Florida “TABOR” Proposal SJR 958 Would Endanger Education, Public Safety, and Infrastructure

Proposal Has Same Flaws as Previous Florida “Tabor” Proposals

The Florida legislature is considering a TABOR proposal, SJR 958, to limit the growth in state revenues by the combined rate of inflation and population growth. The measure would:

- Immediately and over the long term raise Florida’s cost of borrowing to invest in infrastructure, costing the state potentially tens of millions of dollars annually in increased interest payments; and

- Cause a gradual deterioration of public services like health care and education, and hinder state investments, as revenues decline over time relative to the state economy.

In short, adoption of this measure would undermine Florida’s ability to make long-term investments in areas that are key to economic prosperity and would potentially make Florida a much less attractive place to live.

If the bill passes the legislature, the measure would go to a vote of the people to decide whether to place the limit in the state constitution.

Colorado is at present the only state with a TABOR. In 2005, Colorado voters suspended the TABOR formula to halt the deluge of harmful budget cuts that had occurred and were slated to occur under TABOR. Since Colorado adopted TABOR in 1992, over 20 state legislatures have rejected TABOR, and it has been voted down in every state in which it reached the ballot.

In past years, Florida and other states have rejected TABOR because it does more than control state spending, as its proponents often claim. It requires massive reductions in vital services that residents want and need — education, health care, public safety, roads, environmental protection, and others. Previous analyses have shown that if a TABOR with the population-plus-inflation formula took effect right away in Florida, it could require cutting the state’s budget by as much as 25 percent. The Florida Taxation and Budget Reform Commission, after a full and extensive consideration in 2008, determined that TABOR was not in the best interests of state residents and declined to put it on the ballot. Similar efforts to refer TABOR measures to Florida voters failed to make it to the ballot in 2009 and 2010.

The 2011 version of TABOR created by SJR 958 differs from its predecessors. Its revenue limit, even if placed in the state constitution in 2012, would not “bite” into available revenues for several years. But the bite would eventually occur, and once it did, the measure — like the Colorado TABOR — would produce large annual budget cuts that would grow over time.

Already, Florida lags behind the rest of the country on key measures of funding adequacy for public services, such as affordable higher education, health care coverage for low-income seniors and children, and K-12 class size. Over time, SJR 958 would lead to increasingly deep cuts in the amount of revenue to meet existing and emerging needs.

Some problematic aspects of this new TABOR proposal would take effect right away, however. Florida would immediately face higher borrowing costs, which could lead to a decline in infrastructure investment. Because future payments to bondholders would be subject to the TABOR limit, and because the life of bonds sold today would typically be 15 years or more, investors would be more hesitant to invest in Florida bonds now for fear the state would have difficulty making its bond payments once the limit is in place. This would drive up the interest payments that Florida would have to pay, at a potential annual cost to the state of tens of millions of dollars.

What Would SJR 958 Do?

The following are the key provisions of SJR 958:

- The proposal would bar the state government from collecting and spending state revenues in excess of a prescribed limit. The limit for each year would equal the previous year’s limit, multiplied by the preceding five years’ average of the combined rates of annual inflation (defined as the Consumer Price Index for All Urban Consumers, U.S. city average) and population growth.

- The base year for the formula — that is, the year that would determine future years’ limits — would be fiscal year 2013-14. In addition, in each of the first four years of implementation, the limit would include an additional upwards adjustment. This adjustment would allow an additional four percentage points of growth to the limit in the first year (i.e. 2014-15), three points in the second year, two points in the third year, and one percentage point in the fourth year (2017-18). There would be no additional adjustment after the fourth year.

- The limitation would apply broadly to state taxes, fees, assessments, licenses, fines, and charges for services. There is a major exemption: State spending on the parts of the Medicaid program that are deemed “mandatory” under federal law as well as the parts that were expanded at state option before 1994 are exempt from the limit. Other exemptions include lottery revenues that are returned as prizes, receipts of the Florida Hurricane Catastrophe Fund and Citizens Property Insurance Corporation, and a few others. However, interest payments on bonds issued July 1, 2012, or later would not be exempt.

- Revenues in excess of the TABOR limit would first go to the Budget Stabilization Fund, which is intended to help the state weather a recession or emergency, until the fund reaches its maximum limit of 10 percent of the prior fiscal year’s net revenue collections for the general fund. Any additional excess revenues would be used to reduce property taxes for the required local contribution to K-12 education.

