Allowing High-Income Tax Cuts to Expire on Schedule Would Be Sound Economic and Fiscal Policy

In his State of the Union address, President Obama called for allowing the Bush-era tax cuts for high-income Americans to expire on schedule at the end of the year. Critics already are attacking this proposal as an unwarranted tax increase that would harm the weak economy and kill large numbers of jobs, especially among small businesses.

These criticisms fly in the face of a wealth of fiscal and economic evidence.

- Allowing tax cuts to expire for married filers with incomes above $250,000 and single filers with incomes above $200,000— the top 2 percent of U.S. households[1] — will avert $826 billion in added deficits and debt over the next ten years. The savings from allowing the top two marginal tax rates to expire for those high-income households constitute $443 billion of that $826 billion. [2] There is broad consensus among economists and fiscal policy analysts that the deficit and debt levels the government will experience if current tax and spending policies are continued will ultimately be harmful to the economy.

- A Congressional Budget Office analysis issued this month makes clear that extending the tax cuts for high-income households would be the least effective of all spending and tax options that CBO examined for boosting the weak economy and creating jobs. It comes in dead last.

- The sounder policy would be to let the high-income tax cuts expire on schedule and to temporarily use the savings for tax or spending measures that would lead to more jobs and economic growth in the next year or two. For example, a job creation tax credit for businesses — small and large — and additional money to help states avoid additional layoffs would be a more effective use of funds.

- If the goal is both to shore up the economy in the short term and to address unsustainable long-term deficits and debt, then allowing the high-income tax cuts to expire and using the savings for effective stimulus in the short term and deficit reduction after that would represent the soundest course.

- Claims that small businesses would be badly injured and many jobs lost as a consequence are based on misleading use of data. Fully 97 percent of taxpayers with business income would not be touched because they have income below $250,000 (or $200,000 for single filers). Moreover, many of those with business income who would be affected are not small business proprietors, but rather wealthy corporate executives, Wall Street traders, corporate lawyers, doctors, and the like who have some business investments that yield them passive business income. In terms of job creation, it would be far more efficient to provide a temporary tax credit to small businesses for job creation than to give more tax cuts to the highest-income people, who would save much of the money.

The President’s proposal also responds to the stunning increase in income disparities over the past decade. A remarkable two-thirds of the total increase in income in the United States over the economic expansion from 2002 through 2007 went to the top 1 percent of Americans. [3]

Key Tax Policy Decision Is Approaching

Most of the tax cuts enacted in 2001 or 2003 are slated to expire at the end of 2010, including those that disproportionately benefit the highest-income Americans. President Obama has proposed to allow various high-end tax cuts, including the cuts in the top two income tax brackets, to expire on schedule. If this occurs, the top income tax rates will return to 36 and 39.6 percent — the rates under President Clinton — from the 33 and 35 percent rates enacted under President George W. Bush.

Proponents of extending the high-end tax cuts have already begun to argue that the economy will perform better if Congress extends all of the tax cuts rather than allowing those for the highest-income Americans to expire. For example, Senate Republican Leader Mitch McConnell (R-KY) recently made this case on the Senate floor, stating that “struggling small businesses are asking themselves whether they can hire new workers: the prospect of a massive tax hike makes it far less likely they will.”[4] A group of six House Democrats made a similar case to the President in a letter this week.[5] Recent analysis by the Congressional Budget Office (CBO) and other nonpartisan experts demonstrates, however, the weakness of this argument.

The CBO Analysis

In a report issued this month, Policies for Increasing Economic Growth and Employment in 2010 and 2011, [6] CBO examined 11 options to stimulate growth and job creation. The options included boosting unemployment insurance benefits, increased infrastructure spending, state fiscal relief, extending the expansions in refundable tax credits for low- and moderate-income households that were included in last year’s economic recovery legislation, providing an additional one-time payment to Social Security beneficiaries, providing a tax credit to employers for new hires, temporarily suspending the employer or employee share of payroll taxes, and providing businesses with increased tax incentives for investment — as well as extending the 2001 and 2003 income tax cuts. CBO examined all of the options in terms of their expected effects on both economic growth and jobs.

