the amount they deduct.[2] In fact, according to the Tax Policy Center, only 1.2 percent of all taxpayers would be subject to one of the top two rates.[3] And any of those taxpayers who do not itemize deductions would not be affected by the proposal. Thus, more than 98.8 percent of tax filers would be unaffected by the proposed limitation on the benefit of itemized deductions.

Furthermore, the bulk of the revenues that this proposal would generate would likely come from households with incomes well in excess of $250,000. That is true for two reasons.

First, limiting the value of deductions to 28 cents on the dollar would have a larger impact on taxpayers in the 35 percent tax bracket, who currently claim deductions at 35 cents on the dollar, than on taxpayers in the 33 percent bracket, who currently claim deductions at 33 cents on the dollar.

Second, because the average amount of itemized deductions that taxpayers claim rises with income, a large share of the deductions that the proposal would affect are claimed by people with incomes far above $250,000. For example, among filers who itemized deductions in 2006, those with incomes between $200,000 and $500,000 claimed about $48,000 in itemized deductions on average; those with incomes over $1 million claimed about $393,000 on average.[4]

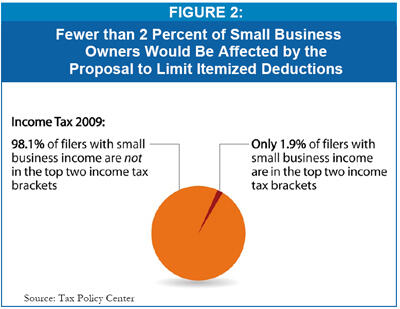

Fewer Than 2 Percent of Small Business Owners Would Pay More; Far More Would Benefit

Despite claims that the proposal would severely harm small business, fewer than 2 percent of taxpayers with income from a small business would likely be affected. Just 1.9 percent of small business filers fall into the top two income tax brackets, according to the Tax Policy Center.[5]

Furthermore, a much larger number of small business owners and their employees would likely benefit from other aspects of the President’s budget. The savings created by the cap would be entirely dedicated to financing health care reform legislation that almost certainly would provide subsidies to help the owners and employees of small businesses obtain health coverage.[6] According to a recent survey, 42 percent of small business owners think that making health care more affordable is one of the most important goals for the federal government to pursue.[7] In addition, many small business owners and employees would benefit from proposed tax cuts for middle-class taxpayers that are in the President’s budget, such as the proposal to extend the expansion of the tax credit that helps families cover college tuition costs, which Congress enacted on a temporary basis last month in the economic recovery legislation. Far more small businesses would benefit from these provisions than the 1.9 percent that might pay somewhat more in taxes.

Effect on Charitable Giving Would Be Modest

Some critics claim the proposal would prompt substantial reductions in charitable contributions, hitting charities at a time when they face rising need for their services and falling contributions due to the recession. These claims are overblown.

Some critics claim the proposal would prompt substantial reductions in charitable contributions, hitting charities at a time when they face rising need for their services and falling contributions due to the recession. These claims are overblown.

The proposal would likely reduce total charitable giving in the United States by only about 1.3 percent, based on research on the effects of tax incentives on charitable giving (see Figure 3.)[8] That’s true for two main reasons. First, contributions claimed as itemized deductions represent only 62 percent of total charitable giving; the rest comes from foundations, estates, and corporations, and from individuals who do not itemize their contributions. Second, as noted above, the proposal would affect only a subset of the 1.2 percent of taxpayers that are in the top two income tax brackets, a group that accounts for 18 percent of the charitable contributions reported as itemized deductions.

Proposal Would Have Little Impact on Home Buying, and Even Less on Home Construction

Some critics claim that the proposal, by capping high-income taxpayers’ deductions for mortgage interest, would significantly harm the housing market and reduce home construction. In fact, the impact would almost certainly be quite small.

As noted above, the proposal would only affect families that: 1) have incomes above $250,000; 2) pay tax at rates above 28 percent; and 3) itemize their deductions. These families account for a very small share of homes sales. Tax filers with incomes above $200,000 account for just 8 percent of those who claim the mortgage interest deduction, according to IRS data.[9] And the proposal would affect only a portion of those taxpayers — those who have income over $250,000 (for couples) and pay at tax rates above 28 percent — and who also are potentially in the market for a new home.

Finally, because those in this group are much better off financially than most other Americans, reducing the tax benefit of their deductions by a fifth — from 35 percent to 28 percent — would not likely have a major impact on their home-buying decisions. The proposal would more likely affect their decision about the size of the mortgage they assume versus the share of the home purchase price that they cover up front.

The proposal would have even less impact on home construction. Only a small share of home purchases involves new homes. For example, a recent National Association of Home Builders’ analysis of the impact of a proposed homebuyer tax credit estimated that fewer than 1 in 5 homes that would be purchased as a result of the credit would be newly constructed homes.[10] Since the proposal only affects 1.2 percent of all households and most of them are not in the market to purchase a home — and since most of the very small number of such households that are in the market will not purchase a newly constructed home — the effect on home building should be miniscule.

