Ineffective “Bonus Depreciation” Tax Break Should Remain Expired

During Congress’ lame-duck session, some members are expected to try to reinstate and even permanently extend the “bonus depreciation” tax break as part of legislation continuing various “tax extenders” (a package of primarily corporate tax provisions that policymakers routinely extend). Bonus depreciation, which expired at the end of 2013, has never been considered a tax extender; it does not belong in the extenders package and should remain expired:

- Bonus depreciation was meant to be temporary. Bonus depreciation allows businesses to take bigger upfront tax deductions for certain purchases, such as equipment. Congress enacted it on a temporary basis in 2008 to bolster the economy during the Great Recession, not to make it a permanent component of the tax code or extend it year after year like a tax extender. In the previous economic downturn, Congress enacted bonus depreciation in 2002 and then a Republican President, House, and Senate let it expire after 2004, when the economy was stronger.

- Research shows that it is of limited effectiveness as stimulus. Studies have shown that bonus depreciation “is largely ineffective as a policy tool for economic stimulus,” according to the Congressional Research Service (CRS).[1] Moreover, enacting bonus depreciation late in the year and making it retroactive to the start of 2014 — as the pending proposals would do — makes even less sense as an incentive, since it would give taxpayer funds to corporations as a windfall to companies for purchases they have already made.

- Making it permanent would sacrifice whatever modest boost it can provide in future recessions. Whatever modest stimulus bonus depreciation may provide stems entirely from its temporary nature. If it is permanent — or if repeated short-term extensions lead firms to expect it will be routinely extended — it will no longer encourage them to accelerate their purchases during economic downturns, as they will get the same tax break regardless of whether the purchases occur when the economy is weak or when it’s strong.

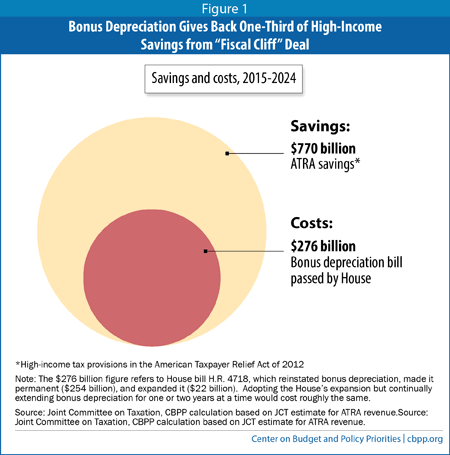

- Making bonus depreciation permanent is very expensive. Extending it permanently and expanding it, as the House has twice voted this year to do, would cost $276 billion over the coming decade (2015-2024), according to the Joint Committee on Taxation (JCT). [2] The cost would be roughly the same over ten years if Congress repeatedly extended bonus depreciation for one or two years at a time so that it never expired instead of formally making it permanent.

- Companies already receive generous tax treatment when they invest in equipment. Under current law, companies pay far less than the statutory 35 percent corporate tax rate on the profits flowing from those investments. In some cases, they receive a tax subsidy for those investments. Bonus depreciation further increases this favorable tax treatment.

- Extending bonus depreciation would be at odds with the push for corporate tax reform. Tax reform seeks to “broaden the base” by scaling back tax subsidies and to use the freed-up funds to lower tax rates, reduce budget deficits, or both. Bonus depreciation narrows the tax base by expanding tax subsidies. If made a permanent part of the tax code, bonus depreciation would make it more difficult to achieve revenue savings and tax-rate reductions through tax reform. Indeed, the corporate tax reform proposal this year from House Ways and Means Chairman Dave Camp, like most such proposals, repealed bonus depreciation rather than extended it.

A Temporary Provision of Limited Effectiveness

One of policymakers’ first steps to stimulate the economy during the Great Recession was to enact bonus depreciation on a temporary basis in 2008. They have since extended it several times as the economy struggled to recover. The provision expired at the end of 2013.

Policymakers have always viewed bonus depreciation as a temporary provision designed to help boost a weak economy. Its treatment has always stood in sharp contrast to the standard group of tax extenders such as the Research and Experimentation Tax Credit, which are repeatedly extended regardless of the state of the economy.