CBO found that the option to extend the 2001 and 2003 tax cuts came in last.[7] Moreover, the option in question was to extend all of the 2001 and 2003 tax cuts, including those for middle- and lower-income families. In its report, CBO indicated that not only did this option come in last, but that if one divided this option into two options — extending the high-end tax cuts and extending the tax cuts for everyone else — the option to extend the tax cuts for high-income households would rate even lower.

This is because, as CBO explains, “the higher-income households … would probably save a larger fraction of their increase in after-tax income.” [8] The economic evidence is strong that upper-income people have a higher propensity to save additional income that they receive and a lower propensity to consume. As a result, channeling a dollar of federal revenue to them during a recession or economic slowdown is a very inefficient way to stimulate more consumer spending and to thereby spur economic growth and job creation.

Sounder Alternatives

The CBO findings also point the way toward much sounder alternatives for job creation and economic growth. Policymakers should allow the high-income tax cuts to expire on schedule and use the savings — for the first year or so — for policies that CBO found would have a much higher “bang-for-the-buck.”

- For example, CBO estimates that directing money to fiscal relief for state and local governments would generate two to three times the economic growth and job creation that extending the Bush tax cuts would have. The disparity between the economic effects of fiscal relief and that produced by extending the high-income tax cuts would be even greater.

- Mark Zandi, chief economist of Moody’s Economy.com, has reached similar conclusions.[9] In a recent summary table on “Job Creation Policies’ Bang for the Buck,” Zandi highlighted the one-year change in GDP for each dollar reduction in federal tax revenue or increase in spending for a range of economic stimulus proposals. Of the 17 policies that Zandi analyzed, extending the Bush tax cuts came in 14th. Only a few inefficient corporate tax cuts fared worse. (See Table 1.)

| Table 1: | |||

| Job Creation Policy Proposal | Bang for the Buck | ||

| Congressional Budget Office | Zandi | ||

| Low | High | ||

| Making Bush income tax cuts permanent | 0.10 | 0.40 | 0.32 |

| General aid to state governments | 0.40 | 1.10 | 1.41 |

| Increased infrastructure spending | 0.50 | 1.20 | 1.57 |

| Jobs tax credit | 0.40 | 1.30 | 1.30 |

| Note: “Bang for the Buck” is the estimated dollar change in GDP for each dollar reduction in federal tax revenue or increase in spending. CBO measures the cumulative effects on GDP over 2010-2015, while Zandi measures the increase in GDP at the end of the first year the policy is in effect. Sources: Mark Zandi, Economy.com; Congressional Budget Office. | |||

Misleading Claims About Small Business

Some proponents of extending the Bush-era tax cuts at the top have made small businesses the poster children for the effort to extend the high-end tax cuts. They seek to leave the impression that most small businesses pay the top rates — and that most people who pay the top rates are small businesses. Both impressions are belied by the evidence.

Most small businesses are just that — small. Their incomes are not high enough to face the top marginal rates. Allowing the two top tax brackets to return to their higher, pre-2001 levels would affect just 3 percent of taxpayers with business income, according to the Joint Committee on Taxation. Fully 97 percent of taxpayers with business income would be entirely unaffected.

Those making the small business claims also tend to rely on a definition of “small business” that substantially overstates the small business impact. [10] Most Americans would not describe the nation’s wealthiest 400 individuals, some of whom are billionaires, as “small businesses.” But, with lots of money to invest, these “Top 400” receive a fair amount of business income. In 2007 (the most recent year for which we have data), the Top 400 had nearly $17 billion in S corporation and partnership income — an average of $83 million each — according to the IRS.[11] In addition to the wealthiest 400 taxpayers, the following types of individuals also meet the commonly used definition of “small business”:

- partners in large corporate law firms;

- Wall Street bond traders who receive multi-million dollar bonuses and invest some of their income in an investment partnership; and

- wealthy executives who rent out their vacation homes (given that such rental income is filed under Schedule E).