- It would take a legislative supermajority to override SJR 958. The legislature could override the limit for one year at a time with a three-fifths vote of each house. A multi-year or permanent override would be even more difficult, requiring either a two-thirds vote in each house of the legislature, or with a three-fifths vote of the legislature plus a popular vote of at least 60 percent of voters.

The Core of the Proposal: the Population-Growth-And-Inflation Formula

Like Colorado’s TABOR, SJR 958 limits state revenues to a formula based on growth in overall population and inflation. This formula does not allow a state to maintain year after year the same level of programs and services it now provides.

Instead it suppresses public services over time and hinders the state’s ability to provide its citizens with the quality of life and services they need and demand, even in prosperous times. [1]

Population

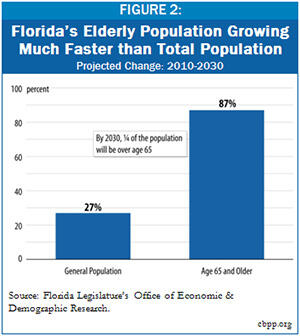

An example is senior citizens. According to Florida’s Office of Economic and Demographic Research, Florida’s total population is projected to increase by 87 percent from 2010 to 2030, while Florida’s population aged 65 and older is projected to increase three times as fast, increasing by 88 percent from 2010 to 2030.[2] As Florida’s elderly population — which will be a quarter of its total population — increases, so will the cost of providing the current level of services they have come to depend upon, such as Meals on Wheels, care for elders with Alzheimer’s or other memory disorders, vouchers to address home heating or cooling emergencies, and in-home care subsidies to help cover the expenses of food, clothing, or medical incidentals not covered by Medicaid.[3] The allowable state revenue limit, however, would prevent services like these from growing with need because it would be calculated using the much slower-growing total population. Services to the elderly could be maintained only if Florida residents were willing to make cuts in other areas of the state budget, such as education or public safety.

Inflation

The second part of the formula — inflation — also does not accurately measure the change in the cost of providing public services, and in fact, no existing measure correctly captures the growth in the costs of these services. The measure of inflation used in SJR 958 is the “Consumer Price Index for All Urban Consumers (CPI-U),” which is calculated by the U.S. Bureau of Labor Statistics. The CPI-U measures the change in the total cost of a “market basket” of goods and services purchased by an average consumer in a U.S. city. Since most urban households spend a majority of their income on housing, transportation, and food and beverages, those items are the primary drivers of the CPI-U. By contrast, the state of Florida spends its revenue primarily on education, health care, corrections, and roads. In short, the market baskets of spending are entirely different.

Moreover, the “goods”— or public services — in the state of Florida’s basket (and in every other state’s) are in economic sectors that are less likely to reap the efficiency and productivity gains achieved by other sectors of the economy. For example, teachers can only teach so many students, and nurses can only care for so many patients. As a result, the costs of these public services are rising faster than the costs in other sectors. Indeed, the items in the “basket of goods” most heavily purchased by states — such as health care, K-12 and higher education, and child care and early education — have seen significantly greater cost increases in the past decade than the items in the basket of goods purchased by urban households, and those faster-growing costs are expected to continue. [4] Limiting the growth in revenues to a formula that uses the rate of growth in general inflation will not affect the level or growth of public service costs in the economy; instead, it will affect the quantity and/or quality of public services the state is able to provide to its citizens.

The Colorado Experience with TABOR

In 1992, Colorado adopted the Taxpayer Bill of Rights (TABOR), a constitutional amendment that limits budget growth to changes in population plus inflation. A growing body of evidence shows that in the 13 years following its adoption, TABOR contributed to deterioration in the availability and quality of nearly all major public services in Colorado. The Colorado experience has serious implications for the residents of Florida because the proposed revenue cap would likely lead to similar outcomes in Florida. [5]

- TABOR contributed to substantial declines in Colorado K-12 education funding . Between 1992 and 2001, Colorado fell from 35th to 49th in the nation in K-12 spending as a percentage of personal income. [6] During that same time period, Colorado’s average per-pupil funding fell from $379 to $809 below the national average; by 2006 per pupil funding was $988 below the national average. [7]

- TABOR played a major role in the significant cuts made in higher education funding. Under TABOR, higher education funding per resident student dropped by 31 percent after adjusting for inflation. Between 1992 and 2001, Colorado’s college and university funding as a share of personal income fell from 35th to 48th in the nation and as of fiscal year 2008, the state maintained this ranking.[8]

