Double Jeopardy for Local Services Under TABOR

Property Tax Increases are Likely Result

Proponents of Maine’s TABOR (Taxpayer Bill of Rights) — a ballot initiative that would place strict spending limits on state and local governments — have been marketing this proposal as a property tax relief package.[1] This is false advertising: TABOR would not create a sustainable reduction in property taxes. Instead, towns and cities would feel more and more pressure to maintain or even raise property taxes through the voting mechanisms provided under TABOR.

TABOR would squeeze the state budget, likely leading to cuts in state aid for local services. If citizens were unwilling to tolerate the resulting larger class sizes, fewer teacher aides, or other declines in education quality, their only option to remedy the situation would be to vote for higher property taxes — the one revenue source localities control. In Colorado, the only state with a TABOR, there were hundreds of successful votes to increase local taxes.

TABOR would also force cuts in local public services by squeezing the budgets of towns and cities. While this squeeze might initially depress property taxes, over time the TABOR-mandated cuts in property taxes would cause a substantial deterioration in public services. Here too, citizens would be unlikely to accept the resulting reduced public safety, crumbling roads and poorer education standards and would be likely to vote to override the local TABOR limit. In doing so, they would cancel most, if not all, of the TABOR-mandated property tax cuts. In Colorado, voters in 88 percent of all municipalities and 94 percent of all counties in the state have voted to override their TABOR limits and thus forgo tax cuts.

If Mainers enact TABOR believing it will lower their property tax bills without harming the public services upon which they depend, they will be disappointed. Such property tax relief is possible, and actions by other states provide examples of how this can be done without enacting a TABOR. Ironically, for reasons described in this analysis, none of the property tax relief packages implemented in other states would have been possible had those states been constrained by TABOR.

State Aid to Localities Likely to Decline Under TABOR; Dependence on Property Taxes Would Increase

Maine’s TABOR is a ballot initiative that uses rigid, unrealistic formulas to severely limit state and local expenditures. It is modeled after a constitutional amendment adopted in 1992 in Colorado with the same name. In Colorado, TABOR limited state expenditures from year to year by the change in the overall population plus the rate of inflation. This population-plus-inflation limit caused significant damage to the state’s public services.[2] In order to allow the state to restore a portion of these fundamental public services, Coloradoans voted in November 2005 to suspend the TABOR limit for five years. To date, Colorado is the only state to have ever adopted a TABOR.

To limit state expenditures, Maine’s TABOR employs the same population-growth-plus-inflation formula as Colorado’s TABOR.[3] Using this formula to restrict state expenditures is highly problematic because it does not accurately measure the costs the state faces to provide goods and services to its citizens (such as health care, the cost of which has been increasing at rates significantly greater than the general rate of inflation) or the more rapid growth of some of the most costly to serve subpopulations in the state (such as the elderly and prisoners).[4] Thus, in order to adhere to the limit, Maine would have to make cuts in its programs and public services.[5]

As the state budget is squeezed down under the TABOR limit, state aid to localities would be a likely candidate for reductions. It is the largest expenditure category in the state’s budget, accounting for 36 percent of all expenditures. Moreover, aid to localities would be competing for funding against other important public service areas such as health care and infrastructure.

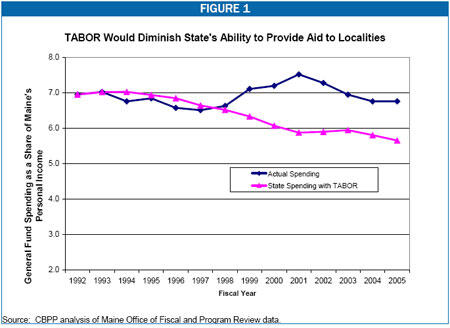

For example, if Maine’s state spending had been limited to changes in population plus inflation from when Colorado adopted its TABOR in 1992 to 2005, the cumulative required cuts in state expenditures would have totaled $2.9 billion (See Figure 1). [6] In 2005 alone, the TABOR limit would have required the state to spend 16 percent less than it actually did, which would have meant a budget cut of $448 million. If this $448 million cut had been distributed proportionally across all expenditures, state aid to localities would have been cut by over $157 million:

- Aid to localities for education would have been reduced by $148 million

- Aid to localities for property tax reimbursements (i.e. the homestead exemption) would have been reduced by $6.1 million

- Aid to localities for criminal justice (i.e. community based corrections) would have been reduced by $1.9 million; and

- Aid to localities for general assistance would have been reduced by $940,000.[7]

Property Taxes in Maine Fund Essential Public Services

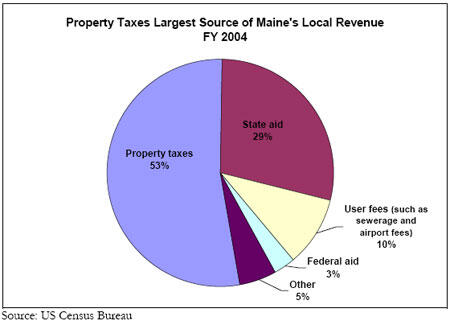

Maine’s towns and cities provide their residents with a number of important services, including K-12 education, police and fire protection, winter and summer road maintenance, economic and community development, issuance of licenses, recreation, parking, solid waste collection and disposal, water and sewer services, emergency medical services, and health and human services. The main source of revenue to provide these services is the property tax since Maine, unlike some other states, does not have a local sales or income tax.

The property tax, in addition to being localities’ largest source of revenue, is also the only revenue source localities control. As such, it allows localities to provide the type, amount and quality of public services their residents desire. For instance, if residents in a town decide they would like to improve their roads, provide their police or fire department with certain equipment, or expand their recycling program, then property taxes will provide them the means to do so. Similarly, if the state is not providing enough revenue for a city to provide an adequate level of services, the city can use property taxes to make up for this shortfall. Or, if localities feel that they have more revenue than necessary to provide public services, they can lower property taxes.

While the state might not choose to distribute cuts proportionally, it is difficult to imagine that the state could achieve budget cuts of this scale without cutting local aid, the largest single part of the budget. Indeed, it is highly probable that the state would choose to cut aid to localities by an even larger fraction than other areas of state expenditures on the theory that localities could fend for themselves. That is, localities could make up this shortfall by raising the one revenue source they control: the property tax.

Localities would likely choose this option since a significant loss in state aid could cripple their budgets and their ability to provide public services. Localities get almost one-third of their revenue from the state (See box above). The largest recipient of this aid is K-12 education, which gets roughly half of all of its funding from the state. Reductions in state aid for schools could lead to lower teacher salaries, larger class sizes, the inability to buy needed school supplies, or fewer teacher aides. Reductions in other types of state aid to localities, such as general assistance, property tax reimbursements, economic development, criminal justice and emergency and disaster relief, would also have serious consequences. For instance, localities might not be able to afford as many security officers in the county jails or the current level of the homestead exemption.

Local Revenue Collections Did Not Fall in Colorado

Since TABOR’s adoption, local revenue collections in Colorado have remained constant relative to people’s income. The only change has been the composition of this revenue. Property tax collections as a share of personal income have fallen slightly since TABOR’s adoption (due to pre-existing property tax limits), but voter-approved increases in sales tax and other taxes, coupled with increases in fees, have offset this slight decline. Voters approved these tax increases in order to maintain services.

| COLORADO LOCAL GOVERNMENT REVENUE AS A PERCENT OF PERSONAL INCOME | ||||

| Fiscal Year | Own Source | Property Tax | Sales Tax | Fees and Other Taxes |

|---|---|---|---|---|

| 1992 | 7.9% | 3.3% | 1.3% | 3.3% |

| 2004 | 7.9% | 3.0% | 1.4% | 3.5% |

In Maine, residents would not enjoy the same flexibility as in Colorado. The only tax localities could vote to increase would be the property tax, as local sales taxes do not exist in Maine. Moreover, unlike in Colorado, fee increases would also have to be approved by voters.

