A Brief Analysis of the Congressional Budget Plan

President's Budget Priorities Move Forward

The budget resolution Congress adopted last week for fiscal year 2010[1] largely reflects the proposals in the preliminary budget President Obama submitted to Congress in February. Under the budget resolution:

- Deficits will be very high by historical standards in the next several years but will decline substantially by 2014. Over the 2010-2014 period as a whole, deficits will be $824 billion lower than if no changes were made in current policies.

- Congress will be free to consider legislation to implement President Obama’s proposals to reform health care, move toward energy independence and limit greenhouse-gas emissions, reform financial aid for higher education, and address other high-priority national needs.

- Congress can extend “middle-class tax cuts,” relief from the alternative minimum tax, and the current estate tax rules (which exempt the estates of 99.75 percent of people who die — 399 of every 400 — from paying any estate tax), rather than allowing these measures to expire as scheduled under current law.

- Total funding for nondefense discretionary programs, which has increased little in recent years, will grow modestly in real terms above the 2009 level but be about $10 billion below the amount the President requested. Funding for defense will be exactly at the level the President proposed.

The budget resolution is not a law and serves only as a blueprint for future tax and spending legislation. But the assumptions in the budget resolution have a significant impact on the shape of that subsequent legislation. These assumptions are detailed below.

Deficits

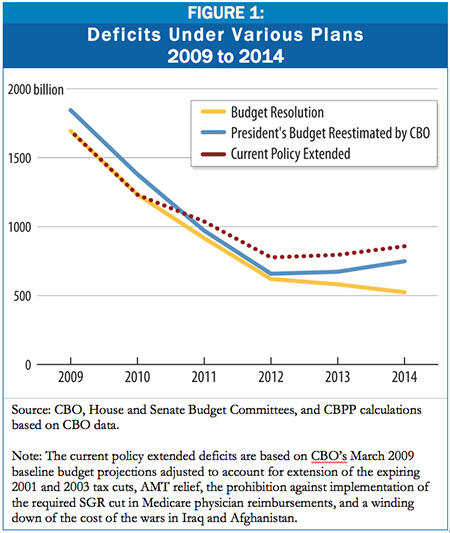

Under the budget resolution, deficits will decline from $1.7 trillion (12.0 percent of Gross Domestic Product, or GDP) in 2009 and $1.2 trillion (8.6 percent of GDP) in 2010 to $523 billion (3 percent of GDP) in 2014, the last year the budget plan covers. (See Figure 1.)

These deficits — fueled by the most severe recession since World War II and the near meltdown of the financial system — are very large by historical standards; relative to the size of the economy, this year’s deficit will be the largest since World War II. Even so, deficits in 2010-2014 will be $824 billion lower under the budget resolution than if current budget policies were left unchanged, and $555 billion lower than CBO’s estimates of the deficits over that period under the budget that President Obama submitted.[2]

Major Policy Changes

The congressional budget plan accommodates consideration of the President’s major proposals — health care reform, energy and climate change policies, and a number of other significant policy changes — with a series of deficit-neutral “reserve funds” and, in the case of health reform and changes in financial assistance for higher education students, the possibility of using the budget reconciliation process.

Deficit-Neutral Reserve Funds

The budget resolution includes 20 deficit-neutral reserve funds for the consideration of legislation in the House and 14 deficit-neutral reserve funds for the consideration of legislation in the Senate. A reserve fund allows the Budget Committee chair to adjust the budget resolution’s overall spending and revenue limits and the spending allocations for particular congressional committees to ensure that legislation accomplishing a reserve fund’s goal — such as “transform[ing] and moderniz[ing] America’s health care system — will not be subject to a procedural bar if it breaches those limits or allocations, so long as the legislation does not increase the deficit. This allows congressional committees to make tradeoffs between spending and revenues, as long as the committees pay for any increase in spending or reduction in revenues. [3]

The budget resolution includes deficit-neutral reserve funds in both the House and Senate for health reform legislation and legislation that would make changes in national energy policy and limit greenhouse-gas emissions. The budget plan does not specify what policies either house should adopt to achieve the desired outcomes — for instance, it neither endorses nor rejects the President’s proposed cap-and-trade system or his proposals for paying for health care reform. Instead, it leaves all of the details to the committees of jurisdiction, so long as the legislation they produce is deficit neutral.