Proposal Would Make Tax System Fairer

Far from unfairly penalizing high-income taxpayers, as some critics claim, the proposal would make the tax system more equitable. That is true for two reasons.

First, itemized deductions are regressive — they provide greater government subsidies, per dollar of taxpayer expenditure, for higher-income taxpayers than for people with more modest incomes.

Each dollar of itemized deductions is worth 35 cents to someone in the 35 percent bracket, but only 15 cents to someone in the 15 percent bracket. So, if a family in the 35 percent bracket claims $10,000 in itemized deductions, its tax bill is reduced by $3,500. The federal government effectively pays for $3,500 of the expenditures, reducing the taxpayer’s cost to $6,500. But if a middle-income family in the 15 percent bracket deducts the same $10,000 for the same expense, its tax bill is reduced by only $1,500, and it must pay $8,500 of the total.

Second, high-income taxpayers, on average, claim more itemized deductions, measured as a share of their incomes, than lower-income filers do.

Due to these two factors, itemized deductions increase after-tax incomes by about 3 percent for the top 20 percent of taxpayers, but by less than 0.5 percent of income for the bottom 60 percent of taxpayers, according to the Tax Policy Center. Itemized deductions, the Tax Policy Center says, cost the Treasury about $154 billion in 2007.[11]

By capping the value of deductions for upper-income taxpayers at 28 percent, the proposal would make itemized deductions somewhat less regressive. Even under the proposal, low- and moderate-income taxpayers would benefit much less from itemized deductions than high-income taxpayers do. Most low- and middle-income taxpayers would still receive a benefit (or subsidy) equal to 15 percent or less of the amount of the deductions they claim, while high-income taxpayers would receive a subsidy equal to 28 percent of their deductions.

Conclusion

The proposal to limit the benefits of itemized deductions for high-income taxpayers would affect few taxpayers, have only a small effect on charitable contributions and other deductible expenditures, and make the tax system fairer. The $318 billion that the proposal would raise would help finance health care reform, which would both provide substantial long-term benefits for millions of Americans and — presuming that its cost containment measurers prove successful — for the federal budget as well.

End Notes

[1] This figure is likely to overstate the number of filers with income at those levels, because TPC uses a somewhat broader definition of income than the Adjusted Gross Income definition used in the tax code. (For details, see Chye-Ching Huang, Jason Levitis, and James Horney, “Very Few Small Business Owners Would Face Tax Increases Under President’s Budget,” Center on Budget and Policy Priorities, February 28, 2009.)

[2] Below the top two rates, the top marginal rate for the regular income tax is 28 percent, as is the top rate under the Alternative Minimum Tax.

[3] A small number of filers who currently pay the AMT would move into the regular tax system due to the deduction cap and thus would be somewhat affected. These filers are included in the 1.2 percent of households that the Tax Policy Center projects would be affected by the proposal.

[4] Internal Revenue Service, “Statistics of Income — 2006, Individual Income Tax Returns,” Publication 1304 (Rev. 07-2006).

[5] This figure is approximate. The TPC estimates likely overstate the number of small business filers affected by the top two marginal income tax rates, because, as noted above, TPC uses a broader definition of income than the tax system and the TPC estimates use the previous administration’s expansive definition of “small business owner,” which includes many wealthy investors who play little or no role in the operation of the business. (For details, see Huang, Levitis, and Horney.) On the other hand, the Obama Administration’s tax proposals may push some filers off the Alternative Minimum Tax, which could modestly increase the number of small business filers who face the top two income tax rates and thus could potentially be affected by the proposal.

[6] For a more detailed discussion, see Huang, Levitis, and Horney.

[7] Robert Wood Johnson Foundation, “Study Shows Small Business Owners Support Health Reform,” Dec. 2008.

[8] Paul N. Van de Water, “Proposal to Cap Deductions for High-Income Households Would Reduce Charitable Contributions by Only About 1 Percent,” Center on Budget and Policy Priorities, March 3, 2009.

[9] Internal Revenue Service, “Statistics of Income — 2006, Individual Income Tax Returns,” Publication 1304 (Rev. 07-2006).

[10] Paul Emrath, “Economic Effects of a Policy to Stimulate Home Buying,” HousingEconomics.com, January 9, 2009.

[11] These figures reflect itemized deductions claimed in excess of the standard deduction. They take into account interactions between different types of itemized deductions and assume that the AMT remains in place, but without continuation of the 2007 AMT “patch.” For more detail, see Chye-Ching Huang and Hannah Shaw, “New Analysis Shows ‘Tax Expenditures’ Overall are Costly and Regressive,” Center on Budget and Policy Priorities, February 23, 2009. See also Leonard Burman, Eric Toder, and Christopher Geissler, “How Big Are Total Income Tax Expenditures, and Who Benefits from Them?” Tax Policy Center, December 2008.

More from the Authors

Areas of Expertise