Thus, under TABOR, localities’ dependence on property taxes would likely increase, as towns and cities would have to rely on them to make up for TABOR-mandated cuts in state aid.

The Local TABOR Limit Would Not Guarantee Property Tax Cuts

TABOR, in addition to affecting cities and towns through the state limit on expenditures, would also impact localities by directly limiting their own budgets. The TABOR limit formula for the expenditures of towns and cities is the change in the locality’s population plus inflation (the same formula used at the state level) or the change in assessed value of the locality’s real and personal property, whichever is less.[8] This limit is even more restrictive than the local limit in Colorado’s TABOR.[9]

The local TABOR formulas do not accurately capture how much it costs from year to year for towns and cities to provide their residents with public services; they do not allow sufficient growth even to maintain the current level of services. A recent analysis by the Maine Municipal Association (MMA) found that about half of all municipalities would have been able to increase their budgets by less than one percent for 2006 had TABOR been in effect for that year. Furthermore, more than one-third of all municipalities either would not have been able to increase their budgets at all or would have had to reduce their budgets below the amount expended in the previous year.[10]

If budgets are so severely constrained, services will deteriorate. If the cost of heating the schools or buying gas for school buses increases, would the town or city lay off teachers to cover those costs? (In some Colorado schools, the children studied in down coats and gloves.) If a particularly snowy winter requires a lot of overtime to keep the roads clear, would potholes remain unrepaired in the spring? And if a locality must go year after year without increasing the salaries of its employees, would the most productive and competent of those employees stay or would they look for other opportunities — potentially reducing the quality of services provided? These are just some of the ways services would deteriorate under the strict and rigid limits of TABOR.

Limiting the expenditures of towns and cities under the TABOR limit for localities would not necessarily have the effect on property taxes that one might expect. While TABOR might initially depress property taxes, maintaining the artificially -reduced level would be very difficult and would come at a very high cost. TABOR would not change the amount or type of public services, such as education, road maintenance, and public safety, that localities are expected to provide to their residents. Nor would it lower the costs of providing these services. Instead, TABOR would make it nearly impossible for localities to continue providing the same quantity and quality of public services to their residents.

Towns and Cities Likely to Override Local TABOR Limit to Avoid Cuts in Public Services

Localities would be faced with a double problem — reductions in state aid and tight constraints on the growth of the local budget — in their efforts to provide services for their residents. The only way to alleviate the problem would be to ask residents to override the TABOR limit on the ballot. If the TABOR limit would otherwise result in property tax cuts, the residents could vote to cancel those cuts or even increase rates — and devote the proceeds to maintaining or improving schools, roads, emergency services, or recreation facilities. Such an override vote would be the only way to avoid the deterioration of services that TABOR would require.

While it may not sound plausible to believe that residents would vote to cancel their tax cuts or increase their taxes, this is exactly what happened in the only state to have ever enacted a TABOR: Colorado. In 88 percent of all municipalities and 94 percent of all counties in Colorado, residents have voted to override their TABOR limits and thus forgo tax cuts (see Table 1). While some of these elections suspended the limit for a defined time period (e.g. two years), many of the successful override proposals allowed localities to permanently come out from under the limit.[11] A full 31 percent of municipalities and 69 percent of counties have permanently rejected the TABOR limits.

LD 1 May Provide Mainers with Property Tax Relief

Last year, Maine enacted LD 1, the overall objective of which is to lower Maine’s total state and local tax burden — the share of income Maine residents pay in state and local taxes — below those of other states.

LD 1 has three main components: 1) growth limits on state and local governments based on the growth of personal income; 2) an increase in the state’s contribution to education expenditures from 50 percent to 55 percent, with 90 cents of every dollar of this additional state aid going towards reducing property taxes; and 3) expansion of the circuit breaker program., which provides property tax relief for people whose property tax bills exceed 4% of their income.