- TABOR led to drops in funding for public health programs. Between 1992 and 2002, Colorado declined from 23rd to 48th in the nation in the percentage of pregnant women receiving adequate access to prenatal care; since 2002, the share of women receiving adequate prenatal care in Colorado has deteriorated from 67.3 percent to 64.5 percent in 2006. Colorado also plummeted from 24th to 50th in the nation in the share of children receiving their full vaccinations. Only by investing additional funds in immunization programs was Colorado able to improve its ranking to 23rd in 2008. [9]

- TABOR failed to grow the Colorado economy and may have worsened the recession. Under TABOR, Colorado saw slower job growth than other Rocky Mountain states. [10] And in the wake of the 2001 recession, Colorado actually fared worse than its neighbors: From March 2001 and January 2006 (when Colorado’s TABOR was suspended), job growth in the eight Rocky Mountain states averaged 9.3 percent; in Colorado, however, it was two-tenths of one percent.

Colorado Business and Community Leaders View TABOR as Deeply Flawed

A wide range of Coloradoans — business leaders, higher education officials, children’s advocates, and legislators of both parties, among others — recognize that TABOR has limited the state’s ability to fund critical services:

“Coloradoans were told in 1992 . . . that [TABOR] guaranteed them a right to vote on any and all tax increases. . . . What the public didn’t realize was that it would contain the strictest tax and spending limitation of any state in the country, and long-term would hobble us economically.” — Tom Clark, Executive Vice President, Metro Denver Economic Development Corporation

“The [TABOR] formula . . . has an insidious effect where it shrinks government every year, year after year after year after year; it’s never small enough. . . . That is not the best way to form public policy.” — Brad Young, former Colorado state representative (R) and Chair of the Joint Budget Committee

“[Business leaders] have figured out that no business would survive if it were run like the TABOR faithful say Colorado should be run — with withering tax support for college and universities, underfunded public schools and a future of crumbling roads and bridges.” — Neil Westergaard, Editor of the Denver Business Journal

TABOR Did Not Improve Colorado’s Business Climate

Colorado, the only state with a TABOR, has an economy that is stronger than Florida’s. However, that has nothing to do with TABOR. The strength of Colorado’s economy is largely a legacy of a post-World War II public investment boom by the military and federal government.

The federal investment left Colorado with a strong infrastructure of high-tech firms and researchers, a young, highly educated workforce, and public universities with well respected science and technology programs. By 1991, before TABOR was adopted, more adults in Colorado had completed at least four years of college than in any other state in the nation.

Other advantages, such as energy resources, natural beauty, a location in the center of the country, and massive public investment in a new Denver airport have also helped create a strong economy. (See https://www.cbpp.org/cms/index.cfm?fa=view&id=2497)

But TABOR did not cause Colorado’s success. A study by two prominent economists in the area of state and local public finance found that Colorado’s growth during the first decade under TABOR was roughly the same as what it would have been without TABOR. The study used statistical analysis to control for factors other than TABOR that could affect economic growth. (See http://www.taxpolicycenter.org/publications/url.cfm?ID=1000940).

Colorado business leaders and citizens banded together and successfully campaigned to suspend the TABOR formula beginning in 2006 and permanently change some of its most damaging features. Although the suspension now has technically expired, Colorado revenues and services remain well below the TABOR limit.

The failure to regain services during the suspension reflects the difficulty of generating enough annual revenue to improve services in the aftermath of so many years of revenue starvation. There would have to be very robust and sustained revenue growth to allow Colorado to go beyond maintaining its current, low level of services and begin to recoup lost ground. It is extremely difficult to restore services once TABOR has been in place for a long period of time.[11]

Colorado’s experience provides Florida with an important cautionary tale.

The Impact of SJR 958 on Florida

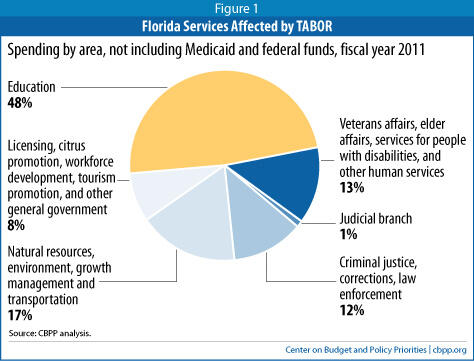

The revenues that are capped by SJR 958 pay for almost everything that the state of Florida does: education (both pre-K through 12, and higher education), transportation, natural resource protection and development, economic development and tourism promotion, public safety, administration of the court system, funds for local governments, and so on. The only major exclusion is for most of the Medicaid program. (See Figure 1.) Such services are essential for long-term economic growth and prosperity. Numerous surveys of business executives, for instance, find that a well-educated workforce, sound infrastructure, and a good quality of life are the attributes that attract them to a state to invest and create jobs.

