Corporate Tax Cut Benefits Wealthiest, Loses Needed Revenue, and Encourages Tax Avoidance

The major tax legislation enacted last December suffers from three fundamental flaws: it’s skewed to the wealthy, fiscally irresponsible, and encourages rampant tax gaming and avoidance.[1] The deep cut in the statutory corporate tax rate from 35 percent to 21 percent is the centerpiece of the 2017 tax law and contributes to all three of these major flaws: the corporate tax cut is skewed to the top since it mostly benefits wealthy shareholders and highly compensated employees such as CEOs; it loses much-needed revenue; and by placing the corporate tax rate far below the top individual tax rate, it creates a significant potential tax sheltering opportunity for wealthy Americans.

The case for a large corporate cut was based on a series of misleading arguments. Proponents, for example, argued that it was required to keep the United States “competitive” as the U.S. corporate tax rate was far higher than other countries’. These analyses typically focused on the statutory rate instead of the rates that companies actually paid and did not focus on comparisons with other large, high-income countries. When proper comparisons were made, the U.S. corporate tax was in line with similar countries’ rates.[2]

Heavily Tilted Toward Wealthy

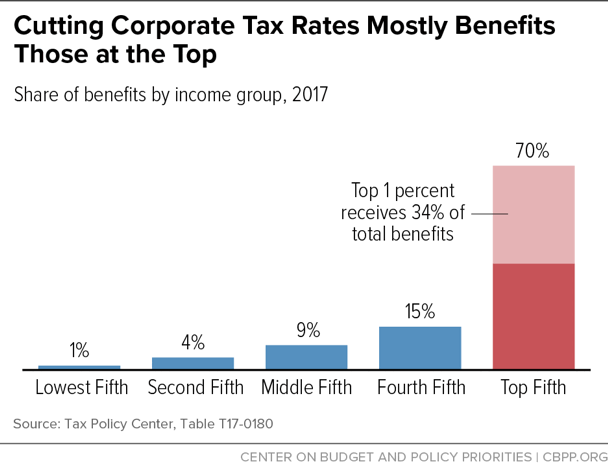

The deep cut in the corporate tax rate is heavily tilted to the top: the Tax Policy Center estimates that a third of the benefits from corporate rate cuts will ultimately flow to the top 1 percent of households, not ordinary workers (see first chart). Proponents of the corporate tax cut say it will substantially benefit working- and middle-class Americans by causing companies to invest more, increasing economic growth and raising workers’ wages. In reality:

- The bill’s growth effects will likely be modest. Non-partisan estimates of its effect on the economy show that it will only modestly boost growth. That’s in part because the law increases the deficit, which reduces national saving, leaving less capital available for investment and causing interest rates to rise.

- U.S. income gains will likely be even smaller than gross domestic product (GDP) gains. One reason is that GDP includes income that accrues to foreign investors. The Congressional Budget Office (CBO) estimates that an average of 43 percent of the additional real income resulting from the bill will accrue to foreign investors over 11 years. Another is that some of the additional GDP won’t go to higher incomes but instead to offsetting the wear and tear (depreciation) of the modest amount of new investment in machines and other capital spurred by the rate cut.[3]

- Mainstream economic research concludes that over 75 percent of the benefits of corporate rate cuts go to shareholders — a disproportionately wealthy group. And, even the modest part of a corporate rate cut that will flow to workers will likely do so in proportion to their share of total wage and salary income. A large portion of that income flows to CEOs and other highly paid executives; only a modest portion goes to workers in the middle and bottom, who have been hurt most by slow wage growth of recent decades.

- Lower- and middle-income families pay for part of the corporate tax cuts in later years. As one of the few parts of the law that is permanent, the corporate tax cuts’ long-run cost had to be offset because of the requirements of the legislative vehicle (“reconciliation”) that Congress used to consider the measure. But the law didn’t increase taxes on corporations enough to offset the cost of its corporate tax cuts (see below). Instead, their remaining cost was paid for in later years by cutting health care (reducing health coverage primarily for low- and middle-income families and increasing premiums in the individual market) and by adopting a new inflation measure (the “chained” Consumer Price Index) that will raise taxes on households at all income levels by slowing the annual adjustment of tax brackets and other tax provisions.