To be sure, CBO notes that some small businesses would benefit from an extension of the current top tax rates because of this pass-through character. But, CBO pointedly rejects the proponents’ argument that Congress should extend the tax cuts because of their impact on job creation. CBO states: “increasing the after-tax income of businesses typically does not create much incentive for them to hire more workers in order to produce more, because production depends principally on their ability to sell their products” (that is, on consumer demand rather than on the level of the businesses’ profits).

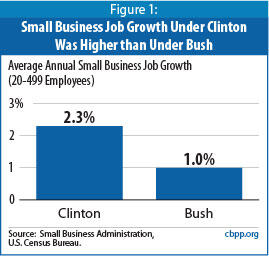

Recent history underscores CBO’s point. Small business employment rose by an average of 2.3 percent (756,000 jobs) per year during the Clinton years, when tax rates for high-income filers were set at the rates to which they are slated to return in 2011. During the Bush years, when tax rates were lower, small business employment rose by just 1.0 percent (367,000 jobs).[12] (See Figure 1.) The tax rates under Clinton were not a deterrent to a robust job-creating economic expansion, and the lower tax rates after 2001 did not prevent a subsequent prolonged jobless recovery.

Finally, as the analyses by both CBO and Zandi make clear, Congress can find much more efficient ways to help small business and spur job creation than through extending the current top income tax brackets. For example, CBO estimates that a job creation tax credit would create four to six times as many jobs per million dollars of revenue lost than extending the Bush income tax rates. The efficiency differential would be even more lopsided if a jobs creation tax credit were compared to extending the high-income tax cuts. Similarly, Zandi estimates that a temporary jobs tax credit would generate $1.30 of GDP for every dollar of tax credit cost, while extending the Bush tax cuts would generate just 32 cents on the dollar.

End Notes

[1] Tax Policy Center, Table T09-0306.

[2] CBPP calculations of savings over 2011-2020 based on OMB estimates from February 2010 ( http://www.whitehouse.gov/omb/budget/fy2011/assets/tables.pdf). The effects on the deficit include lower interest costs from reduced borrowing. President Obama’s other proposals to allow high-income tax cuts to expire include the proposed reinstatement of Pease and PEP and a 20 percent tax rate on capital gains and dividends for the specified income group.

[3] Avi Feller and Chad Stone, “Top 1 Percent of Americans Reaped Two-Thirds of Income Gains in Last Economic Expansion,” Center on Budget and Policy Priorities, September 9, 2009.

[4] “Suggestions for The State of the Union to Reduce Government Spending,” press release from the office of Senate Minority Leader Mitch McConnell, January 26, 2010.

[5] Peter Cohn, “Six Vulnerable Dems Urge Obama To Reconsider Increases,” Congress Daily AM, January 28, 2010.

[6] Congressional Budget Office, Policies for Increasing Economic Growth and Employment in 2010 and 2011, January 2010, available at http://www.cbo.gov/ftpdocs/108xx/doc10803/01-14-Employment.pdf.

[7] One other option — extending relief from the Alternative Minimum Tax — came in only marginally better than extending the 2001 and 2003 tax cuts.

[8] CBO, p. 25.

[9] Mark Zandi, “How to Fix the U.S. Job Market,” Nov. 30, 2009, available at http://www.economy.com/dismal/article_free.asp?cid=119773.

[10] A major data gap distorts the debate over the top tax brackets: the IRS does not publish specific and satisfactory tax information for small businesses. Instead, analysts are left to examine various sources of business income that individuals receive. Some analysts define any tax unit with any business income as a small business, overstating the number of such businesses, particularly among very high-income households. While the use of this definition of small business is understandable, given the lack of alternative definitions, it produces results that can be quite misleading. See Chye-Ching Huang and James R. Horney, “Big Misconceptions About Small Businesses and Taxes,” Center on Budget and Policy Priorities, Feb. 2, 2009.

[11] IRS, “The 400 Individual Income Tax Returns Reporting the Highest Adjusted Gross Incomes Each Year, 1992-2007,” p. 4, http://www.irs.gov/pub/irs-soi/07intop400.pdf.

[12] Jason Levitis and Chuck Marr, “History Contradicts Claim That President’s Budget Would Harm Small Business Job Creation,” Center on Budget and Policy Priorities, March 26, 2009.

More from the Authors