Those services need to keep pace with Florida’s economic growth. Under TABOR, however, the state would fall short. Previous Center on Budget and Policy Priorities analyses have shown that TABOR limits would sharply reduce the funding available for education, public safety, infrastructure and other services. As the Center wrote of the 2010 bill SJR 2420:

“If Florida had adopted a TABOR in 1992, the same year as Colorado did, the limit would have forced drastic cuts in state services by 2006, before the current recession struck and falling revenue collections in the recession forced budget cuts. Compared to actual 2006 general fund revenues, Florida would have had 25 percent less funds to expend on programs and services. …

“Making a cut of 25 percent in the 2006 budget would have been equivalent to Florida eliminating two-thirds of general revenue fund support for preK-12 schools that year. …

“Alternatively, it would have been equivalent to eliminating all general revenue fund appropriations for every aspect of public safety expenditures, including prisons, courts, juvenile justice operations, crime lab services, the state parole board, public defenders, state’s attorneys, and community supervision — combined — plus all general revenue appropriations for environmental protection, transportation, fish and wildlife conservation, veterans affairs, wildfire prevention, the Governor’s office, the state legislature, the attorney general’s office, the secretary of state’s office, the state archives, the state revenue department, public funds accounting, and highway safety.” [12]

The new 2011 TABOR proposal, SJR 958, is different from last year’s proposal. One important difference is that the new bill delays implementation until 2014-2015 and then pads the growth rate for the first four years by adding several percentage points; the total padding by 2018-19 would be 10 percentage points. Another difference is that much of the state’s spending on Medicaid is exempt from the limit. As a result, the new proposal will take longer to affect the state.

Nonetheless, it is clear that before very long, SJR 958 would begin to reduce the state’s ability to finance services needed in a growing economy.

- While SJR 958 would allow revenues to grow at roughly the same rate as the economy (as measured by total personal income) between now and fiscal year 2017-18, beginning in 2018-19, revenues would begin to decline.

- By 2025, allowable revenues would be 26 percent below pre-recession levels as a share of the economy — that is, below FY 2006-07 levels. Even compared with current, extremely depressed levels for fiscal years 2010-11 and 2011-12, allowable revenues in 2025 would be more than 10 percent lower, and would fall even further in years thereafter.

A More Immediate Impact: State Bonds and Bond Ratings

A much nearer-term impact of SJR 958 is that it would result in lower bond ratings and higher borrowing costs for the state, which in turn would reduce the state’s ability to build infrastructure and squeeze other areas of spending. The reason is that the SJR 958 limit has no exemption for interest payments on state debt issued after 2012. When the limit starts to constrain the state’s revenue stream, as it inevitably will, interest payments would have to compete with other state funding obligations for an increasingly limited stream of funds. From the perspective of a potential investor, this would create the specter — however remote — that the state could default on its debt.

The cost to the state of this perceived risk could be large. An extensive study of state revenue limits and borrowing costs conducted for the Public Policy Institute of California by James Poterba, now a professor at MIT, and Kim Reuben of the Urban Institute found that “revenue limits … tend to increase borrowing costs because they hamper the state’s perceived ability to pay its long-term debt. … States with binding revenue limits pay, on average, 17.5 basis points more on their general obligation debt than states without such limits.” [13]

If that finding held in the case of Florida, it would mean an additional $1.75 million in annual debt service for every $1 billion in new bond sales. Outstanding Florida bonded debt in 2009 was about $20 billion, nearly all of it for roads, bridges, school construction, water pollution control, and conservation.[14] This suggests annual costs resulting from SJR 958 could reach $35 million or more annually, which in turn would either reduce the state’s ability to finance infrastructure or squeeze other state services.

Because many infrastructure bonds are issued for very long terms — 15 years or even longer — the prospect of future problems with bond repayment could affect investors’ behavior sooner, meaning that a TABOR proposal that might not limit revenues until after 2020 nonetheless could start affecting state borrowing costs almost right away.

