Joint Statement: The Developing Crisis — Deficits Matter

A Fiscal Crisis

A fiscal crisis is developing in the United States, and the risks of inaction are high. Without a change in current policies, the federal government can expect to run a cumulative deficit of $5 trillion over the next 10 years. Moreover, the fiscal situation will deteriorate markedly in the decades that follow, as the cost of the baby boomers’ retirement and health care needs consumes a rising share of the economy and the budget. Deficits over the next generation will dwarf the already large deficits the nation faces in the decade immediately ahead.

Failing to address the growing imbalance between federal commitments and available revenues means squandering the best opportunity we will have to get our finances in order before the aging of America makes our fiscal situation far more difficult. It means our generation will bequeath to future generations spiraling debt that will shrink economic growth.

But instead of expressing alarm, many in Washington now argue that escalating deficits do not really matter, that they are self-correcting, that they are unrelated to interest rates or future economic well-being, and that tax cuts will pay for themselves later by spurring economic growth. It would be wonderful if this were true. It is not.

There are no easy solutions to the fiscal challenge facing the nation. But policymakers — and the public — must begin now to confront honestly the difficult trade-offs that are required to restore a sustainable fiscal policy.

The Likely Budget Path Under Current Policies

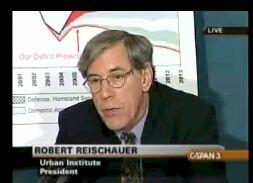

The baseline budget estimates issued by the Congressional Budget Office in August 2003, which cover the period 2004-2013, project a deficit of $480 billion in 2004 and a cumulative 10-year deficit of $1.4 trillion. As CBO itself is quick to point out, however, the “official” baseline projection is constrained by rigid rules. These rules lead the baseline to understate, by large amounts, the likely size of future deficits. For example:

- Official projections do not reflect the future costs of a number of policies currently in effect. In particular, CBO is required to assume that all tax cuts enacted since 2001 will simply be allowed to “sunset,” or expire, as called for by current law.Image

- Nor do the official projections include the costs of new policies that are very likely to be enacted, such as a Medicare prescription drug benefit.

- Official projections also assume that appropriations will grow only at the rate of inflation over the next 10 years. Yet there certainly will be faster growth in such areas as defense and homeland security, and probably in some domestic programs as well.

Our organizations have prepared an alternative, more realistic, projection that we believe provides policy makers with better insight into where current policies are leading us. Our projection starts with the official CBO baseline, but adjusts it to reflect a more realistic set of policy outcomes.

Specifically, it assumes that the expiring tax cuts will be extended and relief from the Alternative Minimum Tax continued, that a prescription drug benefit costing $400 billion over ten years will become law, that the Administration’s multi-year defense plan will be fully funded, and that domestic non-defense programs will keep pace with inflation and population growth.

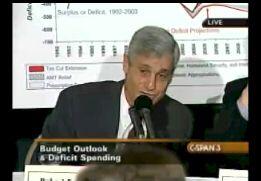

The figures below represent our joint estimate of the budget path the government now is following. They show a deficit of more than $500 billion in 2004 and a cumulative 10-year deficit of $5 trillion. They also show a non-Social Security deficit of $687 billion in 2004 and a 10-year non-Social Security deficit of $7.4 trillion.

| Adjustments to CBO Deficit Projections | |||||||||||

| 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | Total | |

| CBO August projections | -480 | -341 | -225 | -203 | -197 | -170 | -145 | -9 | 161 | 211 | -1,397 |

| Tax cut extension | 3 | -60 | -117 | -127 | -128 | -136 | -141 | -287 | -413 | -447 | -1,854 |

| AMT relief |

| -11 | -31 | -43 | -56 | -71 | -90 | -109 | -129 | -154 | -693 |

| Prescription drug plan | -7 | -10 | -34 | -42 | -49 | -55 | -62 | -68 | -75 | -88 | -491 |

| Defense, homeland security, & international | -40 | -13 | -9 | -9 | -15 | -29 | -41 | -60 | -86 | -92 | -395 |

| Domestic appropriations except homeland security | 1 | -1 | -5 | -9 | -13 | -18 | -23 | -29 | -35 | -42 | -172 |

| Resulting deficit projections | -523 | -436 | -423 | -433 | -457 | -478 | -501 | -561 | -577 | -611 | -5,002 |

| Notes: Negative values indicate deficits or costs that increase the deficit, while positive values reflect surpluses or policies that reduce the deficit. All figures include both the policy’s direct costs and the extra interest it causes. | |||||||||||