Loses Much-Needed Revenue

The 2017 tax law will cost $1.9 trillion from 2018 to 2027, according to CBO. The law could generate additional economic growth to offset a small share of this revenue loss, CBO estimates, but after adding interest costs from the new debt that the law will incur, it will still add $1.9 trillion to the deficit. The corporate tax cut is a major contributor to these revenue losses. The 14-percentage-point rate cut loses $1.3 trillion over ten years, according to the Joint Committee on Taxation. The law includes some provisions that broaden the tax base, but the net corporate tax cut is still $329 billion. The ten-year cost is even higher — $668 billion — after excluding revenue from a one-time tax on multinationals’ existing foreign profits, which cannot offset the long-term costs of the permanent rate reduction and would have been a better used to pay for investments in infrastructure (as lawmakers of both parties considered before 2017).

These revenue losses are irresponsible given the fiscal challenges the nation will face over the next several decades, such as the aging of the population, health care costs likely continuing to rise faster than the economy, interest rates returning to more normal levels, potential national security threats, and challenges such as large infrastructure needs that cannot be deferred indefinitely. The nature and magnitude of these fiscal pressures will require revenue to rise as a percentage of GDP to prevent an unsustainable rise in the nation’s debt ratio over coming decades.

Risks Encouraging Tax Sheltering

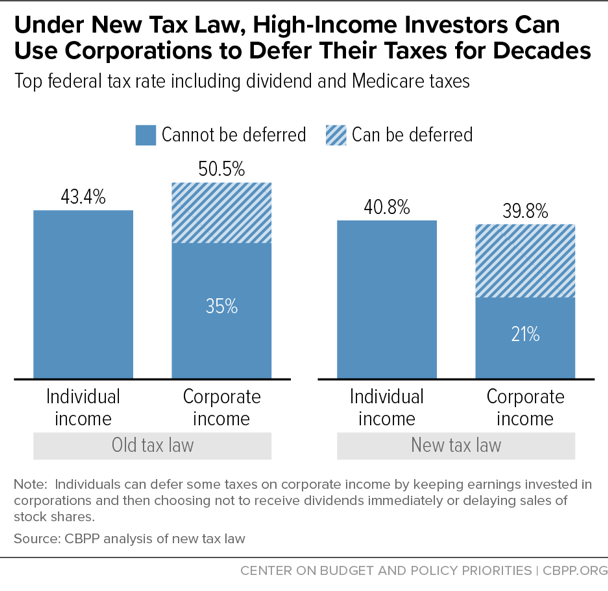

The corporate tax rate cut may also create a tax shelter. Under prior law, income subject to the top individual tax rate was taxed at a lower rate than corporate income after incorporating dividend and Medicare taxes. Now the rates are similar, but — unlike with individual income — taxpayers can defer the second level of tax by, for example, delaying dividend distributions.

High earners and wealthy investors may be able to shield income from the top individual rate by setting up a corporation and reclassifying income as corporate profits. Income sheltered inside a corporation can compound and grow more quickly because it faces only a 21 percent tax each year, instead of the 40.8 percent rate under the individual income tax (see second chart). The owner might eventually owe dividends or capital gains taxes on the wealth that has accrued in the corporation, but those taxes can be deferred for decades and even avoided altogether by, for example, passing on the corporation to heirs using the “step-up basis” loophole. The new law did not include new anti-abuse rules to protect against this sheltering, and existing rules are weak.

End Notes

[1] For further information, see Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” Center on Budget and Policy Priorities, April 9, 2018, https://bit.ly/2HmWnzD.

[2] CBPP, “Actual U.S. Corporate Tax Rates Are in Line with Comparable Countries,” https://bit.ly/2wB8bsa.

[3] Benjamin R. Page and William G. Gale, “CBO Estimates Imply That TCJA Will Boost Incomes For Foreign Investors But Not For Americans,” Tax Policy Center, https://tpc.io/2IDB8cw.