Evidence suggests that bonus depreciation is not a particularly cost-effective form of stimulus:

- “Three studies (two from 2006 and the other from 2007) provide additional support for the view that temporary accelerated depreciation is largely ineffective as a policy tool for economic stimulus,” the Congressional Research Service (CRS) concluded in a summary of the research. CRS cited a Federal Reserve finding that “no more than 10% of companies deemed the [bonus depreciation] allowances an important consideration in determining the timing or level of qualifying investments.”[3]

- Analyses by the Congressional Budget Office and Moody’s Economy.com have concluded that bonus depreciation has a fairly low “bang for the buck” as economic stimulus. Estimates from Mark Zandi of Moody’s suggest that every $1 of tax revenue lost from bonus depreciation generates only 20 cents in economic activity.[4] By contrast, Zandi estimates that extending emergency unemployment benefits, which Congress let expire at the end of 2013, boosts the economy by about $1.50 for every dollar spent. Additional infrastructure spending is also a much more cost-effective investment in a weak economy, boosting the economy by about $1.44 for every dollar spent.[5]

- A Goldman Sachs analysis earlier this year concluded that expiration of bonus depreciation at the end of 2013 “should have little effect” on the economy, while highlighting that “there are multiple indications that firms do not respond strongly to this incentive, for various reasons.”[6]

- An August 2014 survey of 100 senior finance and tax executives by Bloomberg BNA found that “Eighty-three percent of respondents said that the expiration of Section 179 expanded expensing and bonus depreciation has not affected their organizations’ capital expenditures this year.” Bloomberg concluded that “bonus depreciation and Section 179 expensing, while welcomed by the business community, is not viewed by a majority of that same community as an economic stimulus that drives business decisions.”[7]

It is important to note that Goldman Sachs and Bloomberg focused on bonus depreciation’s impact on executives as they made investment decisions. Now that 2014 is almost over, extending the tax break and making it retroactive to the start of the year would provide a generous, taxpayer-funded subsidy to companies for decisions they have already made.

Furthermore, to the extent that a temporary bonus depreciation provision has some — albeit very modest — effect in spurring economic activity during an economic downturn, making the provision permanent would sacrifice that boost. Whatever small boost occurs stems from the fact that the extra tax break applies only to purchases made during the temporary period it’s in effect. The temporary nature of the break may induce a modest number of firms to accelerate some purchases. If the tax break were permanent — or if it is extended enough times that businesses effectively regard it as a permanent measure — firms will have no incentive to accelerate purchases and to make them while the economy is faltering because they will get the same tax break regardless of when they make the purchases. A JCT report found that the House bill to make bonus depreciation permanent would have a negligible impact on employment and only a small impact on economic growth overall, despite its very large cost.[8]

As noted, the House proposal to expand bonus depreciation and extend it permanently would be extremely costly — $276 billion over 2015 to 2024.[10] (The cost would be roughly the same over ten years if Congress expanded bonus depreciation as under the House bill but repeatedly extended it for a year or two at a time instead of formally making it permanent.)[11] By itself, this measure would wipe out one-third of the $770 billion in revenue raised by the high-income revenue provisions of the 2012 “fiscal cliff” legislation. (See Figure 1.)[12]

Investments Already Get Generous Tax Treatment

Even without bonus depreciation, companies receive generous tax treatment when they invest in equipment and buildings, particularly if they borrow the funds to finance the investment.

When a company purchases a piece of equipment, it deducts the cost of the purchase over time. The deductions occur as the equipment ages and loses its value, a process referred to as depreciation. If the deduction is aligned with the equipment’s actual depreciation, the tax treatment is viewed as “neutral.”

Current law provides for “accelerated depreciation,” which lets companies write off equipment investments faster than the equipment actually loses value in real life. One of the largest corporate tax expenditures, accelerated depreciation is a major reason why companies pay far less than the statutory rate of 35 percent on profits flowing from an investment in equipment.

A company can magnify the tax break from accelerated depreciation by financing its investments through borrowing (for instance, by taking out a bank loan or issuing a corporate bond). Borrowing enjoys relatively favorable tax treatment because companies can deduct the interest payments on their debt.

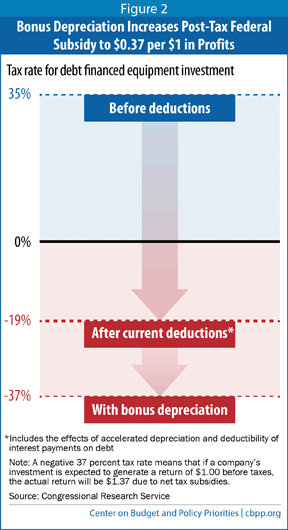

CRS has pointed out that even without bonus depreciation, debt-financed investments face an actual (or effective) tax rate that averages negative 19 percent.[13] In other words, companies do not pay taxes on the profits that flow from such investments but instead receive a tax subsidy of 19 percent, which they can use to reduce or eliminate other taxes owed. Adding bonus depreciation on top of accelerated depreciation greatly expands this generous tax subsidy, pushing the average effective tax rate to negative 37 percent (see Figure 2).