While it is too soon for the effects of LD 1 on property taxes to be fully known, the initial results are promising. Actual budget growth for the 143 municipalities affected by LD 1 last year was less than that permitted by LD 1 (2.53 percent vs. 4.8 percent).i Moreover, in 46 of these towns and cities, property taxes actually fell by an average of 7.5 percent.ii

It might be prudent for Mainers to give LD 1 time to work before seeking other options for property tax relief. In any case, Mainers should recognize that TABOR is unlikely to fulfill their desire for property tax relief.

i Because over half of the municipalities in Maine do not use a fiscal year, they have yet to be affected by LD 1.

ii Maine State Chamber of Commerce and Maine Municipal Association, “Analysis of First Year Impact of Impact of LD 1,” February 2006.

In addition, there were 367 successful votes in Colorado to increase local taxes, including property taxes. Voters saw the damage the TABOR limit was causing to the public services they cared about and they refused to let it continue. Maine residents would likely find themselves in a similar situation if TABOR were to pass.

Thus, under TABOR, localities would face pressure from both the local limits and reductions in state aid to at a minimum maintain property tax levels and even possibly to increase them. Property taxes would be unlikely to decline in the vast majority of Maine cities and towns.

Examples of Long-Term Property Tax Relief that Does Not Hurt Public Services

TABOR may at first blush sound attractive because many Maine residents would like lower property taxes or at least assurances that their property taxes will not increase. In that desire, Mainers are similar to many other people around the country. And to accommodate that desire a number of other states that do not have TABOR limits have found ways to provide property tax relief without decimating the quality of life in the state.

| TABLE 1: | ||

| Municipalities | Counties | |

|---|---|---|

| Number of localities in state | 271 | 64 |

| Number that have passed overrides of their TABOR limit | 238 (88%) | 60 (94%) |

| Number that have permanently rejected their TABOR limit | 83 (31%) | 44 (69%) |

Ideally, property tax relief would lower residents’ property tax bills, while still allowing the state and/or locality to provide residents with the public services upon which they depend. This type of relief is possible, but it usually requires making trade-offs—the revenue loss from cutting property taxes is made up by an increase in another tax that people in the state may prefer. Several states over the last 15 years have enacted legislation that protects public services and cuts property taxes.

- In Michigan, property taxes, or more specifically, the state’s reliance on property taxes to fund schools was reduced by increasing the statewide sales tax.

- In South Carolina, the legislature increased the sales tax in order to be able to remove school operating taxes from homeowners’ property tax bills, reducing these bills by about 50 percent.

- In Indiana, property taxes were reduced when the state pledged to provide localities with more state aid. The state was able to increase aid by raising the cigarette tax and the sales tax.

- In Idaho, property taxes are expected to fall as property tax revenues will no longer be used to pay for school maintenance and operations levies. Instead, they will be paid for by an increase in the sales tax and other general state revenues.

- New Jersey is currently planning significant property tax reductions that will be paid for with changes to the state sales tax.

Different people may or may not agree with the choices these states made. But all of these reforms were made after policymakers seriously examined the state’s tax structure, considered the pros and cons of different options to change it, and ultimately enacted legislation that they thought best suited the interests of their citizens. None of them required adopting a TABOR.

And most — if not all — of these reforms would not have been possible under TABOR. In each case, property taxes were relieved because the state agreed to fund a greater share of services through state rather than local revenue sources. Yet TABOR makes it nearly impossible for the state to continue providing the current level and quality of services; there is no room for it to increase either aid to localities or the proportion of local services it funds. Moreover, it is unlikely that TABOR’s override mechanisms could be used to achieve this type of property tax relief. Under TABOR, the necessary increases in state revenue would require the approval of two-thirds of the legislature, as well as a majority of the voters — a prohibitively high hurdle to surmount.