The budget resolution also includes deficit-neutral reserve funds for a number of other initiatives proposed in the President’s budget, including reforming the student financial assistance programs to make college more affordable and strengthening child nutrition programs. [4]

Reconciliation

The budget resolution also facilitates consideration of the President’s proposals by including reconciliation instructions that Congress could use to help enact health reform and student financial aid legislation. Reconciliation is a process set forth in the Congressional Budget Act that allows for special consideration of legislation affecting mandatory programs or taxes. [5]

The reconciliation instructions in the new budget resolution direct three committees in the House (Energy and Commerce, Ways and Means, and Education and Labor) and two committees in the Senate (Finance and Health, Education, Labor, and Pensions) to report reconciliation legislation no later than October 15 of this year. The full House and Senate would then consider this legislation under special procedures, the most important of which is a limit on the time allowed for debate in the Senate. Under the Senate’s regular rules, 60 votes are needed to prevent a minority of senators from blocking legislation through a filibuster (i.e., by refusing to stop debating the measure), but reconciliation legislation cannot be filibustered. [6]

A budget resolution cannot require a committee to use reconciliation instruction for a specific purpose, [7] but the 2010 budget resolution makes clear that the reconciliation process is intended to be available this year for legislation concerning health care reform and student financial aid.

Democratic leaders in Congress have stated that committees should try to move health reform legislation through the normal legislative process over the next few months without using the reconciliation process, but that it is important to have reconciliation as a backup if a minority of senators tries to block consideration of a health care reform bill. A decision can be made in the fall about whether to use reconciliation for health reform or just for education legislation and, possibly, other matters within the jurisdiction of the reconciled committees. [8]

Tax Cuts

Under the budget resolution, total revenues over the 2010-2014 period will be $764 billion less than under current law. This is largely because the resolution assumes the extension of the “middle-class tax cuts” (the tax cuts enacted in 2001 and 2003, except for the reductions in the two top tax rates and several other tax-cut provisions that would affect filers with incomes over $250,000), as well as extension of alternative minimum tax relief and the 2009 estate tax parameters. Under current law, all of these measures are slated to expire.

The budget resolution assumes that the cost of extending those policies will not be offset by increases in other taxes or reductions in spending. [9] Although pay–as-you-go rules in the House and Senate require the cost of any tax cut or mandatory spending increase to be offset, the budget plan includes a provision enabling the House to consider legislation extending the assumed extensions without having to waive its pay-as-you-go rule. [10] No such provision applies in the Senate. The Senate would have to waive its pay-as-you-go rule (which requires the vote of 60 senators) to consider any tax or mandatory legislation that increases the deficit even if that legislation is consistent with the budget resolution.

In addition, the budget resolution includes deficit-neutral reserve funds that could accommodate additional tax reform and tax relief proposals, such as expanding eligibility for the refundable child credit, as long as they are paid for.

Discretionary Appropriations

The budget plan assumes that funding for discretionary programs in fiscal year 2010 — other than appropriations for unanticipated emergencies or for “Overseas Deployment and Other Activities” (the wars in Iraq and Afghanistan) — will total $1.086 trillion. Funding for defense activities other than Iraq and Afghanistan is assumed to total $556.1 billion, exactly the amount the President proposed. That level is $8.4 billion (or 1.5 percent) above the level provided in 2009, adjusted for inflation.

The total amount assumed for all other discretionary programs in 2010 — that is, all nondefense (international and domestic) discretionary programs — is $529.8 billion. That is $10 billion below the amount the President requested but $29.8 billion, or 6.0 percent, above the level provided for 2009 (excluding the recovery legislation), adjusted for inflation. [11]

It is impossible to know how Congress will distribute these funds among various nondefense functions and activities. A budget resolution simply sets the total amount of discretionary funding available for the year — it is up to the appropriations committees to determine how to allocate the funds among federal programs and activities. (The appropriators could decide to allocate less of the total to defense than the budget resolution assumes, but this seems unlikely, since the amount assumed for defense corresponds exactly to the President’s request.)