Extending Bonus Depreciation Moves in the Opposite Direction of Tax Reform

The fundamental nature of tax reform is to “broaden the base” by scaling back tax subsidies and to use the freed-up funds to lower tax rates, reduce budget deficits, or both. Bonus depreciation moves in the opposite direction by narrowing the tax base. If made a permanent component of the tax code, bonus depreciation would make it more difficult to achieve revenue savings and reduce tax rates.

As noted, accelerated depreciation is one of the largest corporate tax expenditures. The ability to write off investments faster than they depreciate is a valuable deduction for companies — and costly to the Treasury. Bonus depreciation is effectively accelerated depreciation on steroids, allowing companies to take half of the multi-year deductions immediately.

Because it is such a large tax subsidy, the treatment of depreciation tends to be a prime target of corporate tax reformers looking to broaden the tax base. Chairman Camp’s comprehensive corporate tax reform plan, which he advanced earlier this year after extensive consultation with the corporate community and others, is a good example. A central element of his plan is elimination of accelerated and bonus depreciation so that tax depreciation would “match closely the true economic useful life of assets.”[14]

Chairman Camp’s proposal to allow bonus depreciation to expire is sound. Policymakers always intended bonus depreciation to be a temporary corporate tax cut. Given its high cost and limited effectiveness, the now-expired provision should remain so.

End Notes

[1] Gary Guenther, “Section 179 and Bonus Depreciation Expensing Allowances: Current Law, Legislative Proposals in the 113th Congress, and Economic Effects,” Congressional Research Service, May 23, 2014.

[2] Joint Committee on Taxation, “Macroeconomic Analysis for Bonus Depreciation Modified and Made Permanent,” July 3, 2014, https://www.jct.gov/publications.html?func=startdown&id=4652.

[3] Guenther.

[4] Mark Zandi, “U.S. Macro Outlook: Policymakers Must Get It Right,” Moody’s Analytics, July 16, 2012, https://www.economy.com/dismal/article_free.asp?cid=232471&src=mark-zandi.

[5] Mark Zandi, “An Analysis of the Obama Jobs Plan,” Moody’s Analytics, September 9, 2011, https://www.economy.com/dismal/article_free.asp?cid=224641.

[6] Alec Phillips, “US Daily: Business Investment: Bonus Depreciation Expiration Should Have a Limited Effect,” Goldman Sachs, February 25, 2014.

[7] Bloomberg BNA, “U.S. Corporate Capital Expenditures: Consciously Uncoupled From Federal Tax Incentives,” Bloomberg BNA, August 2014, http://www.bnasoftware.com/PDFs/resource-center/Whitepapers/Bloomberg_BNA_Capital_Expenditures_White_Paper.pdf.

[8] Joint Committee on Taxation.

[9] Mark Zandi, “Bolstering the Economy: Helping American Families by Reauthorizing the Payroll Tax Cut and UI Benefits,” Written Testimony Before the Joint Economic Committee, February 7, 2012, p. 7, https://www.economy.com/mark-zandi/documents/2012-02-07-JEC-Payroll-Tax.pdf; Douglas Elmendorf, “Policies for Increasing Economic Growth and Employment in 2012 and 2013,” Statement Before the U.S. Senate Committee on the Budget, November 15, 2011, http://www.cbo.gov/sites/default/files/cbofiles/attachments/11-15-Outlook_Stimulus_Testimony.pdf.

[10] Of that $276 billion ten-year cost, $254 billion would come from extending bonus depreciation permanently, while $22 billion would come from expanding it.

[11] The cost of continually extending bonus depreciation for a year or two at a time without the House’s expansion would roughly equal the $254 billion cost of making it permanent without expanding it.

[12] Chuck Marr and Joel Friedman, “House Efforts to Make ‘Tax Extenders’ Permanent Are Ill-Advised,” Center on Budget and Policy Priorities, May 7, 2014, https://www.cbpp.org/cms/index.cfm?fa=view&id=4140.

[13] Jane Gravelle, “Bonus Depreciation: Economic and Budgetary Issues,” Congressional Research Service, March 24, 2014, http://nationalaglawcenter.org/wp-content/uploads//assets/crs/R43432.pdf.

[14] Chairman Dave Camp, “Tax Reform Act of 2014, Discussion Draft Section-by-Section Summary,” Committee on Ways and Means, http://waysandmeans.house.gov/UploadedFiles/Ways_and_Means_Section_by_Section_Summary_FINAL_022614.pdf.

More from the Authors