Rather than cutting the deficit in half in five years, as projected in CBO’s baseline, the more likely path under current policies is an increase in the deficit over this period. Policy makers could — and badly need to — alter this path. But we do not yet see any evidence that they will.

How Does This Level of Deficits Compare with Past Deficits?

If these budget projections are borne out, the coming decade is likely to rank as the most fiscally irresponsible in our nation’s history.

Even assuming the economy recovers and the costs of operations in Iraq shrink, we project that the federal government is on track to run sustained deficits equal to about 3.4 percent of the size of the economy. With only one exception, the federal government has never run deficits of this size except during times of global depression or full-scale war. The exception is the 1980s and early 1990s, when deficits averaged roughly 4 percent of the size of the economy.

The fact that the federal budget ran large deficits in that period offers little comfort because the situation in the 1980s and early 1990s was very different from the situation today. For one thing, as the Cold War drew to a close, Congress was able to shrink the deficit through large reductions in discretionary spending, particularly for defense. A parallel situation is not present today. More importantly, in the 1980s, the retirement of the baby-boom generation was still a generation away. Today, with the first boomers due to start collecting Social Security in five years, it is just around the corner. We consequently face a much more difficult fiscal situation than we did twenty years ago.

Moreover, when large deficits emerged in the 1980s, a national consensus quickly developed that these deficits were not self-correcting and needed to be addressed. Policy makers worked hard for 15 years to craft revenue-raising and expenditure-reducing measures to erase the deficits. No similar consensus exists today. We run the risk that we will waste this decade’s opportunity.

This Is Not a Self-correcting Problem

If the current budget deficit were a self-correcting or passing phenomenon, it would not be a cause for alarm. But that is not the case.

The long-term deficits we are facing are of such magnitude that the economy cannot possibly "grow out of them," a message that comes across clearly in the reports of institutions such as the General Accounting Office and the Congressional Budget Office. For economic growth to close the gap, productivity would have to increase — for decades on end — at levels far above what GAO, CBO, Administration economists, or private economists believe will occur.

Even over the short term, strong economic growth alone will not be enough to close the gap. CBO’s projections already assume a robust recovery in 2004, with real GDP growing at 3.8 percent, and an average annual growth rate of 3 percent through 2013. (These CBO economic projections are the ones we have used in developing the $5 trillion deficit estimate.) Economic growth is unlikely to be significantly higher than this. Annual real GDP growth has averaged 3 percent since 1970.

To get a sense of the magnitude of the deficits the nation is likely to face without a change in policies, consider that even with the full economic recovery that CBO forecasts and a decade of economic growth, balancing the budget by the end of the coming decade (i.e., in 2013) would entail such radical steps as: raising individual and corporate income taxes by 27 percent; or eliminating Medicare entirely; or cutting Social Security benefits by 60 percent; or shutting down three-fourths of the Defense Department; or cutting all expenditures other than Social Security, Medicare, defense, homeland security, and interest payments on the debt — including expenditures for education, transportation, housing, the environment, law enforcement, national parks, research on diseases, and the rest — by 40 percent. Beyond the next decade, the trade-offs become even more difficult. These mounting deficits represent a daunting challenge that we are yet to confront.

What Happened to the Surplus?

Less than three years ago, the Congressional Budget Office (CBO) projected cumulative budget surpluses of $5.6 trillion for the 2002-2011 horizon. Our assessment of current budget policy indicates the nation is now poised to run deficits over this entire period, totaling about $4.4 trillion. (The $5 trillion figure referred to above is for the period 2004 – 2013.) After adjustments to ensure comparability, this change represents a negative swing in the nation’s expected fiscal position of more than $9 trillion in just 32 months.