Local Government

SJR 958 imposes a TABOR limit on state but not local government revenues, but that doesn’t mean local governments and schools would be protected from cuts. Local governments typically receive nearly 30 percent of their general fund revenues through intergovernmental transfers, largely from state government.[15] If the state is forced to reduce spending, local governments may feel the squeeze as well.

As the state reduces the public services it provides, the pressure on local government to meet the needs of Floridians would increase. With less revenue and more demand for services, local governments would be forced to either raise taxes and fees or cut services.

New Investments, Federal Mandates, and Leveraging Federal Dollars

State and local governments would also find it extremely difficult to make new investments, meet federal mandates, or leverage additional federal dollars under SJR 958. For example, the rigidities of formula-based budgeting, such as a population-and-inflation growth factor, do not allow funding of new priorities that may be embraced by the public, as has happened in the past with initiatives to reduce class sizes or put in place more stringent corrections policies.

SJR 958 also could impede the ability of the state and localities to adapt to federal mandates that require states to spend more in specific areas, such as security and education, or to recieve additional federal dollars for specific priorities. For example, under the American Recovery and Reinvestment Act of 2009, access to federal support for K-12 education required that Florida maintain state spending on education at 2006 levels. Florida was unable to do so; fortunately, the bill contained a “waiver” provision allowing severely recession-impacted states like Florida and a few others to still receive the money, which kept thousands of teachers and others from being laid off. In the absence of such a waiver provision, a measure like SJR 958 could have impeded Florida’s ability to take advantage of those funds had Florida had insufficient revenues to meet the requirement.

SJR 958 also has no provisions for emergency spending on natural disasters or other unanticipated problems. When Florida suffers hurricanes, flooding, oil spills, or other emergencies, government must be ready to step in to help people get through tough times. Beyond use of reserves and the state hurricane trust fund, SJR 958 would make handling emergencies more difficult than it otherwise would be.

How Far Can Florida Fall?

When Colorado adopted TABOR it ranked in the middle of the pack among states on a number of key public services. Under TABOR, Colorado fell to the bottom of states on many of those rankings and despite TABOR’s suspension in 2005, the state has been unable to recover in a number of areas. Florida, unlike Colorado prior to TABOR, already ranks among the lowest-performing states on a range of education and health care measures:

- Florida ranks 49th in the nation in K-12 spending as a percentage of personal income. [16]

- Florida ranks 35th in average per-pupil funding, $1,213 less per student than the national average. [17]

- Florida ranks 37th in the nation in the average number of students per teacher. [18]

- Florida ranks 41st among the states in state funding of higher education per $1,000 of personal income. [19]

- Florida ranks 48th in the percentage of low-income, nonelderly adults with health insurance. [20]

- Florida ranks 50th among the states in its share of low-income children with health insurance. [21]

Florida also has undergone substantial cuts to education and other fundamental services during the recession and in its wake. For example, Florida’s 11 public universities raised tuition by 32 percent within a two-year period and the state has cut back support for K-12 education. Because SJR 958 would prevent revenues from returning to pre-recessionary levels, it would lock in these cuts and permanently depress state support for investments that the state’s residents and businesses want and need.

Adopting the proposed revenue cap, which would restrict the amount of money available to fund these key programs at both the state and local level, would be devastating to Florida. It would hurt not only Florida’s children and adults, but also the economy, which relies on educated individuals and up-to-date infrastructure in order to grow.

Could Florida Override SJR 958?

It would be difficult for Florida to override the TABOR limit. The limit would be enshrined in the state constitution, and would require a supermajority of each house of the legislature to override or amend.

Supermajority requirements can be a recipe for gridlock. Until very recently, California required a supermajority vote in each house of the legislature to enact its annual budget — the only major industrial state (and one of only three nationwide) to have such a requirement. This requirement was widely blamed for California’s perennial difficulty passing a budget. As the Los Angeles Times noted, “Supermajority budgeting rules … have all but brought state government to a standstill.”

Supermajority budget rules also increase the power of individual legislators to demand state funding for pet projects, in return for agreeing to provide the necessary votes so legislation containing revenue-raising measures could obtain supermajority support and pass. To be sure, such vote-swapping can occur under simple-majority rules as well. But as the California Citizens Budget Commission — a blue-ribbon bipartisan body — noted, the degree of vote-swapping tends to intensify along with the level of difficulty of obtaining the necessary votes to pass a budget. The level of difficulty is much greater when a supermajority is required. And, in fact, the Commission found evidence that California’s supermajority rule led to enactment of “pork-barrel” legislation.