Budget resolutions do make assumptions about how discretionary funds should be divided among 17 budget “functions” (the 17 discretionary program categories in the budget). The assumptions that the budget resolution makes for how that funding should be divided among the categories (other than defense) are not very meaningful, however, because the resolution also assumes a $9 billion reduction in funding that is not reflected in these program categories. This means that the total funding shown for the 16 nondefense program areas (international programs and the 15 domestic program categories) will need to be reduced by $9 billion to conform to the total amount actually made available for all discretionary programs. [12] Thus, it is impossible to say what the budget plan actually assumes for international programs or for all domestic programs taken together, much less for any specific domestic program area.

For fiscal years 2011 through 2014, the budget resolution assumes larger reductions below the President’s requested levels for nondefense discretionary programs than the $10 billion reduction assumed for 2010. However, the figures for 2011-2014 are not binding; future budget resolutions will determine the amounts actually available for appropriations in those years.

End Notes

[1] See the “Conference Report to Accompany S. Con. Res. 13” (House Report 111-89):

http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=111_cong_reports&docid=f:hr089.111.pdf .

[2] The deficits assumed in the budget resolution are compared with what the deficits would be under the Congressional Budget Office’s March 2009 baseline budget assumptions, adjusted to account for extension of the tax cuts enacted in 2001 and 2003 and other temporary tax provisions, alternative minimum tax relief, and relief from scheduled cuts in Medicare payments to physicians, all of which are scheduled to expire under current law. For more details on the current-policy projections, see Paul N. Van de Water and Kathy A. Ruffing, “Obama Budget Reduces Deficit by $900 Billion Compared to Current Budget Policies,” Center on Budget and Policy Priorities, March 31, 2009, https://www.cbpp.org/sites/default/files/atoms/files/3-31-09bud2.pdf .

[3] For more detail on reserve funds, see James Horney, “An Analysis of the House and Senate Budget Plans,” Center on Budget and Policy Priorities, April 1, 2009, p. 8, https://www.cbpp.org/sites/default/files/atoms/files/4-1-09bud.pdf .

[4] The deficit-neutral reserve funds are contained in sections 301 through 334 of the budget resolution.

[5] Under House and Senate rules implemented when the Democrats took control of Congress in 2007, reconciliation cannot be used for legislation that would increase the deficit. Previously, it had been used in 2001, 2003, and 2005 for legislation that included tax cuts proposed by President Bush that increased the deficit.

[6] Since the motion to proceed to consideration of non-reconciliation legislation can be filibustered, it is sometimes impossible for the Senate to even begin consideration of legislation without obtaining 60 votes.

[7] The instructions simply call for each committee to report legislation that would reduce the deficit by $1 billion over the 2009-2014 period (to comply with the instructions, the savings should be no less than $1 billion). (The House instructions call for the Education and Labor Committee, which has jurisdiction over student financial assistance and some aspects of health reform, to produce deficit reduction of $1 billion. The statement of managers accompanying the conference report explains, however, that because of overlapping jurisdictions and the way that savings will be allocated among committees involved in health reform, the total savings assumed from the health reform legislation the reconciled committees produce is $1 billion.)

[8] Some opponents of the President’s proposal for a cap and trade system to limit greenhouse gas emissions have expressed fears that reconciliation could be used for such legislation, but Democratic leaders have indicated that will not happen.

[9] In the case of AMT relief, the plan assumes that any extension beyond three years will be paid for.

[10] For details on how the House provision works, see “An Analysis of the House and Senate Budget Plans,” p. 6. It is important to note that the House provision only takes effect if the House has passed legislation reestablishing a statutory pay-as-you-go rule or if the legislation being considered itself includes provisions that would reestablish pay-as-you-go rules in statute.

[11] For purposes of this comparison, the President’s request has been adjusted to be consistent with the Congressional treatment of obligation limitations on transportation trust fund spending and Pell Grant funding. See “An Analysis of the House and Senate Budget Plans,” footnote 7 on page 8.

[12] The reduction is reflected in “Function 920,” a function that contains no programs and can be used to include costs or savings that will be spread among various programmatic categories. The discretionary amount shown for fiscal year 2010 in Function 920 (in a table included in the conference report on the budget resolution) is actually a positive $1.351 billion, but that includes a $10.350 billion reserve for unanticipated emergency appropriations that will not be available to the appropriators for other purposes. Excluding that amount, the function has -$9 billion, or a $9 billion reduction in funding.

More from the Authors