Conclusion

TABOR would not lead to sustainable property tax cuts, but rather could result in an increased dependence on property taxes. State aid to localities would likely decrease as a result of TABOR squeezing the state budget. In order to make up for this shortfall, localities would have to increase property taxes because it is the only revenue source they control. At the local level, TABOR would cause towns and cities to make cuts in public services, such as such as education, transportation, police and fire, and criminal justice. Cities and towns would likely vote to override their TABOR limits to avoid having to make such cuts, thus canceling much or all of the TABOR-mandated reductions in the property tax.

Other states have successfully implemented property tax relief that has lowered property tax bills without hurting public services and none of these required enacting a TABOR. In fact, these reforms would not have been possible with a TABOR. Mainers need to understand that TABOR would not provide such property tax relief and would impede any future efforts to do so.

[1] For instance, Mary Adams said the vote on TABOR “sets the stage” for lower property taxes in Maine. “TABOR advocate stumps in Biddeford,” Journal Tribune, July 24, 2006. J. Scott Moody from the Maine Heritage Policy Center, which authored TABOR, writes that “lower property taxes are approximately half of the total tax savings created by the Taxpayer Bill of Rights.” J. Scoot Moody, “A Taxpayer Bill of Rights: Improving Mainer’s Incomes,” Maine Heritage Policy Center, Sept. 12, 2006.

[2] Technically, the Colorado TABOR limited the amount of revenues that could be expended, which for practical purposes the same as limiting expenditures. For more information, see David Bradley and Karen Lyons, “A Formula for Decline: Lessons from Colorado for States Considering TABOR, Center on Budget and Policy Priorities,” October 2005. Available at: https://www.cbpp.org/10-19-05sfp.htm.

[3] At the state level, the limit applies to the General Fund, the Highway Fund, Quasi-governmental agencies and Other Special Revenue Funds. Since the General Fund is the largest and funds a greater diversity of programs than the other funds, only it will be discussed.

[4] According to the US Census Bureau, Maine’s total population is projected to grow 11 percent between 2000 and 2030. Its population aged 65 and over, however, is projected to grow 104 percent during this same period.

[5] For more information, see Iris J. Lav and Karen Lyons, “The Same Old TABOR: Maine's "Taxpayer Bill of Rights" Proposal Fails to Fix Flaws of Colorado's TABOR,” Center on Budget and Policy Priorities, March 2006. Available at: https://www.cbpp.org/3-16-06sfp.htm.

[6] Spending data in Figure 1 is from the Maine State Legislature, Office of Fiscal and Program Review. To calculate state spending with a TABOR, the previous year’s allowable spending limit was multiplied by the sum of the percent growth in population plus inflation.

[7] Dollar amounts were calculated based on data from Maine’s Office of Fiscal and Program Review.

[8] The formula for school administrative units—school administrative districts (SAD) and community school districts (CSD) — is percent change in student enrollment plus inflation. This paper does not attempt to discuss the effects of TABOR on school administrative units, as they make up only 30 percent (87 out of 290) of all school districts and cover a number of municipalities. For an analysis on these units, please see the Maine Municipal Association http://www.memun.org/public/MMA/svc/SFR/TABOR/TABOR2.htm#ana.

[9] In Colorado, local district's fiscal year spending is limited to inflation plus the change in real property values (or student population for school districts).

[10] The MMA finds that 36 percent of localities (172 of Maine’s 484 municipalities) would have had to enact budgets in FY 2006 that were lower than their FY 2005 budgets. Proponents of TABOR insist that the TABOR proposal would not require towns and cities to reduce their budgets from year to year, but rather keep their budgets constant in nominal dollars when the formula yields a negative growth rate. Thus the interpretation of the measure is in dispute and likely to end up in the courts.

[11] Maine’s TABOR would not allow as much flexibility; instead it would force residents to vote year after year to override the limit. Nonetheless, experience suggests that local voters are willing to increase local property taxes if the alternative is a reduced level of public services.

More from the Authors