Responding to the problems created by California’s supermajority rules, voters in California removed the supermajority budget requirement from the state constitution by a popular vote in November 2010.

End Notes

[1] For a more detailed analysis of the problems with the population-growth-plus-inflation formula, please see David Bradley, Nick Johnson and Iris Lav, “The Flawed ‘Population Plus Inflation’ Formula: Why TABOR’s Growth Formula Doesn’t Work,” Center on Budget and Policy Priorities, January 2005.

[2]Florida Legislature’s Office of Economic & Demographic Research, Demographic Estimating Conference Database, http://edr.state.fl.us/Content/population-demographics/data/Pop_Census_Day.pdf.

[3] See the Florida Department of Elder Affairs for more information on services offered http://elderaffairs.state.fl.us/english/programs_services.php

[4] From 2000 to 2010, the overall CPI-U rose 27 percent, but education costs rose 77 percent, and medical costs rose 48 percent. Costs for fuel and child care/nursery school rose 55 percent and 54 percent respectively. And these are costs to consumers, not costs to governments. Rapidly growing education and health costs are a much higher percentage of state budgets than consumer budgets.

[5] For a more detailed analysis of the problems experienced in Colorado under TABOR, please see Iris J. Lav and Erica Williams, “A Formula for Decline: Lessons from Colorado for States Considering TABOR,” Center on Budget and Policy Priorities, March 15, 2010.

[6] Center on Budget and Policy Priorities calculation of National Center for Education Statistics data (Table 176. Current expenditures for public elementary and secondary education, by state or jurisdiction), and Bureau of Economic Analysis quarterly personal income data ( http://www.bea.gov/regional/sqpi/).

[7] CBPP analysis of National Center for Education Statistics data (Table 184. Current expenditure per pupil in fall enrollment in public elementary and secondary schools, by state or jurisdiction).

[8] “Grapevine Annual Compilation of Data on State Tax Appropriations for the General Operation of Higher Education (2008),” Center for the Study of Education Policy, Illinois State University

[9] United Health Foundation analysis of National Center for Health Statistics data, http://www.americashealthrankings.org/Measure/2009/List%20All/Prenatal%20Care.aspx .

[10] Karen Lyons and Nicholas Johnson, “Education and Investment, Not TABOR, Fueled Colorado’s Economic Growth in 1990s,” Center on Budget and Policy Priorities, March 2006.

[11] Iris J. Lav and Erica Williams, “A Formula for Decline: Lessons from Colorado for States Considering TABOR,” March 2010.

[12] Michael Leachman, Iris J. Lav and Erica Williams, “Education, Health, Public Safety, and Infrastructure Would Decline Under SJR 2420’s Proposed TABOR Limit,” April 2010.

[13] James M. Poterba and Kim S. Rueben, Fiscal Rules and State Borrowing Costs: Evidence from California and Other States, Public Policy Institute of California, 1999.

[14] Florida Department of Financial Services, 2009 Comprehensive Annual Financial Report, p. 101.

[15] U.S. Census Bureau, Survey of State and Local Government Finances, http://www.census.gov/govs/estimate/.

[16] Center on Budget and Policy Priorities calculation of National Center for Education Statistics data (Table 176. Current expenditures for public elementary and secondary education, by state or jurisdiction), and Bureau of Economic Analysis quarterly personal income data ( http://www.bea.gov/regional/sqpi/).

[17] National Center for Education Statistics, “Revenues and Expenditures for Public Elementary and Secondary Education: School Year 2007-08 (Fiscal Year 2008)”, May 2010.

[18] CBPP analysis of National Center for Education Statistics data (Table 66. Teachers, enrollment, and pupil/teacher ratios in public elementary and secondary schools, by state or jurisdiction).

[19] Grapevine Compilation of Data on State Tax Appropriations for the General Operation of Higher Education (2008), Center for the Study of Education Policy, Illinois State University.

[20] Center on Budget and Policy Priorities’ analysis of the Annual Social and Economic Supplements to the 2008 and 2009 Current Population Surveys. Rankings include the District of Columbia.

[21] U.S. Census Bureau, Current Population Survey, 2009 Annual Social and Economic Supplement, “Table HI10. Number and percent of children under 19 at or below 200% of poverty by health insurance coverage and state: 2008,” http://www.census.gov/hhes/www/cpstables/032009/health/h10_000.htm. Rankings include the District of Columbia.

More from the Authors

Areas of Expertise