Overall, tax and spending legislation enacted since 2001 accounts for 65 percent of the more-than-$9 trillion decline in the surplus for 2002 – 2011 under our projections. Changed assumptions account for the remaining 35 percent. More than one-third of the decline can be attributed to tax cuts, with this share rising over time. Nearly one-third of the decline is attributable to new expenditures, the majority of which are for defense and homeland security.

Over the past three years, the economy has grown more slowly than anticipated, and this has had an important effect on the budget in the short term. But large deficits are expected to persist long after the economy has made a full recovery from the 2001 recession. In other words, our deficit problem is structural, not cyclical. It results from a growing mismatch between what Americans are scheduled to pay to government and what they expect government to deliver in return.

Ramifications of Large Chronic Deficits for Future Increases in Income and Living Standards, and for Government Finances

Deficits matter. Over the long term, large, persistent deficits absorb national savings and crowd out productive investment. They put upward pressure on interest rates. They reduce the fiscal flexibility to deal with unexpected developments. And they raise the cost of servicing the national debt.

One of the most worrisome effects of today’s large projected deficits is that they threaten to squeeze out important government programs — for the young and the old, for infrastructure and education, for national defense. These deficits would drive up the national debt by large amounts. As a result, an increasing share of tax collections would have to be diverted from supporting needed programs to paying interest on the mounting debt. Under current policies, interest costs — which currently consume less than nine percent of tax revenue — will consume 15 percent of federal revenue by the end of the decade and much more in subsequent decades. We project that interest payments on the debt will reach $470 billion a year by 2013.

What Do These Deficits Mean for Future Generations?

A major demographic shift is nearly upon us. We are an aging society, and as we age, the declining share of the population that is made up of workers will have to support the retirement and health needs of the growing wave of baby-boom seniors. This demographic shift will place unprecedented strains on the budget.

As a nation we have yet to confront the difficult trade-offs this will require. Certainly, there is wide room for debate on how best to ease the fiscal challenge that future generations will face. But adding to that challenge by running up the national debt over the next decade is not among the responsible options.

Because the demographic transition is entirely predictable, we have no excuse for failing to account for it in our fiscal policies. If we were to save more now — in part by running budget surpluses once the economy recovers — we could generate the resources to help meet part of the “age wave’s” future cost. But instead, we are squandering the opportunity to do so by pursuing policies that will run up more debt just as we are nearing the start of this new and difficult period. In the end, our children will have to face higher taxes, reduced public services, or both. But if we wait until the crisis is upon us, the solutions will be more draconian.

Restoring Fiscal Responsibility

For 20 years, there was bipartisan consensus in Washington that large and rising budget deficits were damaging. The budget debate — from the Tax Equity and Fiscal Responsibility Act of 1982 to Gramm-Rudman in 1985, the Budget Agreement of 1990, the 1993 Clinton budget proposal, and the 1997 Balanced Budget Agreement — was often rancorous, but it was based on the shared goal of shrinking the large, damaging deficits that loomed.

Today, that consensus has evaporated. The absence of responsibility is widely shared: the Administration fails to acknowledge the relationship between its fiscal choices and our long-term future; Democratic alternatives tend to ignore the long-term mismatch between our commitments for retirement, health, and security on the one hand and the revenues available to pay for them on the other hand.

The Center on Budget and Policy Priorities, the Committee for Economic Development , and the Concord Coalition are joining to issue this call to action. Our failure to act responsibly on federal deficits is endangering our future and our children's future.

Today, as we are about to enter a new budget year, we urge in the strongest possible terms that our leaders begin work on a realistic plan for putting the nation’s fiscal house in order as the economy fully recovers. All options should be on the table. Such a plan, to be credible, must also include budget enforcement mechanisms — at a minimum, the “pay-as-you-go” rule for taxes and entitlements that proved effective in enforcing fiscal discipline through much of the 1990s. Finally, as a first step, Congress and the President must act immediately to stop “digging the hole deeper.”