Statement by Chad Stone, Chief Economist, on the July Employment Report

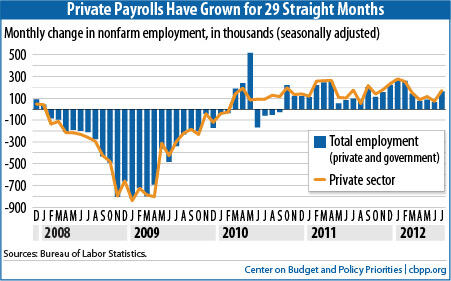

Today’s jobs report showing some pickup in job creation does not reduce the need for policymakers to implement measures to give the flagging recovery a needed boost, including preparing to extend emergency federal unemployment insurance (UI) past its scheduled expiration at the end of the year. Private employers have now added jobs for 29 straight months (see chart). But the overall pace of job creation remains modest, and jobs remain very difficult to find for large numbers of the unemployed — a situation that likely will persist for some time.

The economy shows no signs of generating a robust recovery. To the contrary, the Federal Reserve’s monetary-policy-making committee has again stated that it “expects economic growth to remain moderate over coming quarters and then to pick up very gradually” and “anticipates that the unemployment rate will decline only slowly.” Under those circumstances, the risk of inflation is low, enabling the Fed to pursue more aggressively the “maximum employment” goal of its dual mandate. On the fiscal side, temporary, well-targeted measures that inject new spending into the economy will boost economic growth and job creation without undermining efforts to stabilize the long-term budget deficit or creating financial market instability.

Unemployment insurance is one of the most cost-effective policies available for boosting economic growth and employment in a weak economy, and emergency federal UI has been an important source of support both for unemployed workers and their families and for the economy since mid-2008. The program, however, was scaled back in its latest reauthorization in February and is scheduled to expire altogether at the end of this year. Already, every state has “triggered off” the Extended Benefits (EB) program and the program will pay its last benefits in the last state (Idaho) next week. Starting in September, the number of weeks of Emergency Unemployment Compensation will fall.

The unemployment rate is expected to remain around 8 percent at the end of this year. Since policymakers first created a federal emergency UI program in 1958, they have never allowed it to end when unemployment topped 7.2 percent. Thus, it would be unprecedented if policymakers were to allow that to occur at year-end.

About the July Jobs Report

Job growth picked up in July, but a strong labor market recovery remains elusive.

- Private and government payrolls combined rose by 163,000 jobs in July, a significantly faster pace than in the prior three months. Private employers added 172,000 jobs, while government employment fell by 9,000. Federal employment fell by 2,000 jobs, state government employment fell by 6,000, and local government employment fell by 1,000.

- This is the 29th straight month of private-sector job creation, with payrolls growing by 4.5 million jobs (a pace of 157,000 jobs a month) since February 2010; total nonfarm employment (private plus government jobs) has grown by 4.0 million jobs over the same period, or 138,000 a month. The loss of 543,000 government jobs over this period was dominated by a loss of 392,000 local government jobs.

- Despite the 29 months of private-sector job growth, there were still 4.7 million fewer jobs on nonfarm payrolls in July than when the recession began in December 2007 and 4.3 million fewer jobs on private payrolls. Payroll job growth has averaged 151,000 over the year, and July’s 163,000 jobs are still well below the average of 252,000 jobs a month that the economy created in December through February (although warmer-than-usual weather played a role there by, for instance, allowing for more outside construction jobs).

- The unemployment rate edged up to 8.3 percent in July, and the number of unemployed Americans edged up to 12.8 million. The unemployment rate was 7.4 percent for whites (3.0 percentage points higher than at the start of the recession), 14.1 percent for African Americans (5.1 percentage points higher than at the start of the recession), and 10.3 percent for Hispanics or Latinos (4.0 percentage points higher than at the start of the recession).

- The recession and lack of job opportunities drove many people out of the labor force, and we have yet to see a sustained return to labor force participation (people aged 16 and over working or actively looking for work) that would mark a strong jobs recovery. In fact, the labor force shrank by 150,000 in July as the number of people with a job fell by 195,000 and the number of unemployed rose by 45,000. (These numbers come from a different survey, which shows more month-to-month volatility than the payroll job growth numbers.)

- The labor force participation rate (the percentage of people aged 16 and over working or looking for work) edged down to 63.7 percent; before the current economic slump, labor force participation had not been this low since 1983.

- The share of the population with a job, which plummeted in the recession from 62.7 percent in December 2007 to levels last seen in the mid-1980s and has been below 60 percent since early 2009, edged down to 58.4 percent in July.

- The Labor Department’s most comprehensive alternative unemployment rate measure — which includes people who want to work but are discouraged from looking (those marginally attached to the labor force) and people working part time because they can’t find full-time jobs — was 15.0 percent in July. That’s down from its all-time high of 17.2 percent in October 2009 in data that go back to 1994, but still 6.2 percentage points higher than at the start of the recession. By that measure, roughly 24 million people are unemployed or underemployed.

- Long-term unemployment remains a significant concern. Two-fifths (40.7 percent) of the 12.8 million people who are unemployed — 5.2 million people — have been looking for work for 27 weeks or longer. These long-term unemployed represent 3.3 percent of the labor force. Before this recession, the previous highs for these statistics over the past six decades were 26.0 percent and 2.6 percent, respectively, in June 1983.

# # #

The Center on Budget and Policy Priorities is a nonprofit, nonpartisan research organization and policy institute that conducts research and analysis on a range of government policies and programs. It is supported primarily by foundation grants.

More from the Authors